Started trading forex pairs on Alphax and its really cool

Uid 2846829

@0x_Quant69 @001_lon67622 @BiomeAI

24

xxAutonomyxx retweeted

23 Sep 2025

Thanks @BioProtocol ,Because of you , I got to reward myself with a hearty meal like this

@BiomeAI is truly a successful project that I really love

I’ll keep supporting and spreading the word to friends so the #DeSci community grows even stronger

Now let's continue to accompany Bio, who knows next time we can reward ourselves with an iPhone 17prm too

#BiomeAI #BioProtocol

22 Sep 2025

Chỉ sau 1 ngày mở đăng ký :

$BiomeAI: Oversub 4.3x

$eDMT: Oversub 1.7x

Rõ ràng động lực trong toàn hệ sinh thái @BioProtocol đang tăng tốc mạnh mẽ

Đây mới chỉ là khởi đầu, tuần tới chắc chắn sẽ còn nhiều bất ngờ và cơ hội lớn hơn cho cộng đồng DeSci

173

6

197

9,023

May 16

Latest on Cherrybot.net Trending

1️⃣ BiomeAI | 163.9 % | 808.9K MC

2️⃣ BEPE | 149.6 % | 68.5K MC

3️⃣ HELPCJ | 66.4 % | 16.8K MC

4️⃣ 14 | 57.2 % | 17.9K MC

5️⃣ LUCY | 39.0 % | 72.2K MC

6️⃣ 14 | 27.0 % | 11.6K MC

NFA | DYOR | Trending Alerts updated every 30mins

128

May 11

I used to work an entry-level commission-only sales gig in NYC, made fine money, but I wanted more fulfillment.

So here’s what I did to score my first BD role in crypto (as of Mar 2026):

> joined crypto communities on Discord. DeSci in particular was interesting to me, so I started there

> attended NYC Blockchain events, learned a shit ton and made some incredible friends

> completed a free @Molecule_sci edu course, made connections and even got flown out to Berlin for @DeSciBerlin

> took on some contractual BD work for @psy_dao and @BiomeAI

> quit my job, flew to Argentina for @JoinEdgeCity and @EFDevcon to complete some contracted DeSci work

> made SO MANY FRIENDS and learned SO MUCH ABOUT THE INDUSTRY during my 5 weeks in Argentina

> came back to NYC & began applying to blockchain-related jobs

> had to linkedin DM the sales manager to get a response on my job application, but IT WORKED.

> expressed genuine interest in the position, knowledge about the industry, and a hunger to succeed

> 2 months into my job at @Alchemy and I could not be happier

nobody made this happen but me. I followed my interests, remained authentic, and stayed curious

take risks, be kind, work hard, and you’ll end up EXACTLY where you need to be

May 10

If you didn't break into web3 before 2023, you probably missed the easy way in

I meet people at events all the time who want to get hired in this space. They've read the books, follow the right accounts, know the protocols. None of that gets them through the door anymore.

Web3 hiring used to be wide open. Discord mods became community managers. Community managers became CMOs of the same project a year later. Anyone with curiosity and a network could climb fast because the projects were small and the community was the product.

The projects that survived are real businesses now. RWA wants years of TradFi behind you. Institutional desks want institutional resumes. The soft entry points are gone.

The OGs sometimes act like the path they took is still open. Most of them don't realize they're now the gatekeepers of an industry they once walked into freely.

5

21

3,158

May 3

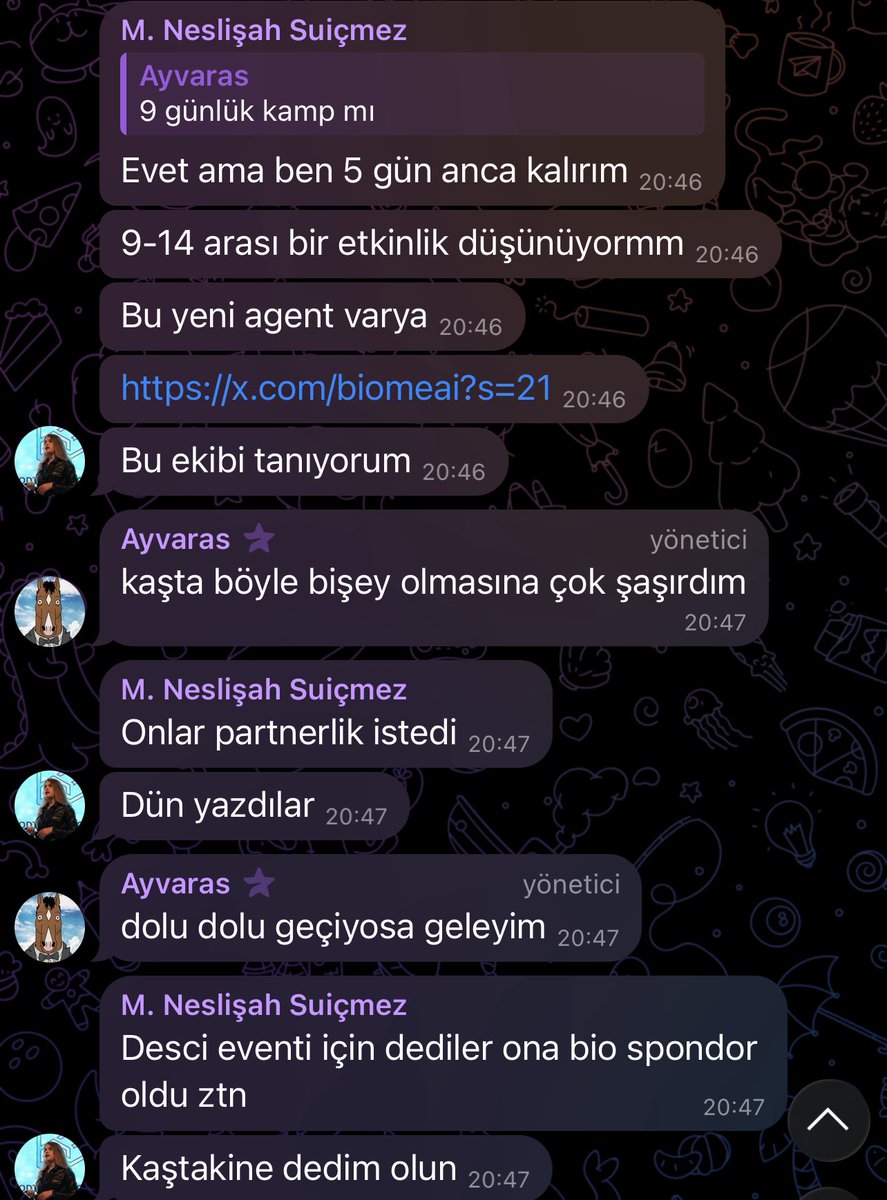

Eda ise Bio team de marketing sorumlusu ikamet Almanya. Almanya lobisi ağır basıyor.

Neslişah Desci bu değil diyip yırtınırken baktı para akıyor proje çıkarıp (ordigenio) kitleyecek. İkamet Almanya yine. Ama DesCi German yerine Desci Türkiye sayfası açıp nerde etkileşim kendisi orda.

BiomeAi sırf kadın diye Türkiye tarafına iteledi. Sonra birşey almadım onlardan dedi , aldığının kanıtı alıntıda. BiomeAi ise RUG.

Feb 4

Neslişah, MicrobiomeDAOdan para aldımmı paylaş dedi… Neslişaha topluluk için BİRŞEYLER (para) ödemişler

EKİBİ TANIYORUM DEMİŞ SPONSOR OLUYORLARMIŞ KAŞ ETKİNLİĞİNE…

Şimdi ise ekip kendini sitelerinden silmiş kayıplara karıştı..

PARALAR NERDE ? RUG ?

2

17

3,305

May 2

Meanwhile we are dropping hot science for free

Apr 13

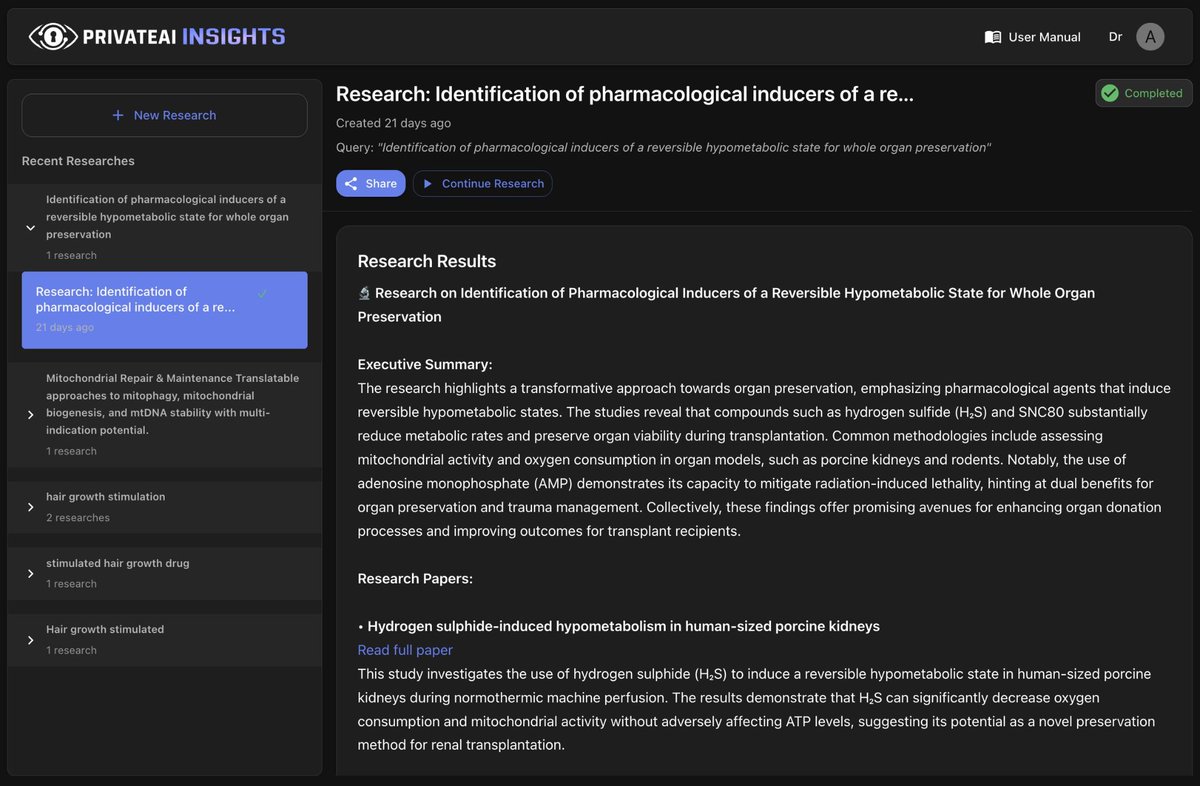

Dev update : Semantic Search powered by $PGPT (1/6):

The problem with keyword search

Scientists waste weeks reading irrelevant papers because search engines match words, not ideas.

A chemistry paper describing vitrification-like processes won't appear when you search "cryoprotection" — even if it's the most relevant result in the field.

PrivateAI finds papers by what they mean, not what they say.

749

May 2

peptide bros finally getting their bull run before the scientists do

2

361

May 2

Interesting to see DeSci gaining steady traction.

These niche narratives tend to expand once broader attention starts flowing in.

1

162

👀

Thesis on solana:bioJ9JTqW62MLz7UKHU69gtKhPpGi1BQhccj2kmSvUJ

Bio Protocol is basically what happens when you take the YC model, strip out the gatekeeping, and rebuild it on-chain for biotech. No big pharma gatekeepers. No opaque R&D pipelines but a community of patients, scientists, and researchers co-owning early-stage medicine from day one.

So what is it actually?

A token-governed launchpad for BioDAOs — community-owned research networks each targeting a specific disease or scientific frontier.

Longevity, neurodegeneration, psychedelics, cryonics, women's health, synthetic biology. The protocol curates which DAOs get admitted, funds their initial raise, manages their secondary market liquidity, and takes a stake in every project it launches. BIO is the connective tissue holding all of it together.

The business model in plain English:

>6.9% equity stake in every BioDAO launched through the protocol

>30% cut of a 1% fee on every secondary market trade of any launched token

>BIO is the mandatory liquidity pair for all project tokens — you need BIO to trade them

>Fees from BioAgent services

>Every sale by any BioDAO is denominated in BIO

One licensing deal, one pharma acquisition, one clinical milestone across any of 60 pipeline projects flows value back to the protocol = structural bet.

Proof of product

Eli Lilly (American multinational pharmaceutical company-- one of the most conservative, credibility-heavy buyers in pharma) paid 300M for Crossbridge Bio — a drug candidate that originated inside the VitaDAO ecosystem. VitaDAO is one of the original BioDAOs running on Bio Protocol. This was the first nine-figure pharma acquisition of IP developed through tokenized, community-governed research.

Pfizer is already running their BixBench benchmarking tool — 59 AI agents, 1,100 hypotheses generated.

The AI angle

Bio Protocol's PeptAI agent designed a novel ADHD drug candidate targeting the OX2R receptor in roughly 24 hours. Validation cost: $1,500. Traditional pharma spends millions and takes years to reach an equivalent decision point. The agent runs a 9-gate pipeline — 8 computational gates, 1 wet lab gate — autonomously, publishes every decision on-chain via Molecule Labs, and pays for wet lab experiments directly from its own wallet.

This isn't the interesting part on its own. The interesting part is what it means structurally: when discovery costs collapse from millions to thousands, a DAO treasury can now fund a candidate all the way to real lab data. That puts entire categories of neglected research within reach that pharma was never going to touch commercially. The biology behind ADHD's orexin system has been documented for years. No institution with the capital chose to develop a drug around it. A BioAgent did.

The pipeline

Eight BioDAOs are currently live.

>VitaDAO ($8M funded, backed by Pfizer Ventures), >CerebrumDAO (struck a deal with Fission Pharma on neurodegeneration),

>CryoDAO ($3M raised, partnered with Oxford >Cryotechnology),

>ValleyDAO ($2M , partnered with Imperial College London),

>AthenaDAO (14 IP deals pending),

>PsyDAO,

>HairDAO,

>Quantum Biology DAO.

PeptAI's ignition sale on Bio Protocol is currently 10.9x oversubscribed — 546K committed against a 50K raise, with 11 days still remaining and 340M BioXP pledged by stakers.

Three new research tokens launched recently — all oversubscribed, 40% demand increase in participation.

Each one of these is a separate pipeline. Each one of these is an additional chance at a pharma exit that reprices the whole protocol. (the structural bet)

The structural problems that still exist

Bio Protocol has been honest about this — the two-engine thesis (community funding agentic AI science) still leaves three unsolved problems.

1) First, data inaccessibility. The training data AI needs to reliably model drug behavior in the body sits locked inside pharmaceutical companies that spent decades collecting it and treat it as a competitive weapon. Molecule is building an open on-chain data layer to address this long-term, but it's not solved.

2) Second, wet labs. Physical validation still requires weeks of contracting and coordination. No amount of AI removes this step. PeptAI routes through Adaptyv Bio for synthesis and SPR validation — that dependency exists and adds friction.

3) Third, clinical trials. Everything DeSci has built reaches the start of the drug development path with something real in hand — a characterized compound, published binding data, permanent on-chain record of every decision. That's a fundamentally different starting point for a pharma conversation. But the clinical stage — three phases, tens to hundreds of millions in cost — is not something the current DeSci stack touches. That gap is real and acknowledged.

The chart context

Token is down -95% from the highs, up ~5X from the lowest point about a month ago.

The Lilly exit happened after most of the price damage. Token is sitting near historical lows relative to what the protocol has actually demonstrated.

Things to keep an eye on right now

>Any licensing deal or pharma acquisition involving a BioDAO project

>PeptAI candidates advancing to wet lab validation and publishing results on-chain

>New BioDAO cohort launches and whether oversubscription trend continues

>Molecule's Science Beach commons gaining traction as an open data layer

>Whether the clinical trial gap starts getting addressed structurally

TLDR (The thesis in one sentence) : a protocol that takes equity in every project it launches, mandates BIO in every trade, and has already produced one nine-figure pharma exit — sitting near all-time lows while the desci/peptide narrative is growing exponentially.

Not financial advice. Do your own research. Follow for more content like this 🫡

1

4

704

May 2

Been doing videos on it, not trending, keywords flopped on youTube... Still early

2

490

May 2

funny thing is i remember you being early to a year ago since speaking to me about it

5

514

We've been covering DeSci projects on gg

$BIO is leading the DeSci movement right now

@paulkhls with @peptai_ designed OX2R-004: a novel 18-residue peptide agonist for ADHD in 24 hours = Wet-lab validation just $1,500

Human genome cost $100 M in 2001 and $100 today.

A million-fold compression in 20 years.

AI is doing to wet-lab biology what it already did to sequencing. Drug discovery is the next cost curve to fall off a cliff and @BioProtocol is positioned as the funding index layer for the AI agents pulling it down:

→ @peptai_ autonomous peptide drug discovery

→ @Molecule_sci IP-NFT marketplace

→ @valley_dao longevity

→ @psy_dao psychedelic medicine

2

142

May 2

u think peptide hype sticks or we get a full retrace once buzz fades

2

189

May 2

seems like I need to pay real attention to that.

being a while I checked up the ones I had on my watchlist

2

169