Price Action. Futures. Options. Algos.

Joined December 2019

- Tweets 3,420

- Following 660

- Followers 967

- Likes 2,142

1,248 Photos and videos

Pinned Tweet

4 Oct 2024

Get this free Trading Journal Notion template to easily log your trades and review them during your commute or spare time.

👉edge-slave.lemonsqueezy.com/

1

9

1,656

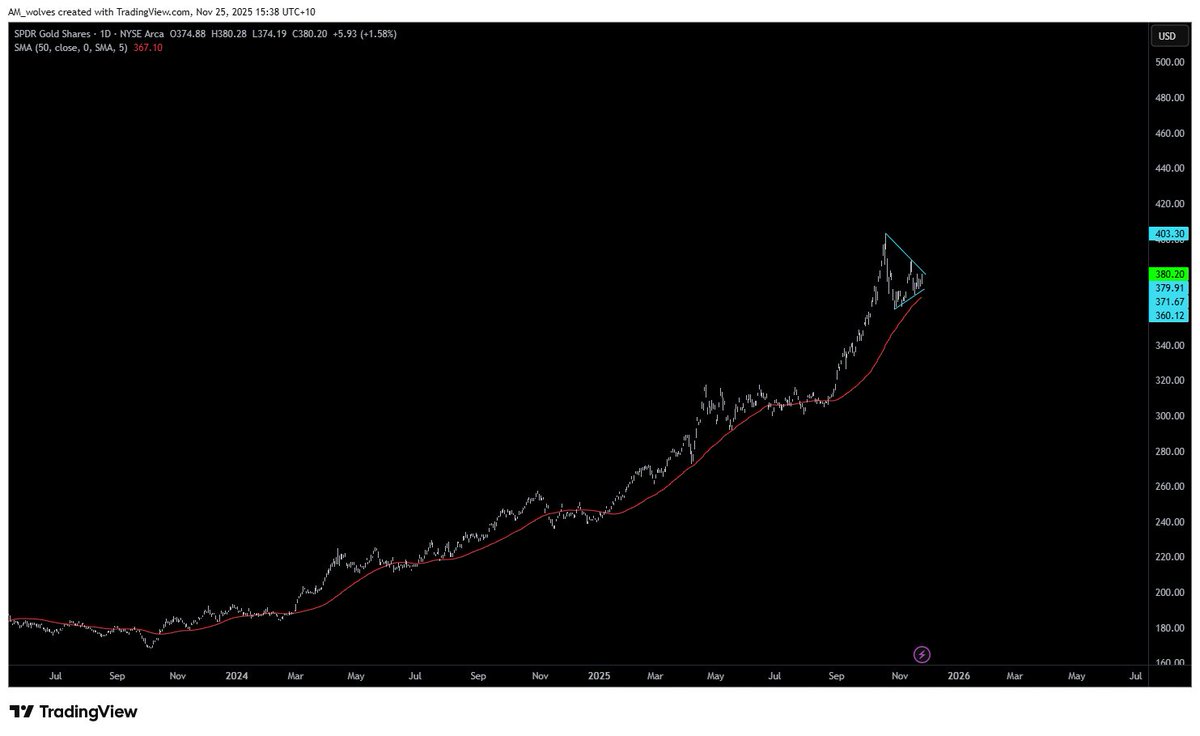

25 Nov 2025

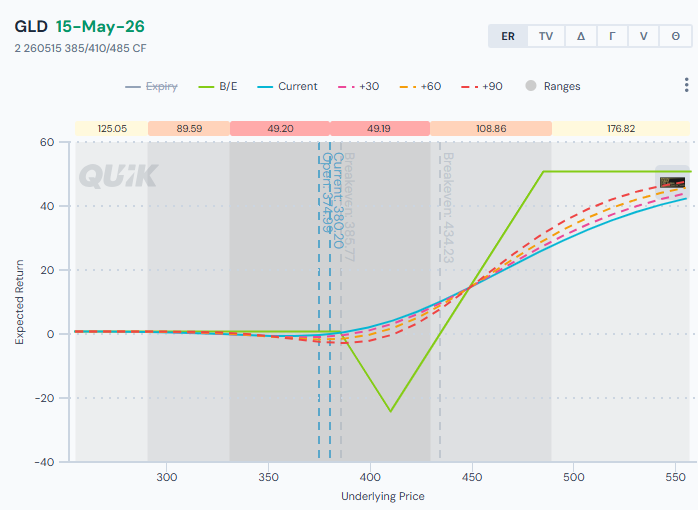

GLD; bet is for breakout to the upside. Flat if wrong and rolls over. Risk is falling in the belly

171

13 Nov 2025

Not losing money for not seeing what you want to see to get in trade is a win in my book. No PA wanted => no trade

1

104

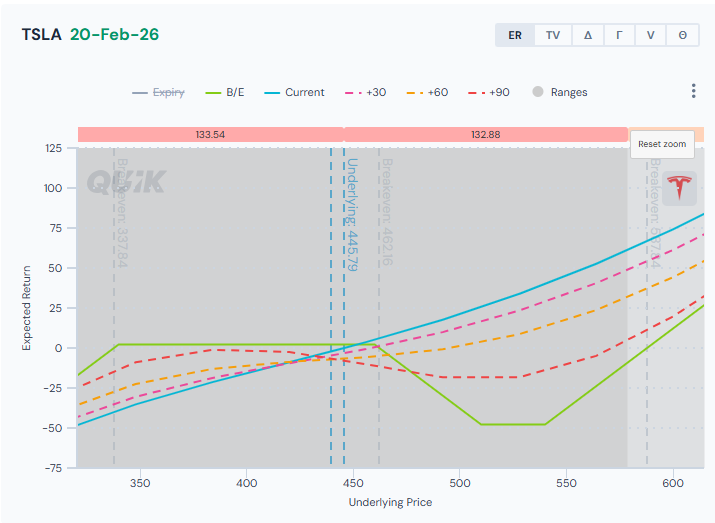

11 Nov 2025

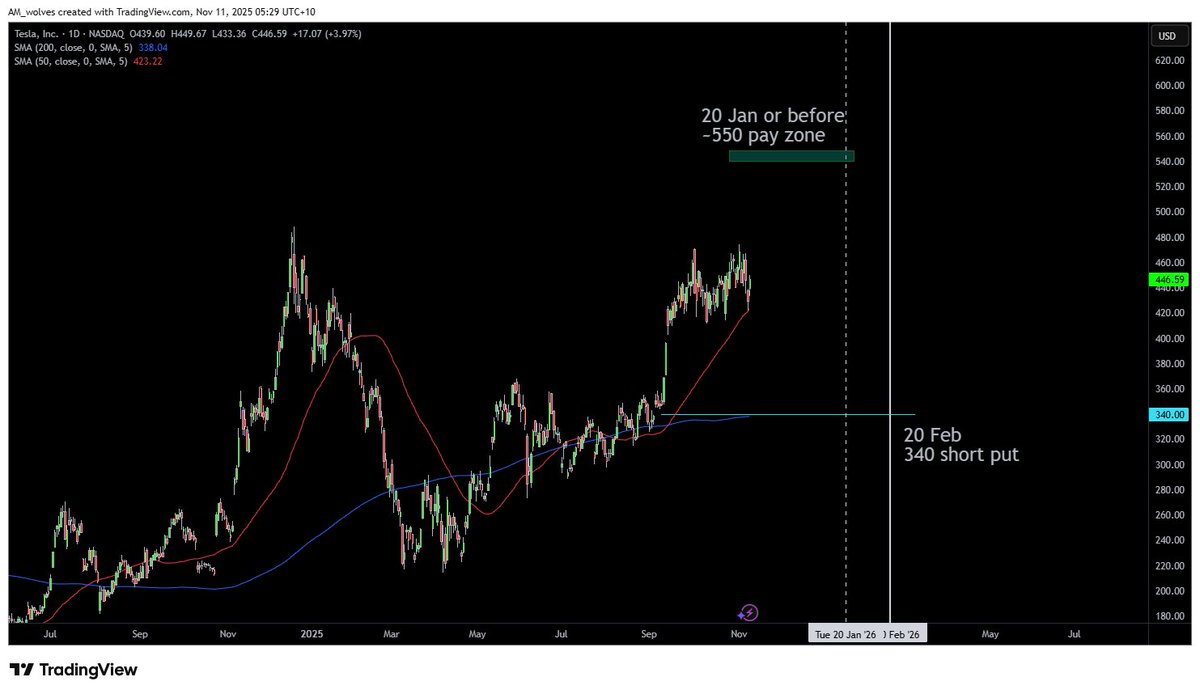

#Tesla @quikoptionsguru Anticipating range breakout... If it breaks down instead, enough room to the short put. Adjust strikes so spread is put for a minor credit

2

208

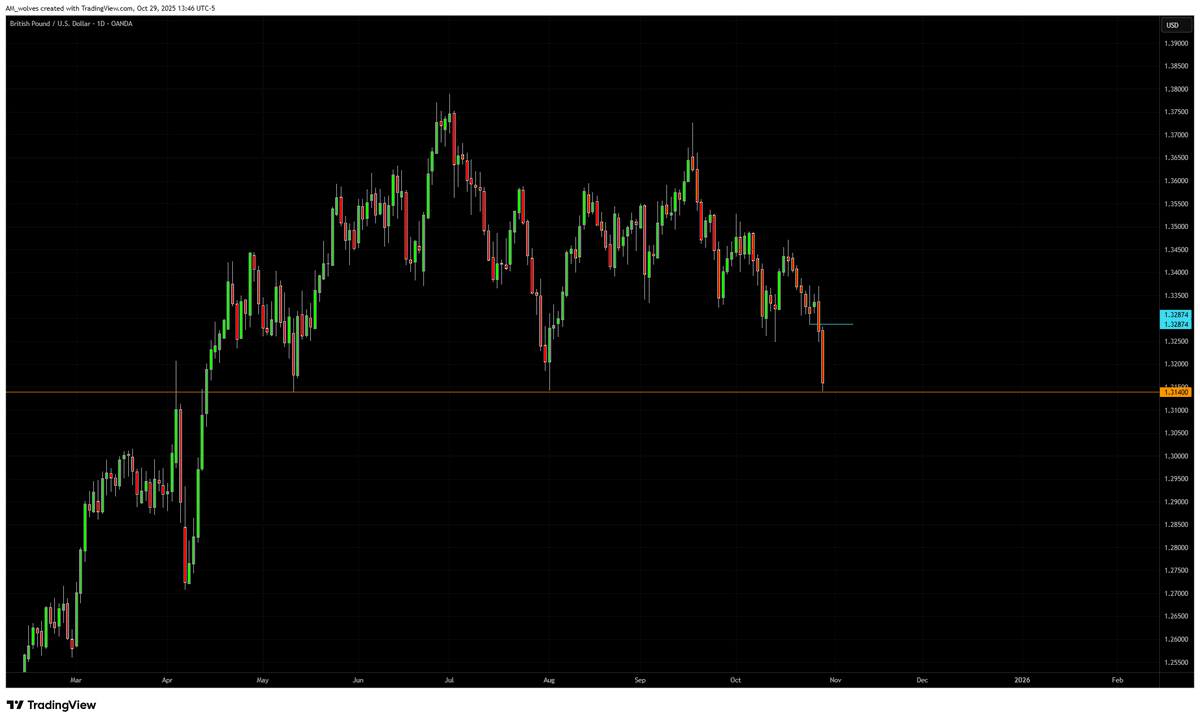

29 Oct 2025

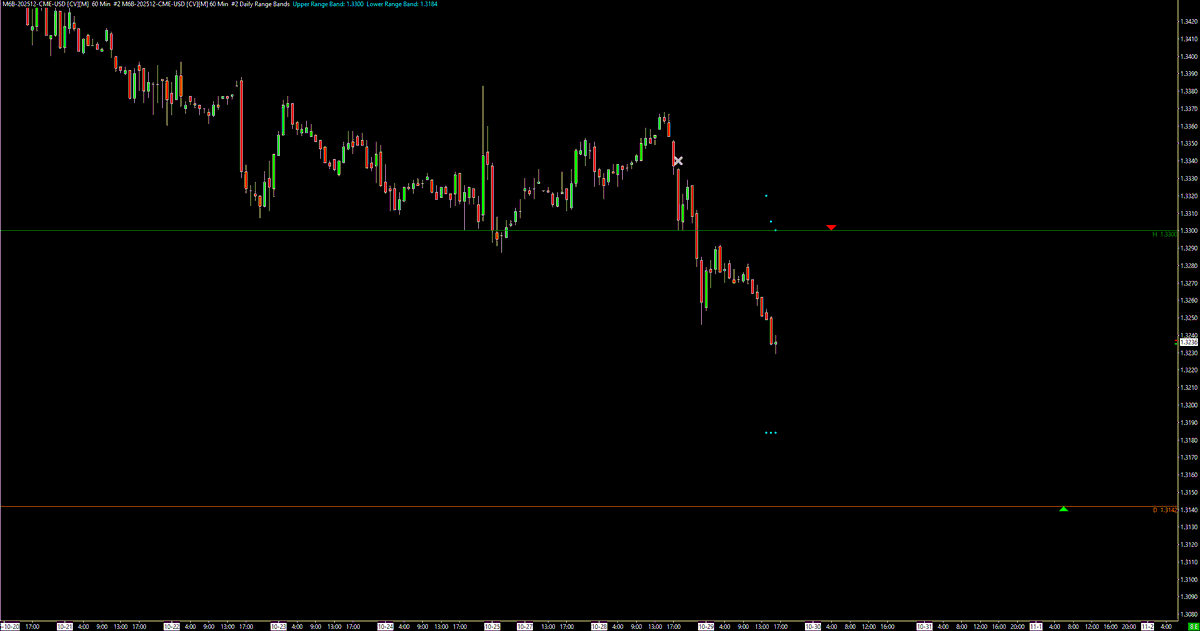

GBP... Looks heavy on the daily... wanting to go for a probe for 1.315. Offering that last swing low, naked on the H1, confluence with ATR, for a good R:R proposition

1

265

23 Oct 2025

ES. If this H1 resistance is broken up, long for a liquidity probe at ATHs

1

3

219

24 Oct 2025

Thesis still in play. Wait for bullish PA in prior resistance which must now prove to hold as support

1

113

24 Oct 2025

Target ATH probe. Thesis right, but didn't see what I wanted to see to get in. No trade

1

87

17 Oct 2025

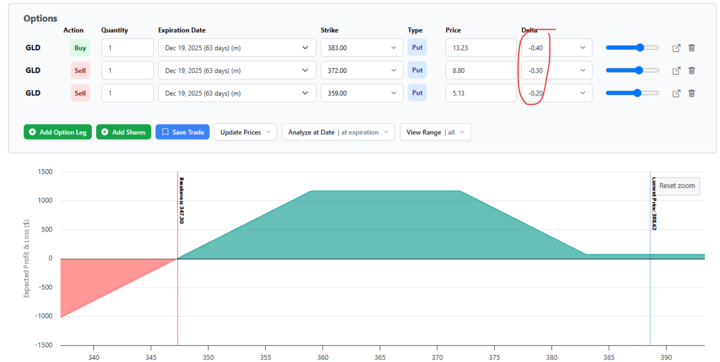

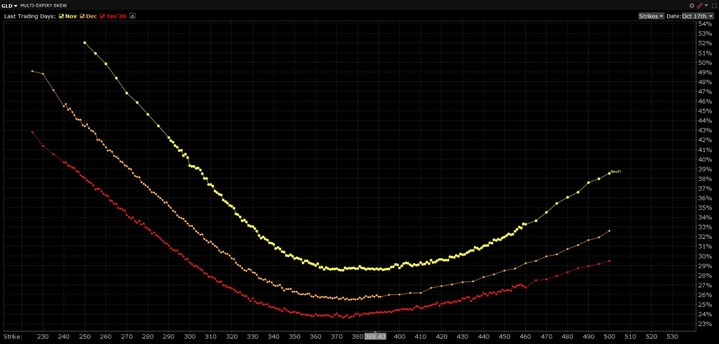

GLD. After parabolic run, bet is for correction/consolidation.

Buy an OTM put, and fund it by selling two farther OTM puts, to profit from put skew which as made the wings expensive:

1

1

151

17 Oct 2025

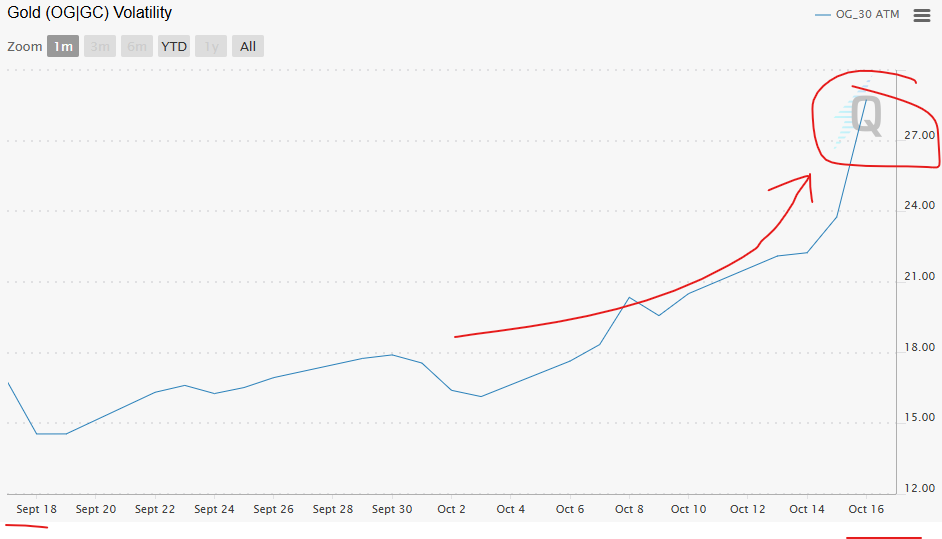

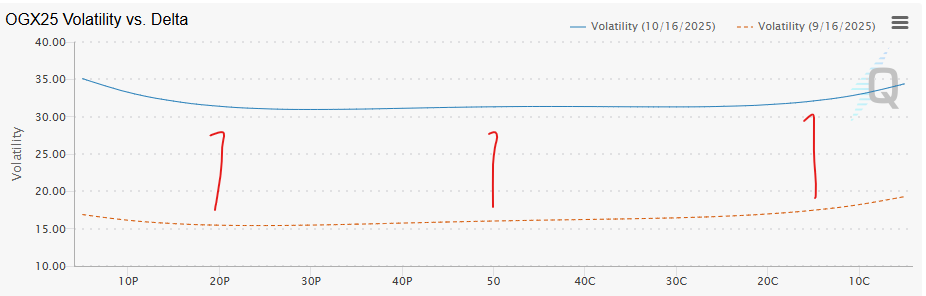

Gold 30d ATM IV & skew today vs 1 month ago. Rather sell vol

1

140

17 Oct 2025

Hi @optioncharts_io Any plans to add:

1) Time lines on P&L expiration diagrams; T0, T 10d, T 20d, etc.

2) Option to lock in a spread and simulate spread and leg value changes for changes in underlying, IV, time?

1

1

141

17 Oct 2025

Hi @optioncharts_io . Any plans to add:

1) Vol skew vs delta, not strike

2) Vol skew at different times (I don't mean for diff expirations, but same expiration but at different times; today, vs 1 week ago, vs 1 month ago)?

1

105

16 Oct 2025

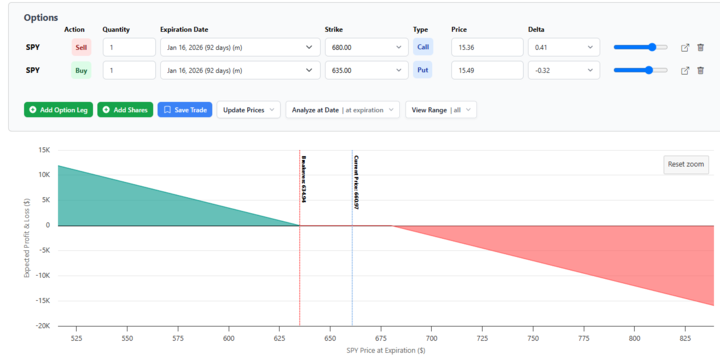

Portfolio hedge.

Ok, I am long overall in many portfolios, pension, etc.

Market is looking a bit shaky

1

1

139

16 Oct 2025

Depending on portfolio size is the number of options needed for [partial] protection.

The call strike is chosen arbitrarily (discretion). I think 680 will cap the market short term. The put strike is chosen so the call pays for it, ie neutral or a for net credit.

1

123

16 Oct 2025

The idea is, if the market corrects/crashes, the long put protects us. If the market resumes rally, we're long the portfolio so the short call doesn't hurt us. If SPY breaks up through the call strike (680), this would be a stop loss for the spread.

110

16 Oct 2025

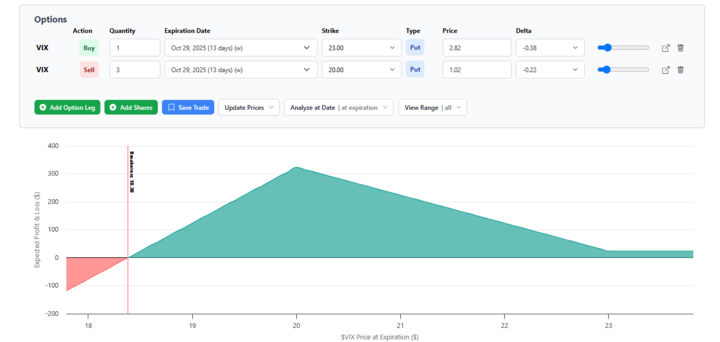

If market crashes and VIX flies, I'm safe on the right hand side of the spread structure. If VIX reverts, I'd look to exit at VIX=20. Quick time decay and VVIX reversion help this position

86