On June 14, 1777, the Continental Congress agreed to the design of the first American flag. Flag Day celebrates this classic symbol, Old Glory. Flag Day was first officially celebrated in 1916, and, in 1949, President Harry Truman signed the formal observance into law. This weekend, we celebrate the Stars and Stripes as a living reminder of the history, freedom, and unity of the United States of America. At First Northern Bank and Trust, we are honored to fly the flag every day.

#BankLocal #CommunityBanking

ALT American flags displayed on porches with flowers blooming from trees.

16

ALT Dog wearing a harness.

4

ALT Dog with his tongue hanging out of his mouth.

4

We care about our neighbors. That's why banking with First Savings and Loan is personal every time.

#FirstSavings #LocalLending #MebaneNC #CommunityBank #TrustedLocal #banklocal

6

ALT Friendly, fluffy dog.

4

Jun 11

It's not often that someone who spends so much time helping others receives the spotlight themselves.

We're proud to celebrate Locality Bank Co-Founder and Chief Technical Officer, Corey LeBlanc, on being named Banker of the Year by the Florida Bankers Association.

This recognition honors not only his contributions to banking but also his impact on colleagues, customers, communities, and the industry as a whole.

Congratulations, Corey, on this well-deserved honor!

Member FDIC

#localitybank #banklocal #fba #bankeroftheyear #recognition #congratulations #coreyleblanc #floridabankers #banking #communitybank #community

1

16

June is a great month to start building smarter financial habits. From online banking tools to savings accounts designed to help you grow — we’re always happy to help! #FirstSouthernBank #BankLocal First Southern Bank is a Member FDIC and Equal Housing Lender.

10

Jun 11

America's #CommunityBanks are systemically important to Main Street! #BankLocal youtu.be/C9xCH1fDBXA?si=TmDz…

3

80

When you bank with First Savings and Loan, your money stays local. Ready to get banking? Click below!

firstsavingsmebane.com/conta…

#FirstSavings #LocalLending #MebaneNC #CommunityBank #TrustedLocal #banklocal

15

First Northern Bank and Trust representatives Bobbie Jo Kleppinger and Diane Perry recently attended the Carbon County Community Foundation banquet at the Blue Mountain Resort. They had an enjoyable time at the event, which included community awards, a silent auction, and a DJ and dancing. Celebrating the Foundation’s 10th Anniversary, this event raised funds to support operations and their Fund for Carbon County.

#BankLocal #CommunityBanking

ALT Two professional businesswomen, metallic couples dance under party streamers, balloons, and lights.

33

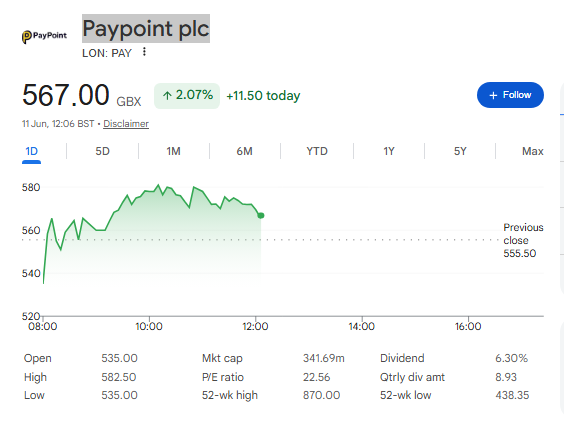

🚨 $PAY (PayPoint plc) FY2026 Earnings

Record profits shareholder returns… while reorganizing for growth 👀

________________________________________

📊 KEY METRICS (Full Year)

🔹 Net Revenue: £190.8M ( 1.7% YoY) 🟢

🔹 Underlying Pre-Tax Profit: £69M ( 1.5% YoY) 🟢

🔹 Underlying EBITDA: £92M 🟢

🔹 Diluted Underlying EPS: £0.736 ( 6.5% YoY) 🟢

🔹 Final Dividend: £0.20/share ( 2%) 🟢

🔹 Total Shareholder Returns: >£90M (buybacks dividends) 🟢

👉 Core takeaway:

Resilient performance with strong capital return

________________________________________

📈 SEGMENT PERFORMANCE

🟢 Shopping & Payments/Banking: Growth

🟢 Love2shop: Stronger profit & revenue

🔴 E-commerce: Declined (new commercial terms)

👉 This is:

Diversified payments & retail services business

________________________________________

🚀 STRATEGIC MOVE

🟢 Reorganizing into four business units

🟢 Clearer accountability & faster execution

🟢 Key initiatives progressing: BankLocal, Royal Mail Shop, Collect

👉 Impact:

Positioned for accelerated revenue growth

________________________________________

⚡ WHAT’S HAPPENING?

• Delivered record underlying profit despite earlier headwinds

• Strong H2 resilience

• Major internal restructure underway

👉 This is:

Maturing UK payments/retail services company entering next growth phase

________________________________________

📅 OUTLOOK

🔹 Net Revenue Growth Target: 5% – 8% annually

🔹 FY2027 Underlying Profit: Expected to exceed FY2026

🔹 Results expected in line with market forecasts

👉 Important: Clear growth framework now in place

________________________________________

🧠 WHAT’S ACTUALLY WORKING

🟢 Record profitability

🟢 Consistent shareholder returns (>£90M)

🟢 Dividend growth

🟢 Multiple growth initiatives gaining traction

🟢 Strong balance sheet & cash generation

________________________________________

⚠️ WEAK SPOTS

🔻 Modest overall revenue growth ( 1.7%)

🔻 Mixed divisional performance (E-commerce drag)

🔻 Execution risk on reorganization

👉 Still: Needs to prove consistent mid-single digit growth

________________________________________

🧠 MARKET SIGNAL

👉 UK-listed payments & convenience retail services play

• Defensive cash flow

• High shareholder returns

• Growth restructuring underway

________________________________________

🔥 BULL vs BEAR

🟢 Bull Case

• Hits 5–8% revenue growth target

• Reorganization unlocks efficiency & acceleration

• Continued generous dividends buybacks

🔴 Bear Case

• Growth stays low-single digit

• E-commerce weakness persists

• Reorg execution takes longer than expected

________________________________________

💭 CONCLUSION

$PAY delivered record profits, hiked the dividend, and is restructuring for faster growth…

👉 A defensive, cash-generative business with improving momentum.

________________________________________

👀 KEY QUESTION

Can PayPoint consistently deliver 5–8% revenue growth post-reorganization?

1

49

Jun 10

This June we’re proud to celebrate our employee work anniversaries. Thank you for your dedication and hard work over the years—here’s to many more with Bank of Clarke! #banklocal

1

10

Jun 10

We are excited to welcome the first participants in Currency Bank’s Summer Internship Program.

Welcome Khushi, Mikhil and Lohan!

Throughout the summer, these students will gain exposure to the day to day operations of a growing entrepreneurial bank.

#BankLocal

89

Jun 10

Visit our Stephens City branch Friday, June 12th or Friday, June 26th from 10 AM - 2 PM to talk with Joyce Stabile, one of our knowledgeable mortgage officers. She's here to help with all your mortgage needs! #banklocal

3

Jun 10

This week, Locality Bank Co-Founder and CEO Keith Costello concludes his term as Chairman of the Florida Bankers Association.

Over the past year, Keith has represented Florida's banking industry while championing the vital role community banks play in supporting local businesses and the communities they serve.

We're incredibly proud of his leadership and grateful for the dedication and impact he has demonstrated throughout his term.

Member FDIC

#localitybank #banklocal #localbank #chairman #pastchair #fba #leadership #keithcostello #southflorida #floridabankers #community #communitybank

9

Nationwide Building Society is live with the PayPoint | BankLocal service! This means Nationwide customers can deposit up to £300 cash in stores enabled for debit card deposits. Find a location: bit.ly/4cVrC3V

1

63

ALT Small dog standing on a table.

1

Need assistance after hours? First Southern Bank’s Express 24-Hour Telephone Banking Service is available whenever you need it. Call 866-452-0015!

We’re here to help — day or night! #FSB #BankLocal First Southern Bank is a Member FDIC and Equal Housing Lender

13

Vacation plans? Keep your finances simple with All-in-one Banking. One bank, all of your accounts, and premium benefits.

Learn more: shorturl.at/nbV2U

#FinancialGoals #AllInOneBanking #TrackYourMoney #SimplifySaveSucceedWithTheFirst #TheFirst #BucksCounty #BucksCountyPA #LocalBanking #BankLocal #MoneyMadeSimple

10

❤️ Local decisions. Local service. Local commitment. When you bank with a community bank, your money helps support the people and businesses right here at home. #BankLocal #CommunityMatters