27s

Any nation aspiring to be among the top three powers must develop its own core technologies across most strategic sectors.

Whether those technologies are first-rate or second-rate is secondary. Their very existence provides sovereignty, resilience & strategic confidence.

The moment you lack capability in a critical domain, you become vulnerable to pressure & arm-twisting.

Nothing ultimately substitutes for indigenous tech strength.

1

If national security is the question, sovereign AI capability is the central answer 🇬🇧

14

The F-4 Phantom first gained fame during the Vietnam War and is now one of the oldest fighter aircraft still in active service. Yet recent images suggest Iran may be pairing this aging platform with a much more modern weapon.

Iranian Air Force F-4s have reportedly been spotted carrying the Qassed-3 air-launched cruise missile, a weapon said to offer standoff strike capability, electro-optical guidance, and man-in-the-loop targeting. Such features could allow pilots to engage targets from a safer distance while maintaining control over the missile's final aim point.

The development highlights an important lesson of modern warfare: an aircraft's age is only part of the story. Sometimes the real question is what weapon is hanging beneath its wings.

#iran #IranWar #F4Phantom #missiles #MissileStrike

9

You frame the issue from your partisan viewpoint and present it as objective analysis. A few notes on your comments:

You assert we are “stranded” between two powers”, whereas we consider it to be our natural place in the world - to be on our own with the capability to act autonomously.

What you term as “confronting China”, we see as pushing back against its encroachment. We are currently the only country to have militarily pushed back against its aggressive expansionism. Not even the U.S. can claim that.

You claim we “lost” the ability to acquire Chinese capital and technology. Quite apart from the fact that we have alternate sources, there is a declining appetite in India to become dependent on foreign sources which can (and are) being weaponized at the turn of a dime. And you must be smoking something particularly potent to suggest we’d go for your capital and tech. There is increasing recognition that the reliance in specific areas on Chinese imports is a vulnerability that needs to be and is being addressed.

As regards America, we will deal with it on our own, as we have dealt with China on our own. The difference is that the U.S. is (still) a democracy, whereas you are from a country that doesn’t allow the vast majority of its people access to this medium of communication you are so blithely trying to lecture us on.

4

I want to understand what's the underlying logic behind "not putting women on a pedestal" requiring one to understimate their looks, mental capability, strength, etc. at minimum and being misogynistic against them at max. How do we go from A to B? But then again, internet.

1

2

1m

The most striking aspect of this story is the tension between capability claims and deployment reality. If a company publicly emphasizes that a model has extraordinary cyber or security related capabilities, it increases the likelihood that governments will eventually treat that model as a strategic technology rather than a normal commercial product.

1

Angela 🌻 retweeted

The funniest part? They contracted out their entire helicopter capability to a US company based in Houston. They had to hitch a ride on US civilian/military helos to conduct the boarding mission.

😂Too funny. The Starmer govt is currently in the middle of a massive crisis surrounding the British military and leadership that has resigned in disgust.

Cue, the U.K staged SAS operation with cameras, lighting, production visuals etc as they battle the Russians for military dominance. It's hilarious and obvious propaganda 😂🤣😂

1

21

61

1,498

Robert Hiebl retweeted

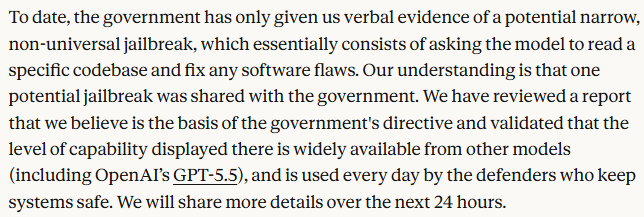

Unless Anthropic is misinformed or lying, the reason this is not “serious” is that whatever capability they thought this jailbreak unlocked is redundant with capabilities other existing public models already have.

6

5

161

9,619

I agree that Europe has serious problems. Compute is hard. Energy is expensive. Regulation can slow builders down. GPU access is not simple. These are real issues and we should not pretend they do not exist. But I do not agree with the conclusion that Europe should simply give up.

As i said when you try, you might win. When you do not try, you already lose.

Europe does not need to copy the United States or China in the exact same way. We need to use what we have better. We have talent, universities, researchers, engineers, founders, open source communities, and public compute. Where capital is missing, talent, focus, and coordination can still make a difference.

The current AI race uses a lot of scale, but progress is not only about buying more GPUs. Better data, better training methods, better evaluation, better efficiency, better deployment, and open collaboration also matter.

Europe is behind, yes. But that is exactly why we need to start. The answer cannot be to wait for others to reach superintelligence and then complain that we have no access.

The answer is to build, reduce friction, support founders and researchers, use European compute better, attract capital, and create open infrastructure that people can actually use.

Limes Labs is not claiming capability yet. We are organizing capability.

Europe has crossed the Rubicon. Now Europe must build.

1

1

That’s really good to hear.

Wish we had more homegrown industry tbh. It’s wrong that we import metals from China and other countries 🤬. We had the capability, so why not use it.

1

4

Kaka Kyari Gujbawu retweeted

Iran should demand that Israel lose its nuclear weapons and long-range missile capability as a condition for peace. Israel is, obviously, the most dangerous nation in the Middle East.

932

2,010

8,315

97,284

It's supposed to. That ground doesn't have one so armagh lost due to lack of capability for a ground to have a hooter. Joke

74

ADISOFT TECHNOLOGIES – DETAILED CONCALL HIGHLIGHTS 🧾📊📑

Adisoft Technologies is a Pune-based industrial automation and digital transformation company that has spent over a decade building capabilities across automation, Industry 4.0, Industrial IoT, machine vision, robotics, traceability, production control systems and smart manufacturing solutions.

Over the years, the company has evolved from being a conventional automation service provider into a complete smart factory solutions provider capable of connecting ERP systems, IT infrastructure and shop-floor manufacturing operations into a single integrated ecosystem.

Management repeatedly highlighted that this integration capability is one of the company's biggest differentiators and allows it to create end-to-end digital manufacturing environments for customers rather than merely supplying automation equipment.

▪ Industrial Automation

▪ Industry 4.0 Solutions

▪ Industrial IoT

▪ Production Control Systems

▪ Traceability Solutions

▪ Machine Vision Systems

▪ Robotics

▪ Smart Manufacturing Solutions

▪ Digital Factory Integration

The company believes the Indian manufacturing sector is gradually moving towards connected factories where machines, software systems and data analytics operate in an integrated manner, creating a significant long-term opportunity.

🔸 INDUSTRY OPPORTUNITY REMAINS STRONG

Management remains highly optimistic about the long-term prospects of industrial automation and digital manufacturing.

As industries increasingly focus on:

▪ Industry 4.0

▪ Digital Manufacturing

▪ Traceability

▪ Smart Factories

▪ Industrial IoT

▪ Machine Connectivity

▪ Real-Time Data Analytics

▪ Error-Proof Manufacturing

the need for integrated automation solutions continues to rise.

The company believes it is well positioned to benefit from this structural shift as Indian manufacturers increasingly invest in automation, productivity improvement and data-driven manufacturing systems.

🔸 AUTOMOTIVE REMAINS THE CORE BUSINESS

Automotive continues to be the company's largest business segment.

Current Revenue Mix:

▪ Automotive – ~80%

▪ Non-Automotive – ~20%

Management remains highly positive on the automotive industry and highlighted continued investments by OEMs and manufacturers in new production lines, automation systems and plant expansion projects.

The company continues to benefit from:

▪ New Manufacturing Lines

▪ Capacity Expansion Projects

▪ Automation Upgrades

▪ Quality Improvement Initiatives

▪ Traceability Requirements

Management expects automotive to remain a major growth driver while simultaneously reducing overall dependence through diversification into other industries.

Long-Term Target:

▪ Automotive Contribution – 60–65%

🔸 DIVERSIFICATION INTO NEW INDUSTRIES

A key strategic objective is expanding beyond automotive.

Management is actively building capabilities and teams across:

▪ Pharmaceuticals

▪ White Goods

▪ E-Commerce

▪ Warehousing

▪ Packaging

▪ Printing

The company plans to hire sector specialists and domain experts to accelerate penetration into these industries.

🔸 PHARMACEUTICAL OPPORTUNITY

Management specifically highlighted pharmaceuticals as a promising growth area.

Rather than competing purely on factory automation, Adisoft is positioning itself around:

▪ Data Collection

▪ Production Monitoring

▪ Reporting Systems

▪ Traceability Solutions

▪ Production Analytics

These are areas where pharmaceutical companies increasingly require digital solutions for compliance, quality control and operational efficiency.

🔸 WHITE GOODS & E-COMMERCE OPPORTUNITY

The company is also targeting:

▪ Air Conditioner Manufacturers

▪ Television Manufacturers

▪ Refrigerator Manufacturers

▪ E-Commerce Warehouses

▪ Logistics Facilities

Management believes many solutions successfully deployed in automotive manufacturing can be adapted for warehouse automation, inventory tracking, traceability and production monitoring in these sectors.

🔸 PRODUCT & TECHNOLOGY PORTFOLIO

The company's offering spans multiple automation and digital manufacturing categories.

Key Solution Areas:

▪ Production Control Systems

▪ Traceability Systems

▪ Tracking Systems

▪ Poka-Yoke Systems

▪ Digital Picking Systems

▪ Vision Inspection Systems

▪ Robotics Solutions

▪ Machine Connectivity Solutions

▪ Smart Manufacturing Platforms

Management indicated that machine vision and robotics are currently among the fastest-growing areas of demand.

For a completely new manufacturing facility, project values can range between:

▪ ₹2.5 Crore to ₹10 Crore

depending on automation requirements and project complexity.

🔸 BUSINESS MODEL & MARGIN PHILOSOPHY

One of the most important insights from the concall was management's explanation of margin expansion.

According to management, the first deployment of a new solution requires significant investment in:

▪ Design

▪ Development

▪ Testing

▪ Customization

However, once the same solution is deployed repeatedly across multiple customers, profitability improves substantially.

This creates operating leverage and allows margins to improve over time without proportionate increases in development costs.

Management believes this reuse-driven model can continue supporting profitability as the business scales.

🔸 NEW BHOSARI FACILITY – MAJOR GROWTH DRIVER

One of the most important developments underway is the company's new facility in Bhosari, Pune.

Key Details:

▪ Plot Size – ~30,000 Sq. Ft.

▪ Built-Up Area – ~70,000 Sq. Ft.

Management described the facility as more comparable to a technology campus than a traditional industrial unit.

Current Status:

▪ Excavation Completed

▪ PCC Work Started

▪ Basement Ground First Floor expected by Sept–Oct FY27

▪ Production Expected to Start – October 2026

▪ Full Facility Expected by March 2027

The facility will integrate:

▪ Manufacturing Teams

▪ Software Teams

▪ Design Teams

▪ Project Execution Teams

under one roof.

Management believes this will significantly improve coordination, execution speed and operational efficiency.

🔸 CAPACITY EXPANSION & REVENUE POTENTIAL

Current infrastructure is approaching practical capacity limits.

Management highlighted constraints related to:

▪ Manufacturing Space

▪ Execution Capacity

▪ Employee Expansion

▪ Infrastructure Availability

The new facility is expected to remove these bottlenecks and support the next phase of growth.

Management indicated:

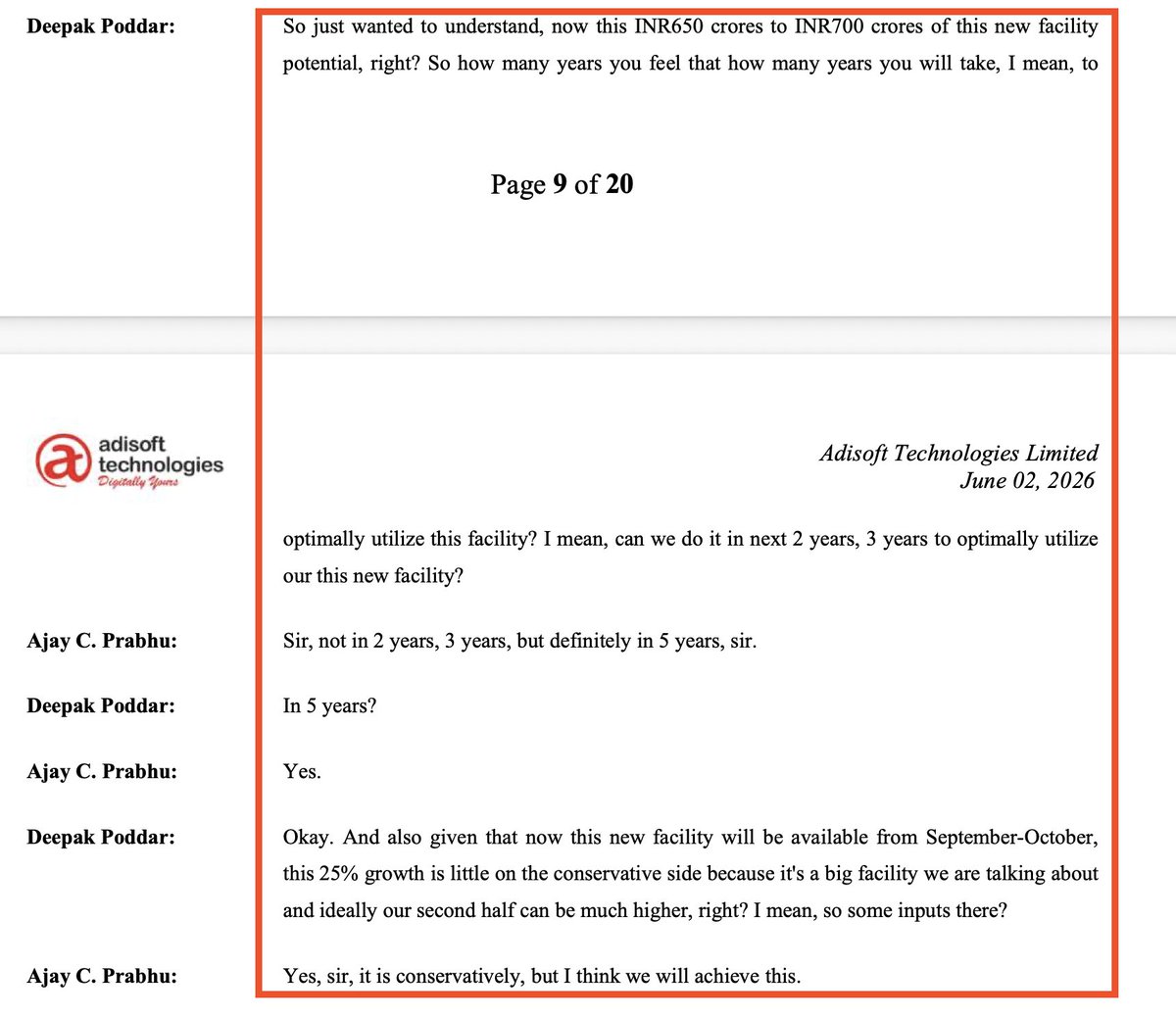

▪ Revenue Potential of New Facility – ₹650–700 Crore

▪ Time Required for Full Utilization – ~5 Years

An important point highlighted during the discussion was that larger infrastructure also improves customer confidence and increases the company's ability to secure larger and more complex projects.

Management believes the new facility will become a key catalyst for future growth.

🔸 ORDER BOOK & BUSINESS VISIBILITY

The company operates with relatively short project execution cycles.

Key Metrics:

▪ Average Project Cycle – 3–4 Months

▪ Opening FY27 Order Book – ~₹40 Crore

▪ Active Pipeline – ~₹85 Crore

▪ Orders Already Received – ₹46–47 Crore

▪ Around 40% of Annual Target Currently Under Bidding

Management expressed confidence in the quality of the order pipeline and future business visibility.

🔸 EXPORT OPPORTUNITY

The company has already executed export projects over the last two years.

Current strategy focuses on:

▪ Supporting Existing Customers Overseas

▪ Following Indian OEM Expansions

▪ Building International Capabilities

Management believes exports can gradually become an additional growth driver.

🔸 COMPETITIVE ADVANTAGE

According to management, Adisoft's biggest differentiator is its ability to integrate the entire manufacturing ecosystem.

The company can connect:

▪ ERP Systems

▪ IT Infrastructure

▪ Production Data

▪ Shop Floor Equipment

▪ Manufacturing Processes

into a unified smart factory environment.

Many competitors focus only on specific departments such as assembly lines, weld shops or press shops, whereas Adisoft can operate across the entire factory ecosystem.

Additional strengths include:

▪ In-House Design Capability

▪ In-House Software Development

▪ Strong Execution Capability

▪ Long-Term Customer Relationships

▪ Deep Manufacturing Domain Knowledge

🔸 TRADING BUSINESS

Apart from automation solutions, the company also operates a trading business.

FY26 Revenue Mix:

▪ Solutions Business – ~75–78%

▪ Trading Business – ~22–25%

Trading Margin:

▪ Approximately 10%

Although margins are lower, management views the segment as strategically important because it provides:

▪ Customer Access

▪ Market Intelligence

▪ Cross-Selling Opportunities

▪ New Business Leads

🔸 CUSTOMER CONCENTRATION

Management disclosed that the largest customer contributed approximately:

▪ ~65% of FY26 Revenue

The relationship has existed since the company's early years and continues to expand.

Management does not currently view this as a concern because of:

▪ Long-Term Relationship

▪ Recurring Opportunities

▪ Strong Customer Trust

Within its specialized automation niche, management estimates:

▪ Wallet Share – ~90–95% with this customer.

🔸 WORKING CAPITAL & RECEIVABLES

Key Metrics:

▪ Working Capital Cycle – ~120 Days

▪ Payment Cycle – 45–60 Days

Receivables increased due to strong execution during the second half of FY26.

Management clarified that collections remain healthy.

Importantly, after year-end collections, only approximately:

▪ ₹28–29 Crore

remained outstanding at the time of the concall.

This provides confidence regarding the quality of receivables and collection efficiency.

🔸 PROFITABILITY OUTLOOK

Management remains confident regarding profitability.

Key drivers include:

▪ Repeat Business

▪ Solution Reuse

▪ Operating Leverage

▪ Better Project Execution

▪ Higher Value Addition

Management indicated that:

▪ PAT Margins of ~13–14% remain sustainable.

▪ Additional improvement opportunities exist over time.

🔸 DEBT POSITION

Management highlighted that the company currently maintains a relatively modest debt profile.

Long-Term Objective:

▪ Debt-Free Status Within Approximately 2 Years

supported by future growth and internal cash generation.

🔸 GROWTH OUTLOOK

Management remains confident about future growth.

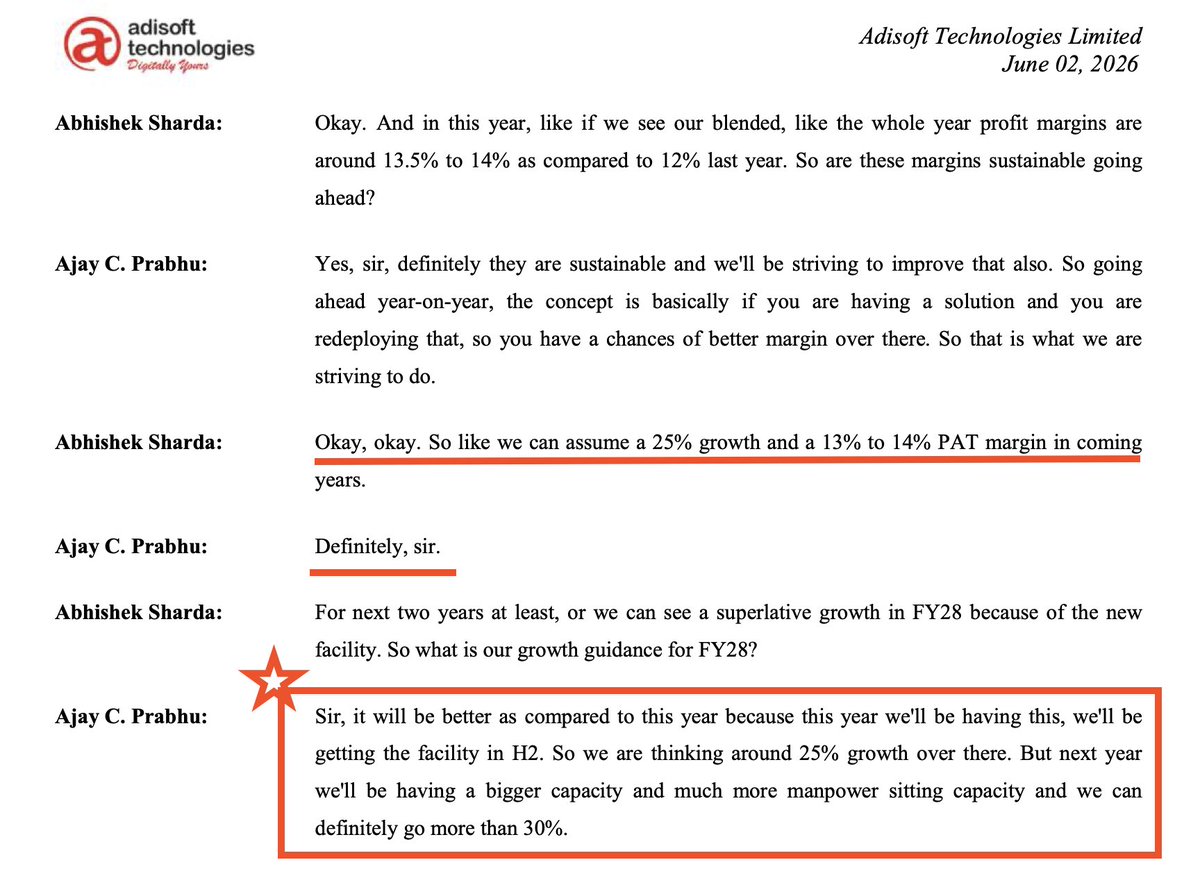

FY27 Guidance:

▪ Revenue Growth Target – ~25%

Management further indicated that FY28 could witness stronger growth because FY27 will only see a partial contribution from the new facility.

With a full-year benefit from the expanded infrastructure, management believes growth could potentially exceed:

▪ 30% Growth in FY28

📌 KEY NUMBERS AT A GLANCE

▪ FY27 Revenue Growth Target – ~25%

▪ FY28 Growth Potential – 30%

▪ Plot Size – ~30,000 Sq. Ft.

▪ New Facility Size – ~70,000 Sq. Ft.

▪ Production Start – October 2026

▪ Full Facility Operational – March 2027

▪ Revenue Potential of New Facility – ₹650–700 Crore

▪ Utilization Period – ~5 Years

▪ Opening FY27 Order Book – ~₹40 Crore

▪ Active Pipeline – ~₹85 Crore

▪ Orders Already Received – ₹46–47 Crore

▪ Project Cycle – 3–4 Months

▪ Automotive Revenue Contribution – ~80%

▪ Long-Term Automotive Mix Target – 60–65%

▪ Trading Business Contribution – ~22–25%

▪ Trading Margin – ~10%

▪ Largest Customer Contribution – ~65%

▪ Wallet Share – 90–95%

▪ Working Capital Cycle – ~120 Days

▪ Payment Cycle – 45–60 Days

▪ Receivables Outstanding After Collections – ~₹28–29 Crore

▪ Typical Project Size – ₹2.5–10 Crore

▪ Sustainable PAT Margin Range – ~13–14%

Disclaimer: This summary is based on management commentary and is intended solely for educational and research purposes. Please conduct your own research before making any investment decisions.

Jun 13

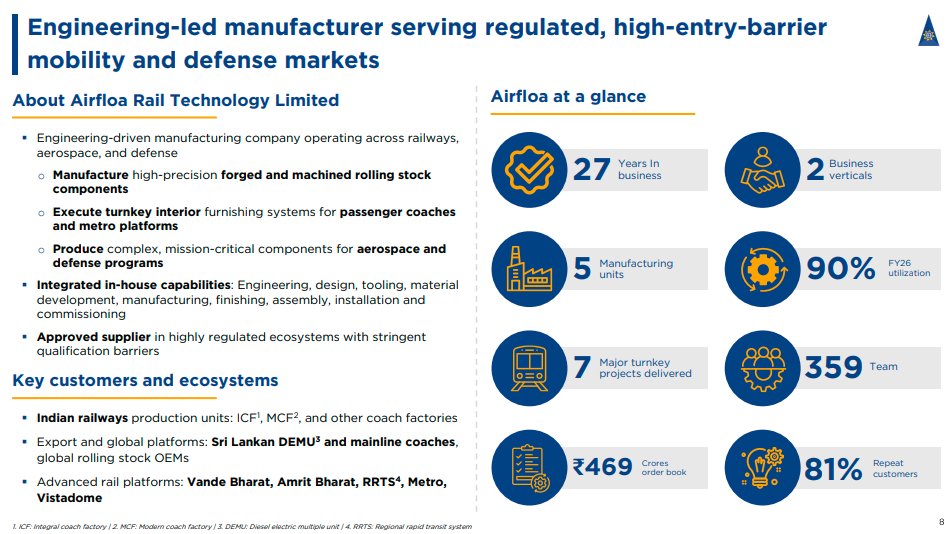

AIRFLOA RAIL TECHNOLOGY – DETAILED CONCALL HIGHLIGHTS 🧾📑

Airfloa Rail Technology continues to evolve from being a railway component supplier into a much broader engineering, manufacturing and technology-driven platform. Over the last few years, the company has gradually moved up the value chain from supplying individual products to undertaking complete turnkey solutions involving design, manufacturing, supply, installation and commissioning.

The company believes this transformation is strategically important as it enables higher value addition, stronger customer relationships, improved profitability and participation in significantly larger opportunities.

🔸 Today, Railways remain the largest contributor to the business and management continues to remain highly optimistic on the sector's long-term growth prospects.

The opportunity pipeline is being driven by:

▪ Vande Bharat Trains

▪ Vande Bharat Sleeper Trains

▪ Amrit Bharat Trains

▪ Metro Rail Projects

▪ Coach Refurbishment Programs

▪ High-Speed Rail Projects

▪ Regional Transit Projects

▪ Border Modernization Initiatives

According to the company, Indian Railways is entering a multi-year investment cycle where modernization, safety upgrades, refurbishment and indigenous manufacturing will continue to create significant opportunities for specialized players.

🔸 One of the most important opportunities discussed during the call was the railway coach refurbishment program.

The Government has already sanctioned approximately ₹26,000 crore for refurbishment activities covering nearly 25,000 railway coaches. The company believes this could become one of the largest opportunities available within the railway ecosystem over the next few years.

Airfloa has already started positioning itself aggressively in this segment and is targeting approximately ₹100 crore worth of refurbishment orders during FY27 alone.

🔸 Apart from refurbishment, the company is actively pursuing opportunities under Vande Bharat Sleeper, Amrit Bharat and multiple metro rail projects, which together form a significant portion of the future pipeline.

The metro business continues to emerge as another important growth driver.

The company currently has approximately ₹70 crore worth of metro-related orders under execution and is evaluating another ₹120 crore worth of opportunities from the active pipeline.

Management believes increasing investments in urban transportation systems across India will continue creating long-term opportunities for metro rail suppliers.

🔸 Order visibility remains strong.

As of May 2026:

▪ Unexecuted Order Book – ₹486.9 Crore

▪ Active Bid Pipeline – ₹1,200 Crore

▪ Historical Bid Win Ratio – 20–25%

Importantly, nearly ₹900 crore of the active pipeline belongs to the railway segment itself, providing strong visibility for future growth.

The pipeline includes opportunities across:

▪ Vande Bharat Sleeper

▪ Amrit Bharat Projects

▪ Metro Rail

▪ Coach Refurbishment

▪ Kavach Related Opportunities

▪ Regional Transit Systems

▪ Turnkey Railway Projects

Management sounded particularly confident regarding the quality of the order pipeline and believes the company is well-positioned to benefit from India's ongoing railway modernization efforts.

🔸 A major highlight of the concall was the company's continued focus on profitability rather than simply chasing revenue growth.

Over the last year, the industry witnessed sharp inflation in raw material prices.

▪ Aluminium prices increased more than 80%.

▪ Stainless steel prices increased approximately 60–65%.

Since raw materials account for more than 60% of product costs, the impact on profitability was significant.

However, instead of accepting low-margin contracts, the company consciously adopted a disciplined approach.

This included:

▪ Selective bidding.

▪ Price renegotiations.

▪ Supplier optimization.

▪ Advance procurement.

▪ Cost-control measures.

▪ Re-tendering of unattractive projects.

Management clearly stated that they are not willing to sacrifice margins merely to achieve revenue targets.

📌 This disciplined approach is one of the reasons why the timeline for achieving the company's long-term ₹1,000 crore revenue aspiration may shift slightly. However, management reiterated that the target itself remains fully achievable.

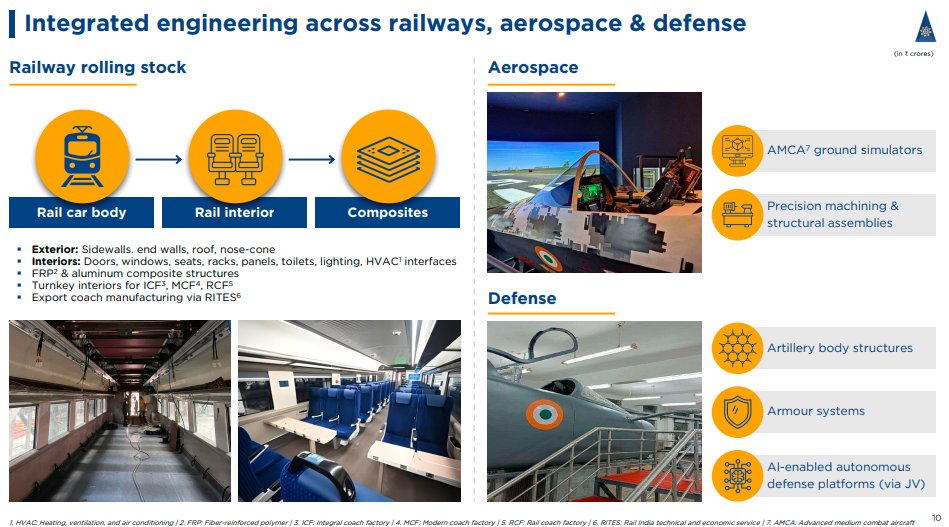

🔸 A significant portion of the discussion focused on defence, which management views as the company's next major growth engine.

Management described FY26 as a foundational year for the defence and aerospace vertical. While the contribution remains relatively small today, the focus has been on capability building, technology acquisition and creating the foundation for long-term growth.

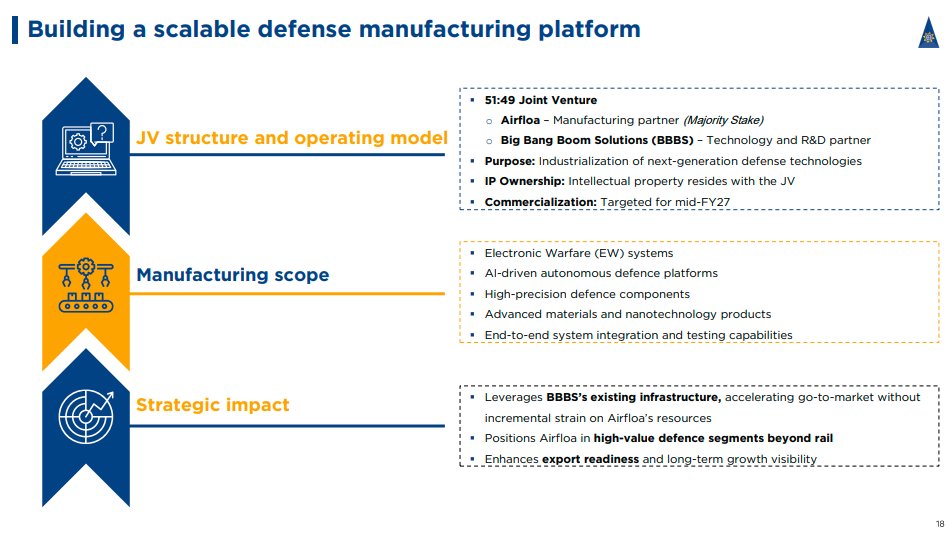

A major milestone is the proposed Joint Venture with Big Bang Boom Solutions, which management expects to be incorporated within approximately two weeks and before mid-June 2026.

The JV will focus on:

▪ Autonomous Drones for Defence & Industrial Applications

▪ Electronic Warfare Systems

▪ High-Power Microwave Systems

▪ Laser-Based Defence Technologies

Management clarified that the operating structure is strategically designed where the JV will act as the technology holder, while manufacturing rights for these technologies will be given to Airfloa.

The company plans to invest approximately ₹25 crore into JV-related activities and technology development.

While some revenue contribution may begin during FY27, management repeatedly highlighted that defence is a long-gestation business and should be viewed as a multi-year opportunity.

▪ Management emphasized that defence procurement involves extensive testing, validation and approval cycles, making it a longer-gestation opportunity compared to the railway business.

They described it as a "two-year program" with a more meaningful impact expected across FY27–FY28 as technologies complete validation, testing and procurement cycles.

The company also highlighted opportunities linked to HAL and indicated that defence opportunities worth approximately ₹60–70 crore are currently visible through the HAL ecosystem.

Current defence order book exposure stands at approximately ₹29 crore.

Discussed simulator-related opportunities connected to the AMCA ecosystem and clarified that the opportunity currently relates to simulator systems and training infrastructure rather than the actual aircraft platform.

🔸 Management indicated that research and development spending is expected to increase significantly.

Historically:

▪ R&D Spend – ~4% of Revenue

Going Forward:

▪ Target R&D Spend – 8–9% of Revenue

The increase will primarily support:

▪ New Product Development

▪ Technology Transfers

▪ Defence Technologies

▪ Aerospace Technologies

▪ Electronic Warfare Systems

▪ Autonomous Platforms

An important disclosure made during the call was that management expects a significant portion of this R&D spending to be reflected on the balance sheet, making it an important metric for investors to monitor going forward.

🔸 The company has also established a subsidiary focused on electroluminescent dynamic display boards and flexible electronics.

Management sees applications across:

▪ Railway Display Systems

▪ Commercial Signage Networks

▪ Aerospace Applications

▪ Space Applications

▪ Flexible Electronics

The initiative is being positioned as an additional growth driver outside the current railway and defence businesses.

Management expects commercialization opportunities to emerge during FY27 and clarified that potential revenue from this business is currently not included in existing order book or tender pipeline disclosures.

🔸 Another interesting area discussed was technology development.

The company is currently developing an AI-based railway security platform.

Management clarified that this solution is different from Kavach.

The platform focuses on:

▪ AI-enabled monitoring.

▪ Remote security management.

▪ Railway asset protection.

▪ Advanced surveillance applications.

The company expects demonstrations before Railway Board and RDSO during FY27.

If approved, management believes this could create a completely new technology-led business vertical within the railway ecosystem.

🔸 Capacity utilization was another important discussion point.

Current facilities are operating at approximately:

▪ Capacity Utilization – ~90%

To support growth despite high utilization levels, the company has already implemented a two-shift operating model.

Management indicated that a full year of two-shift operations should significantly increase throughput even before major new manufacturing facilities become operational.

▪ Management further indicated that the upcoming infrastructure project is expected to effectively double the company's existing manufacturing capacity over time, creating additional headroom for future railway and defence opportunities.

The company is also pursuing a channel partner strategy to improve scalability.

Under this model:

▪ Airfloa manufactures products.

▪ Regional partners execute projects locally.

▪ Lower infrastructure investments required.

▪ Reduced working capital burden.

▪ Lower bank guarantee requirements.

▪ Improved profitability.

Management believes this model can help scale the business efficiently towards ₹1,000–2,000 crore revenue levels without proportionately increasing fixed infrastructure costs.

🔸 A major strategic initiative underway is the development of a new integrated manufacturing campus.

The company has already secured:

▪ 14 Acres of Land

Development plans include:

▪ Initial Manufacturing Area – 50,000 to 1,00,000 Sq. Ft.

▪ Long-Term Expansion Potential – 3,00,000 to 4,00,000 Sq. Ft.

The objective is not merely capacity expansion.

Management intends to consolidate multiple smaller facilities into a more integrated manufacturing ecosystem.

Expected benefits include:

▪ Reduced rental expenses.

▪ Better operational efficiency.

▪ Improved manufacturing integration.

▪ Higher productivity.

▪ Better economies of scale.

▪ Management highlighted that the company currently incurs approximately ₹20–25 lakh per month in rental expenses and expects meaningful savings as operations are gradually consolidated into larger owned facilities.

Over time, the company expects to operate primarily through two major manufacturing facilities rather than multiple smaller units.

🔸 To support future growth, Airfloa has outlined significant investment plans.

FY27 Capex Guidance:

▪ ₹30–40 Crore

Infrastructure Development Spend:

▪ ₹30–35 Crore

The investments will primarily support:

▪ Manufacturing Expansion

▪ Defence Capabilities

▪ Product Development

▪ Technology Development

▪ New Facility Construction

Research and Development continues to be a major priority.

The increased spending will focus primarily on:

▪ Defence Technologies

▪ Aerospace Technologies

▪ Electronic Warfare Systems

▪ Autonomous Systems

▪ Advanced Product Development

Management believes these investments are necessary to create technological differentiation and long-term competitive advantages.

Funding plans were also discussed in detail.

The company clarified that:

▪ No equity dilution is planned during FY27.

▪ Debt funding of approximately ₹120 crore is being arranged.

▪ ₹60 crore has already been sanctioned.

▪ Additional ₹60 crore is expected shortly.

▪ Borrowing cost is approximately 8.25%.

Management believes existing cash flows, receivable collections and debt funding will be sufficient to support the company's expansion plans.

🔸 Working capital improvement remains another major focus area.

Management is targeting:

▪ Working Capital Cycle – 60–70 Days

▪ Receivable Cycle – 60–70 Days

▪ Expected Collections by June 2026 – ₹100–110 Crore

The company expects collections and working capital efficiency to improve meaningfully over the next few quarters.

Looking ahead, management remains highly confident regarding FY27.

🔸 Guidance provided includes:

▪ FY27 Revenue Target – ₹500 Crore

▪ FY27 PAT Margin Guidance – 12–13%

The confidence is supported by:

▪ Strong ₹486.9 crore order book.

▪ ₹1,200 crore active pipeline.

▪ Railway modernization opportunities.

▪ Metro expansion opportunities.

▪ Defence diversification.

▪ Manufacturing expansion.

▪ Technology initiatives.

▪ Channel partner model.

Management also reiterated confidence in eventually achieving:

▪ ₹1,000 Crore Revenue

▪ ₹150 Crore PAT

while maintaining profitability discipline and avoiding low-return business.

KEY NUMBERS AT A GLANCE

▪ Order Book (May 2026) – ₹486.9 Crore

▪ Active Bid Pipeline – ₹1,200 Crore

▪ Railway Pipeline – ~₹900 Crore

▪ Metro Pipeline – ~₹120 Crore

▪ Defence Pipeline – ₹60–70 Crore

▪ Current Metro Orders – ~₹70 Crore

▪ Bid Win Ratio – 20–25%

▪ FY27 Revenue Guidance – ₹500 Crore

▪ FY27 PAT Margin Guidance – 12–13%

▪ Long-Term Revenue Aspiration – ₹1,000 Crore

▪ Long-Term PAT Aspiration – ₹150 Crore

▪ Capacity Utilization – ~90%

▪ Land Acquired – 14 Acres

▪ Initial Manufacturing Area – 50,000–1,00,000 Sq. Ft.

▪ Long-Term Expansion Potential – 3,00,000–4,00,000 Sq. Ft.

▪ FY27 Capex – ₹30–40 Crore

▪ Infrastructure Spend – ₹30–35 Crore

▪ Planned Debt Funding – ₹120 Crore

▪ Debt Already Sanctioned – ₹60 Crore

▪ Additional Debt Expected – ₹60 Crore

▪ Interest Rate – 8.25%

▪ R&D Spend FY26 – ~4% of Revenue

▪ R&D Spend Target – 8–9% of Revenue

▪ JV Investment Commitment – ₹25 Crore

▪ Railway Refurbishment Opportunity – ₹26,000 Crore

▪ Refurbishment Scope – ~25,000 Coaches

▪ FY27 Refurbishment Target – ₹100 Crore

▪ Working Capital Target – 60–70 Days

▪ Receivable Cycle Target – 60–70 Days

▪ Expected Collections by June 2026 – ₹100–110 Crore

Disclaimer: This summary is based on management commentary during the conference call and is intended solely for educational purposes. Please conduct your own research before making any investment decisions.

1

45

✨ retweeted

NEW: Anthropic claims the capability cited by the U.S. in restricting Fable 5 is already widely available from other models, including OpenAI’s GPT-5.5.

351

288

5,955

1,232,517

I mean, let's be fair. White people have the capability of genuinely being the ugliest in the room at any time. So, if this is a Jewish woman's worst, I can see why white people are angry

They are almost always significantly "uglier" than that on any given day, even with effort

3

Every government is necessarily limited by reach, expertise, capability, etc. Private companies exist even in communist regimes for that reason.