FCF or Bust retweeted

Addus Homecare Corp $ADUS stands as a dominant force in the home-based care sector by providing essential, non-medical assistance that keeps at-risk patients out of expensive institutional facilities. The company capitalizes on the massive demographic wave of an aging population, driving continuous growth through a smart blend of organic expansion and programmatic regional acquisitions. Despite generating robust free cash flow and consistently beating earnings expectations, the stock currently trades at a deep discount to sector peers due to lingering regulatory fears regarding future Medicaid margin caps. Given the critical need for cost-effective care networks, will upcoming state-level exemptions serve as the ultimate catalyst to unlock this stock's true intrinsic value?

1

68

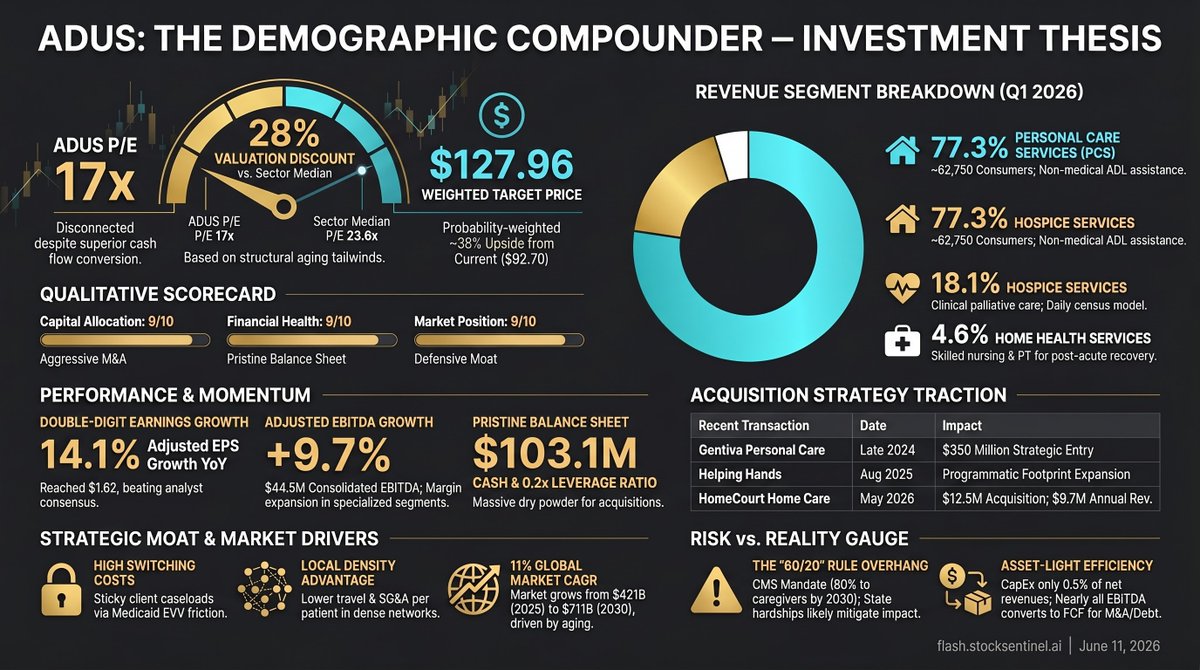

Wall Street is terrified of the looming CMS 80/20 mandate, driving $ADUS to a 52-week low despite a recent earnings beat. But they missed the fine print: state-level hardship exemptions are heavily favored to neutralize this regulatory threat. While regional peers panic, Addus is leveraging its near-zero capex model to quietly scoop up local care books at distressed multiples. It's a pure-play demographic compounder severely mispriced by a broken narrative. 📉⚖️ #ValueInvesting #Healthcare

auth.flash.stocksentinel.ai/…

46

Jun 3

3/ $ADUS — Addus HomeCare (home & personal care services)

Trailing PE: 16.44 ✅

Forward PE: 11.03 ✅

Debt/Equity: 12.4% ✅

3yr EPS CAGR: 22.5% ✅

PEG: 0.49 ✅

Market cap: $1.66B ✅

1

8

10,471

Had a great visit with Addus HomeCare at their corporate office in North Texas, where we discussed the ongoing challenges of waste, fraud, and abuse in the industry, and the real impact it has on providers like them.

With more than 260 locations nationwide, Addus delivers high-quality care to over 62,000 patients each week.

2

3

14

818

📍Lübnan Türkmenleri:

🔻Lübnan, mezhepsel çeşitliliği ve karmaşık siyasi yapısıyla bilinen bir Ortadoğu ülkesi olsa da, sınırları içinde yüzyıllardır varlığını sürdüren bir Türk kökenli topluluk dikkat çeker: Lübnan Türkmenleri (veya Lübnan Türkleri). Bu topluluk, Selçuklu, Memlük ve özellikle Osmanlı dönemlerinden kalan göç dalgalarının ürünüdür. Tolunoğulları ve İhşidîler gibi erken Türk devletlerinin izleri, Selçuklu fetihleri sırasında Bekaa Vadisi’ne yerleşen Türkmen aşiretleri ve Osmanlı idaresi altında Anadolu’dan gelen yerleşimciler, bugünkü Lübnan Türkmen nüfusunun temelini oluşturur. Bazı gruplar Memlükler tarafından kıyı güvenliği ve vergi toplama amacıyla 14. yüzyılda bölgeye yerleştirilmiştir.

🔻Günümüzde Lübnan Türkmenleri, ülkenin kuzeyindeki Akkar bölgesi ile doğusundaki Bekaa Vadisi’nde yoğunlaşmıştır. Nüfus tahminleri kaynaklara göre değişiklik gösterir. 2011 verilerine göre yaklaşık 80 bin yerli Türkmen olduğu belirtilirken, daha yeni değerlendirmelerde (2025) bu rakam 60 bin civarına çekilmekte, Suriye iç savaşı sonrası gelen Suriye Türkmeni mültecilerle birlikte toplam sayının 200-280 bin’e ulaşabileceği ifade edilmektedir. Lübnan’ın toplam nüfusunun (2026 itibarıyla yaklaşık 5,9 milyon) küçük bir kısmını oluştursalar da, özellikle belirli köylerde yoğun ve homojen bir varlık gösterirler.

🔹Ana Yerleşim Alanları ve Köyler

🔻Akkar Bölgesi (Kuzey Lübnan):

Türkmen nüfusunun en yoğun olduğu alan burasıdır. En bilinen yerleşim Kavaşra (Kouachra/Qawashra) köyüdür. Yaklaşık 2.800-5.000 nüfuslu köyün tamamı Türkmen’dir ve halk günlük hayatında akıcı Türkçe (“Obaççi” lehçesi) konuşur. Köy, adeta Anadolu’nun bir parçası gibi görünür; düğünler, gelenekler ve aile yapısı bu bağı yansıtır.

Yakınındaki Aydamun köyü ise heterojendir: 3.000 nüfusun yaklaşık p-75’i Türkmen’dir, kalan kısmı Hristiyan Araplardan (çoğunlukla Rum Ortodoks) oluşur. Diğer Akkar köyleri arasında Debabiyeh, Dousseh, Masta Hasan ve Dinniye (Hawwara, Jairoun) gibi yerlerde de Türkmen aileler yaşamaktadır. Akkar Türkmenleri genel olarak daha dışa açık, tarıma dayalı bir sosyo-ekonomik yapıya sahiptir.

🔹Bekaa Vadisi / Baalbek Çevresi (Doğu Lübnan):

Bu bölgedeki Türkmenler daha kapalı ve aşiretçi bir yapı sergiler. Şii ve Hristiyan nüfusun yoğun olduğu bir coğrafyada Sünni Türkmen köyleri adacıklar halinde varlığını korur. En önemli köyler şunlardır:

🔻Şeymiye (Şuhamiyye): Nüfusu yaklaşık 1.000-1.200, tamamı Türkmen. Türkçeyi en iyi koruyan yerleşimlerden biridir; çocuklar bile akıcı konuşur. Anadolu köylerini andıran mimarisi ve yaşam tarzıyla dikkat çeker.

🔻Nananiye (Nanaiyye): Tamamı Türkmen, yaklaşık 800-900 nüfus.

🔻Addus: 800 nüfus, � Türkmen.

🔻Hadidiye: Küçük bir köy/mezra, 500 nüfus, tamamı Türkmen.

🔻Duris: Daha büyük bir kasaba (8.000 nüfus); burada Türkmenler azınlıktadır (yaklaşık 600 Sünni Türkmen). Şehirleşme nedeniyle Türkçe kullanımı azalmış, Lübnanlı Sünni kimliği öne çıkmıştır.

🔻Al Kaa (Meşari Al Kaa): Suriye sınırına yakın, tarıma dayalı, tamamı Türkmen.

🔻Bekaa Türkmenleri, çevredeki mezhepsel gerilimlere rağmen kendi içlerinde homojen bir yapı korur ve akrabalık bağlarıyla birbirine bağlıdır.

🔹 Dil, Kültür ve Kimlik

Lübnan Türkmenleri Sünni Müslüman’dır ve kimliklerini “önce Lübnanlı, sonra Sünni, ardından Türkmen” şeklinde tanımlar. Konuştukları lehçe “Obaççi” olarak bilinir; Akkar ve özellikle Şeymiye’de orta yaş üstü ve genç nesilde hâlâ canlıdır. Ancak Arapça eğitim sistemi, karışık evlilikler ve şehirleşme nedeniyle gençlerde dil erimesi riski vardır.

🔻Kültürlerinde Anadolu Türkmen/Yörük izleri belirgindir: Aile isimleri (Karanuhlu, Karaalili, Doğanlar, Ekinler vb.), düğün gelenekleri, yemekler ve bazı köylerde görülen hayvancılık geçmişi bu bağı gösterir. Türkiye’ye karşı güçlü bir kültürel yakınlık hissedilir; son yıllarda Türkçe kursları, ziyaretler ve sivil toplum çalışmaları bu bilinci güçlendirmiştir.

7

40

172

5,065

🌟 | Intégration au portefeuille

J'intègre, au sein de le thématique "3ème âge" de mon portefeuille, la small-cap Savaria | 🇨🇦, avec l'achat de 50 titres.

🔎 | Savaria est spécialiste des solutions d'accessibilité, à destination tant des particuliers que des professionnels. Elle propose des gammes complètes de monte-escaliers, élévateurs pour fauteuils ou encore des ascenseurs.

La société est également présente dans les équipements médicaux tels que les lits et les harnais de manipulation de patients.

🎯 | Dans le contexte actuel de vieillissement global de la population et de développement de l'accessibilité pour les personnes handicapées, les activités de Savaria sont appelées à croître durablement.

Ce rythme de croissance n'est pas forcément appelé à être très élevé d'une année à l'autre. Par contre, touz les éléments sont réunis pour quelque chose de long terme !

🟰 | Savaria vient donc compléter mes positions déjà existantes dans la thématique "3ème âge"...

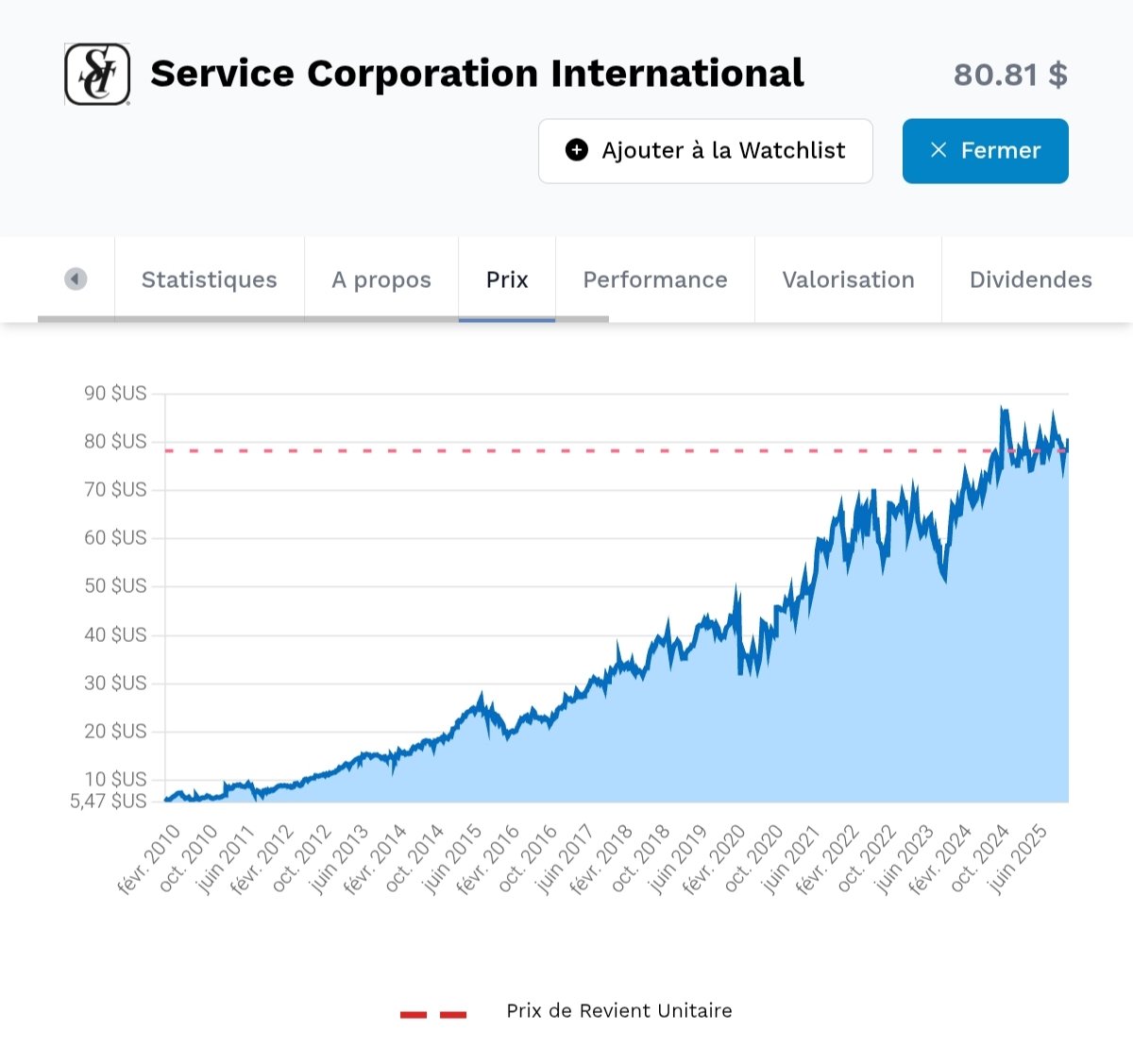

▫️Service Corporation International | Sevices funéraires

▫️Addus Homecare | Soins à domicile

▫️The Ensign Group | Établissements de soins et hébergement de personnes âgées

2

3

15

10,917

Pas encore de position FR dans la thématique, mais plusieurs positions US...

⚰️ | Service Corporation International | 🇺🇸

▫️Services Funéraires, leader US.

🏥 | The Ensign Group | 🇺🇸

▫️Établissements de soins et hébergement de personnes âgées, leader US.

⚕️ | Addus Homecare | 🇺🇸

▫️Soins à domicile

En parallèle, je surveille un acteur canadien de l'accessibilité. Déjà présente dans Sous les Radars il y a quelques mois.

Mar 22

Il y a désormais plus de décès que de naissances en France.

Je parle de plus en plus de ce sujet car je pense qu'il aura un impact majeur sur l'économie dans les décennies à venir.

Pour vous, quels sont les secteurs à privilégier dans ce contexte ?

Source de l'infographie : datagora

Source des données : INSEE

1

3

7

3,838

Mar 19

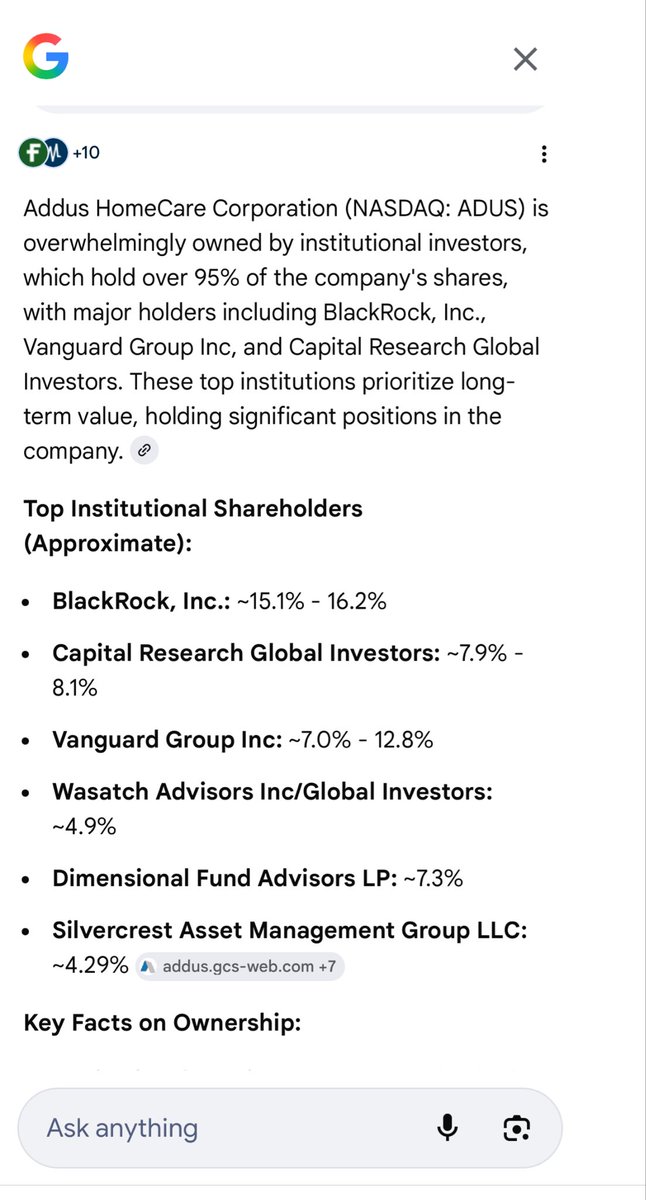

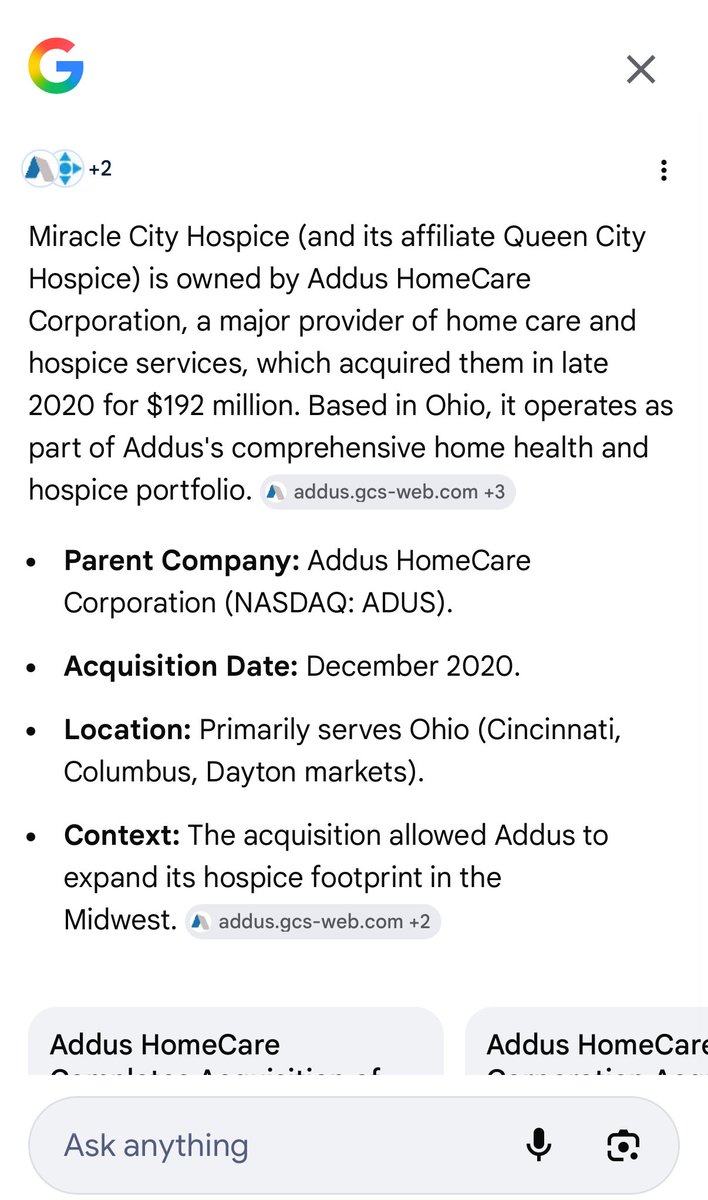

He is not telling the whole story. Who controls the hospice business in this country?

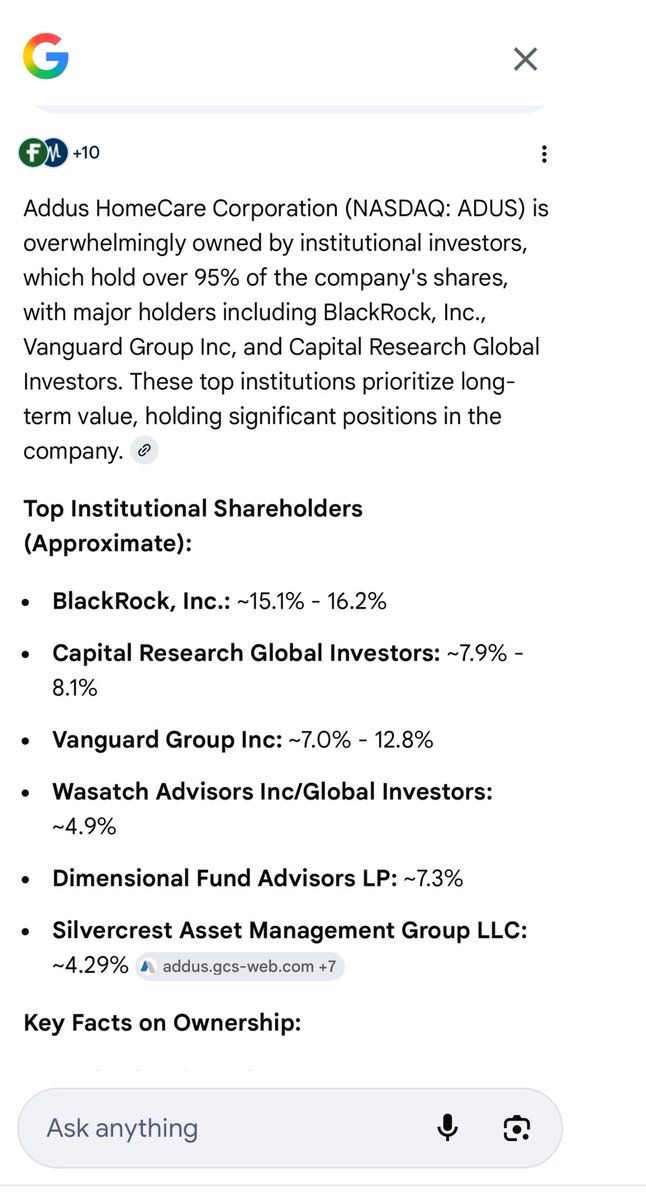

He exposed Miracle City Hospice. Miracle City Hospice is owned by Addus Home Care Corporation. The top shareholders are BlackRock, Vanguard. Same people with many LLCs control the hospice business and everything else in this country. Fraud doesn’t have a color. Hypocrites.

3

2

17

482

Mar 19

He is not telling the whole story and since magatards don’t like to investigate. Who controls the hospice business in this country?

He exposed Miracle City Hospice. Miracle City Hospice is owned by Addus Home Care Corporation. The top shareholders are BlackRock, Vanguard. Same partners with many LLCs. They control all the hospices in the Country. Always the same tribe.

7

1

14

6,644

Mar 18

Miracle City Hospice is owned by Addus Home Care Corporation. The top share holders are BlackRock, Vanguard. They control the Hospices in the Country. Always the same tribe controlling everything in this country

1

5

15

564

Mar 18

Miracle City Hospice is owned by Addus Home Care Corporation. The top share holders are BlackRock, Vanguard. They control the Hospices in the Country. Always the tribe controlling everything in this country

1

4

343

Opérations du jour...

🛒 | Amphenol | 🇺🇸 | 3 ▶️ 31

▫️ Je profite de la forte baisse du jour pour reprendre 3 actions de la société, acteur majeur des interconnexions de semi-conducteurs et des câblages hautes performances ( photonique).

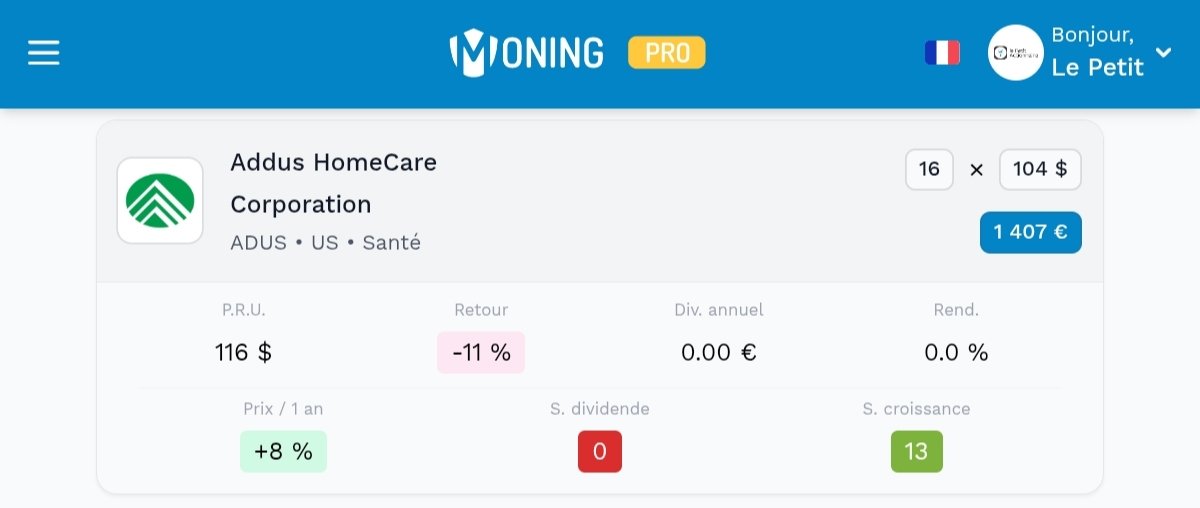

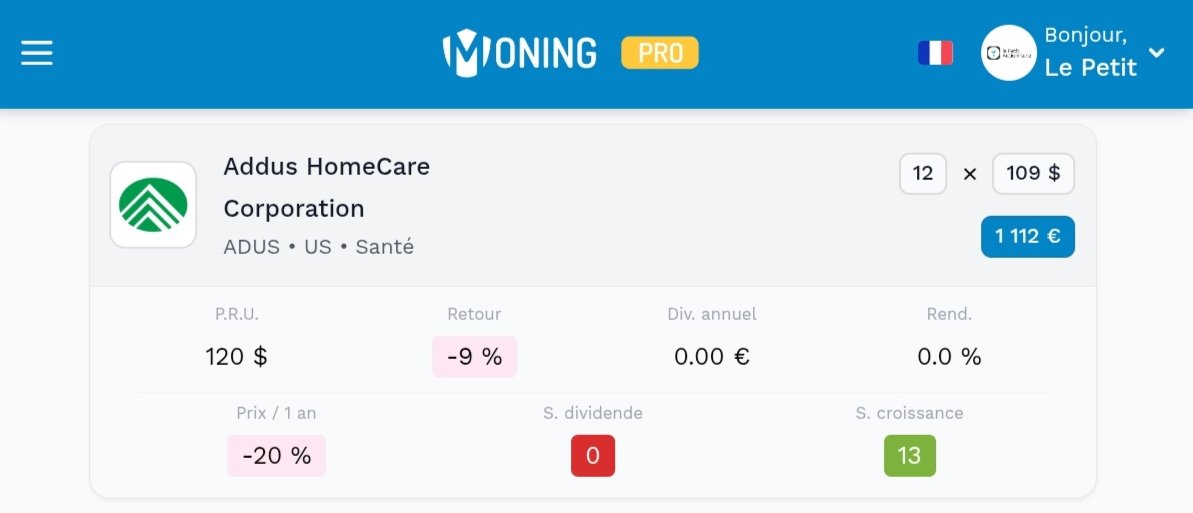

🛒 | Addus Homecare | 🇺🇸 | 2 ▶️ 16

▫️Je poursuis la construction de ma ligne, méga-tendance du vieillissement de la population, sur le spécialiste US des soins à domicile.

20

3,422

Feb 25

Doğu Akdeniz’in Nadide İncisi: Lübnan Türkmenleri

Lübnan’daki Türk nüfusu, 8. yüzyılda Abbasi döneminde Bekaa Vadisi’ne sınır güvenliği amacıyla yerleştirilen Türk askerî birlikleriyle oluşmaya başlamış; Selçuklu ve Osmanlı dönemlerinde Anadolu’dan getirilen Türkmen unsurların iskânıyla kalıcı hâle gelmiştir. Osmanlı Devleti’nin Girit’teki hâkimiyetini kaybetmesinin ardından güvenliği tehlikeye giren Müslüman Türk nüfusun bir kısmı da II. Abdülhamid döneminde Trablusşam ve Bekaa hattına yerleştirilerek bölgedeki Türk varlığı ikinci bir iskân dalgasıyla tahkim edilmiştir.

Bugün Bekaa Vadisi’ndeki Şıhemiye, Addus, Nanaiye ve Duris ile Kuzey Lübnan’daki Kuvaşra ve Aydamun başta olmak üzere; Beyrut ve Trablusşam’da yaşayan Lübnan Türkmenlerinin nüfusu yaklaşık 50.000 civarındadır.

Ancak İslam ülkelerinin çoğunda olduğu gibi mezhep temelli kayıt sistemi ve kamusal hayatın tamamen Arapça olması, bu topluluğu yoğun bir asimilasyon tehdidiyle karşı karşıya bırakmaktadır. Türkçe daha çok yaşlı kuşakların aile içi iletişiminde sınırlı biçimde yaşatılabilmekte ve Eğitim Bakanlığı nezdinde seçmeli ders statüsünde dahi Türkçe eğitimi bulunmamaktadır. Sadece birkaç yıl önce açılmış tek bir Türk Dili ve Edebiyatı bölümü mevcuttur. Arz-ı Mev’ud hedefi doğrultusunda İsrail’in uzun yıllardır sürdürdüğü askerî baskı ve saldırılar karşısında istikrar ve huzur bulamayan Lübnan’da, Türkmenlere yönelik Türkiye’nin kurumsal ve sürdürülebilir ilgi ve desteğinin olmaması da dikkat çekicidir.

#LübnanTürkmenleri #TürkDiasporası #DoğuAkdeniz

1

5

32

813

Feb 10

Caregivers are forced to join SEIU in Illinois. Look into DORS, Help at Home and Addus.

2

6

386

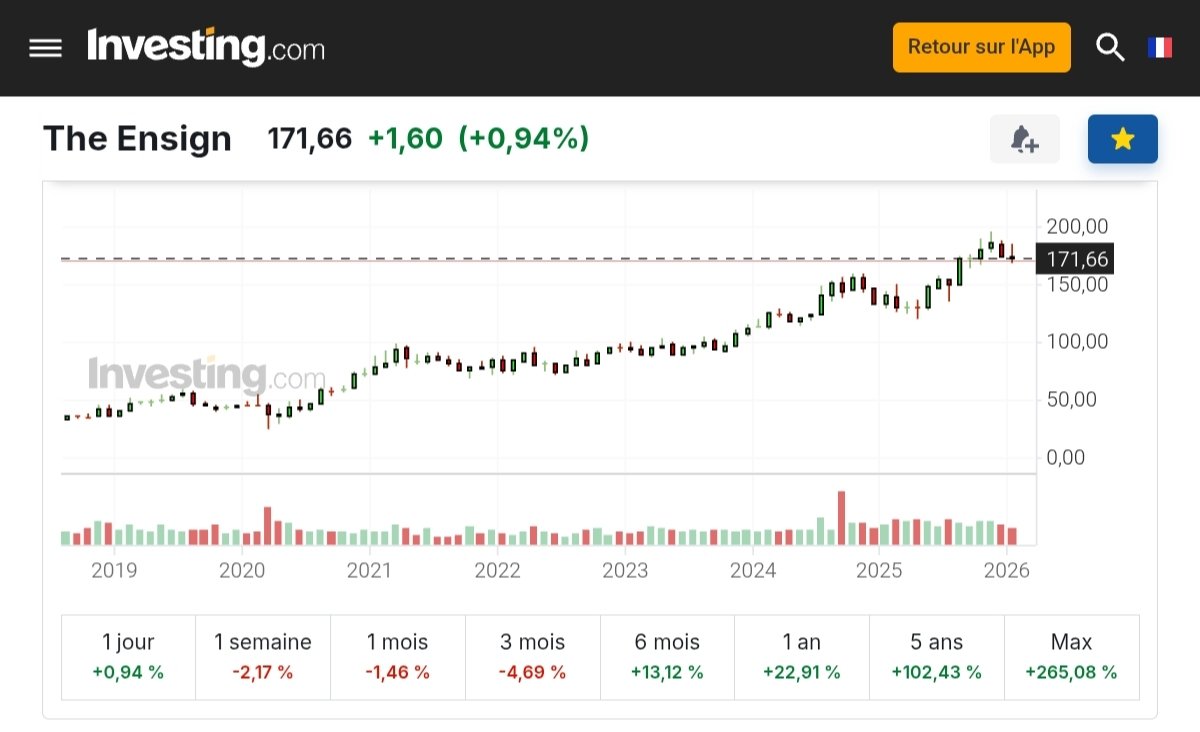

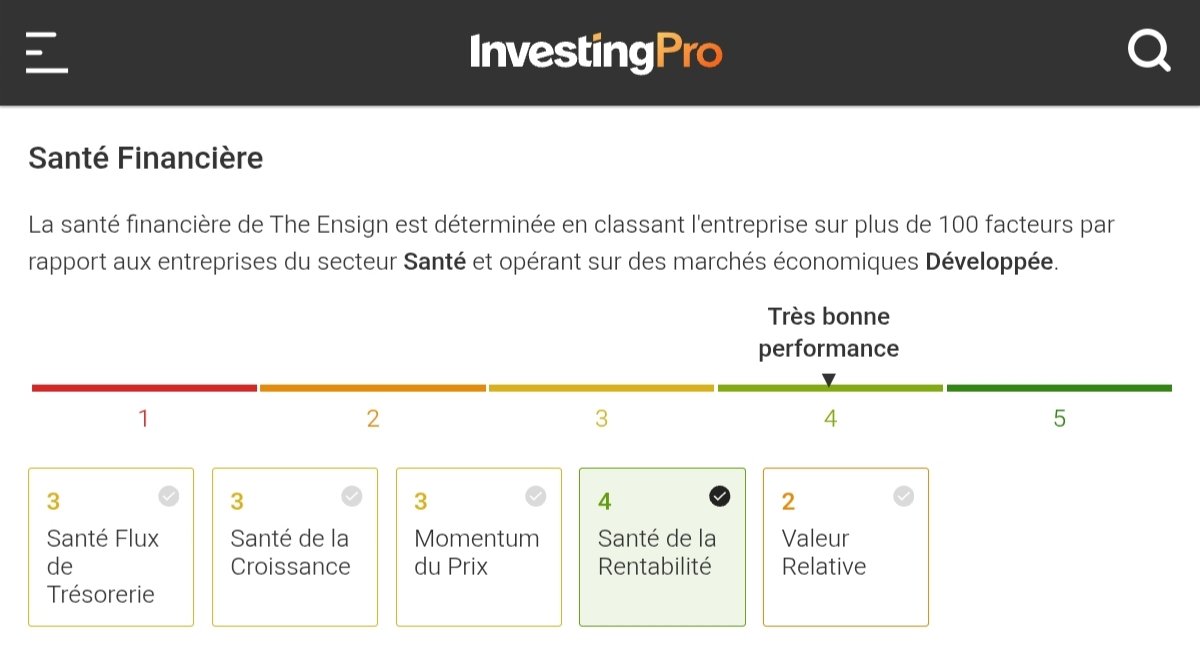

The Ensign Group est en petite correction, désormais à 11,5% de son ATH...

🔎 | Je commence à réfléchir à la possibilité d'effectuer un petit renforcement sur le leader US des soins infirmiers en établissement et de l'hébergement de personnes âgées...

Après avoir effectué un renforcement de ma ligne Addus Homecare (soins infirmiers US à domicile) pas plus tard que la semaine dernière, cela marquerait ma volonté de faire croître mes positions dans ce secteur plutôt défensif qu'est celui du troisième âge.

💵 | The Ensign Group affiche une croissance CAGR de son cours (dividendes intégrés) de 26,4% !

1

14

1,885

Double opération ce soir en portefeuille...

👋 | Allègement The Descartes Syst. Group | 🇨🇦 | -14 ▶️ 14

The Descartes Systems Group est une magnifique entreprise, qui opère dans un secteur hautement stratégique...

Pour autant, le marché rejette totalement, depuis plusieurs semaines les SaaS, sur fond de craintes au sujet de l'IA. Je me décide donc à récupérer une partie de mes liquidités, en prenant une moins-value partielle de 29%.

Je reste très positif à long terme sur la société, dont l'exécution a toujours été excellente. Le reliquat de ma ligne peut potentiellement être cédé afin de libérer de nouvelles liquidités. De la même façon que si des signaux devaient se présenter, de nouveaux renforcements pourraient être envisagés !

🛒 | Renforcement Addus Homecare | 🇺🇸 | 2 ▶️ 14

Face à la situation de plus en plus tendue du côté sur le marché, j'effectue un petit renforcement sur la plus petite de mes positions "troisième âge". Une méga-tendance bien plus défensive que la Technologie et l'IA...

1

11

3,228

La fécondité, et par extension le "Vieillissement de la population" est probablement la méga-tendance la plus ignorée / sournoise qui soit.

🔎 | Tout simplement parce que tout le monde le sait, mais comme ses effets réels, bien que déjà perceptibles aujourd'hui, ne se font sentir qu'à très long terme, tout le monde botte en touche pensant refiler le bébé aux générations futures.

Sauf qu'à "effets (très) long terme", seules des réponses sur de mêmes horizons peuvent éventuellement s'envisager. Les réponses aux défis de demain devraient donc s'envisager dès maintenant !

💵 | Il en est de meme en matière d'investissement... Les positions "Vieillissement de la population" doivent s'envisager dès aujourd'hui... Je dirais même qu'elles auraient dû l'être hier, voire avant-hier. En particulier pour tout ce qui touche à l'être humain.

Alors oui, ce ne sont pas des positions qui vont faire du 100% en six mois seulement. Par contre, elles peuvent apporter une certaine "stabilité" / "prévisibilité" à un portefeuille d'actions.

👋 | Mi-juin 2025, je présentais dans Sous les Radars #9 la canadienne Savaria, spécialiste des solutions d'accessibilité / mobilité, pour personnes handicapées et personnes âgées : 34% (en CAD) depuis.

👋 | Toujours dans Sous les Radars #2, je présentais également The Ensign Group, spécialiste US des centres de soins / réadaptation / hébergement de personnes âgées. C'était le 03 avril 2025 : 32,5% (en USD) depuis et 40% en portefeuille.

👋 | Plus récemment, dans Sous les Radars #27 du 19 octobre 2025, c'est Addus Homecare dont je parlais. Depuis, le spécialiste US des soins à domicile affiche une baisse de 8,2% (en USD) et de -9% dans mon portefeuille.

Dans une grande partie du monde, la fécondité s’effondre.

Chine à 1,0.

Russie à 1,4.

U.S. à 1,6.

Inde désormais à 2,0.

Même les pays historiquement jeunes convergent vers la baisse.

👉 Pourquoi c’est crucial pour les marchés ?

• Moins de naissances = moins d’actifs dans 20 ans → tension sur la production et les retraites

• Vieillissement accéléré = pression budgétaire, dette publique et hausse des impôts

• Ralentissement structurel de la croissance potentielle

• Besoin massif d’automatisation et d’IA pour compenser la main-d’œuvre manquante

💡 Ce que cela implique pour les investisseurs

Le futur appartiendra aux secteurs capables de faire “plus avec moins” : robotique, IA, automatisation industrielle, santé, silver economy, énergies renouvelables, et même immigration qualifiée pour certains pays.

La démographie ne fait pas les gros titres comme l’inflation ou la Fed.

Et pourtant je pense que c’est probablement le facteur le plus sous-estimé pour la Bourse des 30 prochaines années.

📩 Ma newsletter gratuite pour aller plus loin :

lc.cx/LATABLEDESINVESTISSEUR…

#Économie #Bourse #Investissement #Démographie #MarchésFinanciers #Macroéconomie

3

1

13

6,958

En 2025, en France, le nombre de décès a été supérieur, pour la première fois depuis la fin de la seconde guerre mondiale, au nombre de naissances...

▫️651000 contre 645000

🔎 | Une situation qui existe dans la quasi totalité des pays développés...

🔴 | Le "vieillissement de la population" n'est pas qu'une expression, mais bien une réalité ! Une réalité qui s'impose aux cartes économiques et sociales, et qui a déjà commencé à totalement remodeler le monde.

Pourtant, bien que tout le monde ait ou - conscience de la partition qui se joue depuis déjà des décennies maintenant, rares sont ceux qui en profitent réellement. Alors même que le potentiel est énorme !

🎯 | Il est très facile de se positionner sur cette thématique, laquelle est d'ailleurs l'une des méga-tendances les plus fortes et les plus prévisibles...

▫️soins hospitaliers

▫️soins à domicile

▫️hébergement senior

▫️appareils auditifs

▫️solutions d'accessibilité

▫️croisières

▫️casinos

▫️services funéraires

▫️etc.

💵 | Bien que mon exposition à cette thématique soit bien plus faible qu'à celle des Énergies, le troisième âge demeure l'un des axes importants de développement de mon portefeuille d'actions.

Je suis, en effet, déjà positionné sur les hospitalisations, aussi bien en établissements de soins qu'à domicile. Ainsi que sur les services funéraires et l'hébergement de personnes âgées...

▫️The Ensign Group | 🇺🇸 | hospitalisation en établissements et hébergement de personnes âgées)

▫️Addus Homecare | 🇺🇸 | hospitalisation à domicile

▫️Service Corporation International | 🇺🇸 | Services funéraires

🔎 | Cette thématique du troisième âge n'est pas celle à envisager pour obtenir du rêve, ni pour viser des capitalisation complètement folles. Pourtant, les bons acteurs de la thématique délivrent de grosses performances. !

Ainsi, sur les 16 dernières années et dividendes compris...

▫️Addus Homecare a eu une performance CAGR de 16,9%

▫️SCI a réalisé une performance CAGR de 17,7%

▫️Sur exactement la même période, The Ensign Group affiche une performance CAGR de l'ordre de 26,7%

De quoi rendre complètement jaloux le SP500 !

Est-il encore temps d'acheter cette thématique ?

Pour ne considérer que les trois acteurs évoqués dans ce tweet, Addus Homecare affiche un PER 2026 très en-dessous de son historique à 5 ans. Quant à The Ensign Group et SCI, tous deux sont, toujours en 2026, sur des niveaux similaires à leur moyenne à 5 ans.

Aussi, à défaut de dire s'il est encore temps d'acheter ou non, le fait est que ces entreprises, malgré leurs belles performances boursières (même si, récemment, un peu plus compliquée pour Addus Homecare), ne sont pas "moins bon marché" qu'au cours, globalement, des cinq derniers exercices.

3

10

8,648

Oppenheimer Research released a list of its best ideas for small-caps and mid-caps in the new year.

Analysts said that, absent the traditional warning signs that have historically preceded market downturns – narrowing breadth, defensive leadership, and tightening credit – the firm is targeting the S&P 500 (SP500) to reach 7,700. However, should those warning signals emerge and a bear cycle develop, Oppenheimer analysts have set a downside case for the S&P 500 (SP500) at 6,100, corresponding to last summer’s breakout above the pre-tariff peak.

The firm’s best small and mid-cap ideas offer investors exposure to innovators positioned to benefit from several high-growth themes. These include companies tied to the aging population, artificial intelligence, defense technology, health and wellness, internet software platforms, online sports betting, private capital markets, robotics and automation, therapeutic innovation, and the U.S. industrial renaissance.

The diversified selection spans multiple sectors, from biotechnology and healthcare services to technology infrastructure, financial services, and manufacturing, providing broad exposure to transformative trends shaping the economy.

Below is a comprehensive list of Oppenheimer’s best “smidcap” ideas for 2026, along with the rationale behind each price target:

Academy Sports and Outdoors (ASO) — Price Target: $70

The 12- to 18-month price target is predicated on 10-12x the firm’s FY26 (January 2027) EPS estimate of $6.30. This level represents a modest premium to current trading parameters while maintaining a discount to shares of Dick’s Sporting Goods (DKS).

Addus HomeCare Corp. (ADUS) — Price Target: $155

The price target equates to approximately 15x the 2026 EBITDA estimate of $191M, a multiple that is approximately in line with the 5-year average EV/EBITDA for the home health/hospice group.

Amprius Technologies (AMPX) — Price Target: $17

The target is based on 6.0x 2026E revenue of $412M, discounted one year at 15%. Analysts note the multiple is in line with mature battery and advanced material peers, with a higher discount rate applied to account for ramp and technology risk.

Axsome Therapeutics, Inc. (AXSM) — Price Target: $220

Valued using DCF (discounted cash flow) methodology with a 7% discount rate—reflecting risk associated with a commercial-stage biotechnology company—and a -5% terminal value growth rate based on assumed timing for patent expirations. Analysts forecast risk-adjusted peak total revenues of approximately $6.0B in 2038.

Blue Owl Capital Corp. (OBDC) — Price Target: $16

Estimates suggest OBDC can earn a 9.5% ROE. Given an estimated cost of equity capital of 9%, analysts calculate a fair value of $15.72/share, or 1.06x book value.

Centessa Pharmaceuticals plc (CNTA) — Price Target: $62

Valued using DCF methodology with a 10% discount rate, reflecting risk associated with a clinical-stage biotechnology company, and a -1% terminal value growth rate based on assumed timing for patent expirations.

Crinetics Pharmaceuticals (CRNX) — Price Target: $87

Based on a revenue multiples analysis, applying a 6x multiple to estimated peak revenues for paltusotine and atumelnant in their current development indications, in line with the 5-8x industry average. Analysts project peak US/EU paltusotine revenue of $929M in acromegaly (2030) and $941M in carcinoid syndrome (2033), with success probabilities of 100% and 75%, respectively. Peak US/EU atumelnant revenue is estimated at $704M in CAH (2033) and $295M in Cushing’s disease (2035), each with 60% probability of success. A 10% discount rate is applied.

DigitalOcean, Inc. (DOCN) — Price Target: $60

Based on approximately 7x EV/sales on the CY26 revenue estimate, a multiple conservatively below the 10.1x average for infrastructure software and IT service providers. Analysts believe the multiple should improve as both revenue growth and FCF (free cash flow) margins inflect higher.

Gossamer Bio (GOSS) — Price Target: $12

Valued using a sum-of-the-parts methodology with a 30% annual discount rate from peak sales, attributing a 1-10x multiple based on development stage. The valuation assigns a 70% probability of a positive readout in Q1 2026 for seralutinib, which would put the drug on track for potential U.S. and Japanese approval and launch in Q1 2027.

JFrog Ltd. (FROG) — Price Target: $75

Reflects a CY27E EV/sales multiple of 12.5x, justified by technological leadership, a competitive “moat” in binary package management, growth prospects in new market areas including security, AI, compliance, and governance, and potential upside as platform consumption grows.

KBR Inc. (KBR) — Price Target: $60

Derived from a sum-of-the-parts analysis. The STS unit is expected to trade at 12x 2026E EBITDA, a discount to E&C peers due to risk that Lake Charles does not go FID and the company cannot replace Plaquemines by 2027. The MTS unit is expected to trade at 9x 2026E EBITDA, a discount to peers due to government headwinds, smaller scale, and exposure to lower-margin logistics, operations, and readiness/sustainment contracts.

Lyft, Inc. (LYFT) — Price Target: $26

Based on 15x estimated 2026 EBITDA, representing a 3% premium to peers.

Madrigal Pharmaceuticals Inc. (MDGL) — Price Target: $650

Valued using DCF methodology with a WACC (weighted average cost of capital) of 10% and a residual growth rate of -5% due to patent expiration (modeled in 2045). Analysts expect worldwide sales of Rezdiffra in NASH to reach approximately $6.0B at peak (~$4.6B in the U.S.).

McGrath (MGRC) — Price Target: $143

Represents McGrath’s multiple expanding from 7.7x currently to 10x EV/EBITDA on the 2026 adjusted EBITDA estimate of $389M. The company’s 5-year historical average EV/EBITDA multiple is 9.5x, and it has received two publicly confirmed acquisition bids at 10.7x and 10.9x EV/EBITDA.

Modine Manufacturing Co. (MOD) — Price Target: $185

Based on 14.3x FY28E adjusted EBITDA of $701M, a discount to the peer average for HVAC OEMs. The multiple is considered appropriate given MOD’s margin improvement trajectory and increasing contribution of Climate Solutions to company EBITDA.

Nurix Therapeutics (NRIX) — Price Target: $28

Uses a probability-weighted sum-of-the-parts NPV (net present value) methodology, including contributions from NX-2127 sales across multiple indications with success probabilities ranging from 20% to 40%, and NX-5948 in 2L CLL/SLL (60% PoS) and wAIHA (10% PoS). The valuation includes a projected cash position of $1.11/share.

Onto Innovation Inc. (ONTO) — Price Target: $180

Based on a 29.0x 2026E P/E multiple, reflecting a 30.5% premium to the S&P 500’s current multiple. The company has averaged a 30-40% premium since the GenAI boom began in late 2022.

P10, Inc. (PX) — Price Target: $22

Derived by taxing 2026E fund management distributable earnings including equity-based compensation of $1.14/share at 21%, applying a 20% premium to a 22.8x NTM market multiple, and subtracting $3.00 per share of net debt.

Palvella Therapeutics Inc. (PVLA) — Price Target: $200

Calculated using probability-of-success-adjusted, sum-of-the-parts analysis with DCF modeling out to 2038 with no terminal value and a 12% WACC. The model assumes success likelihoods of 85% for Qtorin in microcystic lymphatic malformations, 75% in cutaneous venous malformations, and 60% for both the angiokeratoma and pitavastatin opportunities. Only U.S. opportunities are modeled, and the valuation includes $64M net cash.

Pharvaris (PHVS) — Price Target: $50

Based on an average of multiple and DCF valuation approaches, applying a 6x revenue multiple for HAE to estimated, risk-adjusted global peak revenues of approximately $1.1B for prophylaxis and $350M for on-demand therapy. Models assume a 95% probability of success for on-demand therapy indications and 70% for prophylaxis, using a 14% discount rate.

Porch Group (PRCH) — Price Target: $20

Assumes 25x FY26E EBITDA, a 39% discount to the InsureTech peer average, while estimating FY24-FY27E EBITDA to grow 146% faster than peers.

Pursuit Attractions and Hospitality (PRSU) — Price Target: $48

Based on 12x the 2026 EBITDA estimate. Analysts believe PRSU should trade at a premium to comps (currently ~11x) given its financial flexibility and potential upside from M&A and high ROI projects.

SPX Technologies (SPXC) — Price Target: $240

Equates to a 27.5x P/E multiple on 2026E EPS plus assumed capital deployment, contemplating approximately 1 turn of additional leverage with average post-spin deal economics.

Semtech Corp. (SMTC) — Price Target: $81

Represents 29x the CY27 EPS estimate, in line with the AI peer average. Analysts believe SMTC is well-positioned to gain share in ACC and LPO, while core businesses in LoRa technology and handsets continue to grow at double-digit rates long term. The firm believes SMTC deserves to trade at a premium to the group.

Sensata Technologies Holding PLC (ST) — Price Target: $43

Based on approximately 11x 2027E adjusted EPS versus the stock’s current 10x 2025E multiple. The target anticipates steady operating refinements, sustained positive organic growth with net end-markets stabilized, and balance sheet deleveraging, representing approximately 25% potential upside including a 1.4% dividend yield.

Super Group Ltd. (SGHC) — Price Target: $18

Based on 14x 2026E consolidated EBITDA versus peers at approximately 6x. The premium is considered reasonable given SGHC is growing consolidated EBITDA at a 2024-2026E CAGR of 33% versus peers at 7%.

TeraWulf Inc. (WULF) — Price Target: $20

Based on an EV/MW of approximately $20M on 2027E capacity, supported by a DCF assuming a WACC of 9.0%, 3.5% long-term growth rate, and terminal EBIT of approximately $2B.

Universal Display Corp. (OLED) — Price Target: $185

Based on 32x the 2026 EPS estimate of $5.83, matching the stock’s five-year historical average FY2 P/E. The target reflects positive catalysts including wider OLED adoption in the IT market, recovery of OLED TV sales, production ramp of Gen 8.7 fabs, and commercialization of the blue emitter, offset by macro uncertainty and timing of blue emitter commercial sales.

Via Transportation, Inc. (VIA) — Price Target: $59

Based on a 7x sales multiple applied to the 2027 total revenue forecast of $651M. The firm assumes VIA can expand its sales multiple in the outer year with consistent quarterly earnings reports. The stock currently trades at 4x FTM total revenue estimate of $502M, a two-turn discount to the Tier 1 software group average.

Wave Life Sciences Ltd. (WVE) — Price Target: $32

Valued using DCF methodology with an 11% discount rate, reflecting risk associated with a development-stage biotechnology company with initial proof-of-concept clinical data, and a -5% terminal value growth rate. Analysts forecast WVE’s risk-adjusted total revenues of approximately $1.5B in 2035.

Wix.com Ltd (WIX) — Price Target: $160

Derived from an eight-year DCF projecting a top-line CAGR of 13% and a terminal EBIT margin of 21% (versus mature SaaS peers in the mid-20s). The valuation applies a terminal cash flow multiple of approximately 8.5x, discounted at a WACC of 11%.

2

1

5

687