Giovanni Tarello retweeted

Pietrykowski to typowy karierowicz i pozorant i żadna normalna kobieta nie uwierzy w tą jego tanią autopromocję.

1

1

26

masKi ✌️ retweeted

May 17

At KACHI AUTOPRO, we provide top-quality auto accessories and upgrade solutions to give your ride that look, comfort and performance it deserves ✨

Please muts follow my business page 🫂 @KachiAutoPro

2

7

7

188

masKi ✌️ retweeted

May 26

Where luxury meets reliability.

Quality automobiles, seamless delivery & premium customer experience.

KACHI AUTOPRO 🚘

CUSTOMERS SATISFACTION IS OUR PRIORITY💯

5

18

39

711

Mimikaelo❤️🩹💜🩷🩺🇪🇸 retweeted

8º Crawler Transporter, de Marion Power Shovel Company & Rockwell International (40 m)

Es el vehículo terrestre autopropulsado más grande del mundo. Se utiliza para transportar cohetes y su precio es de 14 millones de dólares. Esta máquina ha aparecido en la película documental ‘Apollo 11′ y en ‘Transformers: El lado oscuro de la Luna’.

2

6

75

41,188

Loro estocástico retweeted

Jun 7

Creo que después de lo de Jon muchos le hemos puesto la cruz al innombrable

Que pegue berrinches el solo y que se autoproclame vencedor

8

6

143

23,089

Jun 7

My name is Mascot Maduagwu Odinakachi

I’m the CEO @KachiAutoPro a trusted automotive brand dedicated to providing quality vehicles spare parts and reliable auto-related services.

At KACHI AUTOPRO, we don’t just sell & fix, we build lasting relationships through integrity, excellence and exceptional services.

CUSTOMERS SATISFACTION IS OUR PRIORITY 💯

11

28

52

6,537

Welcome back Napa Autopro - Sharp Automotive Repair Ltd.!

Thanks for helping keep the wheels turning, the engine running on all cylinders , and Terriers hockey moving full speed ahead.

#yorktonterriers

#welcomeback

#CommunityStrong

#SJHL

4

275

May 7

$GFS INVESTMENT COMMITTEE TAKEAWAY

GlobalFoundries’ May 7, 2026 Investor Day was a materially thesis-enhancing event, but it was not a full de-risking event. Management attempted to re-rate GFS from a mature specialty foundry with cyclical end-market exposure into a differentiated AI infrastructure and physical AI enabler with structurally higher growth, higher margins, higher free cash flow resilience, and a more explicit shareholder return framework. The core message was that GF’s historical absence from leading-edge GPU/CPU manufacturing is becoming less strategically limiting as AI system bottlenecks migrate toward optical connectivity, power delivery, advanced packaging, differentiated RF/analog/mixed-signal, low-power edge compute, and secure geographically diversified manufacturing. That reframing is credible in several areas, especially silicon photonics, SiGe, FDX, BCD, and U.S./Singapore/Germany supply optionality. It remains more speculative in co-packaged optics share capture, data center power share capture, RISC-V/custom silicon monetization, and the speed of physical AI adoption. The event therefore improves the medium-term fundamental narrative but also raises the bar for execution evidence, because the current equity value already discounts a meaningful portion of the 2028 bridge.

STRATEGIC RESET

The Investor Day marked a clear strategic transition from “essential semiconductor foundry” to “holistic technology partner.” Management’s 3 organizing megatrends were rapid scaling of AI data centers, proliferation of AI into the physical world, and the need for resilient global semiconductor supply. The structure of the presentation was deliberately designed to connect these megatrends to GF-specific assets rather than to generic semiconductor demand: silicon photonics and SiGe for optical networking; BCD and GaN for power; FDX, FinFET, eNVM, RF, and RISC-V IP for physical AI; and a cross-qualified U.S., European, and Asian manufacturing footprint for supply assurance. The most important change was not the existence of these technologies individually, most of which have been part of GF’s portfolio for years. The change was management’s assertion that these assets now address the highest-growth bottlenecks in the AI stack and can be monetized through higher-value revenue layers, including technology services, advanced packaging, optical modules, IP licensing, software, and custom silicon.

The strategic logic is strongest where AI infrastructure bottlenecks are visible and near-term. Morgan Stanley has cited more than $700B of 2026 announced capital expenditure by the world’s largest technology companies, up 69% from 2025, with investor debate centered on whether big tech is overbuilding AI infrastructure. GF’s thesis does not require the company to win in the accelerator compute layer. It requires that optical interconnect, power conversion, and supply resilience become increasingly valuable attachment markets around the accelerator layer. That framing is economically attractive because these bottlenecks are no longer peripheral. They directly affect XPU utilization, rack density, power loss, thermal envelopes, and cluster scalability. (Morgan Stanley)

The event also reduced some prior ambiguity around management’s long-term growth algorithm. GF is targeting 10% to 12% through-cycle revenue CAGR, 40% non-IFRS gross margin by exit 2028, 45% longer-term gross margin, 25% non-IFRS operating margin by exit 2028, 35% longer-term operating margin, $4.00 annualized EPS by exit 2028, $6.00 longer-term EPS, approximately 20% net capex intensity through the cycle, and 10% adjusted free cash flow margin. Compared with 2021 to 2025 revenue CAGR of only 1%, this is an aggressive inflection. Compared with 2021 to 2025 non-IFRS gross margin expansion from 16% to 26% and operating margin expansion from 3% to 15%, the margin portion has more historical support than the revenue acceleration portion.

SILICON PHOTONICS IS THE HIGHEST-QUALITY GROWTH VECTOR

Silicon photonics was the most investable portion of the Investor Day because it combined 4 attributes that are rarely present simultaneously: a visible AI infrastructure bottleneck, clear customer urgency, GF-specific manufacturing capability, and explicit revenue targets. GF framed optical networking as a fundamental solution to copper’s reach, bandwidth density, energy efficiency, and compute utilization limitations. The company’s deck argued that beyond 200G per lane, optical becomes the preferred solution, and management highlighted optical’s ability to improve XPU utilization from approximately 15% under copper-constrained architectures to approximately 85% under optical networking assumptions. These utilization claims are illustrative, but the directional conclusion is consistent with the broader industry transition toward higher-radix, lower-latency, lower-power optical interconnect.

The commercial target is material. GF guided to a silicon photonics revenue trajectory that includes a greater than $1B run-rate by 2028 and approximately $2B annual revenue by 2030. The Q&A clarified that the path to 2028 is primarily pluggables, while the post-2028 inflection is expected to come from near-packaged optics and co-packaged optics. This distinction matters because pluggables are closer to current volume economics and customer adoption, while CPO is the higher-content, higher-integration opportunity with greater timing and share uncertainty. The target does not depend entirely on CPO being a 2026 or 2027 revenue event, which makes the silicon photonics bridge more credible than a pure CPO story.

GF’s SCALE announcement is strategically important. The company announced SCALE as an OCI MSA-capable co-packaged optics platform, built on GF silicon photonics, with CWDM and DWDM, bi-directional transmission, demonstrated 8λ and 16λ DWDM capability, photonic devices, TSVs, and fiber-attach approaches designed to support design-to-volume transitions. The OCI MSA itself is meaningful because its founding members include AMD, Broadcom, Meta, Microsoft, Nvidia, and OpenAI, and the specification is intended to create an open, interoperable optical interconnect for AI scale-up that shifts connectivity from a module-centric model toward a silicon-centric model. This provides external validation that the industry is standardizing around the type of optical architecture GF is emphasizing. (GlobalFoundries) (OCI MSA)

The AMF acquisition improves the credibility of GF’s silicon photonics claim. AMF adds a Singapore-based silicon photonics foundry platform, manufacturing assets, IP, talent, R&D, and a 200mm platform that GF plans to scale toward 300mm as market needs grow. GF described the acquisition as establishing the company as the largest pure-play silicon photonics foundry by revenue and as expanding the roadmap for pluggables and co-packaged optics. The strategic value is not only technical; it adds geographic resilience and a second photonics manufacturing center outside the U.S., which matters for hyperscalers and networking customers that increasingly require regional supply optionality. (GlobalFoundries Inc.)

The primary risk in photonics is not whether optical demand grows. The risk is share capture, customer architecture control, and module-level economics. GF’s competitive claim is strong but not yet fully supported by named CPO customers, volume commitments, or detailed share assumptions. In Q&A, management acknowledged that major cloud service providers and system architects may prefer at least 2 sources and that CPO market leadership will be contested. The most relevant debate is whether GF is paid only for wafers and photonic components or captures optical-engine/module-level value. The latter would materially improve revenue and gross profit per AI system, but it also increases execution complexity across assembly, test, fiber attach, EIC/PIC integration, yield, reliability, and customer qualification.

POWER DELIVERY IS STRATEGICALLY PLAUSIBLE BUT LESS DE-RISKED THAN PHOTONICS

The data center power narrative was compelling at the system level. Management’s argument was that AI racks are moving toward much higher power density, higher-voltage DC distribution, fewer power conversion stages, and much faster current transients. GF positioned BCD and GaN as enabling technologies for the transition from energy delivery to intelligent power management. The deck’s selected architecture moved from 800V DC to 48V DC to 6V intermediate bus and then below 1V at the XPU module. GF highlighted 100V GaN for intermediate bus conversion, BCD/GaN integrated voltage regulation, 48V to 6V efficiency around 97%, core VR efficiency above 92%, operating temperature above 125°C, current density above 5A/mm2, fast transient response, integrated high-Q inductors, high-density MIM capacitors, TSV, and wafer-to-wafer bonding.

The revenue ambition is significant: approximately $1B of incremental annual revenue by 2030 from power across mobile, automotive, and data centers. This target is plausible as a portfolio opportunity because GF already has BCD positions in mobile and automotive, Tagore added production-proven Power GaN IP, and AI data centers are forcing system-level redesign in voltage regulation, conversion efficiency, thermal control, and reliability. The Tagore acquisition externally supports the view that GF has been building a power roadmap specifically for automotive, IoT, and AI data center applications. (GlobalFoundries)

The underwriting risk is that data center power is a more fragmented and competitive opportunity than silicon photonics. Incumbents in power semiconductors, controllers, modules, substrates, and power systems have established customer relationships and application-level know-how. GF’s process capability may be necessary but not sufficient unless it is paired with design wins at the module or controller level. The Investor Day provided strong technical mapping but less evidence of named hyperscaler, accelerator, or power-module customer pull compared with photonics. The power target should therefore be treated as a credible option value path rather than a fully de-risked revenue line.

PHYSICAL AI AND RISC-V ARE HIGH-UPSIDED BUT LONGER-DURATION

GF’s physical AI thesis was broader and less immediately quantifiable than the data center thesis. Management defined physical AI as devices that sense, think, act, and communicate in dynamic real-world environments. The identified physical AI SAM was $18B by 2030 across transportation, industrial, consumer, and medical applications. This is a logical extension of GF’s portfolio because these workloads require low power, analog and RF integration, embedded non-volatile memory, sensors, actuation, safety, security, and deterministic compute rather than leading-edge GPU-class logic.

The MIPS and ARC strategy is a major shift in GF’s business model. GF completed the MIPS acquisition in 2025 and agreed to acquire Synopsys’ ARC Processor IP Solutions business in January 2026. The ARC transaction includes ARC-V, ARC-Classic, ARC VPX-DSP, ARC NPX NPU, ASIP tools, and engineering teams, and GF intends to integrate these assets with MIPS to create a more complete processor IP suite tailored to physical AI. The Investor Day described a combined platform with 41 RISC-V and AI cores and 300 customers across MIPS and ARC, with a target of approximately $1B revenue run-rate by 2030 from IP licensing, royalties, software, and custom silicon. (GlobalFoundries Inc.)

The strategic rationale is coherent. GF can use processor IP and software to engage earlier in customer design cycles, increase customer lock-in, increase pull-through to GF manufacturing nodes, and capture higher-margin technology services revenue. FDX and RISC-V also appear naturally paired for real-time, low-power, deterministic workloads in automotive, robotics, industrial automation, wearables, and secure edge devices. The transcript’s humanoid robotic-arm MCU example illustrated the intended architecture-level co-optimization: a RISC-V core above 800MHz, a gigabit MAC, sensor fusion, motion control, and low-power form factor requirements on 22FDX.

The risk is execution and ecosystem depth. RISC-V adoption is real, but Arm remains deeply entrenched across mobile, edge, automotive, and IoT. IP revenue also depends on software support, toolchains, verification quality, safety certification, developer familiarity, and customer willingness to source compute IP from a foundry. The custom silicon layer could broaden GF’s serviceable revenue pool, but it also adds engineering intensity and potential customer-channel complexity. CFO commentary acknowledged that technology services are gross-margin accretive but R&D intensive, which explains why operating margin expands less than gross margin during the early part of the model.

END-MARKET OUTLOOK

GF’s end-market framework is more diversified than in prior cycles. The company’s serviceable addressable market is expected to grow from $75B in 2025 to $120B in 2030, implying roughly 10% CAGR. Management expects GF revenue to outperform the underlying SAM in automotive, IoT, and communications infrastructure and data center, while smart mobile devices are expected to remain roughly flat despite a modestly growing SAM. The intended portfolio mix is to move manufacturing services revenue away from smart mobile concentration, with automotive, IoT, and CI&D representing approximately 75% of manufacturing services revenue by 2030.

Automotive remains a high-quality proof point. GF grew automotive revenue from approximately $0.1B in 2020 to approximately $1.4B in 2025, driven by content rather than vehicle units. Management expects low-double-digit automotive revenue CAGR from 2025 to 2030, supported by 1.5x GF content growth per vehicle, 1.5x automotive design-win growth in 2025 versus 2024, and a position as a leading supplier to the #1 automotive MCU player. FDX radar is the most differentiated automotive example: GF cited 5 to 8 radars per car by 2030, 20 auto customers on FDX, more than 75% receiver-sensitivity improvement versus traditional CMOS, greater than 300m range, less than 0.1° resolution, GF AutoPro qualification at 150°C and ASIL-D, and a sub-3W power envelope.

IoT is positioned as the highest physical AI adjacency. GF expects mid-teens IoT revenue CAGR from 2025 to 2030, supported by more than 200 home and industrial IoT design wins in 2025 and engagement with 7 of the top 8 industrial IDMs. eNVM is a central differentiator because autonomous edge devices need secure code storage, deterministic wake-up, low latency, offline inference capability, and reduced standby/refresh power relative to volatile-memory alternatives. GF’s breadth across eMRAM, ReRAM, and Flash across FDX, FinFET, BCD, and other platforms is strategically relevant. The risk is timing: IoT has a history of large installed-base narratives but uneven monetization, and “physical AI” could be a slower revenue ramp than management implies if robotics, industrial automation, and medical edge AI adoption lag.

Smart mobile devices are no longer the growth engine. Management expects SMD revenue to be roughly flat through 2030, with diversification into alternative form factors such as smart glasses, wearables, hearables, wireless charging, audio, haptics, RF, imaging, display, and power. GF remains deeply engaged, with all top 5 smartphone OEMs and 9 of the top 10 advanced RF suppliers cited as customers, but management appropriately avoided relying on smartphone unit growth. The strategic implication is favorable because flat SMD revenue becomes a stabilizer rather than a thesis driver; however, cyclicality and customer concentration in mobile remain relevant if RF or premium-smartphone demand weakens.

Communications infrastructure and data center is the central growth category. GF expects 30% revenue CAGR from 2025 to 2030, driven by silicon photonics, SiGe, data center power, and satellite communication. Management cited more than 1B cumulative TIA driver IC unit demand by 2030, 4 of the top 5 pluggable transceiver players engaged with GF, more than 70% of data center networking ports becoming optical by 2030, and 3x satellite broadband subscriber growth from 2025 to 2030. SiGe is an underappreciated asset because it is required for high-frequency drivers and transimpedance amplifiers that convert optical signals back into electrical domain at 200G/λ and 400G/λ speeds.

DESIGN-WIN QUALITY AND CUSTOMER TRACTION

The design-win disclosure was one of the strongest leading indicators in the presentation. GF reported more than 500 design wins in 2025, up from approximately 325 in 2024, representing more than 50% growth. Approximately 95% of 2025 design wins were sole-sourced. The company also claimed engagement with all top 6 mobile device fabless and OEM players, 7 of the top 8 industrial IDMs, all top 5 automotive OEMs, 4 of the top 5 U.S. aerospace and defense prime contractors, and all top 4 U.S. hyperscalers. This breadth supports management’s claim that the portfolio has become more embedded across the ecosystem.

However, design wins require careful interpretation. A sole-sourced design win in specialty foundry can indicate differentiated technology, high customer switching cost, or node-specific dependence, but it does not eliminate demand risk, launch risk, customer program risk, ASP risk, or capacity timing risk. Automotive and industrial design wins can take years to convert into production revenue. Hyperscaler engagement is not equivalent to committed volume. The correct investment interpretation is that design-win momentum improves visibility into the 2027 to 2030 plan but is not the same as backlog or take-or-pay revenue.

GEOGRAPHIC FOOTPRINT AND SUPPLY RESILIENCE

GF’s manufacturing footprint is a strategically valuable asset in the current geopolitical environment. Management argued that more than 50% of global greater-than-10nm capacity is located in China and Taiwan, creating vulnerability for automotive, industrial, defense, communications, and AI infrastructure supply chains. GF’s differentiated claim is not merely that it has fabs in multiple geographies, but that it has cross-qualified capacity and technologies across the U.S., Germany, Singapore, and a China-for-China partnership. This creates customer flexibility to design once and manufacture across regions, which is particularly valuable for customers with U.S., European, and Asian regulatory or national security considerations.

The U.S. capacity story is especially important. The U.S. Department of Commerce awarded GF up to $1.587B in direct CHIPS Act funding to support approximately $14B of capital investment over more than 10 years in New York and Vermont, including a new 300mm New York fab, expansion of the existing New York campus for advanced packaging with silicon photonics focus, and modernization of Vermont operations. This directly aligns with GF’s Investor Day emphasis on silicon photonics, advanced packaging, defense, communications, and resilient domestic supply. (NIST)

Government support is both a strength and a risk. The Investor Day cited expected recoveries of 35% to 55% in the U.S., 40% to 50% in Germany, and 30% to 50% in Singapore. These recoveries lower net capex intensity and support margin targets, but they also introduce dependency on policy continuity, milestone timing, compliance, eligibility, and reimbursement mechanics. The company’s own forward-looking statement flagged risks that anticipated funding could be delayed or withheld. The committee-level issue is that reported net capex discipline partly depends on government execution rather than solely on organic capital productivity.

May 7

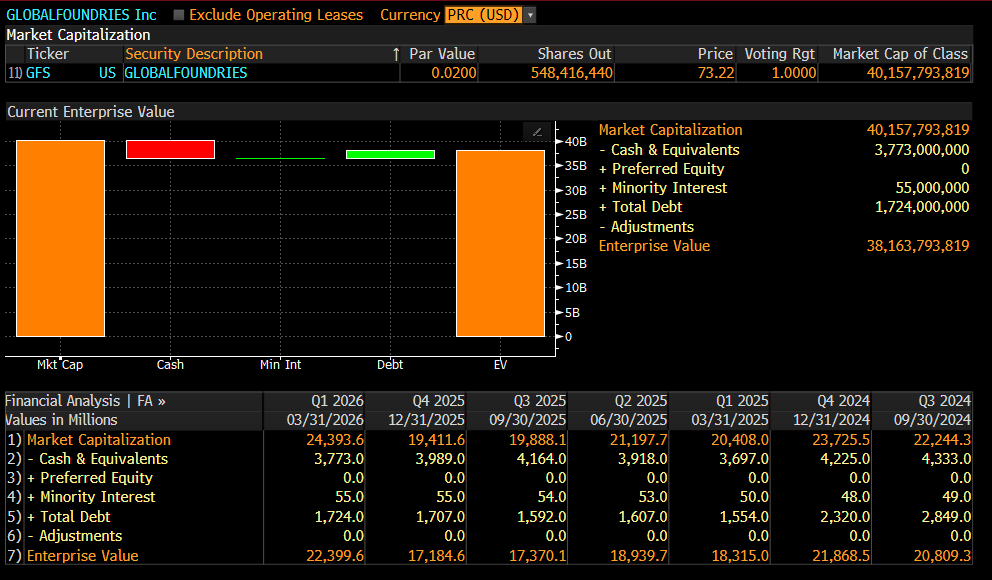

$GFS with $38bn EV and 15x EV/'26 EBITDA. Too cheap for a US-based fab with outstanding optical end markets. Additionally, looking at the materials and depth of information that management provides in calls, presentations, and investor days (now), you know it is a high-quality team that seems to work very well together.

1

1

10

14,552

May 6

Prevent small car scratches from worsening with the AutoPro Car Scratch Eraser. Its water-resistant clear coat formula fills damaged protective layers on any paint color, providing a professional DIY repair in seconds.

unicun.com/product/autopro-c…

#CarCare #AutoMaintenance #DIY

22

Apr 27

At KACHI AUTOPRO, we deliver top-notch car upgrades, accessories, and premium services that keep your vehicle standing out on every road. From stereo upgrades to modern auto enhancements, we bring comfort, class, and durability to your drive🚗 🚘 🚙

Trusted service, quality delivery, and customer satisfaction remain our priority. Your car deserves the best and we make it happen.

📞 Patronize us today and experience excellence on wheels.

@oku_yungx please help retweet and support us.

Thank you 🙏

1

4

2

82