Private investor. I analyze structural bottlenecks in AI infrastructure, space, and defense. I post the work and take positions when the opening is there.

Joined March 2009

- Tweets 2,774

- Following 504

- Followers 2,250

- Likes 1,282

91 Photos and videos

Pinned Tweet

Jun 12

$APRTEC is a Swedish thermal management company validated in space by NASA and ESA, with a global tech customer integrating its EHD technology into chip-level product development.

Every watt of AI compute becomes heat. In 3D-packaged chips that heat is trapped inside the package, and rack-level cooling cannot reach it. The solution requires a pump small enough to operate at microchannel scale with no moving parts. Mechanical pumps have a physical lower bound on miniaturization. Electrohydrodynamic conduction pumps do not.

APR has spent 15 years developing EHD micropumps for highly demanding thermal environments, including spacecraft qualified by ESA and NASA. Space qualification imposes reliability requirements that are among the most demanding in any industry and are generally more stringent than those found in commercial data center environments. An unnamed global tech company has now integrated APR’s EHD pump into its product development and placed a pilot production order. That moves the relationship beyond pure evaluation.

The confirmatory event is a volume order from the tech customer. It would move APR from a component in a competitive cooling layer to a potential node in near-chip thermal management.

Risks:

•The tech customer remains unnamed and the volume decision is not yet taken. The relationship could stall.

•APR’s space and defense channel runs through ZIHET, which controls production, distribution and customer relationships. The economics accruing to APR remain uncertain.

•Core EHD conduction pumping is prior art from 2003. Patent protection covers specific implementations, not the principle. A well-funded competitor could develop an alternative path.

Position:

Long, small and a volume order from the tech customer would materially change the size of this position.

4

4

11

1,915

$SPCX. The question is not whether it is a great company. It is when you get paid.

SpaceX has built what is arguably the strongest competitive position in aerospace, with a near-monopoly in reusable heavy launch and a dominant LEO constellation in Starlink. The open question is when a public shareholder actually gets paid, and the filing answers it more honestly than the price.

At around $2.1T, $SPCX trades near 112x revenue. The only profitable segment is Starlink, roughly $4.4B in operating income. Launch appears to generate lower economic returns than Starlink and is increasingly used to support internal demand. The AI segment is consuming capital at a pace that likely exceeds $30B annually. You pay a monopoly multiple for one profitable network alongside a lower-return launch business and a capital-intensive AI segment.

History sets the base rate. Seven of the ten largest US IPOs of the past decade were underwater a year later. Didi fell 84%, Rivian 64%. Facebook spent over a year below its offer price before it became a great investment.

The timing sits in the lockup. There is no single 180 day wall. After the Q2 report in late July, 20% of insider shares unlock, then 7% tranches roll for months, then 28% more after Q3. Up to 2.4B shares, roughly 4.3x the float, become sellable within 90 days. That supply lands while index funds are forced to buy $SPCX into the Nasdaq 100. Musk himself is locked until June 2027.

My framework suggests a buy zone around $35 to $55. There you pay 30 to 50x Starlink forward EBITDA and the AI segment is free, which is where I value it until compute leasing becomes a revenue line instead of a cost line.

No position. This is a wait. What gets me long is a price in that zone combined with one fundamental confirmation: either stabilising Starlink ARPU or compute leasing proving it can become a meaningful revenue stream.

1

130

22h

$VRT has added $75B in market value over the past 12 months.

The market has decided cooling is infrastructure.

What it hasn't decided yet is which part of the cooling problem is actually solved.

This article maps the thermal stack and where value may migrate next.

It's also why I'm long $SHT and $APRTEC.

1

1

12

2,674

Jun 12

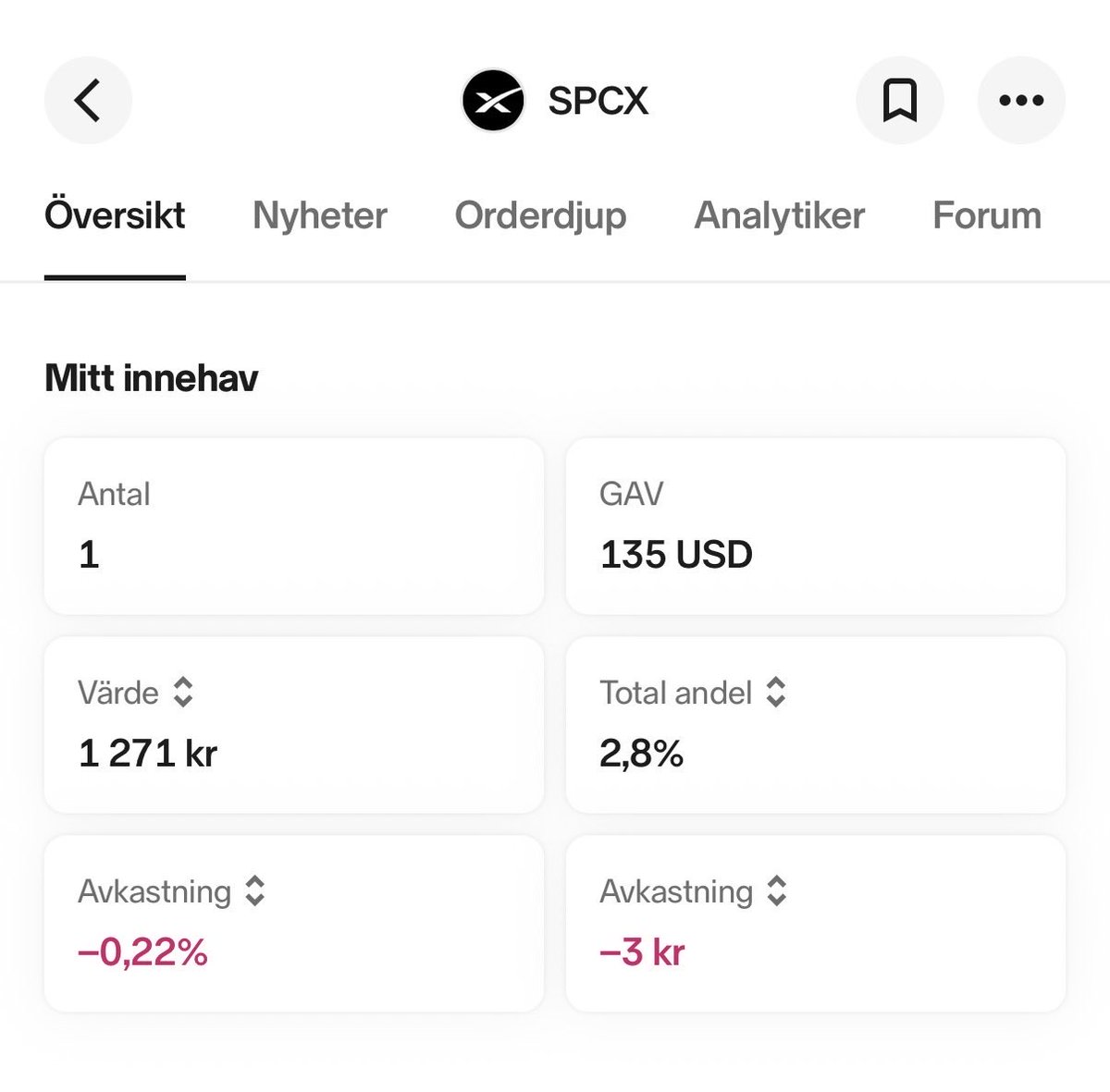

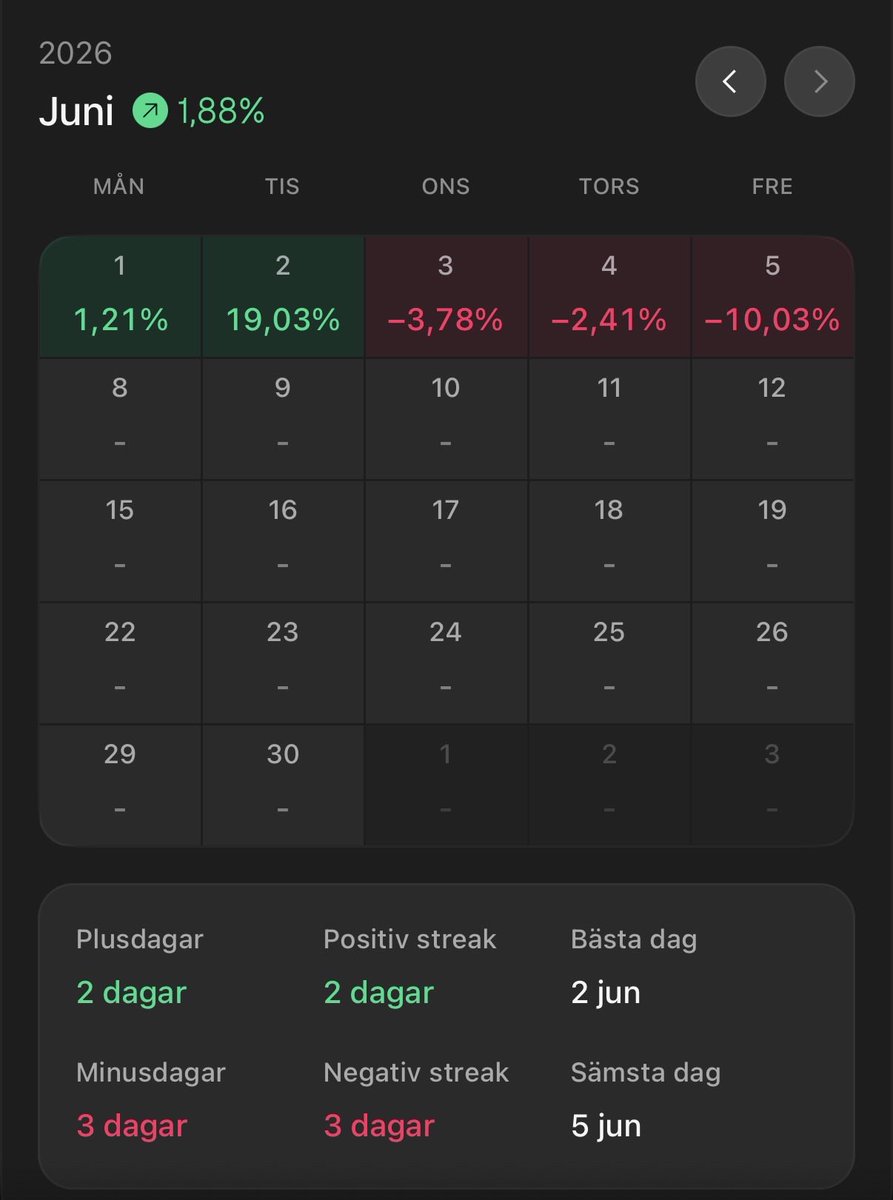

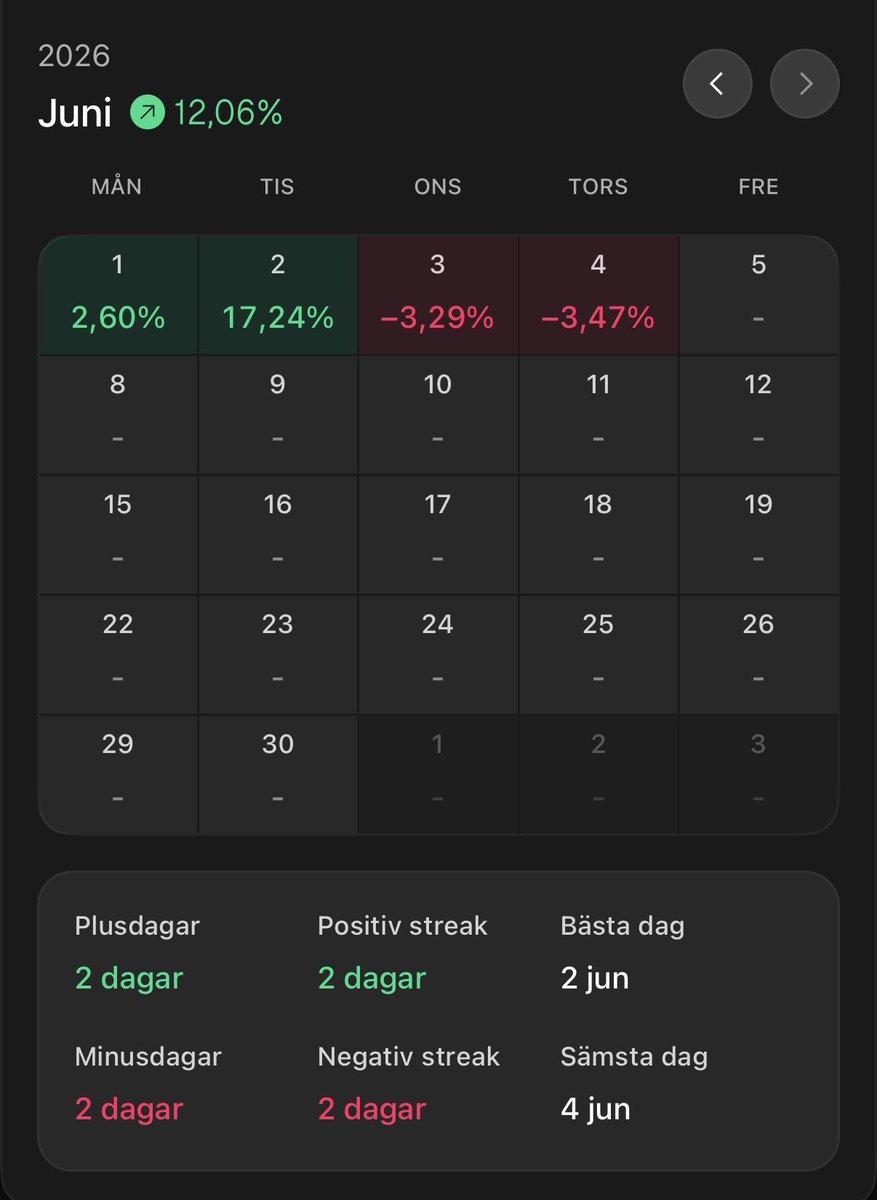

My $SPCX position is now officially established.

One share.

Retirement is imminent. 🚀😄

3

1

12

1,198

Jun 11

I’ve had a good run with $LPK, but last week I decided to watch from the sidelines and wait for a new trigger.

That trigger came sooner than I expected.

The thesis on glass replacing organic substrates is as relevant as ever.

Happy to be back.

Jun 11

Just thought this was interesting: $LPK is an unknown SpaceX supplier.

You can find it in SpaceX US import logs.

It's fun information discovery ahead of Space'x IPO this week. Though, not sure what the exact contract entails.

Disclosure: I have positions in LPK, NFA, credit to my follower Albert_TheVoid for the DM!

Especially since everyone seems to be talking about about SpaceX with Velo...

Just a fun, new direct relationship between $LPK and SpaceX if people want to do more digging.

1

21

3,658

Jun 10

I’ve always struggled with taking profits.

Why sell a winner?

But step by step, I’m learning that taking some profits from winners may be smarter than selling temporary underperformers, only to watch them rip the next day.

So today I practiced.

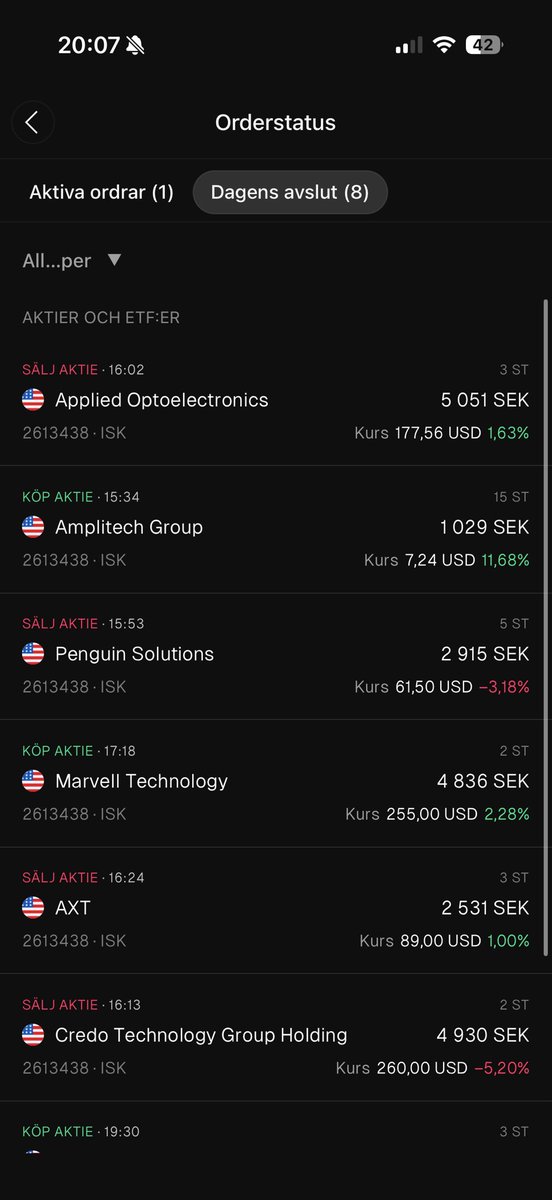

Sold some $AAOI, $AXT, $CRDO and $PENG.

Added $MRVL and $AMPG.

Then bought back $AXT and $CRDO at lower prices.

Not perfect.

But better than staring at the portfolio and calling conviction a strategy.

1

650

Jun 10

Stepped off the $AXTI ride at $69 back in March. Found it again at $78 yesterday. Not too late to rejoin the party.

Here we go again.

391

Jun 10

So ... another red day.

I suppose.

BREAKING: May CPI inflation rises to 4.2%, the highest level since April 2023.

Core CPI inflation also rises to 2.9%, the highest since September 2025.

Inflation in the US is officially back above 4% and more than double the Fed's target.

Odds of Fed rate hikes are rising.

4

938

Jun 10

Today, the European Commission published the final Code of Practice on marking and labelling of AI-generated content.

I’m all for transparency. But there’s a point where disclaimers stop clarifying the message and start replacing it.

If the same logic applied fully to X, every post would become:

One sentence of opinion.

Nine sentences explaining why the opinion may not be an opinion, advice, recommendation, endorsement, promise, forecast or reliable indication of future performance.

At some point, you don’t read the message anymore.

You just scroll through the legal fog.

This message is not financial advice. It is not legal advice. It is not political advice. It is not medical advice. It is not a recommendation to buy, sell, hold, panic, breathe deeply, log off or reconsider your life choices.

The author may own stocks, change his mind, misunderstand regulation, overestimate irony or underestimate the willingness of institutions to make things unreadable.

This post was written on a MacBook Air, with human intention, machine-assisted spell check, mild caffeine exposure and no guarantee that all jokes will perform as expected.

Past humor is not indicative of future humor.

ec.europa.eu/commission/pres…

1

2

336

Jun 10

Seems like we Europeans may finally get a chance to buy SK Hynix during normal waking hours.

With a U.S. listing reportedly coming as soon as August, I’m looking forward to owning SK Hynix and keeping a normal sleep cycle. reuters.com/world/asia-pacif…

4

523

Jun 10

New institutional positions in $SIVE.

BlackRock and Fidelity just showed up on the shareholder list, following JP Morgan last week.

Looking forward to reading the analysis explaining why U.S. institutions keep buying a “meme stock”. 😄

Jun 9

Just seen both BlackRock and Fidelity showing up as $SIVE institutional ownership? Is this completely new?

morningstar.com/stocks/xsto/…

1

1

34

3,332

Jun 10

The world grows more uncertain. AI infrastructure holds.

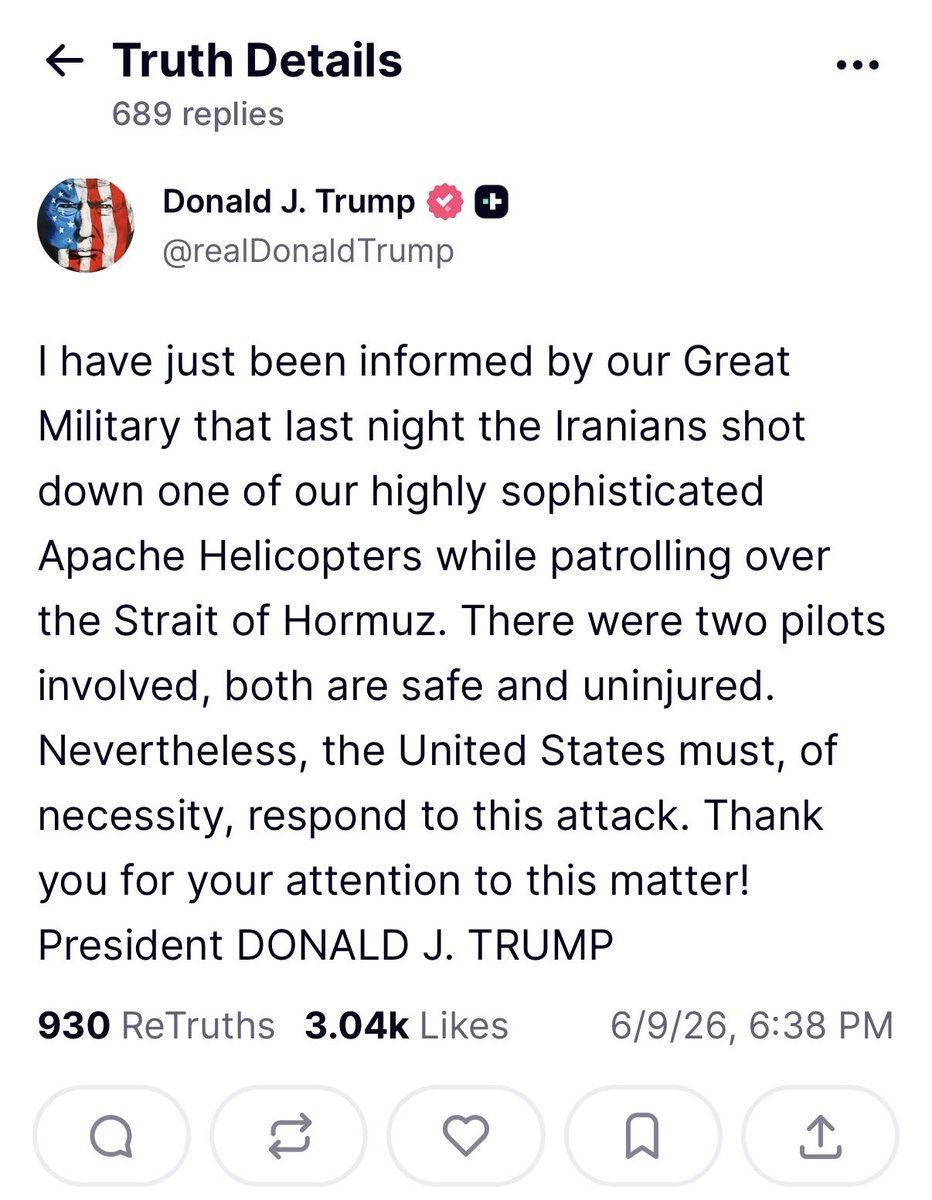

Iran launches missiles at U.S. bases. VIX is around 19. Markets are nervous, but far from panicked.

What hasn’t changed is the AI buildout.

Advanced packaging remains constrained. HBM capacity is largely committed. CoWoS remains a key bottleneck.

The core investment theses remain intact.

Today’s focus is U.S. CPI at 14:30 CET.

Higher oil prices can feed inflation expectations, which in turn affect multiples and market sentiment. The underlying company stories, however, remain largely unchanged.

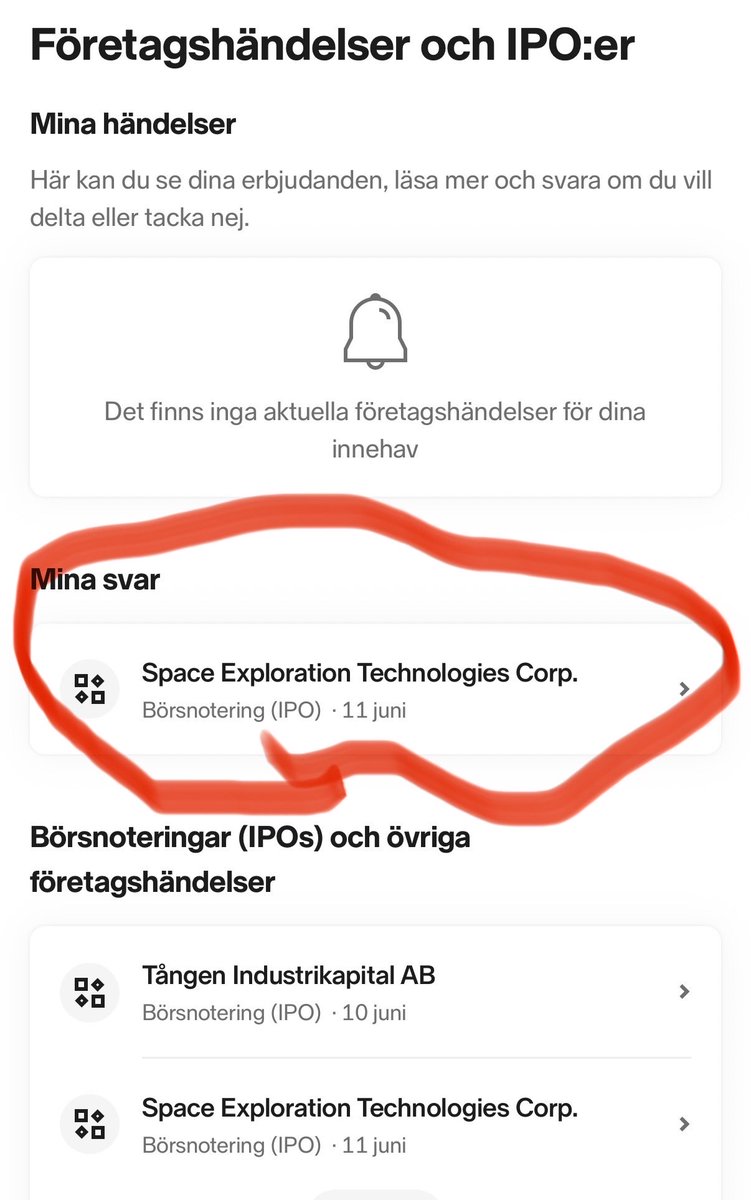

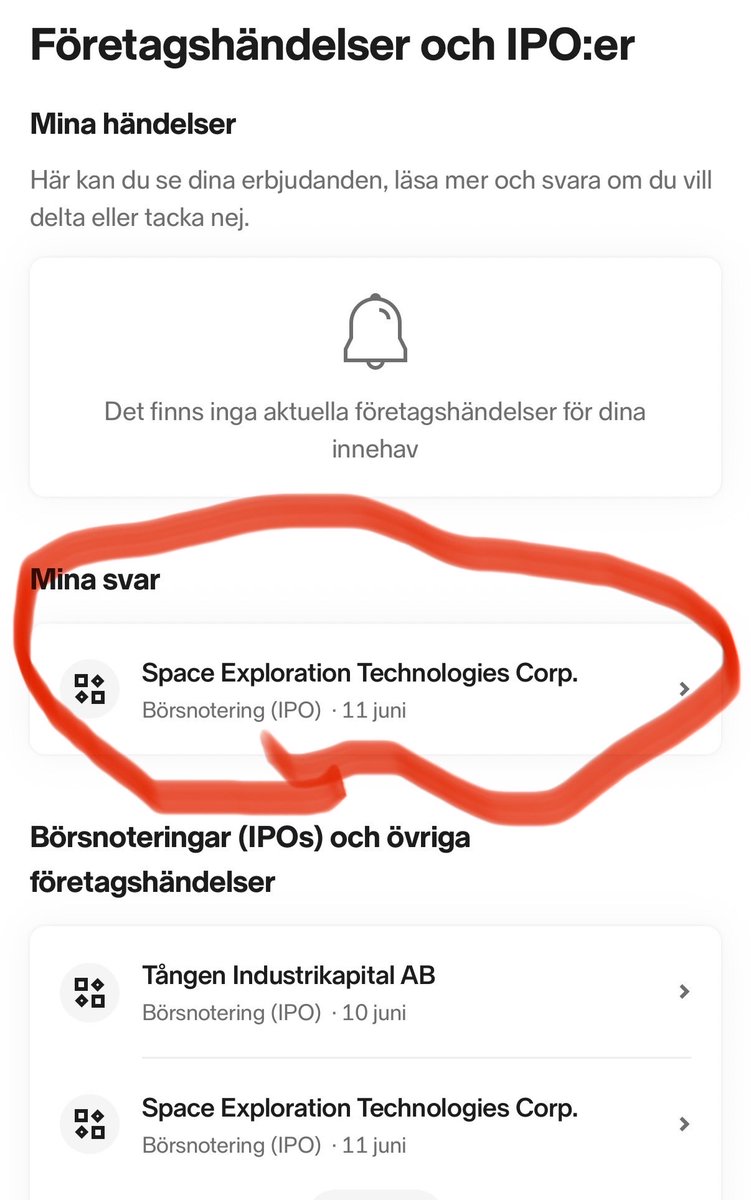

On Friday, SpaceX is expected to begin trading. With a $75B raise at a $1.75T valuation, it would become the largest IPO in history.

It’s been a volatile week. The volatility is likely to continue, but the theses remain intact.

2

413

Jun 10

This is exactly why I bought Credo. One of the few stocks green yesterday.

🚨The AI chips are useless without it.

A GPU is just expensive silicon until you can move data between them at the speed AI demands and that connection layer is becoming the real bottleneck.

That's the $CRDO thesis. And I've been long for a while.

$CRDO built its name on copper connectivity -> the SerDes, DSPs, and active electrical cables that move data between AI chips. The one open question was always what happens when the industry shifts from copper to optical. With the DustPhotonics acquisition, Credo brought silicon photonics in-house and now owns the full connectivity stack: SerDes → DSP → active cables → optical transceivers → silicon photonics, spanning 800G to a 3.2T roadmap. Electrical and optical, end to end.

That's the moat. When Jensen says the future of AI depends on connectivity, this is the layer he means and $CRDO is the pure-play that owns all of it.

The fundamentals: FY26 revenue more than tripled to $1.34B, non-GAAP net income rose 5x to $662M, ~68% gross margins, $1.4B cash and no debt.

$CRDO - run the forward math*👇

→ Revenue CAGR (FY26–FY28): ~61%

→ PEG: ~0.52 -> Re-Rate ✨

→ EV/Sales: ~17x FY27 → ~11x FY28

→ Forward P/E: ~65x trailing → ~42x FY27 → ~27x FY28

A company compounding revenue at ~61% with a PEG of ~0.5.

The multiple isn't the story. The growth is. Watch the "expensive" 65x compress as earnings catch up to 42x, then 27x.

“Expensive” on today's numbers. Cheap on where it's going re-rate.

Everyone's buying the chips.

The chips are useless if you can't connect them.

$CRDO owns the connection. 👀

*Estimated from projections

2

439

Jun 9

One good thing about frequent red days is that I get to practice patience.

So far, I haven’t bought anything…

…yet.

1

3

476

Jun 9

I invest the way I do because of my background.

I'm a reserve officer in information operations and an AI consultant helping lawyers make better decisions with AI.

Both taught me the real constraint is never the brain. It's the infrastructure the brain depends on.

This is what it looks like in my portfolio.

Eight theses. Real positions. 🧵

3

10

1,422

Jun 9

8/ Space and defense are converging

Satellite constellations are becoming strategic infrastructure. Electronic warfare, autonomous platforms, and space-based ISR all need real-time AI. This demand doesn't follow civilian capex cycles. It follows threat environments.

Positions: $ASTS $RKLB $UNIBAP $KULR $AMPG

2

1

5

1,071

Jun 9

The common thread:

I'm not trying to pick winners.

I'm trying to understand where the constraints

are. Physical infrastructure doesn't lie the

same way narratives do.

I could be wrong. Several of these positions

are already teaching me humility.

But the bottlenecks feel real.

That's enough to stay positioned.

3

381