never say never.. I would love varus in 2xko because they always make ranged champs rly interesting and there’s somehow no darkins yet but they’ve added so many adcs for some reason, hope he gets added sooner than later

1

y'a une grosse difference entre une game en inter et des splits complets où les mecs jouent et s'ameliorent tous les jours contre les meilleurs adcs du monde, Calliste il va pas step up en tabassant Supa en boucle

3

企業向けの無線APならRADIUS機能はほぼ標準で付いてて企業ならADを運用してるので

ADサーバーにADCSとNPS機能を有効化。

ドメインに参加したら各端末に証明書を自動で発行する仕組みを入れて

NPSと無線APにRADIUSの設定したら

証明書認証のWi-Fiができるが情シスには荷が重すぎる

企業向けWifiって結局は証明書インストールしてEAP-TLSするしか安全に運用する方法は無いって思ってるんだけど、RADIUS回りの知識が無いと難しいので、意外に普及してないんだよなあ

1

2

13

3,528

Shahid Iqbal retweeted

Jun 10

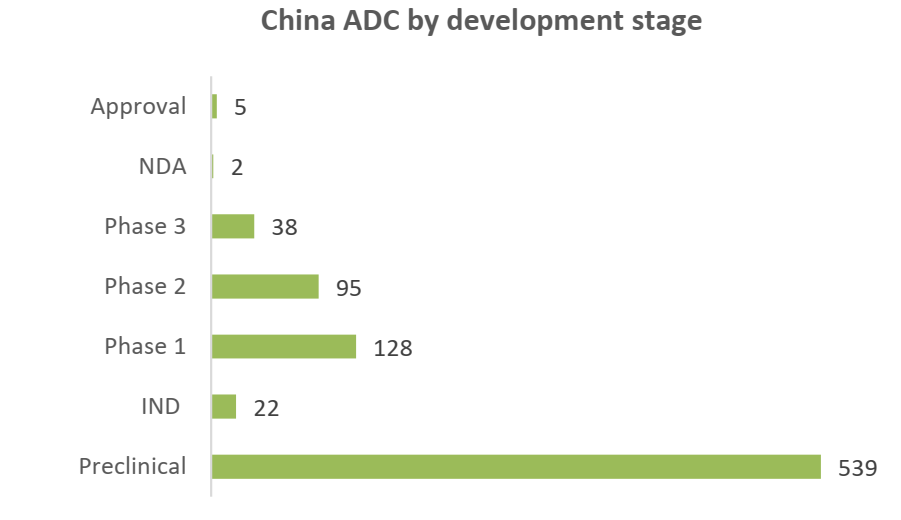

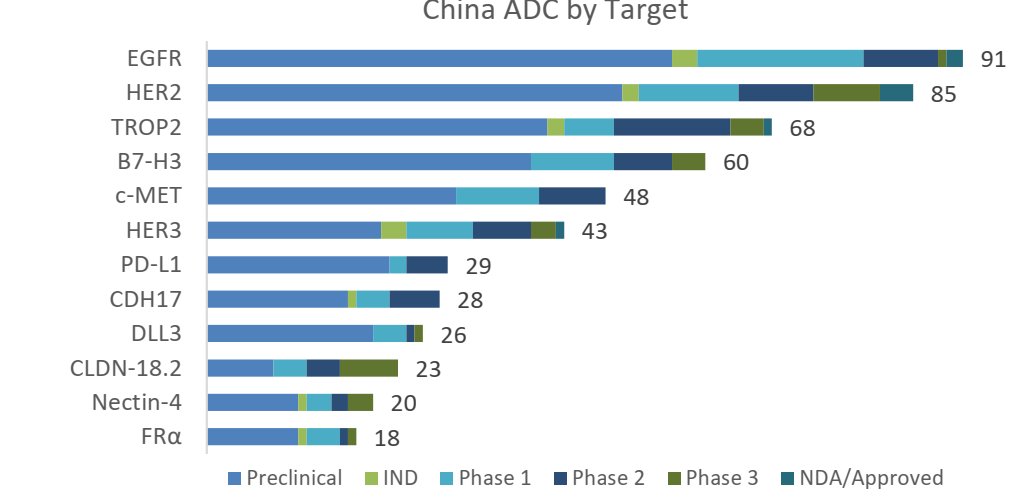

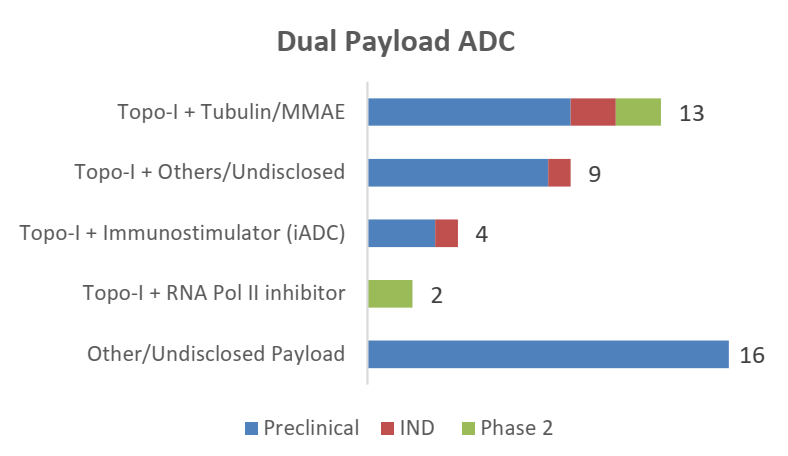

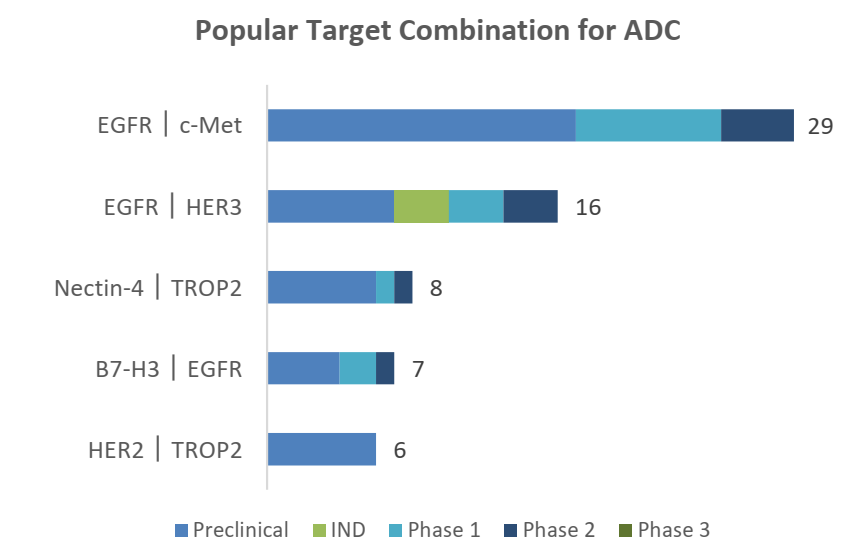

>250 Chinese ADCs currently in clinical trials

>500 in preclinical testing

🤯

Jun 10

China ADC landscape (Great report from Locust Walk)

Next wave is more innovative (bispecifics, new payloads dual payload)

3

15

76

9,067

And multiple augments don’t even work the augments you roll just got much worse. Before this patch you got adc augments with an adc, tank augments with a tank etc. Now i get tank and mage shits on adcs😅😂

1

Oncology is not just the biggest sector in biotech.

It’s the fastest moving.

First PROTAC ever approved. ADCs reshaping chemo. Alpha therapy attracting $7.5B in M&A in a single year.

Here’s who to watch 🧵

1

28

All T1 ADCs flash forward to fight more instead of flashing away to safety

46

Why r u cheering like im writing fic thqg im publishing ? All im saying is i’ll learn how adcs work

1

21

This happens with like 25% of the roster in top every patch but somehow toplaners tell you the role is weak and adcs should get nerfed again

2

4

1,102

⎐كُـود⎐كوبـِون⎐خـِصم⎐

волками с готовой киркой

⎐السيف⎐جالري◗ON5◖

⎐احذية⎐كروكس◗R73◖

⎐كرديال⎐⊵MH135⊴

⎐ناتشرال⎐تاتش◗B91◖

⎐ناتشورال⎐

Подружитесь

___

aDcs

RISKS DISCUSSED IN CONCALL

🔴 Customer concentration: Top client = 12% of revenue, Top 5 = 37%, Top 10 = 54%. Mitigated by the fact that the top customer relationship spans multiple services.

🔴 Geopolitical / supply chain: Middle East tensions driving up logistics and input costs. Recovery from customers may lag cost incurrence.

🔴 Quarterly lumpiness: CRDMO revenues are inherently lumpy — driven by PO timing, not production cycles. Q4 FY26 grew just 4% YoY despite a strong full year. Investors must evaluate on annual, not quarterly, basis.

🔴 New capacity inefficiency: Scaling new plants introduces temporary cost inefficiency before utilisation ramps. EBITDA margins may fluctuate within the 28–30% band.

🟡 Tariff environment: Being monitored closely. No direct impact seen yet. Large pharma proactively restructuring deals to mitigate tariff exposure.

HIDDEN SIGNALS BETWEEN THE LINES

🟢 Acquisition appetite confirmed: Management is actively evaluating deals — specifically for new modality capabilities or small pharma companies. No announcement yet, but the intent is clear.

🟢 "Sai Academy" launched: Internal knowledge transfer program led by a senior ex-pharma head of research. This is how they're systematising what they learn from large pharma — a serious moat-building move.

🟢 Bidar is 100% renewable: First Indian CRDMO site to achieve this. Not just ESG optics — this is increasingly a procurement requirement from large pharma sustainability teams.

🟡 New modalities at only 4% of revenue: Fell from 7% in FY25. Management clarified this is the clinical campaign cycle at play, not structural decline. But the revenue contribution remains small relative to the investment narrative around ADCs and peptides.

1

21

Growth drivers

Next-Generation Technologies — The Long Game

• ADCs (Antibody–Drug Conjugates): Significant pharma interest; moving from discovery-side capability to evaluating clinical conjugation and fill-finish. Class 6 containment upgrade underway.

• Peptides: Development capability pilot-scale manufacturing coming online this year. Capex started in FY26.

• HTE (High-Throughput Experimentation): Platform established at Hyderabad R&D campus — enabling more integrated, faster discovery programs.

• Organoids & Cell-Based Assays: Positioned ahead of FDA's push toward newer testing methodologies (NAMs), reducing reliance on animal testing over time.

AI & Digital — More Serious Than Most Peers

Management's AI framing goes beyond a buzzword. Key points:

Building an "AI canvas" internally — a unified data/automation platform for scientists and leadership.

Integrating with large pharma's own systems for data transmission.

AI-enabled retrosynthesis and route design tools already in use.

Proof-of-concept outcomes expected in CY2026.

CEO was explicit: it's not one tool — it's a complete operational transformation.

Biotech Funding Recovery — A Tailwind in Waiting

YTD biotech funding was up 52% year-over-year, with April 2026 alone at $10.6 billion. IPO activity has strengthened. Management expects biotech to "come back in the next 24 months" and restore the 50/50 pharma-biotech balance in their CRO business. When it does, it adds incremental volume on top of the pharma-led growth that's already running.

1

19

In brief 👉 highligjts :

Cohance Biz Developments (FY26)👉

Challenges: FY26 revenue declined ~13% YoY due to destocking in two large commercial products, customer inventory adjustments, shipment delays, and temporary site disruptions. Q4 net profit dropped sharply (~84% YoY) to 19.55 Cr amid lower volumes and investments.

Margins faced pressure (adj. EBITDA ~21%) from ramp-ups in new capabilities and subsidiaries.

Positives:

Underlying growth in Pharma CDMO (adjusted for destocking) and niche tech (now >17% of revenue, targeting low-20s).

Strong pipeline: 140 active projects, 10 Phase 3 programs, new ADC/oligo advancements, and filings/validations in API .

Leadership refresh with Umang Vohra (ex-Cipla) as Executive Chairman & Group CEO (Apr/May 2026) for strategic focus on execution and growth.

Capex ~ 2.15 Bn deployed on ADC, oligo, and quality infrastructure; healthy cash position.

Outlook

FY27: Expect growth to return, especially in H2, FY27.

Q1 likely the bottom (low revenue/EBITDA due to phasing and costs).

Must note and track this ⬆️

Recovery driven by re-stocking/re-loads in CDMO, new commercial wins, normalized API execution, and pipeline conversion.

Medium-Longer Term: Mgmt maintains ambition for ~$1 Bn revenue with mid-30s EBITDA margins, supported by modality expansion (ADCs, oligos), customer base (top 20 innovators), and investments yielding operating leverage.

Now we need to track executions.

Hoe this helps 🙏

1

475