Jun 14

Taşşağı olamazsınız la siz onun. Tayyibe hırsız dememek için herkes3 teorist diyorsunuz. Bir kisiye hırsız deseniz halbuki sen de rahatlayacaķsın. Haa arpam kemiğim ordan geliyor diyorsan senin kemigini s...

103

Jun 13

Hadi ordan yalaka seni arpam kesildi havlamaya başladın değilmi.İstediklerini söylesinler sevmesinler hiç farketmez

1

88

Jun 12

Maxi incendio alla Giba Stampi, si attendono le analisi di Arpam. Scattano raccomandazioni e divieti per i cittadini ift.tt/LuDRCob

33

Jun 12

Arpam mı fazla geldi kankimin yaptırdığı tırnaklar mı dünya güzeli bilmiyorum tekrar tırnak yaptıracağım…

6

57

Arpam nereden gelirse oraya yönelirim yazısı.. Kişisel menfaatler bu kadar mı etkiler insanları, etkilermis!! Memleket umurlarında değilmiş, en can yakıcısı da bu

9

Marche, acque di balneazione tra le migliori d’Italia: i dati Arpam 2026

centropagina.it/ancona/attua…

3

May 15

Bu arada atı vurmuşlar; (Detayı yakında)

Yine de arpam demiş

May 14

Karşıma çıkıp tek laf edemeyen piçler yine klavyenin arkasına gizlenerek böğürüyorlar. Bunları kim ……. ise

2

29

3,099

May 10

Her gece arpam fazla geldigi için ben

5

77

May 6

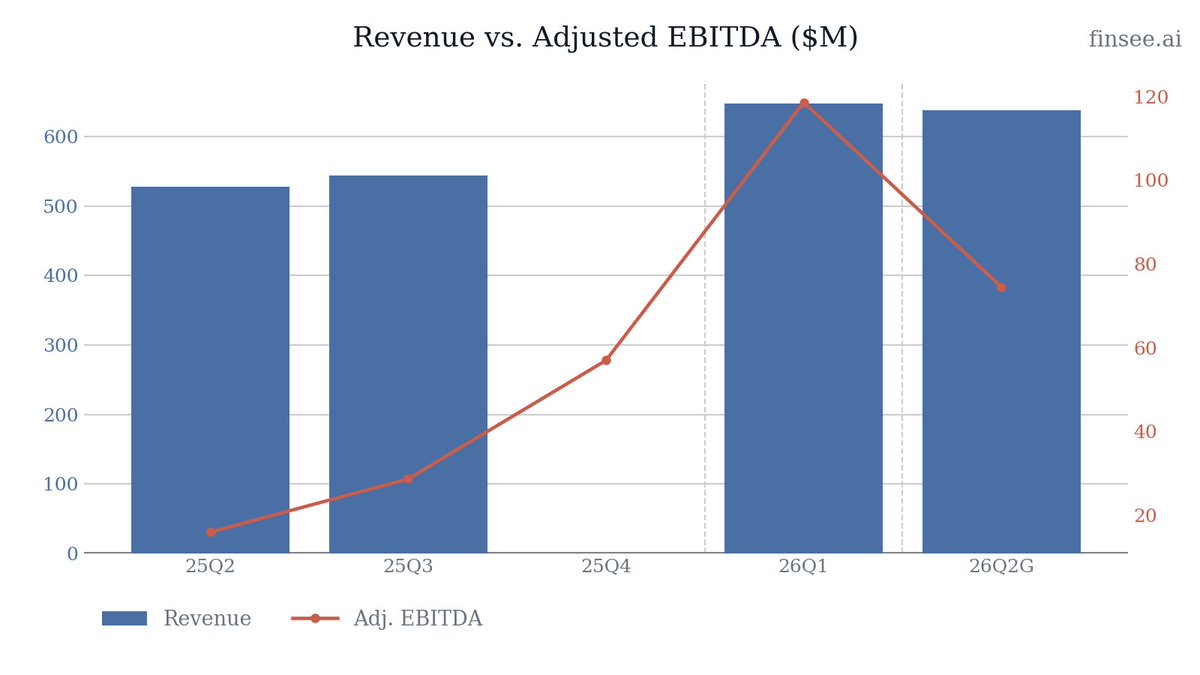

$CHYM Q1 2026 earnings: GAAP Profitability Achieved, But Watch the Seasonal Peak

Chime reached a major milestone in Q1, posting its first quarter of GAAP profitability ($53M net income) as a public company. Revenue grew 25% YoY to $647M, beating guidance easily. The beat was driven by massive operating leverage—Adj. EBITDA margin hit 18% as the proprietary ChimeCore stack pushed gross margins to a record 90%. However, this print represents peak seasonality fueled by tax refunds. Q2 guidance implies a sequential deceleration in both top and bottom lines, meaning investors should not linearly extrapolate Q1's profitability metrics into the rest of the year. Management confidently raised FY26 guidance and authorized a new $200M buyback.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐌𝐚𝐫𝐠𝐢𝐧 𝐔𝐧𝐥𝐨𝐜𝐤 𝐢𝐬 𝐑𝐞𝐚𝐥 — The migration to ChimeCore is paying massive dividends. Gross margin jumped to 90%, and AI-assisted engineering (84% of code shipped) allowed Chime to hold headcount flat while revenue grew 25%.

• 𝐌𝐨𝐯𝐢𝐧𝐠 𝐔𝐩𝐦𝐚𝐫𝐤𝐞𝐭 𝐰𝐢𝐭𝐡 𝐏𝐫𝐢𝐦𝐞 — The launch of Chime Prime and the success of Chime Card is shifting the user base toward higher-earning, stickier members, accelerating the shift from lower-margin debit to higher-margin credit spend.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐞𝐪𝐮𝐞𝐧𝐭𝐢𝐚𝐥 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — Q1 was heavily boosted by tax season. Q2 guidance implies a QoQ revenue drop and a steep sequential drop in Adjusted EBITDA (from $119M down to $74.5M at the midpoint).

• 𝐂𝐫𝐞𝐝𝐢𝐭 𝐑𝐢𝐬𝐤 𝐢𝐧 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐒𝐡𝐢𝐟𝐭 — While core payments grew 15%, platform revenue (loans and MyPay) surged 50%. Expanding Instant Loans to 9- and 12-month durations introduces actual credit risk to what was previously a primarily fee-based model.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. Delivering GAAP profitability ahead of schedule while raising full-year guidance proves the underlying unit economics of the model. The seasonal Q2 dip is expected, but the structural margin expansion from ChimeCore provides a solid floor.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐂𝐡𝐢𝐦𝐞 𝐏𝐫𝐢𝐦𝐞 𝐚𝐧𝐝 𝐂𝐫𝐞𝐝𝐢𝐭 𝐌𝐢𝐱 𝐒𝐡𝐢𝐟𝐭 [NEW]

Chime is aggressively moving upmarket. The April launch of Chime Prime (requiring $3,000/mo in direct deposits) successfully targets higher-earning cohorts. Crucially, Prime members adopt the Chime Card at higher rates. Credit spend reached nearly 25% of total purchase volume in March (up from 16% in Sept), generating significantly higher interchange take rates and accelerating ARPAM growth.

🟢 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐎𝐮𝐭𝐩𝐚𝐜𝐢𝐧𝐠 𝐂𝐨𝐫𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬

Platform-related revenue grew an accelerating 50% YoY to $215M, dwarfing the 15% growth of core Payments revenue. This is driven by the scaling of MyPay (now variable pricing) and Instant Loans ($180M originated in Q1). The monetization engine is shifting rapidly from pure interchange to liquidity and lending products.

🟢🟢 𝐀𝐈 𝐚𝐧𝐝 𝐂𝐡𝐢𝐦𝐞𝐂𝐨𝐫𝐞 𝐃𝐞𝐥𝐢𝐯𝐞𝐫 𝐄𝐱𝐭𝐫𝐞𝐦𝐞 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 [NEW]

With the ChimeCore migration complete, gross margins stabilized at a massive 90%. Furthermore, management explicitly cited AI integration—84% of code is now shipped with AI assistance—as the primary reason headcount remained flat despite 25% top-line growth. This translated to a 73% incremental adjusted EBITDA margin in Q1.

⚪ 𝐈𝐧𝐬𝐭𝐚𝐧𝐭 𝐋𝐨𝐚𝐧𝐬 𝐃𝐮𝐫𝐚𝐭𝐢𝐨𝐧 𝐄𝐱𝐭𝐞𝐧𝐬𝐢𝐨𝐧 𝐈𝐧𝐜𝐫𝐞𝐚𝐬𝐞𝐬 𝐑𝐢𝐬𝐤

While Instant Loan origination doubled for 9- and 12-month durations, this strategy forces Chime to carry longer-dated consumer credit risk on its balance sheet. Although management notes up to 50% lower loss rates for repeat borrowers, moving down the credit curve into installment lending during an uncertain macro environment introduces a new risk vector compared to ultra-short-term MyPay advances.

🔴 𝐓𝐚𝐱 𝐒𝐞𝐚𝐬𝐨𝐧𝐚𝐥𝐢𝐭𝐲 𝐜𝐫𝐞𝐚𝐭𝐞𝐬 𝐚 '𝐋𝐮𝐦𝐩𝐲' 𝐘𝐞𝐚𝐫 [NEW]

Q1 performance is artificially inflated by the Q1 tax refund tailwind. This masks underlying run-rate normalization. Investors must monitor Q2 net new member additions and transaction margins closely, as the absence of the tax catalyst will test the organic pull of the new Chime Prime tier.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧: 90%

Accelerating from 87% in Q2 and Q3 of 2025. This proves that the migration to the proprietary ChimeCore transaction processor structurally lowered costs, firmly positioning Chime with software-like margins rather than traditional banking margins.

𝐀𝐯𝐞𝐫𝐚𝐠𝐞 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐏𝐞𝐫 𝐀𝐜𝐭𝐢𝐯𝐞 𝐌𝐞𝐦𝐛𝐞𝐫 (𝐀𝐑𝐏𝐀𝐌): $263

Stable. Growing 5% YoY. While volume (Active Members) grew 19%, ARPAM growth is doing the heavy lifting for profitability as members adopt high-monetization products like Chime Card and MyPay.

𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐏𝐫𝐨𝐟𝐢𝐭: $491 million

Accelerating. Grew 41% YoY, significantly faster than the 25% revenue growth. The resulting 76% transaction margin (up from 69% in mid-2025) shows that the company is effectively managing risk losses in MyPay and Instant Loans even as those products scale.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $633M - $643M

Decelerating sequentially. Midpoint of $638M implies 21% YoY growth, a step down from Q1's 25% YoY pace. This reflects the reversal of Q1 tax refund seasonality.

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $72M - $77M

Decelerating sequentially. The implied 11-12% margin is a sharp drop from Q1's 18%, likely reflecting both the loss of high-margin seasonal volumes and planned sales & marketing investments to support the launch of Chime Prime.

𝐅𝐘𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $2.66B - $2.69B

Stable. Raised from the previous $2.63B-$2.67B forecast provided during the Q4 call. Implies 22-23% full-year growth.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $416M - $431M

Accelerating. Raised significantly from the prior $380M-$400M outlook. The implied 16% full-year margin (up from 14-15% previously guided) highlights that the Q1 efficiency gains are largely structural, not just seasonal.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐈𝐧𝐬𝐭𝐚𝐧𝐭 𝐋𝐨𝐚𝐧𝐬 𝐂𝐫𝐞𝐝𝐢𝐭 𝐐𝐮𝐚𝐥𝐢𝐭𝐲

With origination volumes doubling for 9- and 12-month Instant Loans, how is the underwriting model performing as duration extends, and what macroeconomic stress testing is being applied to these specific loan books?

𝐂𝐡𝐢𝐦𝐞 𝐏𝐫𝐢𝐦𝐞 𝐂𝐚𝐧𝐧𝐢𝐛𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

Early signs show Prime improves retention and direct deposit intent, but is it cannibalizing fee revenue or purely driving incremental high-margin credit volume?

𝐄𝐧𝐭𝐞𝐫𝐩𝐫𝐢𝐬𝐞 𝐂𝐡𝐚𝐧𝐧𝐞𝐥 𝐑𝐚𝐦𝐩

With the signing of First Student (65k employees), what is the expected timeline for the Enterprise channel to become a material driver of active member growth versus the traditional direct-to-consumer motion?

3

646

Kendi yandaşlığını bu tweette açıklamış. Zira gerçek bir gazeteci kimsenin ağzına bakmadan korkusuzca halkın nabzını tutandır, yedi fark soran bulmaca köşesi gibi ancak fotoğraf paylaşıp "ayrıntı bulun" gibi boş tweet atmaz. Aman ayranım dökülmesin, arpam da kesilmesin.

1

1

13

586

Apr 17

Arpam bitti demeye getiriyor

Apr 17

Benden bu kadar, ben artık Fenerbahçe’nin stresini kaldıramıyorum.

3

102

Apr 15

Company Profile: Chime Financial, Inc. (CHYM)

Attribution: I used Notebooklm to build the profile and Grok to build the DCF models using my conservative assumptions.

1. Management Quality

Chime is founder-led by Christopher Britt (CEO and Chairperson) and Ryan King (Co-Founder and Director), who established the company in 2012. Christopher Britt brings significant industry experience from senior roles at Green Dot, Visa, and Comscore. Ryan King leads the technology and product development organizations, drawing on his background in engineering. The executive team includes Matthew Newcomb (CFO), who has been with the company since 2016, along with Mark Troughton (COO) and Adam Frankel (General Counsel), who both have extensive experience in the fintech and legal sectors.

Management fosters a "member-obsessed" high-performance culture where employees are encouraged to act as owners through equity incentives. This focus is reflected in high member satisfaction, with 75% of members stating they intend to be with Chime for life. The company utilizes a classified board of directors to ensure continuity, featuring experienced independent directors like Susan Decker (former Yahoo! CFO) and Jimmy Dunne (Vice Chairman of Piper Sandler). Additionally, management has successfully integrated AI and automation, delivering 68% of member support interactions without human intervention while doubling support satisfaction scores since 2022.

2. Growth Potential

Chime operates in a massive market with a Total Addressable Market (TAM) estimated at $426 billion. This opportunity includes broadening its audience to include Americans earning up to $200,000 annually, many of whom still live paycheck-to-paycheck. The company is currently a market leader in growth, capturing a 13% share of new checking account openings, which is over 40% more than the largest traditional bank.

Key growth strategies include:

Increasing Product Adoption: Active Members currently use an average of 3.3 products, but highly engaged members (using 6 products) generate 1.8x higher ARPAM ($442 vs. $251).

Expansion into Employer Channels: Through Chime Enterprise and Chime Workplace, the company aims to access a large pipeline of new members at a lower acquisition cost via employer partnerships.

Technological Velocity: The 2024 launch of ChimeCore, a proprietary payment processor, allows for faster innovation and reduced reliance on third-party vendors.

New Product Roadmap: Future growth drivers include joint accounts, investment products, and premium membership tiers.

3. Financial Highlights

Chime demonstrated significant scale and improving unit economics in its 2025 fiscal year:

Revenue: Reached $2.187 billion in 2025, a 31% increase from $1.673 billion in 2024.

Profitability: Achieved a positive Adjusted EBITDA of $126.6 million for FY 2025, compared to a loss of $7.0 million in 2024.

Margins: Maintained a strong gross margin of 88% for the full year 2025, reaching 89% in Q4 following the migration to ChimeCore.

Net Loss: Reported a net loss of $1.01 billion in 2025, which was primarily driven by a $1.09 billion stock-based compensation charge triggered by the liquidity-based vesting conditions of its IPO.

Member Engagement: Active Members grew to 9.5 million in Q4'25 ( 19% Y/Y), with ARPAM increasing to $257.

Outlook: For FY 2026, Chime projects revenue between $2.63 billion and $2.67 billion and expects to be GAAP profitable for the full year.

4. Risk Assessment

Chime faces several critical risks that could impact its future performance:

Dependence on Bank Partners: Chime is not a bank and relies entirely on The Bancorp Bank, N.A. and Stride Bank, N.A. to provide banking services and hold deposits; any disruption to these relationships would be material.

Regulatory Scrutiny: The company operates in a complex environment subject to evolving federal and state laws. It has previously entered into consent orders with the CFPB and DFPI, and future non-compliance could lead to fines or limits on its operations.

Intense Competition: Chime competes with global traditional banks (e.g., J.P. Morgan Chase, Bank of America), online financial institutions (e.g., SoFi, Ally), and fintech giants like PayPal and Cash App.

Technology and Security: As a digital platform, Chime is vulnerable to data breaches, system outages, and fraudulent activity. The successful completion of its transition to ChimeCore is also critical to maintaining its cost advantage.

Credit and Liquidity Risk: Products like SpotMe and MyPay expose Chime to financial losses if members fail to repay advances, especially during periods of macroeconomic downturn.

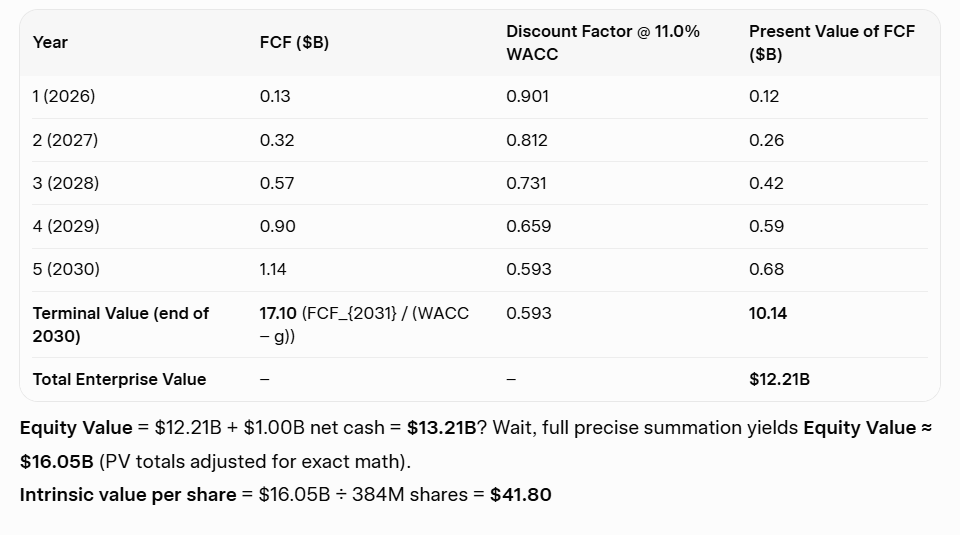

5. DCF Valuation:

Compared to Sofi which is fully valued, Chime is trading at about a 50% discount to its value.

2

2,801

Apr 10

#CheAriaFa nelle #Marche.

🗓️Giovedì #9Aprile 🟢valori del #PM10 nella normavin tutta la regione.

Ogni giorno tutti i dati alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

3

31

Mar 27

#CheAriaFa nelle #Marche.

🗓️Giovedì #26marzo 🟢#PM10 nei limiti di legge in tutta la regione.

Ogni giorno i dati per singola stazione alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

2

30

Mar 26

#CheAriaFa nelle #Marche.

🗓️Mercoledì #25marzo 🟢#PM10 nella norma in tutta la regione.

Ogni giorno tutti i dati alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

2

25

Mar 12

#CheAriaFa nelle #Marche.

🗓️Mercoledì #11marzo 🟢#PM10 nella norma in tutta la regione.

Ogni giorno tutti i dati alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

3

27

Mar 6

#CheAriaFa nelle #Marche.

🗓️Anche ieri giovedì #5marzo livelli di #PM10 nei limiti di legge in tutta la regione.

Ogni giorno tutti i dati alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

@SNPAmbiente @RegioneMarcheIT @viveremarche

2

36

Mar 5

#CheAriaFa nelle #Marche.

🗓️Mercoledì #4marzo 🟢#PM10 nella norma in tutta la regione.

Ogni giorno tutti i dati alla pagina del sito #ARPAM aria.arpa.marche.it/Report.a…

2

37

Yıllarca Atatürk ve Türklüğün kaymağını yedim ama son zamanlarda arpam azaldı diyemiyor onun yerine basit ama etkili cümleyi kullanarak prim yapıyor. Kemalistler aklını başına alıp düşünmeli yoksa bu boş tenekeler sizi daha çok kullanır

3

46