Yoshimitsu Jingu retweeted

Yui Hasegawa y Risa Shimizu estuvieron presentes en el debut de Japón en el Mundial 2026, alentando a los 'Samuráis Azules' ante Países Bajos.

💙🇯🇵 #FIFAWorldCup

17

196

3,259

103,959

𝔻𝕖𝕖𝕡 🍑P𝕖𝕒𝕔𝕙 retweeted

30 Mar 2025

Even though I saw it once, I still want to see Azu jealous again!!!! 🤭

1

1

5

233

🐟 Un cardiólogo lo confirma: las sardinas son una auténtica "bomba de salud" para tu organismo

❤️ Descubre cómo este pescado azul protege tu corazón, mejora el colesterol y potencia tu memoria

cope.es/actualidad/salud-bie…

1

5

14

2,736

#lifestyle cdmx SWLGBTI retweeted

Jun 14

VID SOLD! MILF Azucar Alejandra latina de Fuego … my first cream pie Available Only

loverfans.com/AzucarAlejandr…

#azucaralejandra #mexico #españa #usa #canada

31

77

2,804

55,427

SHA256 retweeted

$MSFT --- $MSFT just delivered Q3 Microsoft Cloud revenue exceeding $54 billion, up a massive 29% YoY. Previously, Azure growth had been hit by capacity constraints due to Nvidia chip shortages and data center power supply bottlenecks. But as Microsoft ramped up Capex in 2026 and optimized its compute supply chain, those Azure capacity gaps are steadily closing. Management expects growth to remain red-hot at 37-38% in coming quarters.

The market had been sweating bullets that Microsoft's aggressive AI capital spending would crush margins — but in the latest quarter, Operating Margin didn't just hold steady, it actually EXPANDED to 46%. The efficiency gains from Azure and Microsoft 365 Copilot perfectly offset infrastructure depreciation costs.

$MSFT shares saw a notable technical pullback from highs back in April, driven by the tariff-induced tech sector rotation. But this selloff had NOTHING to do with deteriorating fundamentals — instead, it created an absolutely juicy "golden entry point" valuation for long-term capital in May and June.

1. The most certain AI monetization flywheel (absolute B2B king)

While most tech companies are still burning cash and telling AI fairy tales, Microsoft has already built the complete closed-loop ecosystem: compute power foundation models (OpenAI) cloud infrastructure (Azure) application layer (M365 Copilot/GitHub).

Enterprises might skip buying flashy AI gimmicks — but they CANNOT live without Word, Excel, Outlook, and Teams.

Microsoft simply needs to raise prices (boost ARPU) via Copilot across its hundreds of millions of existing enterprise subscribers to print money nonstop. This B2B stickiness and per-customer monetization power is unmatched by any other internet company.

2. Decimating cloud competition from above

With generative AI exploding, enterprises increasingly prioritize LLM ecosystems when choosing cloud providers. By deeply integrating OpenAI's cutting-edge models (including the GPT-5 era tech stack), Microsoft has turned Azure into the default choice for deploying enterprise AI applications. This is allowing $MSFT to consistently capture the largest slice of incremental market share vs. AWS and Google Cloud.

3. Bulletproof balance sheet and shareholder returns

Microsoft sports a near-AAA rated balance sheet with hundreds of billions in cash on hand, and Free Cash Flow hitting all-time highs every single year.

In this macro environment of economic volatility and uncertain interest rates, this mega-cap stock — boasting massive cash generation, a 0.93% dividend yield, and ongoing share repurchase programs — is the natural "safe haven" for global institutional capital.

2

8

36

2,309

morrong retweeted

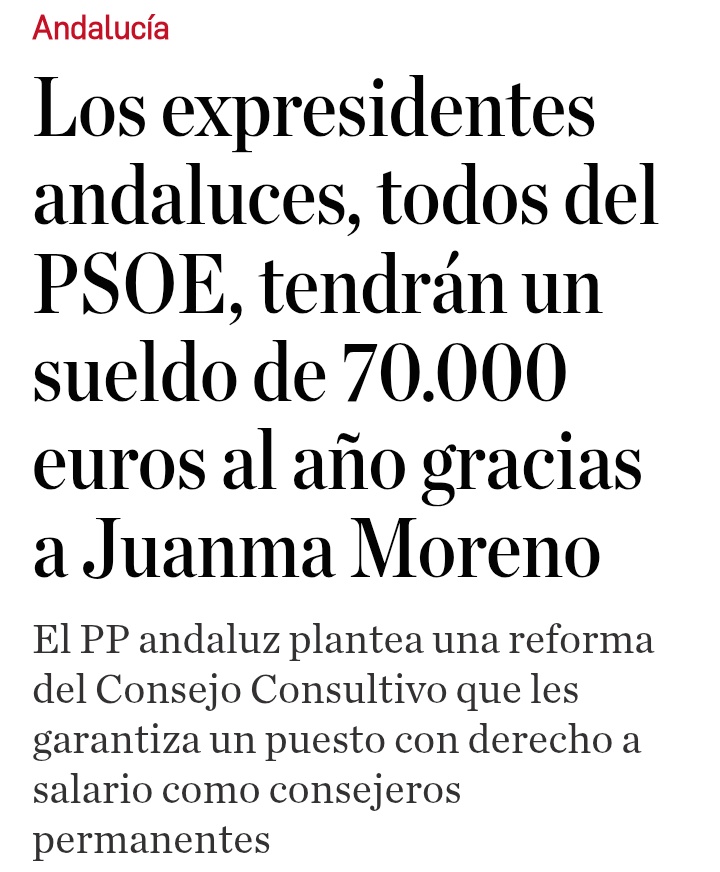

Juanma el moro siempre ha querido que el PSOE BUENO vuelva a Andalucía..... Es otro socialista vestido de azul

1

2

2

124