BuildOps says its goal is to hire nearly 300 workers for its Downtown Raleigh office. bizjournals.com/triangle/new…

448

BuildOps says its goal is to hire nearly 300 workers for its Downtown Raleigh office. bizjournals.com/triangle/new…

332

BuildOps says its goal is to hire nearly 300 workers for its Downtown Raleigh office. bizjournals.com/triangle/new…

356

BuildOps raised $127M at $1B valuation. Their contractors still wait 60 days to get paid. We built the thing they forgot: contractshield.io

4

May 21

Toronto showed up and so did we 🍁

BuildOps officially opened its dedicated Canadian headquarters in downtown Toronto. Big moment for our team and a lot more to come.

Appreciate the coverage from The Globe and Mail.

Read more: theglobeandmail.com/investin…

2

62

May 13

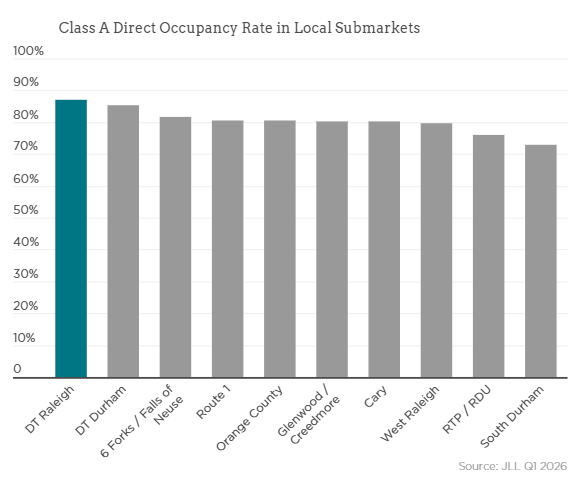

Downtown Raleigh has the highest occupancy rate for Class A direct office space in the Triangle!

With leases from Smith Anderson, Rapid Scale, BuildOps and more to come, Downtown's office market continues to build back with a strong draw of amenities and nearby housing.

2

11

2,360

商業設備業者向けのBuildOpsが、AIプラットフォーム強化に動いています。

対象はHVAC、配管、電気、防火、冷凍などの専門工事会社。

つまり、AI活用は「大手ゼネコン」だけの話ではなくなっています。

専門工事会社でも、

・作業指示

・見積

・顧客対応

・保守履歴

・職人への共有

・追加工事の判断

こういう業務がAI化されていく。

リフォーム会社も同じです。

現調メモ、写真、音声、見積項目がバラバラなままだと、AIを入れても効果が出にくい。

まずは情報を残す習慣から始めるのが、AI導入の第一歩です。

2

67

商業施工向けのAI化も、かなり進んできています。

BuildOpsという施工管理プラットフォームが、

AI強化のために新CTOを起用しました。

注目すべきは、

単なるチャットAIではなく、

「施工業務そのものにAIを組み込む」

という流れです。

たとえば、

・次に何を確認すべきか

・どの案件が遅れそうか

・どの作業が利益を圧迫しそうか

・誰に何を依頼すべきか

こういう判断をAIが支援する世界です。

リフォーム会社も同じです。

現場、営業、見積、職人、事務。

情報がバラバラな会社ほど、

AIの価値は大きくなります。

AI導入で最初に見るべきは、

「人を置き換えるか」ではなく、

「社長や管理者が、毎日どこで判断に時間を取られているか」

です。

そこをAIに手伝わせると、会社はかなり変わります。

2

66

Mar 25

Big news at BuildOps 🎉 We’re welcoming Will Lehrmann as our new Chief Product Officer to help power the next chapter of our AI-native platform for commercial contractors. More here: constructiondive.com/press-r…

3

32

BuildOps 1.0 – Turning Student Innovation into Scalable SaaS Ventures!

#ksrct1994 #ksr #ksrei #BuildOps #StartupTN #SaaSStartup #StudentInnovation #StartupEcosystem #Entrepreneurship #TechInnovation #AIStartups #DigitalVentures

10

23

48

Feb 17

#openSUSE's git-workflow meeting is happening today. Join the session to learn about the #architecture and usage presented by the #BuildOps lead. More info at calendar.opensuse.org/teams/… #contribute #community #opensource #Linux

4

14

868

Feb 13

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Day eleven, Procore, $PCOR, which is up 10% today on earnings:

Peak share price: $103.28 (July 30th, 2021)

Share price today: $52.94 (-49%)

EV today: $7.8bn

ARR today: $1.4bn ( 16% Y/y)

NRR: 106% (95% gross retention)

EV/ARR: 5.6x

GAAP Operating Margin: -12%

EV/Run-rate GAAP EBIT: N/A

Headcount: 2,068 ( 4% Y/y)

What it does: Procore is the leading vertical SaaS company for the construction industry, focused on commercial/non-resi construction. The company has an incredibly broad platform, stitching together GCs, subcontractors, architects, owners and others into one unified platform for managing projects from bid to timetracking to construction management.

AI bear case: Procore is software, and as such is exposed to the bear case that as the price of creating software collapses, it may face pressure from independent ISVs as well as homegrown solutions spun up by nimble internal teams.

AI bull case: In almost any world of AI abundance, it feels likely that construction activity increases as the physical world becomes a bottleneck, providing a tailwind to Procore's business. The software has an intrinsic network effect as users from various constituencies use it to collaborate, making straight-up disruption harder. Construction is a famously conservative market- it seems deeply unlikely that customers will vibe-code their own solutions and if anything Procure could add valuable incremental AI revenue streams to its cross-sell motion.

AI traction:

Disclosed 700 customers and 66,000 active users on Procore AI. (Vs. 3m active users on Procore)

Adjacent AI-native startup summary:

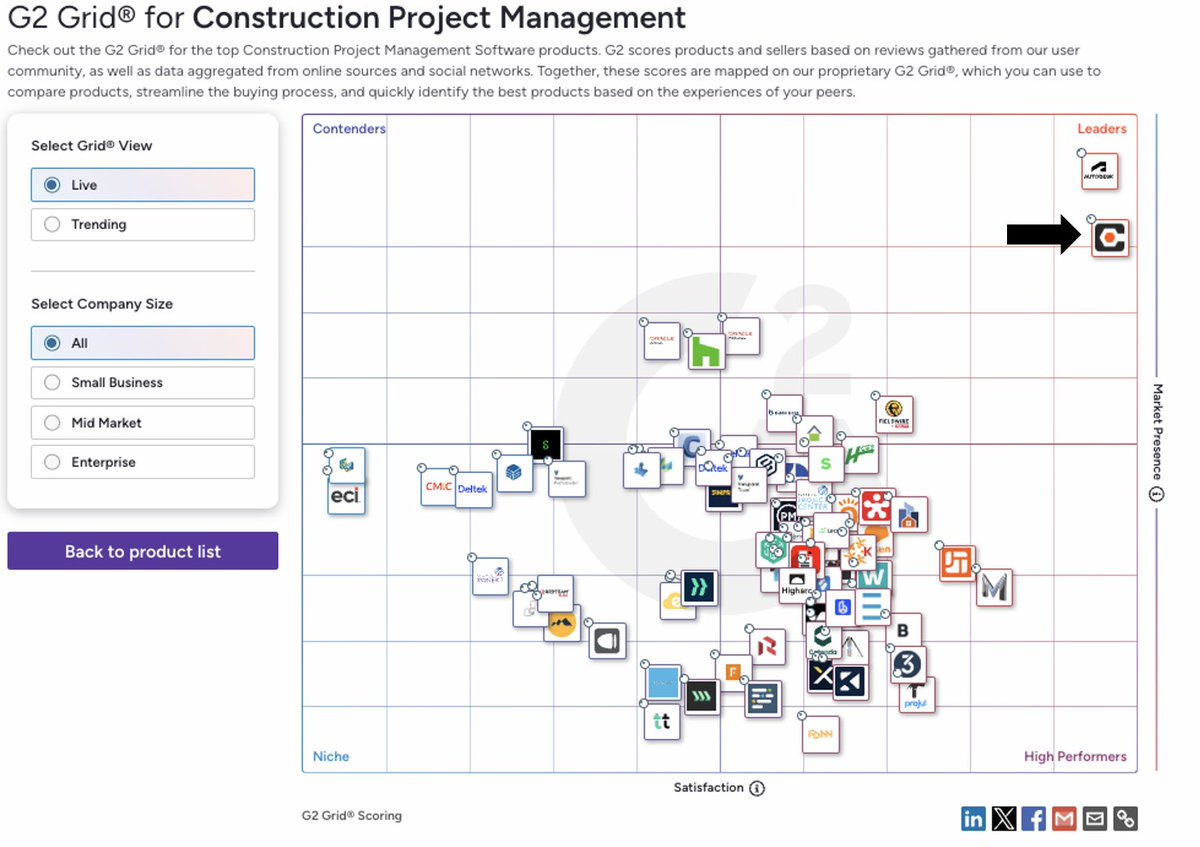

Procore is overwhelmingly compared to/competes with Autodesk, Oracle, etc. but there are some AI-powered startups, especially with machine vision as a wedge:

BuildOps (Adjacent, targets subcontractors vs. GCs but colliding)- 625 employees, 59% Y/y

Kahua (Direct competitor)- 345 employees, 46% Y/y

Openspace (Machine vision for construction)- 310 employees, 9% Y/y

Doxel (Machine vision for construction)- 109 employees, 42% Y/y

Various others.

Management Quotes:

"We believe that the combination of Procore Helix and data grid will generate notable product synergies due to our highly complementary capabilities and road maps bringing premier advanced reasoning and broad third-party integration capabilities into Procore. We call this combined offering Procore AI."

"As construction's mission-critical system of record with nearly 3 million active users, Procore has a massive proprietary dynamic data set. And the value is not only in the volume of data, it's in the depth of its context. We map the complex dynamic interactions between people, workflows and the physical job site, capturing and continuously updating every document allocation and day-to-day change. This dynamic relevance is exactly what's needed to power high-stakes agentic AI."

"So let me just answer your question about monetization of AI and then I'll turn it over to you to Howard. Look, as in any business and new business opportunity, the first thing you've got to do is to establish a compelling ROI and we believe that we're doing that. We know that we're doing that. Our customers are seeing benefit and value from the technology, as I described in the example, where they're saving time and are able to do things that they wouldn't have otherwise been able to do given the shortage of labor and given the limited amount of hours in the day that they have."

Commentary:

Procore seems well positioned in an AI world, with its natural network effect and dominance perhaps exceeding even ServiceTitan's and potential LT tailwinds to construction over time. That said, progress on AI products still feels nascent and raises questions about the bull case mid-term- it seems unlikely that Procore sees any material AI revenue for at least the next year, if not longer.

Still, Procore typifies vertical SaaS- defensible, durable, etc. and given that its customer base will likely see AI disruption last, it arguably has a longer runway than most to adapt to AI disruption.

3

25

4,636

Jan 23

WTF is going on with our Economic Development Department. They need to hire me!

Why BuildOps picked Raleigh over Austinand Atlanta for 300-job tech hub - Triangle Business Journal

bizjournals.com/triangle/new… via @TriangleBIZJrnl

3

1

2

449

17 Dec 2025

This year we grew in the ways that matter.

BuildOps was named one of Forbes America’s Best Startup Employers, earned a spot on Built In’s Best Places to Work, landed at #93 on the Inc. 5000, and was recognized on Construction Executive’s 2025 CE Top Tech™ list.

1

10

27

15 Dec 2025

We built BuildOps to solve this exact problem.

A platform that eliminates the friction driving talent out.

When your electrician has tools as good as his personal apps, he stops looking elsewhere.

1

9

34

12 Dec 2025

Modern contractors are doing the exact same thing right now.

At BuildOps, we're working to amplify the trades and give contractors the respect they truly deserve.

If you're a builder, operator, or leader exploring your next big step, DM me

1

9

2,420

10 Dec 2025

It would have been thousands.

Physical problem-solving prevented total collapse.

At BuildOps, we're building tools to amplify the heroes who hold the line - because the workers who saved Texas deserve better than chaos.

1

9

26

8 Dec 2025

Modern tools are closing the gap between the available workforce and massive project demands.

That's why we built BuildOps.

We saw contractors losing massive opportunities because they couldn't manage complexity at this scale.

1

9

74