29 Oct 2025

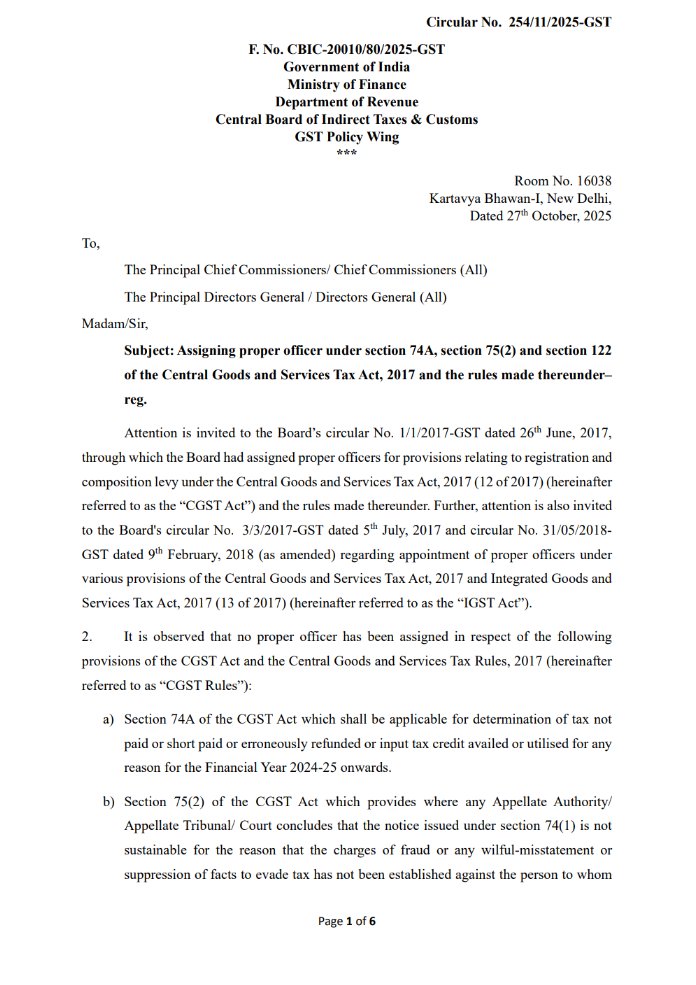

🚨 CBIC’s Circular No. 254/11/2025-GST, dated October 27, 2025 clarifies assignment of proper officers and monetary limits for adjudication and penalty proceedings under Sections 74A, 75(2), and 122 of the CGST Act, 2017.

Here’s a simple breakdown 👇

👉 Section 74A – Adjudication Limits

Covers determination and demand for unpaid or short-paid tax, refunds, and ITC discrepancies for FY 2024–25 onwards.

Proper officers assigned under Section 74A:

✅ Superintendent of Central Tax – Demands not exceeding ₹20 lakh (aggregate CGST IGST).

✅ Deputy/Assistant Commissioner of Central Tax – Demands above ₹20 lakh and up to ₹2 crore (aggregate CGST IGST).

✅ Additional/Joint Commissioner of Central Tax – Above ₹2 crore, no upper limit.

👉 Section 122 – Penalty Proceedings

✅ For imposing penalties under Section 122, the same monetary thresholds apply as above.

✅ Officer assignment is based on the combined amount of penalty for both CGST and IGST.

👉 Section 75(2) – Reclassification of Proceeding

If an appellate authority or court finds that fraud or wilful misstatement isn’t established in a Section 74(1) notice —

➡️ The proper officer must reassess tax as if the case falls under Section 73(1).

➡️ The same officer who handled the earlier adjudication will reassess.

👉 Administration & Applicability

The specified monetary limits apply to all pending and future adjudication cases under these sections from the circular’s effective date.

The Circular can be accessed here 👇

🔗drive.google.com/file/d/1I70…

#GST #IndirectTax #CBIC #TaxLaw #CircularUpdate #GSTLitigation #CGSTAct

4

6

854

10 Jun 2024

Gold enthusiasts, take note! Cerrado Gold just filed its circular and shared some updates. Stay tuned for the latest developments in the world of goldmining: ibn.fm/1oode

#CerradoGold #CircularUpdate #goldmining

1

3

91

12 Jan 2024

🌐 Circular Update Announcement 🌐

Hello Circular Community! 👋🏼 We're excited to bring you a new app and firmware update – Version 15.0.3, released on January 12, 2024.

Best, Circular Team 🟠⭕️ #CircularUpdate #WearableTech #ReleaseNotes

circular.xyz/release-notes

6

2

401

31 Aug 2023

ఈపీఎఫ్వో అలర్ట్: వివరాల అప్డేషన్కు కొత్త మార్గదర్శకాలు

sakshi.com/telugu-news/busin…

#epfo #circularupdate #EPFAccount #BusinessNews

1

294

6 Oct 2021

We have been working hard this year, as part of the shared goal with @WCTD2050 to achieve full circularity. And we were asked: what is the one thing we need from other to succeed in our circularity ambitions?

#CircularUpdate

3

8

5 Oct 2021

Join us on Friday at 2pm for @WCTD2050 - our first year in review. Sign up for the livestream, wctd2021.eventbrite.co.uk & catch up on what has happened within the themes of national strategy, raw materials, products & services and people & society #CircularUpdate Tweet Q's 4 us!

2

7