Joined November 2015

- Tweets 7,525

- Following 2,476

- Followers 27,031

- Likes 6,327

1,009 Photos and videos

Pinned Tweet

16 Oct 2025

ADL is a relic of isolated margin systems copied from @BitMEX. It doesn’t work for options, and at best is a terrible experience for cross-margin users.

Paradex deliberately chose not to implement ADL.

It breaks cross-platform hedges, adds a lot of unpredictability to users’ risk management, and fails for complex assets and portfolio-margin setups. There’s also no guarantee of finding profitable ADL counterparties under cross margin, without further amplifying liquidations. @DeribitOfficial also operates without ADL.

Socialized loss (SL) is a far better experience for users and scales easily to more complex assets and margin types 👇

Portfolio-Level Integrity

ADL operates at the single-market level, without considering the user’s overall account exposure. The trader who is high on the ADL queue due to a highly profitable/leveraged position on one market isn't necessarily profitable on an account level.

Example:

BTC = $100,000, ETH = $4,000

Insurance Fund (IF) = $100,000 collateral short 40 BTC perps.

Alice has a $4M BTC-ETH spread on, i.e. 40 BTC perps (long) and –1,000 ETH perps (short)

→ Both BTC and ETH rally 5%

→ BTC to $105,000, ETH to $4,200.

Under a normal scenario, Alice’s BTC and ETH positions offset, leaving her with flat PnL. But the insurance fund’s bankruptcy price is $102,500. To protect the fund, ADL is triggered and forces Alice’s BTC leg to be closed at $102,500 as it cannot afford a loss that is higher than $100,000. Alice realizes BTC profits based on a 2.5% move while her ETH short continues to lose 5%, leaving her with a $100,000 loss. This can, in theory, lead to an unfair liquidation of Alice's account.

"Ethena" Risk

The same is true for a trader that could be holding the opposite position on a different exchange. If the position is subject to ADL, it closes the profitable leg, leaving the user with a naked losing leg. This destroys the intended hedge and amplifies risk exposure. @ethena smartly negotiated this provision away for it's trading on CEXs but that now means the risk of ADL is being unfairly borne by the exchange's other users. Smart for Ethena but not scalable for the exchange.

Given the potential market exposure imposed on affected accounts, ADL often triggers a forced unwind of positions, leading to fire-sale behavior that further amplifies market volatility and erodes liquidity.

This mechanism is particularly unsuitable for exchanges with options, where users frequently hold multiple correlated instruments on the same underlying asset for hedging or risk-neutral strategies. In such environments, forcibly closing a single profitable leg through ADL can break portfolio hedges, destabilize the portfolio and, by extension, the market.

To our knowledge, NO EXCHANGE discloses how cross-instrument exposures are handled under ADL.

Conditional Reversible

Under a SL mechanism, losses are conditional, deferred (not immediately realized) and give users a choice. They are applied only upon withdrawal, and only if the platform is still experiencing a solvency deficit at that time.

If the market rebounds, or if the insurance fund grows (either through profitable liquidations or additional allocations) and covers the deficit, the shortfall is erased and no SL is applied.

By contrast, ADL crystallizes losses instantly and doesn’t give the user a choice. If a sudden market move causes insurance fund depletion, the system immediately closes profitable positions via deleveraging. Those users now permanently lose their realized profits.

SL introduces time, and recovery potential into the loss-allocation process while giving users a choice. It penalizes only those who exit during insolvency, while long-term users benefit if solvency is later restored.

Fair Predictable Risk Distribution

ADL targets specific traders (often highly leveraged and profitable ones), forcibly closing their positions to cover the platform shortfall. It penalizes traders for system-level insolvencies outside their control.

SL by comparison avoids arbitrary targeting and maintains fairness. All users share the risk evenly and only when a persistent shortfall exists.

Transparency

ADL is a complex, queue-based mechanism that is very hard to anticipate for users. In contrast, a SL adjustment is a simple, transparent function of the insurance fund shortfall relative to the platform’s TVL. As it affects users only when they withdraw, it ensures predictability and transparency in the loss allocation.

Compute Efficient = "Chain Friendly"

SL simplicity makes it straightforward to implement on-chain in a trustless manner. There is less compute complexity which means cost and throughput constraints are alleviated. ADL’s dynamic queue logic is computationally heavy as it requires scanning all accounts on the platform, making it very expensive and error-prone. It also adds congestion to a system that is likely to already be congested when ADL is triggered.

October 10 = Wake Up Call

If your CEX can’t guarantee portfolio integrity under stress, it’s the architecture that’s broken. Switch to DEXs with intelligent loss-allocation that protects hedges, distributes risk fairly while staying conditional and predictable.

Paradexio

14 Oct 2025

This is so highly misleading by only focusing on the ADL on the largest coins, which suffered from far less price discolation and ADL overall than other coins

If you are running a long / short book as I was, you are long these assets below, not short them

This also looks at ADL in a vacuum, and without regard to anything else in an account

Your larger shorts are going to be in the other top 50 alts that are dog shit imo (ATOM, STX, APT, FET) - those shorts closed much earlier and blew you out leaving with only longs to liquidate your account

There are so many other places where the @HyperliquidX platform is broken for perps (no ADL transparency / queue, no flash crash protection, one touch price oracles for liquidation (non time based), no whale risk blocker, and zero insurance fund is laughable for someone at $hype scale

So please get this propaganda off my timeline, it is insulting. I can assure you @HyperliquidX did not perform well for anyone running a larger profitable long / short book, or even any sort of mild leverage on just longs. I cannot recommend to anyone serious or an instó to trade on hype when they don't even acknowledge these issues.

In fact, between @DriftProtocol and @dYdX where I run very similar books, only @HyperliquidX blew me out.

Still waiting for my @chameleon_jeff chat 🫡

147

67

517

178,662

BRUNSON HALF OF ALL KNICKS POINTS FML

INSANE!!!!

2

3

469

fiddy.dime - priv/acc 🦡 retweeted

Jun 10

A DEVELOPER IS USING CLAUDE MYTHOS TO BUILD ANIMATED AWARD-WINNING WEBSITES AND DROPPED A FREE 12-MINUTE TUTORIAL SHOWING EXACTLY HOW.

Bookmark this.

39

224

2,057

255,432

Agree. I think pure sciences background plus applied experience in an unrelated field is the winning combo.

Jun 10

I think that's despite, not because. Survivorship bias, not to mention most if not all of the folks in my class were morons. Smart people self select for "harder majors", and pay a degree premia due to being international, or from a non finance feeder program. Most quant PM's are not from the continental US. (French, Asian, Indian etc. ), and are thus compelled to get an obsolete pedigree in shit that hasn't mattered since '08. Can you do advanced ML/DL, Optimization, Linear Algebra and LL Programming/Optimization. Do you love positive expectancy, pay the price to ride the ride. Nothing to do with Continuous PDE's or Bergomi Vol Model. That's more for academic morons, look at ADIA. Then look at most multistrats.

One of the heads of my program was a literal moron, famously so. He fully ripped off another professor's slides, and parroted them while name dropping other academic morons. Avellaneda, De Prado, Capponi...morons. No edge, just hiding behind Latex.

Most MFE programs are just a transaction cost. I'd rather encourage folks to study pure/applied sciences or stats.

2

1

2

676

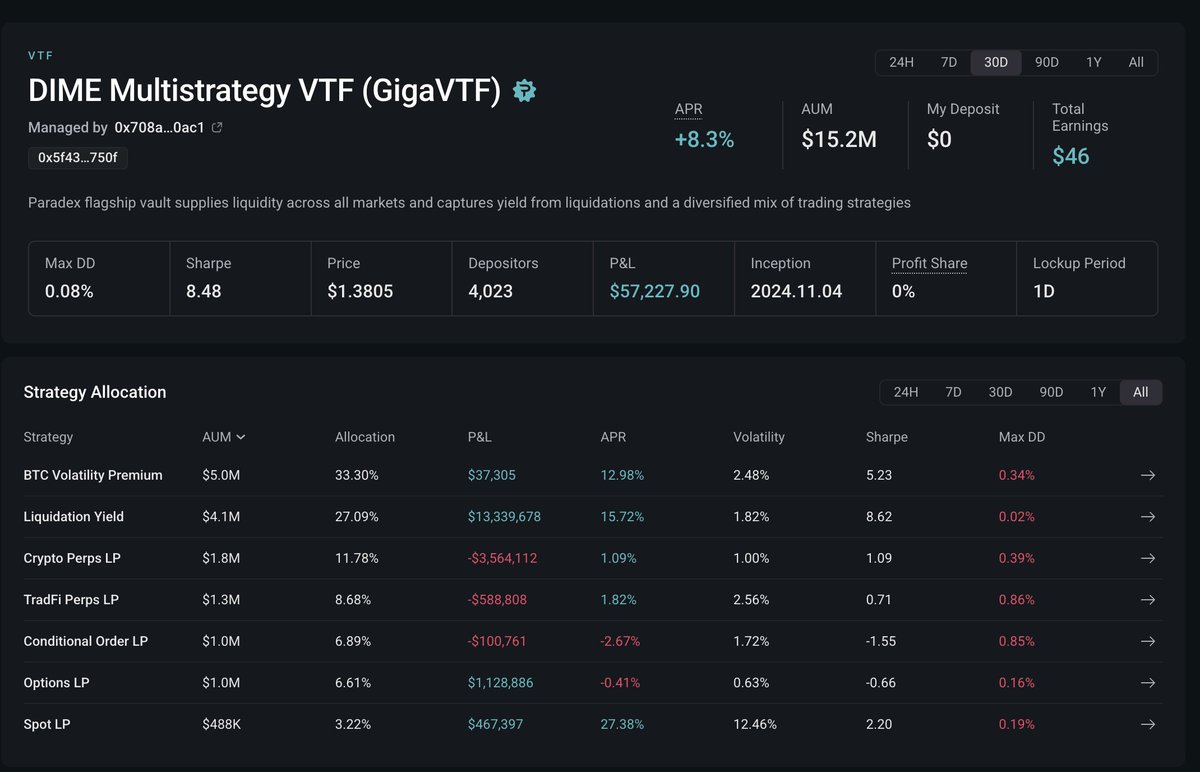

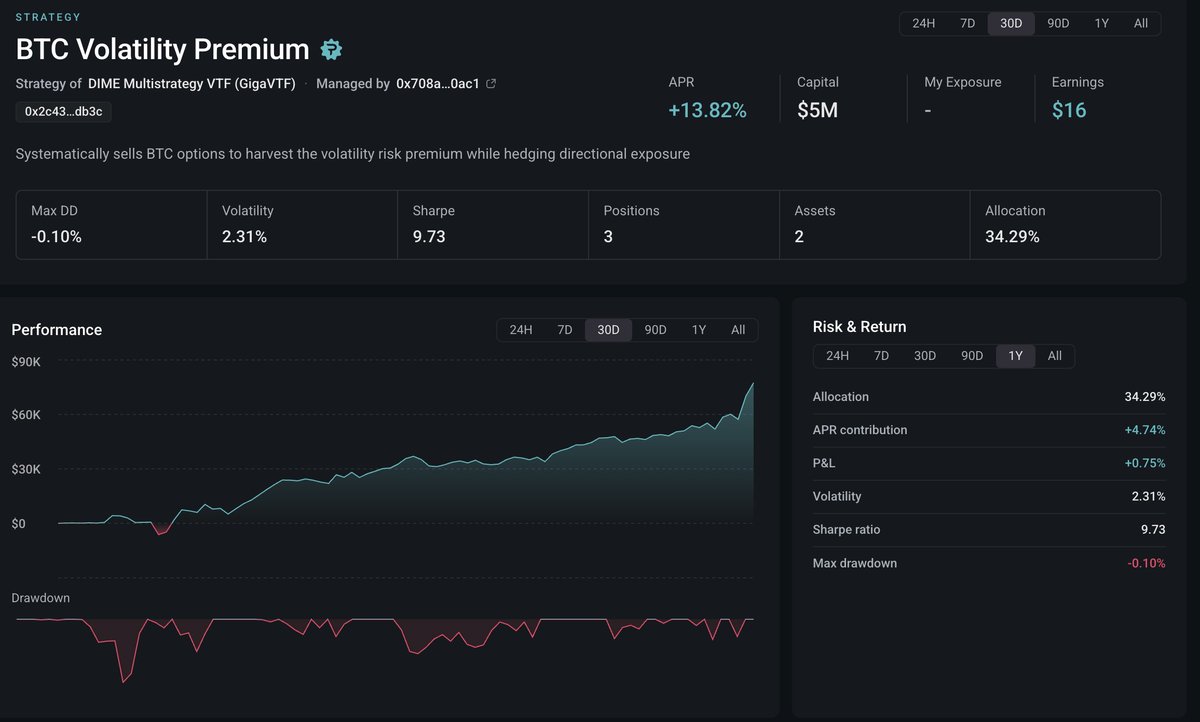

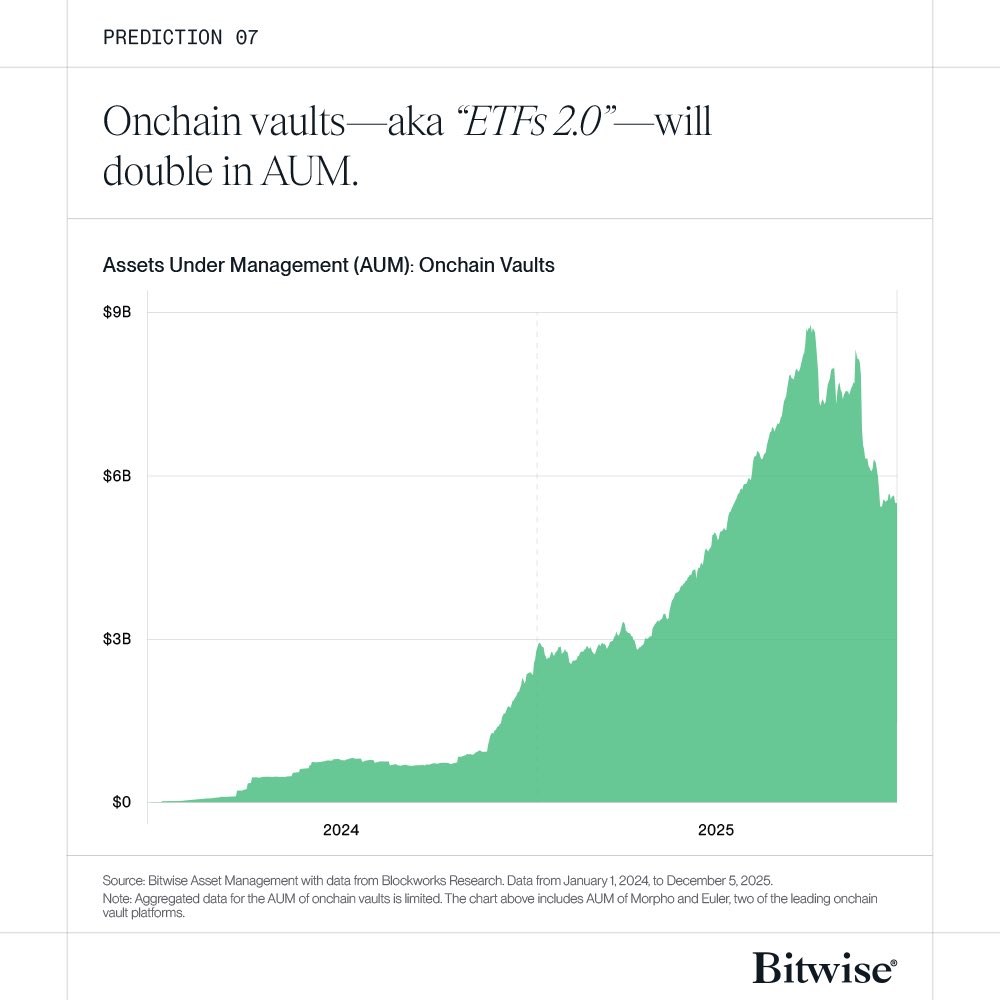

They’re called VTFs ;)

2026 PREDICTION: Onchain vaults will double in AUM.

•What are they? Think "ETFs 2.0" – investment funds that manage assets on the blockchain for yield.

•The Growth: From $0.1B$ in 2024 to $8.8B peak in 2025.

•Why 2026? We expect a wave of high-quality "curators" will be coming in.

•Our take: AUM will double, and Wall Street will notice.

1

1

7

569

👀👀

Wuts this @apoorvsadana??

Jun 8

Every financial innovation connects previously disconnected parties, unlocking billions in value.

11.06.2026

3

1

10

1,211

this should be illegal

Jun 7

Who thought it was a good idea to let donk play in Stage 2?

Bro is just smurfing 😭

1

5

653

shiiiiit what a time to be in NYC

LFG KNICKS!!!!

4

1

11

1,055

long ZEC

Very important update. There will be bugs in all software. The best hope is to have the very best teams find them first. Like this case.

I strongly support Zcash.

1

3

790

looking forward to blowing minds when we roll out RFQ 🔥

CEO @fiddybps1 on RFQ coming to Paradex:

pair trades in size (long $BTC / short $ETH, spot vs perp) with bulk leg execution

basket trades: one RFQ, one price, 50-asset portfolio

exit your entire book instantly. no working orders across multiple books

mix perps & options into programmable portfolios

"nothing like this exists in crypto" perfected on Paradigm since 2019.

minimum block sizes in the hundreds of dollars.

institutional execution for everybody.

2

1

12

1,257

probably some generational opportunities after this bloodbath is over but i reckon theres way more pain to come. doesnt make sense to keep your BTC right now. sellers will test saylor to see where he will capitulate

gg

1

1

5

596

as soon as you click on an instrument, you see everything you need: trades, order book, and the option grid all at the same time. we've been building for options traders for years, so all that experience has gone into making this a best-in-class experience.

seamless navigation when moving between strikes

order book, trades & grid all visible at once

1-click trading for fast market trading

4

3

14

1,289

we've been listening to options traders since 2019 so naturally our options UX is best in class. we're on our way to making @paradex THE screen for crypto options

if you are trading options and don't have this screen up, you are going to lose out

CEO @fiddybps1 on new features bringing institutional-grade speed to paradex:

one-click trading directly on the order book

pre-set default order sizes per asset (USD or BTC)

double-click to execute IOC at best bid/ask

zero friction between seeing price and filling

"on paradigm, one-click trading with RFQ is immensely popular. everybody uses it. this is the default way of executing"

now it's on paradex

trade options with full privacy 24/7

app.paradex.trade/options

3

1

9

786

going to do a live stream tonight with @cissora and @FBChaiTrading 🔥

we've been cooking and we'll cover the following:

Magic with Dime Terminal (do not miss)

Paradigm RFQ Integration

How Paradex is becoming a home for all options traders in crypto

Hosted by: @FBChaiTrading & @cissora

Featuring: @fiddybps1

Saylor selling BTC

VTFs

$HYPE options

DIME Terminal & aggregated market intelligence

Today 21:30 SGT | 09:30 ET

2

2

11

984

wonder how many times this has happened in crypto

Jun 2

wow thank god nobody has thought to do this in comparatively illiquid crypto markets

1

2

1,136