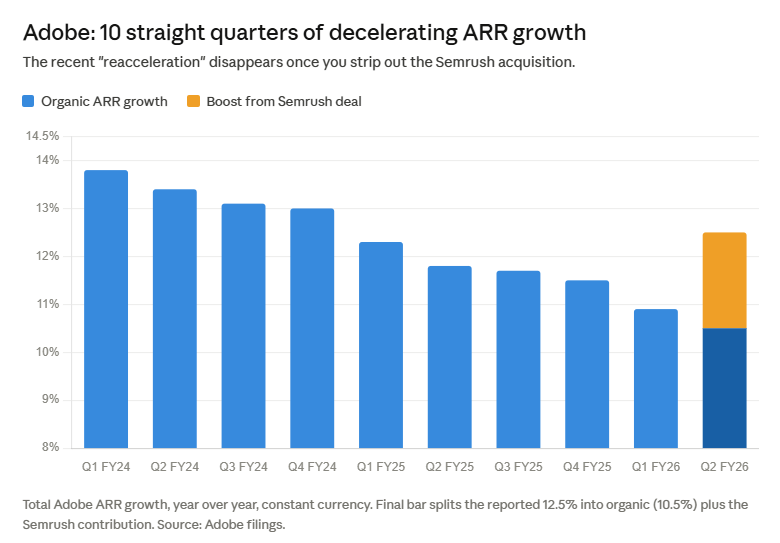

Adobe was a textbook compounder for years.

Now: organic growth decelerating for the tenth straight quarter, the CEO on his way out, the CFO too.

Buy and verify, not buy and forget.

7

452

There is someone in Substack who covered Games Workshop a.k.a the owner of warhammer 40k. It made me realize how Sharp execution alongside with cult-like fandom could be a great compounder.

11

🚨 IS $SPCX ABOUT TO GIVE RETAIL THE SAME LESSON $TSLA DID?

Tesla IPO’d at $17, closed its first day at $23, then pumped to $30 on day two, then dropped roughly 50% from its early IPO high before becoming one of the greatest trades ever.

Initially, Tesla wasn’t treated as a sacred long-term compounder. It was treated like a volatility instrument.

And it wasn’t just Tesla.

This is what happened after some of the most hyped tech listings:

– Facebook: -54%

– Snap: -56%

– Uber: -68%

– Pinterest: -70%

– Lyft: -79%

– Rivian: -88%

– Robinhood: -90%

Median first-year drawdown: -54%.

Average: -55%.

SpaceX can be one of the most important companies on earth and but still the market likes to punish impatient buyers.

The SpaceX IPO setup is starting to look familiar:

– Peak media hype

– Retail FOMO

– Insiders up life-changing multiples

Limitless traders now see a 40% chance $SPCX hits $200 in June (trade here: limitless.is/spcx-june)

The question isn’t whether SpaceX is a generational company.

The question is whether retail is about to buy another generational top and sit with an underwater position for 6 months.

4

2

9

512

I like it. I ran it for $NVO, it goes through things in digestible detail. Then I asked for a summary.

Novo Nordisk is a fallen compounder in a structural reset, not a broken business. The stock has declined ~70% from its 2024 all-time high and now trades at ~14× forward earnings — a valuation that prices in permanent impairment. The variant perception is that the market is confusing a deliberate strategic transition with terminal decline.

Consensus reads this as distress. The counter-thesis is that this is a calculated sacrifice of near-term revenue to cement a decade-long moat.

1

77

$NOW — ServiceNow is quietly becoming the operating system for enterprise IT. Net retention rates most SaaS companies dream about, and AI tailwinds that could accelerate everything. The kind of compounder you want to own for a decade.

1

86

$NOW — ServiceNow is quietly becoming the operating system for enterprise IT. Net retention rates most SaaS companies dream about, and AI tailwinds that could accelerate everything. The kind of compounder you want to own for a decade.

1

86

Ondas Inc $ONDS Investment Thesis

1. Investment Summary

Ondas Holdings Inc. is executing one of the most dramatic corporate transformations in the history of small-cap defence technology. In the space of eighteen months, a company that was generating $4.3 million per quarter in revenue from industrial wireless and early-stage drone operations has acquired six companies, merged with a US defence prime contractor, signed demining contracts worth $80 million, won a border protection tender involving thousands of drones, secured selection for the 2026 FIFA World Cup, been drawn into a $982 million US Army IDIQ loitering munitions programme, and raised its FY2026 revenue guidance to at least $390 million — a 670% year-over-year increase. Q1 2026 revenue of $50.1 million, reported May 14, 2026, was 25% above the high end of management guidance and 31% above analyst consensus. The stock traded at $7.39 before Q1 results, surged 26.5% on the day, and now sits at $9.33 with an analyst consensus target of $20.12 — implying over 116% upside from current levels.

This is not a conventional investment thesis. Ondas is not a stable, predictable compounder with decades of earnings history. It is a defence autonomy platform company executing an aggressive, acquisition-driven consolidation strategy in the fastest-growing segment of the global defence budget at the precise moment when geopolitical instability, the Ukraine drone warfare playbook, and escalating great-power competition have made autonomous and counter-autonomous systems a procurement priority at every level of Western and allied defence establishments. The investment thesis is built on three structural pillars: the unprecedented global demand surge for counter-UAS and autonomous systems driven by modern conflict dynamics; Ondas’s System-of-Systems integration strategy that assembles best-in-class aerial, ground, and cyber capabilities into a unified defence platform; and the Mistral acquisition that provides the US prime contractor status required to access the largest and most valuable procurement programmes in the world’s largest defence budget.

The risks are substantial and must be addressed with full transparency. Ondas remains adjusted EBITDA negative at the company level, with profitability not expected until Q1 2028. The acquisition pace is extraordinary — six companies in 2026 — and integration risk is real. The backlog of $457 million must convert to recognised revenue to justify the $390 million FY2026 guidance. And at $4.8 billion in market capitalisation on $50 million in quarterly revenue, the valuation prices in a significant amount of future execution. For investors who understand these risks and can commit to the multi-year growth thesis, Ondas occupies a uniquely positioned slot in the defence autonomy ecosystem with few publicly traded equivalents at comparable scale and ambition.

For full newsletter: open.substack.com/pub/anandc…

2

183

2/ $ANET – Arista Networks 9% ✅

Arista builds the high-speed networking gear that hyperscalers and cloud providers rely on. Dominant in 400G/800G ethernet for AI clusters. Quiet compounder, strong moat.

2

2

23

Advice to Pharm.D students:

Trust God. Never Give up (Blessing's Insight)

(DJ play me- Oluwa ni. Biliki. Olorun l'ole seeee)

🔥MEET THE COMPOUNDER OF THE DAY🔥

Fine "EJIRINDE BLESSING ITUNUOLUWA(Blessing)"

1

7

Give yourself time to understand yourself, your strengths, weaknesses, and use it to create a system that will help you achieve your goals. (Abdulrahman's Blueprint)

(DJ play me- Lonely at the top. Asake. Ololade mi Asakeeee)

🔥MEET THE COMPOUNDER OF THE DAY🔥

1

1

10

$ESENTIAII.MX

Largest private gas pipeline network in Mexico — 2,000 km moving Waha gas into the industrial heartland.

The growth story:

↳ Phase I expansion ( 297 MMcfd) commissioning early 2027

↳ Phase II approved, Siemens turbines en route

↳ 50% capacity by 2028. All pre-contracted before shovels hit dirt.

Consensus sees Sales 10% in FY2027, 21% in FY2028 — EPS accelerating even faster ( 37% / 42%) as interest burden drops post $2B investment-grade refinancing

Not a trade. A 3-year infrastructure compounder thesis

34

Chiragindian retweeted

🔔 Stock watch: Five-Star Business Finance

A Quiet Compounder in the MSME Lending Space?

One company that has quietly built a strong franchise serving underserved entrepreneurs is Five-Star Business Finance.

Why it stands out:

• Focuses on secured business loans for small business owners, self-employed individuals and micro-entrepreneurs who are often overlooked by traditional lenders.

• Operates a highly granular lending model with loans backed primarily by self-occupied residential properties, helping contain credit risk.

• Consistently delivers industry-leading asset quality despite lending to borrowers in the informal and semi-formal economy.

• Strong AUM growth driven by increasing penetration across South India and expansion into new geographies.

• Asset-light branch expansion strategy continues to support scalable growth.

• Backed by reputed institutional investors and private equity shareholders, reflecting confidence in the long-term business model.

What I like:

✓ Large and underpenetrated MSME lending opportunity

✓ High ROA and ROE compared to many lending peers

✓ Secured lending model

✓ Strong asset quality track record

✓ Long runway for branch expansion and customer acquisition

✓ Beneficiary of India’s formalization and financial inclusion trends

Key risks:

• Valuation premium versus traditional NBFCs

• Any slowdown in MSME activity could impact disbursement growth

• Rising competition from banks, fintechs and other NBFCs

• Regulatory changes affecting lending practices

Financial Inclusion MSME Lending Secured Credit Long Growth Runway

Five-Star Business Finance is a scalable financial-services franchise addressing a massive credit gap in India’s small-business segment.

If management can continue growing AUM while maintaining asset quality and profitability, this could remain one of the higher-quality compounding stories in the NBFC space over the next decade.

(Not a recommendation. Please do your own research & analysis after gaining good knowledge)

#FiveStarBusinessFinance #NBFC #FinancialServices #MSME #SmallCaps #IndianStockMarket #Investing #WealthCreation #Compounding #FundamentalAnalysis #LongTermInvesting

1

2

17

2,005

Elliott Management stirring the pot again. Bunzl’s been a steady compounder for years — defensive distribution play with solid margins. 5% stake is classic Elliott: enough to get a board seat and push for efficiencies or a break-up premium. Watch for margin expansion targets or portfolio pruning next.

14

Crypto Nelson retweeted

10 Jan 2024

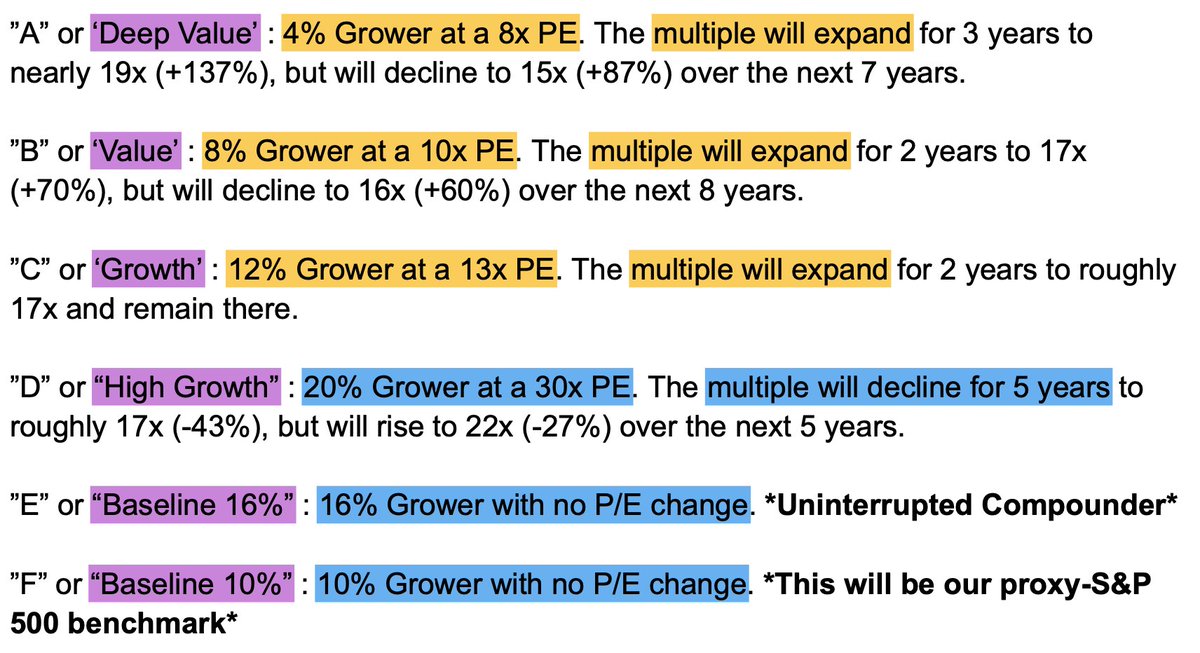

Yesterday my friend Andrew was sending me some amazing research work he’d done on whether “deep value” or “compounder” stocks should be considered more attractive?

Let me summarize his work and a few of his major takeaways:

Essentially, Andrew set out to assess the impact of changes in valuation multiples on your near-, mid-, and long-term returns and created a visual that may surprise some of you!

He starts by asking a question: Which business would you rather buy:

A) A business that compounds at 4% but that is trading at a very low multiple (below 10x earnings) or

B) A great business that compounds at 20% but that is trading at a much higher multiple (>30x earnings).

He highlights that there is not one correct answer to the question and an intelligent investor would need to ask some follow-up questions such as …

❓ #1 How certain am I that these growth rates will persist that long into the future?

❓ #2 Where will my returns come from (i.e. - multiples vs growth)

❓ #3 How long will it take me to achieve these returns?

In order to visualize where the actual return from stocks comes from over time he came up with 6 different kinds of stocks:

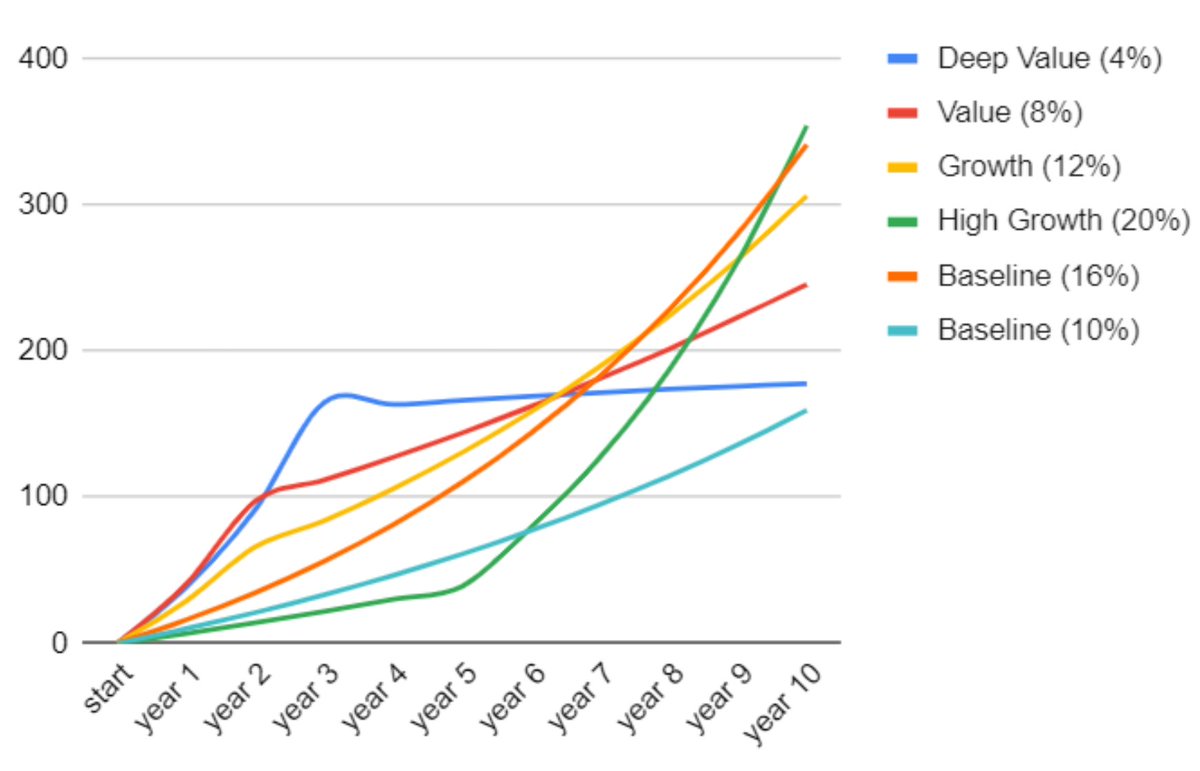

He then proceeded with a chart that visualizes the returns of each stock over time:

I’ll share his major takeaways in the next tweet below ⬇️

14

41

276

112,405

Doctor ni pilavakunda , compounder ni pilusthaarra eddi lanjodaka

2

837

Studying a high-quality health tech compounder rather than a traditional outsourcing co.

Not only in revenue growth but there is an ability to build a scalable, AI-enabled platform with recurring revenues, strong operating leverage n high customer retention.

Stay connected ~~

7

#Shreeref has given 100% in last 3 months...

A quality SME compounder...

Yet PE is still within range..

Does it have some gas left? Or Train has crossed the station now?

#moneymatterswithcj #investing #usirandeal

Jun 7

Weekend Stock Analysis: Shree Refrigerations

Strong business quality. Medium governance risk.

Unique naval HVAC franchise. Richer valuation.

AI-assisted stock analysis human judgement.

Not SEBI registered.

Not investment advice.

DYOR

#MoneyMattersWithCJ #investing

1

93

6 year's but they sold off the company so that's the only reason I left next job was 6 years chemical compounder. 80-90 hours a week covered in bad chemicals daily so gf of then 14 years 1st pregnancy asked me to leave for health reasons.

10