Jun 13

Containers Tumble From Boxship onto Bunker Vessel in Antwerp share.google/6lDu7gGLCUlmtTw…

12

Jun 10

Maritime risk is back the hard way. An MSC boxship was struck in an Iraqi port June 1, and piracy is resurging off Yemen as navies redeploy to the Gulf. War-risk premiums and reroutes don't show up in the headline rate index — they land on your invoice. Price the risk in.

Jun 7

4. 📈 CMA CGM SECURES INDUSTRY-LARGEST ORDERBOOK WITH FRESH BOXSHIP SERIES

Expanding its aggressive fleet dominance, CMA CGM has finalized a new shipbuilding contract with China's Hengli Heavy Industries for eight 6,000 TEU containerships. Alphaliner intelligence confirms that the French carrier now holds the global industry's largest active orderbook, boasting over 150 vessels on order to counter structural fleet depletion from long-haul Cape of Good Hope routing.

1

69

Jun 4

MTT Shipping pushes fleet growth strategy forward with Wuhu boxship deal dlvr.it/TStG1h

1

6

646

⚓️ The Quiet Decarbonisation: New Ships, Conventional Fuels

Lloyd's List reports a shift in the boxship orderbook. Alternative fuel orders have stalled. Conventional-fuel feeders and mid-size vessels are back.

The logic is simple: a modern conventional newbuild is 20–30% more efficient than the 15-year-old tonnage it replaces. Lower fuel burn. Lower emissions. No methanol infrastructure required.

This is not the IMO's ideal pathway. But it is the pragmatic one. Fleet renewal is doing more for near-term decarbonisation than alternative fuel mandates.

Cleaner ships are being built. They just aren't running on green fuel yet.

#ContainerShipping #Decarbonisation #IMO #Newbuilds #Shipping

1

5

14

297

⚓️ Yangzijiang Buys 10% of Seaspan — The China-West Connection

A Chinese shipyard just bought a piece of the world's largest containership lessor.

Singapore-listed Yangzijiang Shipbuilding paid $825.7 million for a 10% stake in Poseidon Acquisition Corp—the holding company behind Seaspan. All funded from internal cash. No debt. No external raise.

The strategic logic:

• Yangzijiang has built Seaspan's ships for 20 years. Now it owns part of the customer.

• Seaspan operates ~ abt 190 vessels (1.9 million TEU) with dozens more on order—roughly 10–15% of Yangzijiang's containership orderbook.

• The deal gives the yard visibility into future demand, production planning, and a board seat.

The China-West connection:

A Chinese yard now holds equity in a historically Western/Canadian-linked lessor.

Meanwhile, Japan's Ocean Network Express (ONE) increased its stake to nearly 49%. Fairfax Financial (Canada) and the Washington family sold down.

The result: a Chinese shipbuilder and a Japanese carrier now have some control in world's largest independent boxship owner.

Vertical integration is reshaping the container shipping supply chain. Builders want a seat at the owner's table.

#Yangzijiang #Seaspan #ContainerShipping #Singapore #Shipbuilding @Center_MTR

2

6

284

Video: MSC Boxship Holed During Two Attacks by IRGC While Sailing off Iraq

#MSCBoxship #MaritimeSecurity #IRGC #ShippingNews #IraqWaters

maritime-executive.com/artic…

2

3

256

May 31

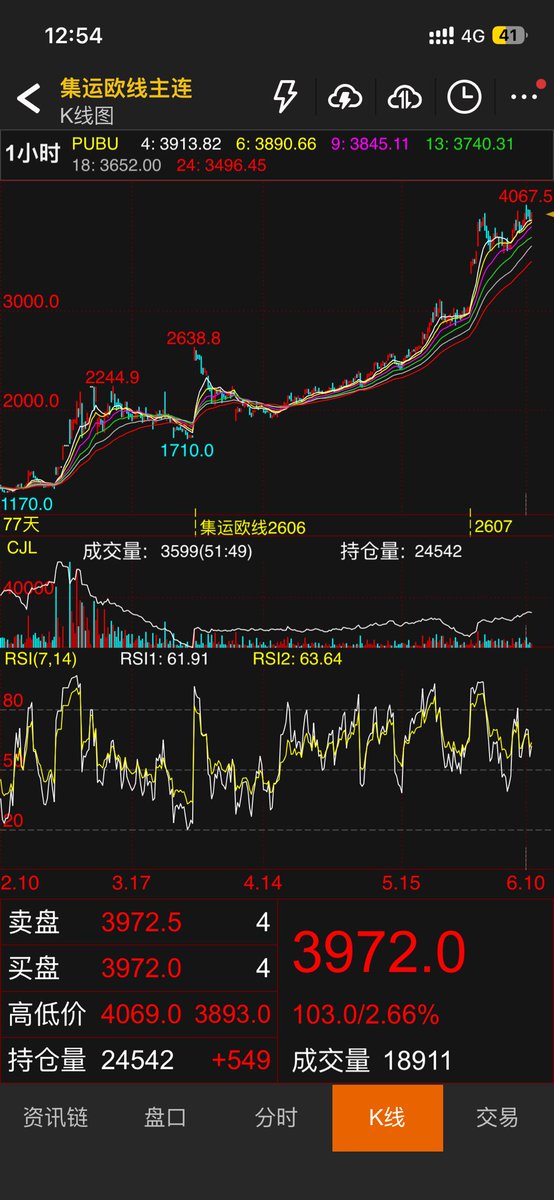

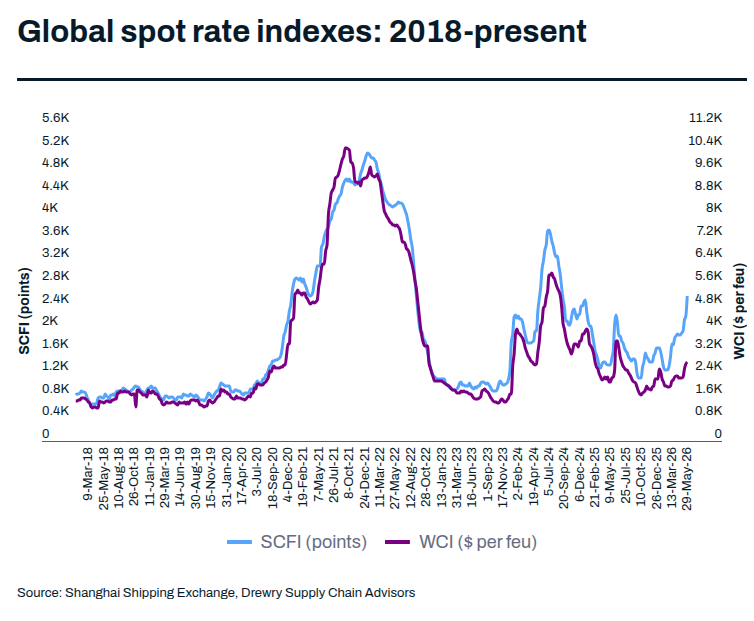

Hormuz crisis side effect: a sharp rise in container shipping rates | Greg Miller, Lloyd's List

- SCFI global composite index has doubled since the war with Iran began and is at its highest point since September 2024, during the Red Sea crisis

- Bunker fuel costs have jumped by almost 70% and container lines are successfully passing incremental costs along to shippers

- Shanghai-Los Angeles spot rates are up 59% vs late February, with Shanghai-New York rates up 66%, according to Drewry assessments

---

Spot container freight rates continue their ascent as ocean carriers pass along much higher fuel costs resulting from the effective closure of the Strait of Hormuz. If the strait doesn’t reopen soon, the impact on container market could intensify

IMPORTERS of containerised goods around the globe are paying more for their ocean transport as a result of the Hormuz crisis.

In yet another side effect of the Middle East war, container lines are successfully passing along fuel costs inflated by the effective closure of the Strait of Hormuz.

The Shanghai Containerized Freight Index global composite rose to 2,572 points in the week ending Friday, up 16% from the week before. It is now double its level in late February, just before the US and Israel attacked Iran.

This week’s SCFI global composite reading was the highest since the week of September 6, 2024, during the Red Sea crisis.

Impact of higher bunker fuel costs

“Geopolitical tensions in the Middle East are weighing on sentiment, with elevated bunker costs and fuel surcharges adding upward pressure across trade lanes,” said Drewry.

Maersk chief executive Vincent Clerc said in a conference call that his company is paying around $500m per month in extra fuel costs due to the Hormuz crisis “that we must find a way to pass through”.

Hapag-Lloyd chief executive Rolf Habben Jansen said that his company is paying €50m-€60m extra per week ($250m-$300m per month) and “rate increases have been roughly in line with the cost increase we have faced”.

When importers pay more for ocean freight, it is the same as “when you go to the petrol station and you have to pay a higher price”, said Habben Jansen.

Pass-along fuel costs may also be affecting peak season timing, further boosting spot rates.

“Demand is being pulled forward into June ahead of the expected July 1 bunker fuel adjustments, supporting stronger shipment flows,” said Drewry, citing “early peak season” trends in both the transpacific and Asia-Europe trades.

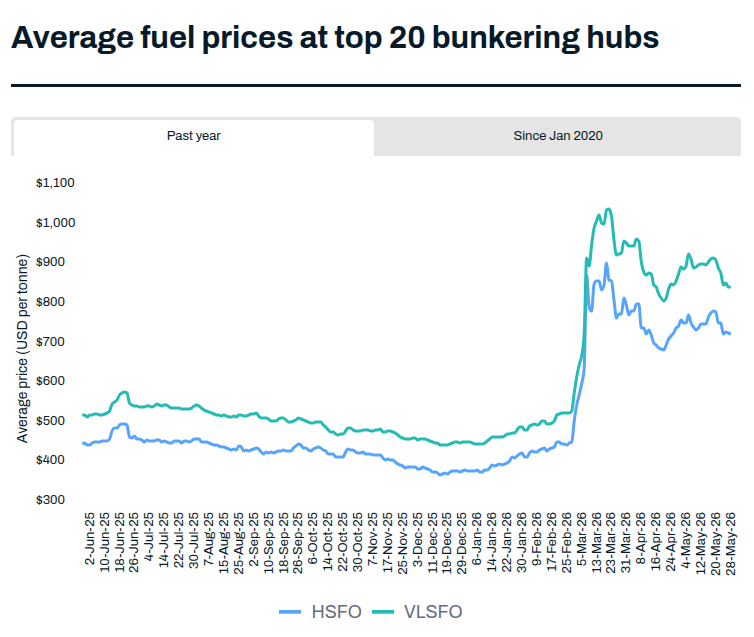

The average price of very low sulphur fuel at the top 20 bunkering hubs was $856 per tonne on Thursday, up 68% from mid-February, according to data from Ship & Bunker.

The average price of high sulphur fuel oil was $736.50 per tonne on Thursday, up 66% versus mid-February.

VLSFO pricing moves in line with Brent crude. The Brent price would decline if there is a peace agreement between the US and Iran, or surge if the Strait of Hormuz remains effectively closed for longer.

Neil Chapman, senior vice president of ExxonMobil, issued a blunt public warning on Thursday, asserting that the dated Brent price could spike to $150-$160 per barrel if the strait doesn’t reopen in the next few weeks.

If Brent goes higher, bunker costs — and shipper fuel surcharges — would also rise.

Disruption helps offset capacity overhang

The good news for carriers is that, so far, they have been able to offset fuel costs despite an ongoing flood of newbuilding capacity.

Their ability to do so relates, in part, to the Hormuz crisis.

Liners’ continued aversion to the Red Sea route amid the war in the Middle East reduces effective capacity by 12%, said Constatin Baack, chief executive of boxship lessor MPC Container Ships, on a quarterly call on Wednesday.

Slow steaming due to higher bunker costs has absorbed another 2% of capacity. “With energy prices up sharply, carriers have throttled back fleet speeds,” Baack said.

Port congestion takes out another 5% of capacity, bringing the total reduction of effective capacity to 19%.

“On paper, supply and demand have been diverging since 2023. The market should be trending toward oversupply,” said Baack. “In reality, rates have been increasing.”

According to Peter Sand, chief analyst at Xeneta, “Carriers entered the year facing a potential market collapse as services [were expected to return] to the Red Sea, but have ultimately found themselves able to charge higher and higher rates to shippers across the market.”

Asia-Europe spot rates

Different spot index providers use different methodologies and come up with different rate assessments, but they all show the same directional trend.

The SCFI Shanghai-Mediterranean index was at $7,500 per feu this week, up 63% versus the last week of February, just before the war began. It was the index’s highest reading since January 2025.

Drewry’s World Container Index assessed the Shanghai-Genoa spot rate at $4,253 per feu, up 50% versus late February.

Xeneta’s daily assessment of average short-term rates on the Asia-Med route was $4,326 per feu on Thursday, up 30% compared to pre-war levels.

The SCFI’s Shanghai-North Europe index was at $4,949 per feu this week, up 74% versus late February to its highest point since January 2025.

The WCI Shanghai-Rotterdam index was at $2,861 per feu, up 37% since before the war, and Xeneta’s Asia-North Europe assessment was at $2,880 per feu, up 30%.

“As the early peak season approaches and carriers continue to raise FAK rates, we expect rates to rise further in the coming weeks,” said Drewry.

Transpacific spot rates

US importers are now dealing with two policy decisions of US President Donald Trump: the attack on Iran and tariffs.

US importers continue to face steep tariff bills on top of rising freight costs due to fuel, even after the Supreme Court ruled against Trump’s emergency tariffs in February.

According to the Budget Lab at Yale, the current average tariff rate paid by US importers is 11.8%, the highest since the 1940s, excluding 2025. That is almost six times the 2% average at the beginning of Trump’s second term.

Nevertheless, US import demand remains resilient, supporting recent spot rate gains by carriers.

The SCFI Shanghai-US west coast index was at $4,149 per feu this week, up 129% versus late February. The SCFI Shanghai-US east coast index was at $5,333 per feu, up 100%.

A year ago, Asia-US spot rates were even higher, as that was the period when Trump gave a temporary tariff reprieve, allowing US importers to frontload.

The WCI assessed Shanghai-Los Angeles rates at $3,473 per feu this week, up 59% from late February, and Shanghai-New York rates at $4,597 per feu, up 66%.

“With early peak-season trends emerging and seasonal demand strengthening through June, we expect further upward pressure on [transpacific] rates,” said Drewry.

Xeneta’s assessment of average Asia-US west coast spot rates came in at $3,624 per feu on Thursday, up 74% versus late February. Xeneta’s Asia-US east coast assessment was $4,367 per feu, up 65%.

“There is no hiding place from this market turmoil,” said Sand.

“The June increases on the transpacific were driven mainly by the market mid-low [the midpoint between the low and the average], which are the rates generally paid by the larger-volume shippers who command greater negotiating power.”

lloydslist.com/LL1157327/Hor…

2

1

12

1,585

May 27

The single-ship company that legally owns Ernest Russ boxship Solong is entitled to limit financial liability following its high-profile allision with a Stena tanker in the North Sea last year, the High Court has ruled

lloydslist.com/LL1157299/Sol…

1

2

1,108

North Sea, May 21 — Small fishing vessel Stella Polaris (9 kts, S) sustained severe wheelhouse damage in a crossing collision with the megamax boxship Singapore Express (7-8 kts, E). Despite the impact north of Terschelling, only one minor injury was reported. The fishing vessel was towed to Harlingen; the 24,000 TEU container ship continued to Hamburg

maritime-executive.com/artic…

2

3

229

May 24

CMA CGM Notre-Dame de Paris, world's largest LNG boxship, completes maiden Shanghai call! 🇫🇷🌊

shipping-daily.com/index/ind…

#GreenShipping #CMA_CGM

1

2

58

May 20

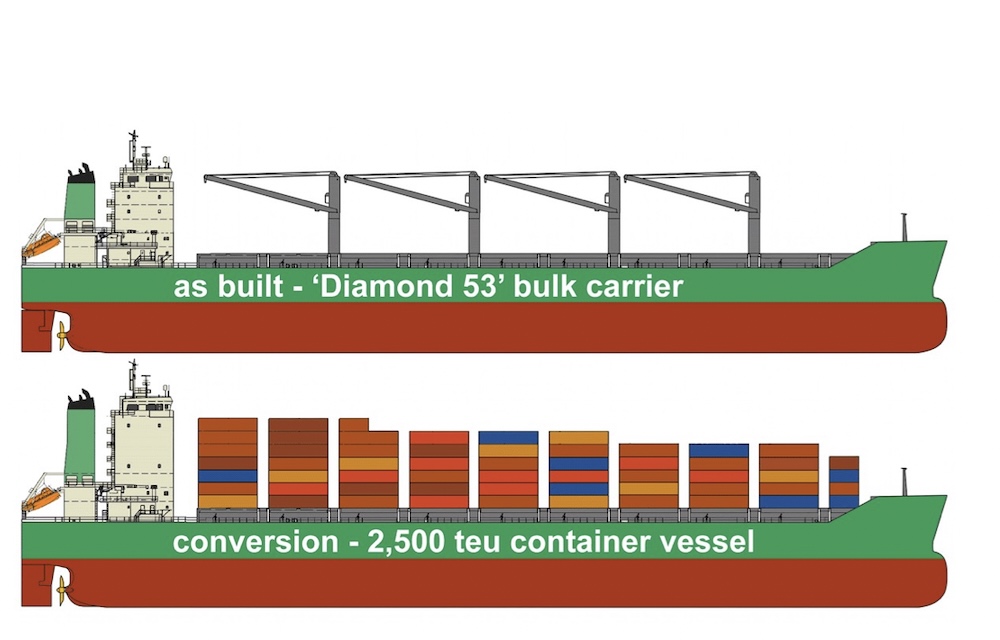

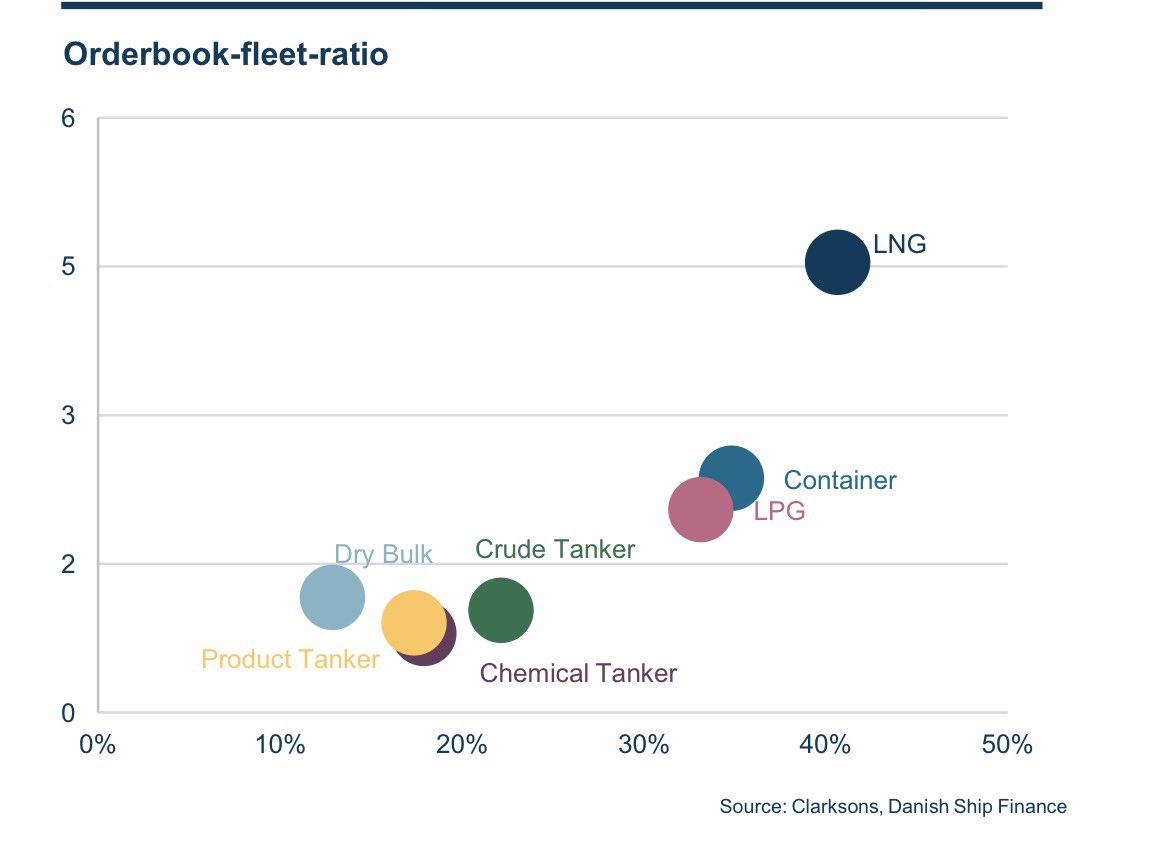

Crude tankers aren’t even the worst…I guess time for Logothetis/Lomar to repeat the 2010s boxship trade

Sources (also in screenshot): Danish Ship Finance and Clarksons

May 19

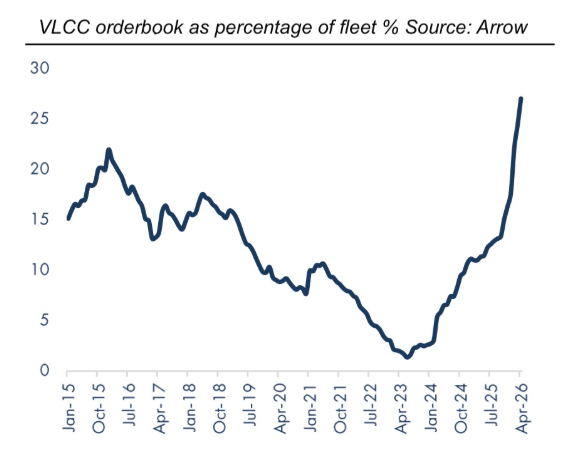

Tanker orders are surging toward record levels in 2026 (5th highest YTD this millennium), with fleet growth ~11% by 2027 vs 1–2% oil demand growth, raising oversupply risk even as red-hot rates stay supported by geopolitics and inefficiencies.

2

4

20

3,036