Macroeconomist @IIF. Sci-Fi Lover. Bolivian. jfortun@iif.com

Joined May 2018

- Tweets 1,713

- Following 2,498

- Followers 5,723

- Likes 3,695

1,002 Photos and videos

Jun 7

Bolivia is being read abroad as another EM reform story.

Subsidies. Protests. IMF. Lithium. Bonds. Investor patience.

All relevant.

But not enough.

The old political order lost the presidency, but it did not leave the operating system.

That is where the story turns darker.

Stuck in the Loop, Part IV

The Country They Keep Misreading

linkedin.com/pulse/stuck-loo…

1

185

May 21

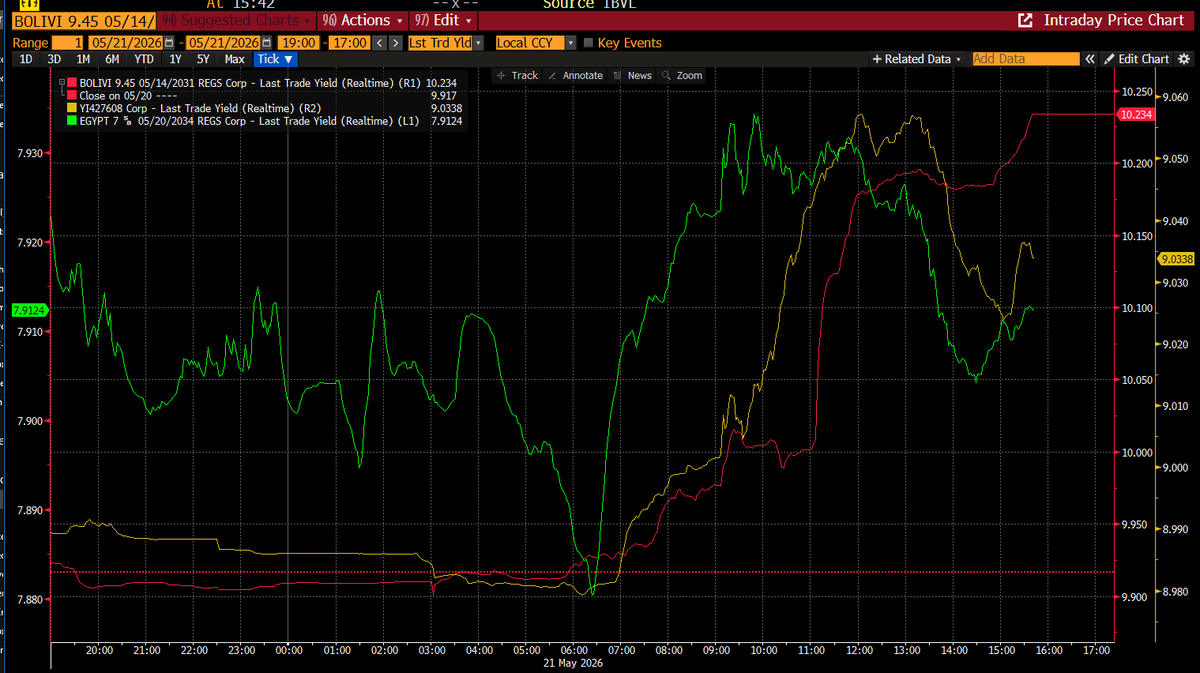

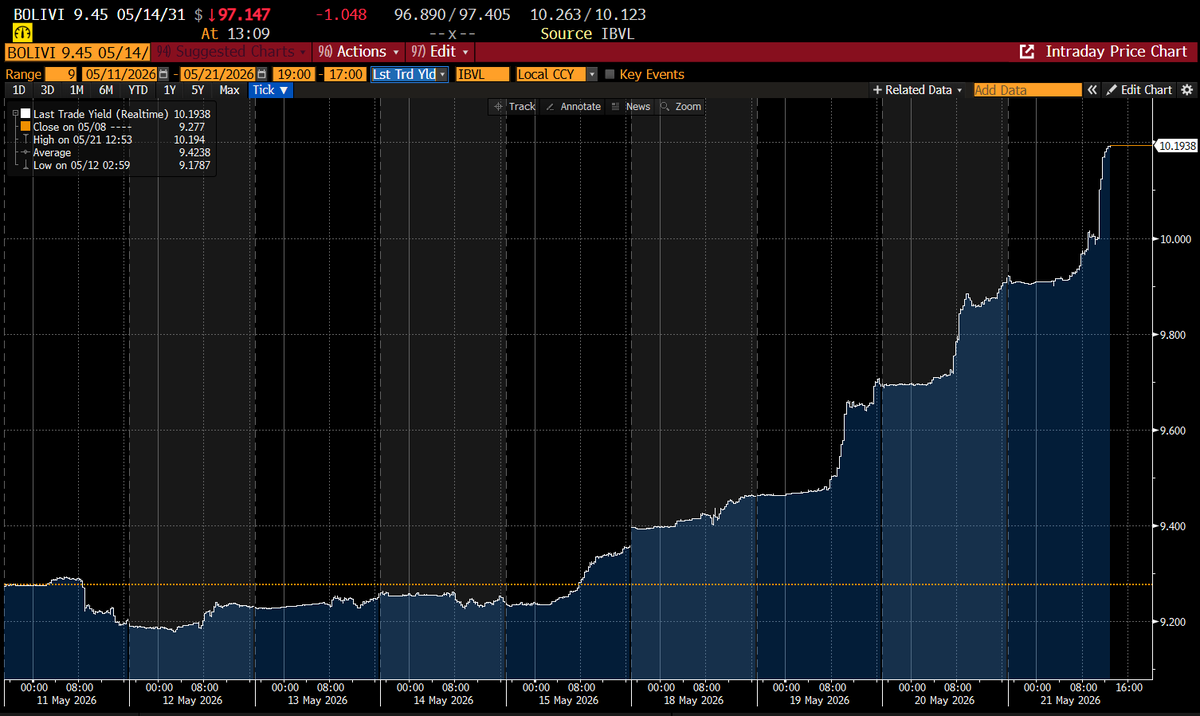

Bolivia’s new 2031 bonds did not even get a honeymoon.

Issued at a 9.75% yield, they are already trading above 10.1%. That is the market’s way of saying the optimism around fresh external financing is conditional, fragile, and reversible.

The problem was never just access. It was credibility.

Bolivia managed to reopen the door, but investors are already asking whether the adjustment program behind that access is politically durable enough to matter. In a country still trapped between FX scarcity, fiscal stress, fuel subsidies, and weak governability, a new bond can

buy time.

It cannot buy confidence.

3

1

4

623

May 19

La Paz is tense before the IMF program has even arrived.

That is the warning. Bolivia has market access, but not stabilization. The streets are moving, inflation is still high, banks are hedging, and the old political machinery was never fully removed.

Stuck in the Loop Part 3: The Market Opened, the Streets Closed linkedin.com/pulse/stuck-loo…

2

199

May 8

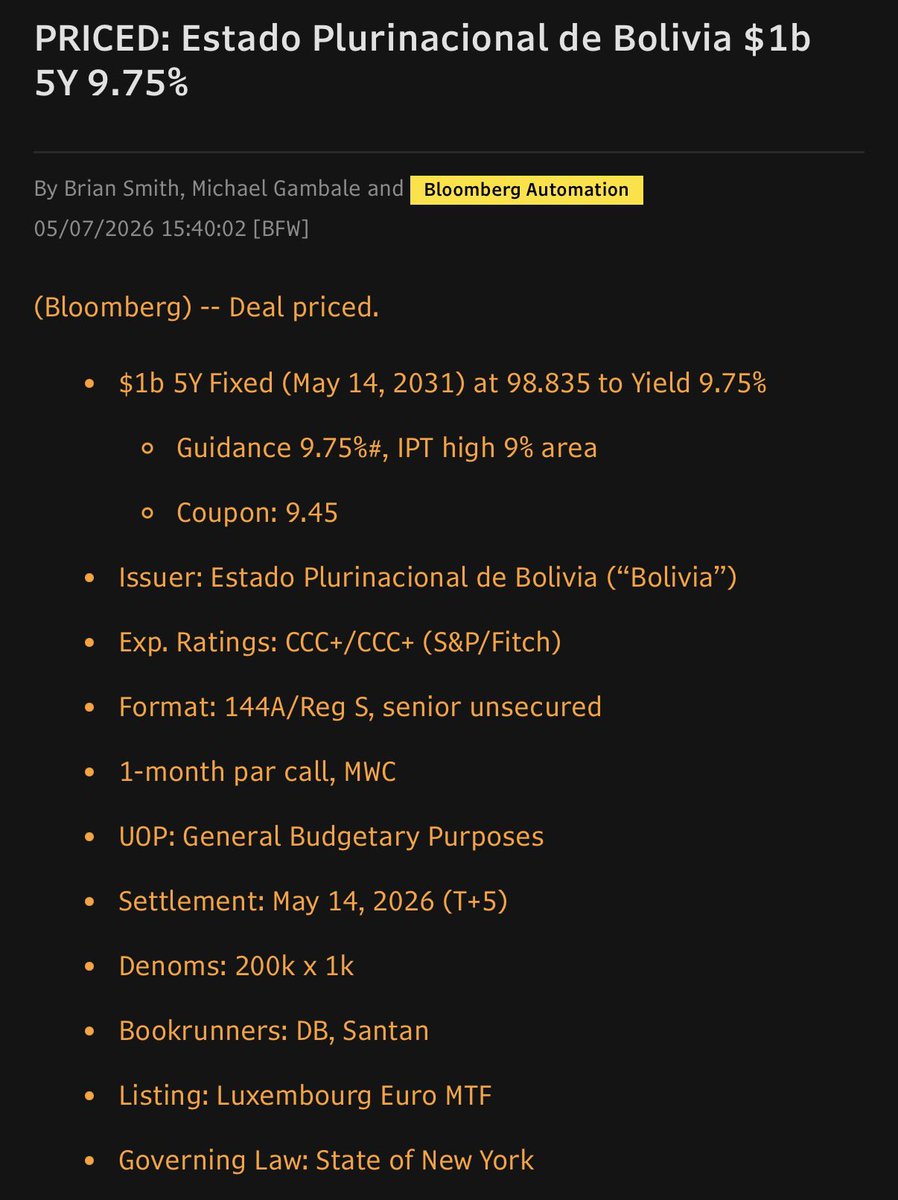

Bolivia just issued USD 1bn in 5Y debt at 9.75%.

The signal is mixed.

Authorities are also seeking up to USD 3.3bn from the IMF. Normally, stressed sovereigns try to secure the IMF anchor first, then return to markets with lower uncertainty. Ecuador is the cleaner comparison: IMF framework first, stronger market access after.

Bolivia seems to be doing part of that sequence backwards.

Pricing also matters. The target was reportedly closer to 9%. Final yield came at 9.75%. Oversubscription helps the headline, but demand at a high coupon is not the same as restored confidence.

Then maturity. Five years is short. Côte d’Ivoire placed longer dated paper in 2024, including roughly 9Y and 13Y maturities. Ecuador also managed longer maturities once the IMF story was more anchored.

So yes, Bolivia reopened market access. But this still looks more like expensive bridge financing than clean normalization.

1

3

12

1,746

Apr 21

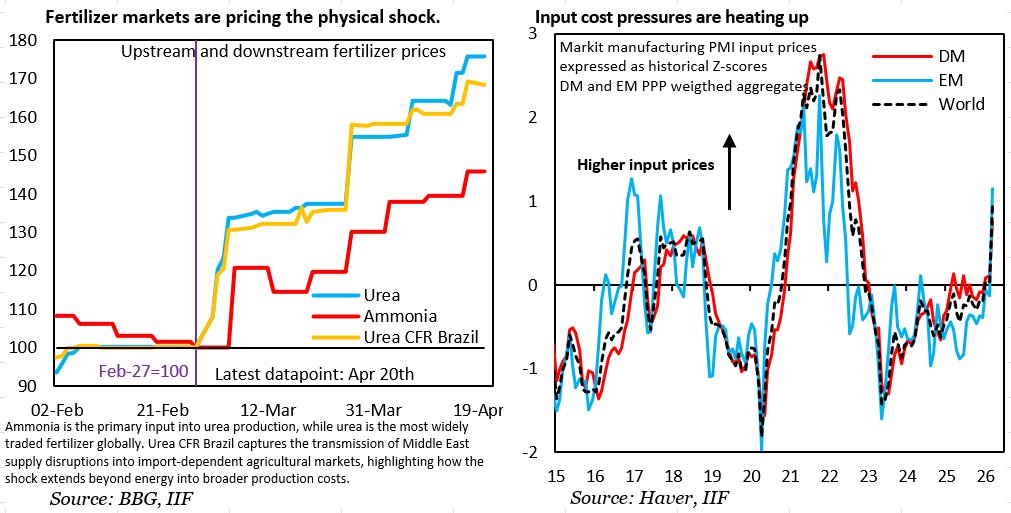

The key question is no longer just where oil settles. It is whether the shock is starting to spread into inputs, fertilizers, and supply chains more broadly.That is what looks increasingly likely.If so, the next phase is not really about relief. It is about transmission.And once that process gets going, inflation becomes much harder to bring down.

1

1

3

281

Apr 8

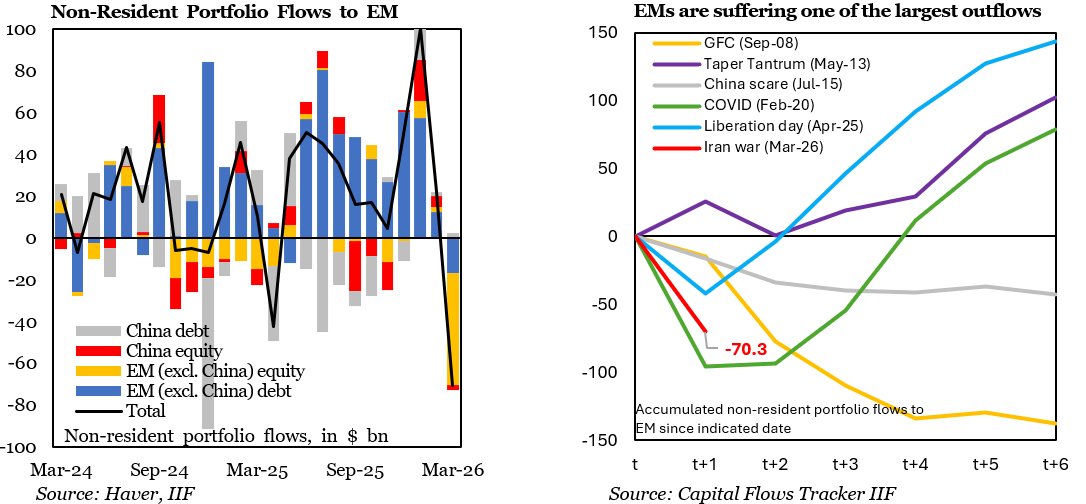

EM flows just had one of their worst months since the pandemic.

And it came in the first month of the Iran war.

March saw ~ $70 bn in outflows. Not a drift. A break.

So far this is an equity liquidation story, not a full funding stop. But that is how these episodes begin.

A truce may stabilize things.

But with this kind of on and off risk, the real shift is rising variance.

And that is where accidents happen.

2

6

522

Jan 7

The most dangerous moment in a stabilization is not the shock. It is the calm that follows.

Bolivia has lifted fuel subsidies. Protests are starting, the government is negotiating, and markets have already moved on. Spreads have compressed. Market access suddenly looks imaginable again.

That is exactly when bad sequencing becomes tempting.

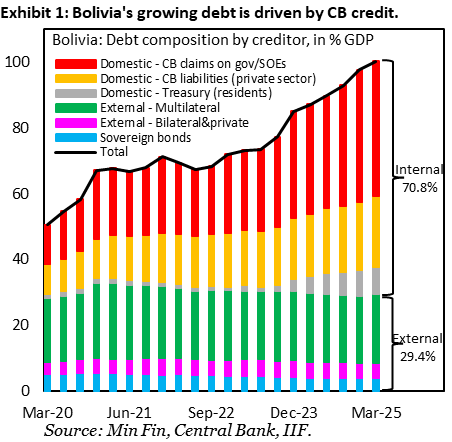

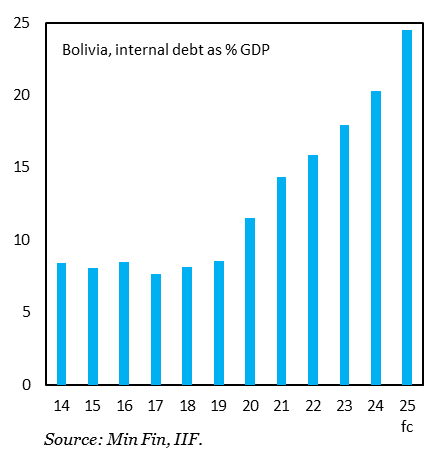

In Stuck in the Loop, Part II, I look at why this moment feels like progress and why it is not. How market appetite can return before the macro regime is fixed. Why Bolivia’s debt composition matters more than the headline ratio. And why low reserves turn “going back to markets” into a much harder problem than it appears.

This is the second entry in a time-loop series on Bolivia’s recurring adjustment cycle. Same country. Different cast. The same structural trap around timing and escape.

The danger is not that Bolivia cannot borrow.

The danger is that it can.

Link below.

linkedin.com/pulse/stuck-loo…

2

222

22 Dec 2025

Bolivia is debating fuel subsidies again.

The arguments are familiar.

What’s being missed is timing.

December is not neutral. Activity is already peaking, pass-through is faster, and expectations shift immediately. The same reform lands very differently depending on when it’s done.

Bolivia has seen this movie before.

Stuck in the Loop, Part I: December Is Not Neutral

linkedin.com/pulse/stuck-loo…

2

261

18 Dec 2025

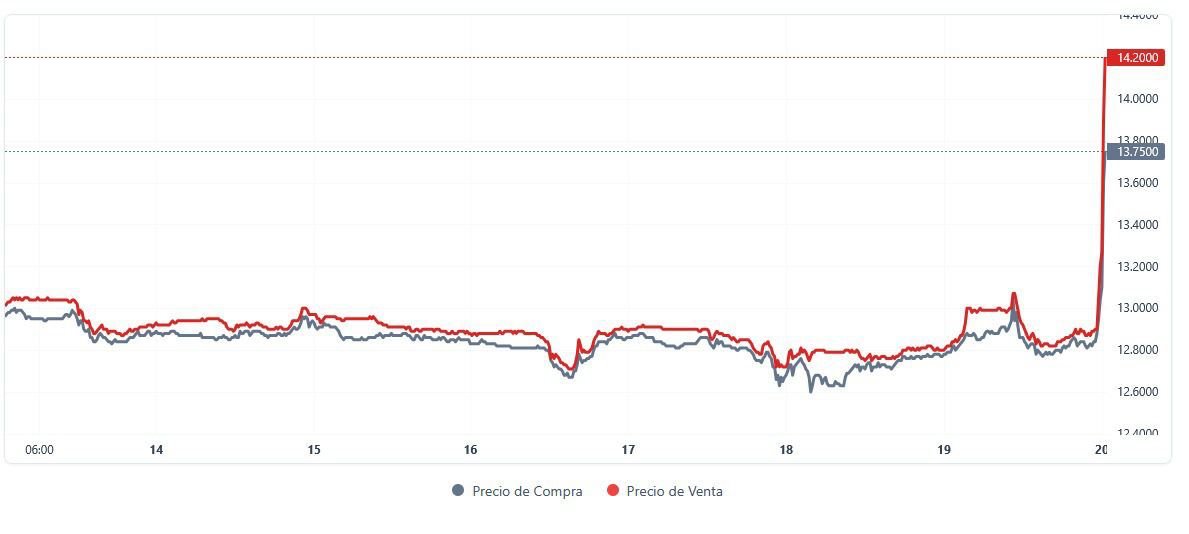

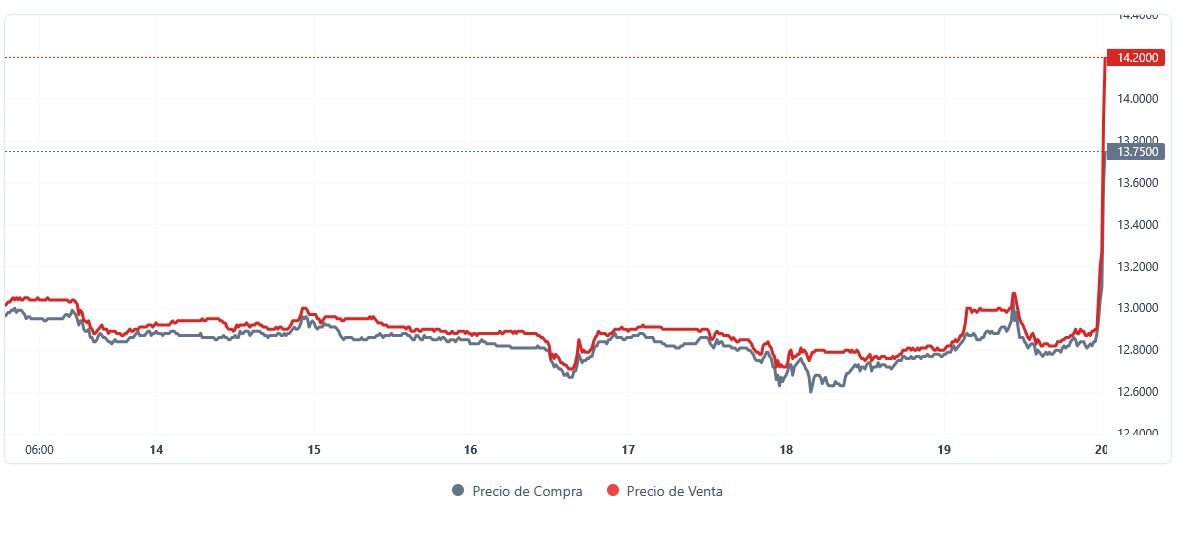

Bolivia just lifted fuel subsidies. This is a structural break, not a marginal adjustment.

From a macro perspective, it was unavoidable. The subsidy regime had become fiscally corrosive and a major source of FX leakage. But timing matters. This comes days before Christmas, with a new government that has not yet accumulated political capital, and with subnational elections ahead.

The immediate market reaction was predictable. The parallel dollar moved sharply, in the 9–11 range. Inflation pass-through is not a question of if, but how large and how fast. The decree itself acknowledges this risk, but expectations will be formed in real time by households and firms.

What happens next will depend on execution and politics. Social response over the coming days, credibility of compensatory measures, FX management, and internal cohesion within the government will matter as much as the policy design.

I’ve written a first-read analysis with my initial impressions and what I’ll be watching closely as this plays out.

LinkedIn article here 👇

linkedin.com/pulse/bolivias-…

1

6

246

18 Dec 2025

This is the executive order itself that frames the overall policies taken today (in spanish) slideshare.net/slideshow/el-…

166

10 Nov 2025

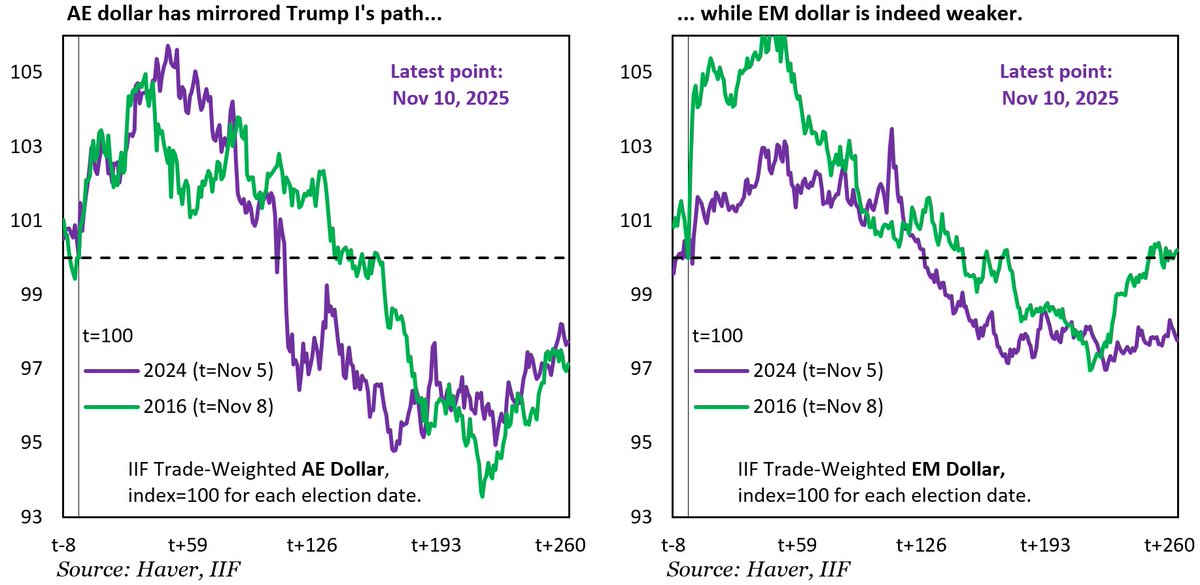

Two dollars, one story.

The AE dollar has weakened, but no more than it did under Trump I... nothing extraordinary.

The EM dollar is weaker still, as EM currencies quietly regain ground.

The dollar isn’t collapsing, it’s evolving.

2

284

23 Oct 2025

Quoted in @business on Bolivia’s macro path after the election of Rodrigo Paz. The fiscal hole is immense. Adjustment is no longer optional, only a question of speed and disruption.

The government may resist the optics, but in my view they will need to turn to the IMF.

Fresh off winning Sunday’s election, Bolivia’s next president Rodrigo Paz is blazing a rare centrist path out of his country’s economic crisis, focusing on practical policies over ideological divisions engulfing its neighbors bloomberg.com/news/articles/…

2

7

601

20 Oct 2025

Rodrigo Paz has won Bolivia’s presidency with 54.5% of the vote. But the fiscal hole exceeds 16% of GDP, fuel subsidies are unsustainable, and his economics team is fractured. The crisis is already unfolding. Read my latest take here: linkedin.com/pulse/bolivias-…

2

3

260

20 Oct 2025

The tiny Bolivian market welcoming the newly elected president Paz. Complete lack of credibility in his economic plan

2

227

13 Oct 2025

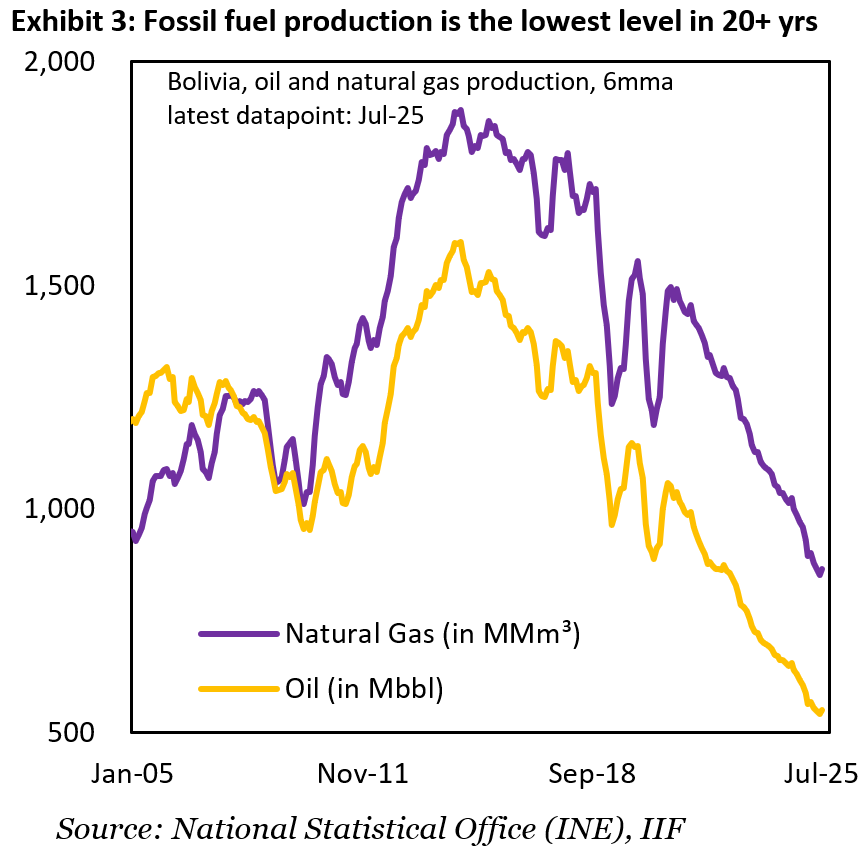

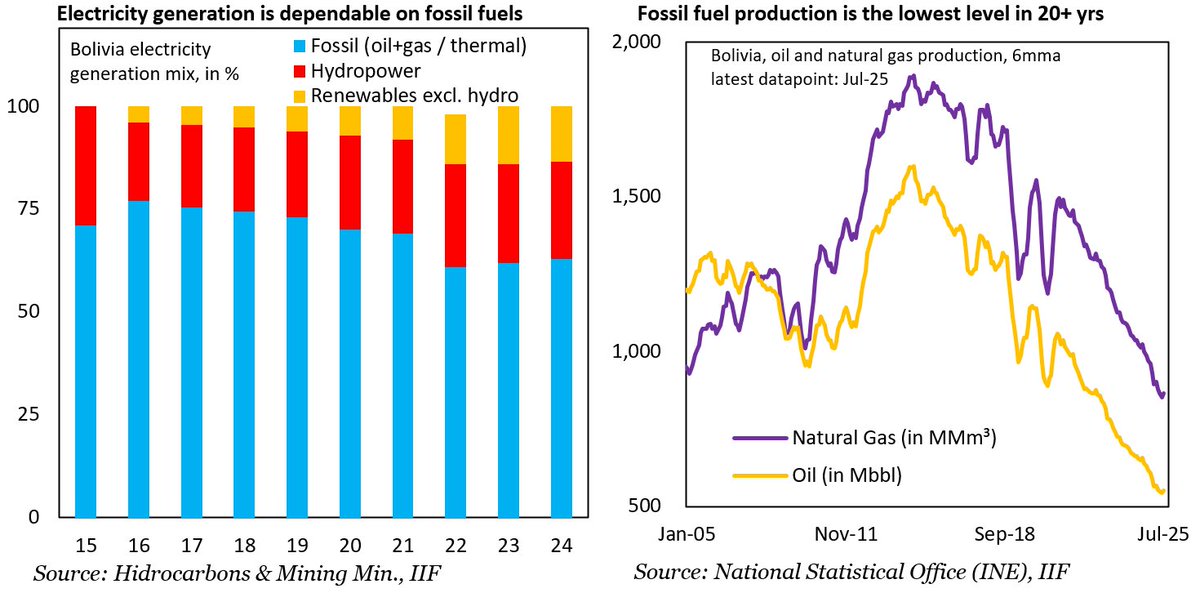

Bolivia está a 7 días del balotaje, pero la próxima crisis ya comenzó. No es inflación ni deuda. Es energía. El gas se acaba. El diésel es impagable. La red eléctrica está al límite.

Parte V de la serie Zombie: La Frontera del Apagón linkedin.com/pulse/bolivias-…

1

2

322

12 Oct 2025

Bolivia is T-7 from a runoff but the next crisis is already here This one is not about inflation or debt It's about energy. Gas is running out. Diesel is unaffordable. The grid is exposed. Blackouts are coming

Bolivia Apocalypse V: The Blackout Frontier

linkedin.com/pulse/bolivias-…

1

1

3

616

Jonathan Fortun retweeted

10 Oct 2025

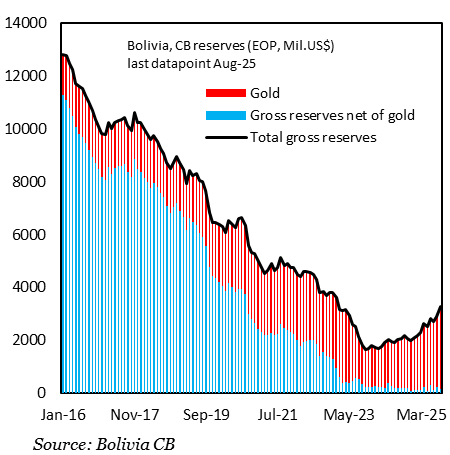

El Instituto de Finanzas Internacionales (IIF) advirtió que el modelo económico de Bolivia se ha agotado, con un modelo de financiamiento agotado, reservas mínimas y déficit persistente, según reportó Bloomberg

brujuladigital.net/economia/…

2

1

3

545