May 16

纳斯达克上市公司 Datavault AI(NASDAQ:DVLT)发布了截至 2026 年 3 月 31 日 Q1 业务更新。报告显示,该公司已签署超过 8 亿美元的代币化合同,预计 2026 年将确认近 1 亿美元的费用收入。第一季度实现营收 340 万美元,同比增长 443%,增长主要得益于对 CompuSystems Inc.(CSI)的收购。此外,该公司通过 6000 万美元的普通股注册发行使营运资金达到约 1.4Target 亿美元;并获得了 1.2 亿美元的非稀释性资金。wublock123.com/news/news-611…

6

1

2,489

May 15

$DVLT Q1 2026 earnings: Grand Vision Collides with Severe Cash Burn and Margin Collapse

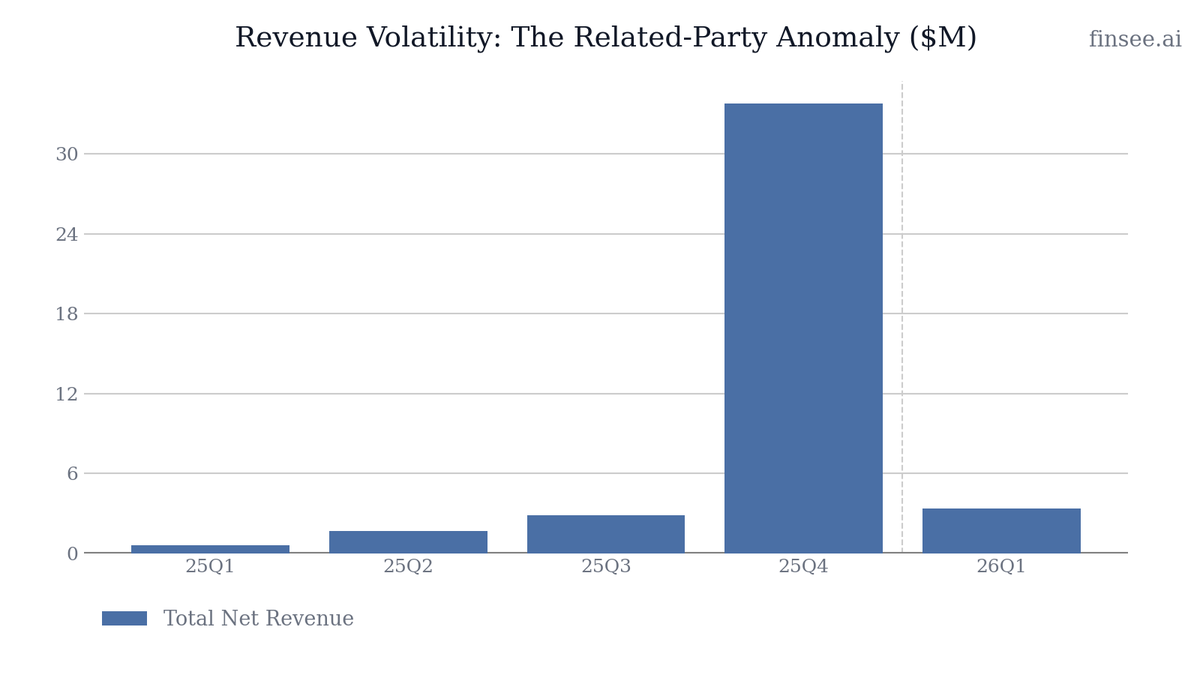

Datavault AI's Q1 2026 results expose a massive gulf between management's multi-trillion-dollar visionary narrative and the company's deteriorating financial reality. While the company highlights $800M in signed tokenization contracts and reiterates a $200M FY26 revenue target, Q1 revenue was just $3.4M. Stripping out the Q4 2025 $30M related-party patent license anomaly, core operations are highly unprofitable. Gross margin collapsed to 3%, operating expenses exploded 227% YoY to $31.1M, and the company posted a $53.1M net loss. With only $2.2M in cash remaining, survival currently depends entirely on hyper-dilutive ATM equity issuance and volatile crypto assets.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐬𝐬𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 — Management claims to have signed $800M in tokenization contracts in Q1, which are expected to generate nearly $100M in fees recognized in 2026. If these materialize into cash, it validates the Real-World Asset (RWA) tokenization strategy.

• 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐅𝐮𝐧𝐝𝐢𝐧𝐠 — The company secured $120M in non-dilutive funding from Scilex to roll out the SanQtum AI quantum-ready GPU network across 100 U. S. cities, positioning DVLT as a foundational AI infrastructure provider.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐫𝐞 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐨𝐧𝐬 𝐇𝐚𝐯𝐞 𝐍𝐞𝐠𝐚𝐭𝐢𝐯𝐞 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 — The newly acquired Live Event Production segment generated $2.5M in revenue but cost $2.8M to operate, yielding a negative gross margin. The company is losing money on every event before even factoring in $31.1M of operating expenses.

• 𝐄𝐱𝐭𝐫𝐞𝐦𝐞 𝐃𝐢𝐥𝐮𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐂𝐫𝐮𝐧𝐜𝐡 — Despite a massive $30M ATM equity raise this quarter, the cash balance ended at a dangerously low $2.2M. The weighted average share count has exploded from 53.6M a year ago to 574.2M, severely diluting existing shareholders.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴🔴

Strong Bearish. The financial foundation is crumbling. Management is aggressively promoting future exchange launches and AI infrastructure while the core business generates a 3% gross margin, burns massive amounts of cash, and relies on unpredictable related-party deals and crypto asset valuations.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐥𝐥𝐚𝐩𝐬𝐞 𝐚𝐧𝐝 𝐍𝐞𝐠𝐚𝐭𝐢𝐯𝐞 𝐔𝐧𝐢𝐭 𝐄𝐜𝐨𝐧𝐨𝐦𝐢𝐜𝐬 [NEW]

Overall gross margin decelerated drastically from 11% in Q1 2025 to just 3% in Q1 2026. The primary culprit is the newly acquired CompuSystems (CSI) business. The 'Live Event Production' segment reported $2.49M in revenue against $2.79M in costs—a fundamentally broken unit economic profile that destroys value with every sale. Cost control measures are urgently needed.

🔴 𝐓𝐡𝐞 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐂𝐫𝐞𝐝𝐢𝐛𝐢𝐥𝐢𝐭𝐲 𝐆𝐚𝐩

Management reiterated a $200M revenue target for FY26. With only $3.4M achieved in Q1, the company must average over $65M per quarter for the rest of the year. Historically, the only time the company achieved eight-figure revenue was Q4 2025 ($33.8M), which was heavily reliant on a one-time $30M related-party patent license. Without similar one-off injections, hitting this accelerating trajectory is highly improbable.

🔴 𝐂𝐫𝐲𝐩𝐭𝐨 𝐓𝐫𝐞𝐚𝐬𝐮𝐫𝐲 𝐑𝐢𝐬𝐤 𝐑𝐞𝐚𝐥𝐢𝐳𝐞𝐝 [NEW]

The company's reliance on holding crypto assets introduced massive earnings volatility. In Q1 2026, the company recorded a $16.1M fair value loss on crypto currency and an $822k loss on the sale of Bitcoin. Total crypto assets shrank from $92.2M to $57.1M. For a company with only $2.2M in hard cash and an $8.7M quarterly operating cash burn, this volatility represents a severe liquidity risk.

🟢 𝐑𝐞𝐚𝐥-𝐖𝐨𝐫𝐥𝐝 𝐀𝐬𝐬𝐞𝐭 (𝐑𝐖𝐀) 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 [NEW]

Management is aggressively positioning the company as the tollbooth for digital asset tokenization, leaning on their NYIAX acquisition and NASDAQ Financial Framework integration. In Q1, the company signed approximately $750M to $800M in new tokenization contracts. The H2 2026 planned launches of the International Elements Exchange (IEE) and Sports Illustrated Exchange (SiX) are the critical catalysts needed to convert this backlog into recognized revenue.

🟢 𝐒𝐚𝐧𝐐𝐭𝐮𝐦 𝐀𝐈 𝐄𝐝𝐠𝐞 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐑𝐨𝐥𝐥𝐨𝐮𝐭 [NEW]

In a pivot toward hardware and infrastructure, Datavault AI executed a term sheet for $120M in funding from Scilex to deploy a quantum-ready distributed GPU edge network. Launching first in New York and Philadelphia, the network aims to scale to 100 U. S. cities and 48,000 GPUs by the end of 2026. If executed, this provides a highly tangible, recurring revenue stream compared to their more speculative blockchain exchange projects.

⚪ 𝐌𝐚𝐜𝐫𝐨 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝: 𝐀𝐧𝐭𝐢𝐜𝐢𝐩𝐚𝐭𝐢𝐨𝐧 𝐨𝐟 𝐭𝐡𝐞 𝐂𝐋𝐀𝐑𝐈𝐓𝐘 𝐀𝐜𝐭 [NEW]

Management specifically highlighted the pending CLARITY Act as a crucial macro tailwind. By building integrated AI-driven cyber risk mitigation (via the planned CyberCatch acquisition) and continuous compliance, Datavault AI is attempting to front-run regulatory frameworks to attract institutional capital to its tokenized asset markets.

🔴🔴 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐄𝐱𝐩𝐥𝐨𝐬𝐢𝐨𝐧 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧

Operating expenses are accelerating aggressively, hitting $31.1M in Q1 2026 (up 227% YoY). General and administrative expenses alone were $18.7M, fueled by a $4.4M increase in salaries/stock-based comp and massive consulting/legal fees ($4.1M combined). This bloated cost structure is unsustainable against a $3.4M revenue base.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐍𝐞𝐭 𝐋𝐨𝐬𝐬 (𝐐𝟏 𝟐𝟎𝟐𝟔): $(53.1) million

Reversing sharply from the brief $0.66M profit seen in Q4 2025. The loss was amplified by heavy non-operating items, including a $16.1M fair value loss on crypto assets, $2.5M impairment of non-marketable securities, and $16.8M in net other expenses.

𝐖𝐞𝐢𝐠𝐡𝐭𝐞𝐝 𝐀𝐯𝐞𝐫𝐚𝐠𝐞 𝐒𝐡𝐚𝐫𝐞𝐬 𝐎𝐮𝐭𝐬𝐭𝐚𝐧𝐝𝐢𝐧𝐠: 574.2 million

Accelerating dilution. Up roughly 10x from the 53.6M share count in Q1 2025. During Q1 2026 alone, the company raised nearly $30M via an At-The-Market (ATM) offering. The May 2026 $60M registered direct offering will dilute the equity base even further.

𝐑𝐞𝐥𝐚𝐭𝐞𝐝 𝐏𝐚𝐫𝐭𝐲 𝐑𝐞𝐜𝐞𝐢𝐯𝐚𝐛𝐥𝐞: $29.5 million

Stable, but highly concerning. This likely stems from the $30M related-party patent license revenue booked in Q4 2025. The fact that it only decreased by $0.5M in Q1 indicates Datavault has not yet collected the cash for its single largest historical revenue event.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘 𝟐𝟎𝟐𝟔 𝐓𝐨𝐭𝐚𝐥 𝐍𝐞𝐭 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $200 million

Accelerating dramatically. Reiteration of this target requires an astronomical leap in run-rate from Q1's $3.4M. Management expects this to be heavily back-end loaded in H2 2026, relying on nearly $100M in expected tokenization fees and the launches of the IDE, SiX, and NYIAX exchanges.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐋𝐢𝐯𝐞 𝐄𝐯𝐞𝐧𝐭 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲

The newly acquired Live Event Production segment generated a negative gross margin this quarter, with costs exceeding revenue by nearly $300k. What specific structural changes or pricing actions are being implemented to make this segment profitable?

𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐁𝐫𝐢𝐝𝐠𝐞 𝐭𝐨 $𝟐𝟎𝟎𝐌

Given the lack of patent license revenue in Q1 and a baseline run-rate of $3.4M, how much of the projected $200M target is strictly transaction-based fees from the H2 exchange launches versus recurring SaaS or stable licensing agreements?

𝐑𝐞𝐥𝐚𝐭𝐞𝐝 𝐏𝐚𝐫𝐭𝐲 𝐂𝐚𝐬𝐡 𝐂𝐨𝐥𝐥𝐞𝐜𝐭𝐢𝐨𝐧

The balance sheet still shows a $29.5M related-party receivable. When do you expect to collect cash on the $30M patent license booked in Q4, and how does this impact your near-term liquidity planning?

𝐂𝐫𝐲𝐩𝐭𝐨 𝐓𝐫𝐞𝐚𝐬𝐮𝐫𝐲 𝐑𝐢𝐬𝐤 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭

With a $16.1M fair value loss on crypto assets this quarter and only $2.2M in cash remaining, how is the treasury department hedging against further crypto volatility to ensure basic working capital needs are met without tapping the equity markets again?

1

7

2,346

Apr 28

Event Citadel (formerly CompuSystems), attended the @aga_naturalgas AGA Operations Conference and Spring Committee Meetings in Tampa, FL.

The AGA represents more than 200 local energy companies that deliver clean natural gas throughout the United States.

It was great to see what’s new in the industry and to highlight all our services as an all-in-one event registration solution.

A special thanks to the team who represented us on the floor for all your great work! 🌟

🌐 learn more: eventcitadel.com

#DatavaultAI #EventCitadel #CompuSystems #EventRegistration #RegistrationSoftware #AGA

1

4

21

1,405

Apr 23

CCP Compusystems because it will be cobbled together with Chinese parts

3

264

29 Oct 2025

DD on $DVLT as requested by @UhhHello :

- American company building AI-powered platforms to tokenize, value, and monetize data/assets via blockchain and Web 3.0

- Building software infrastructure for data security, HPC

Solid management team of innovators, but young

- CEO has 25% and other insiders have 25%, 1-5% institutional (big funds like Synergy hold tiny stake), retail heavy at 50%

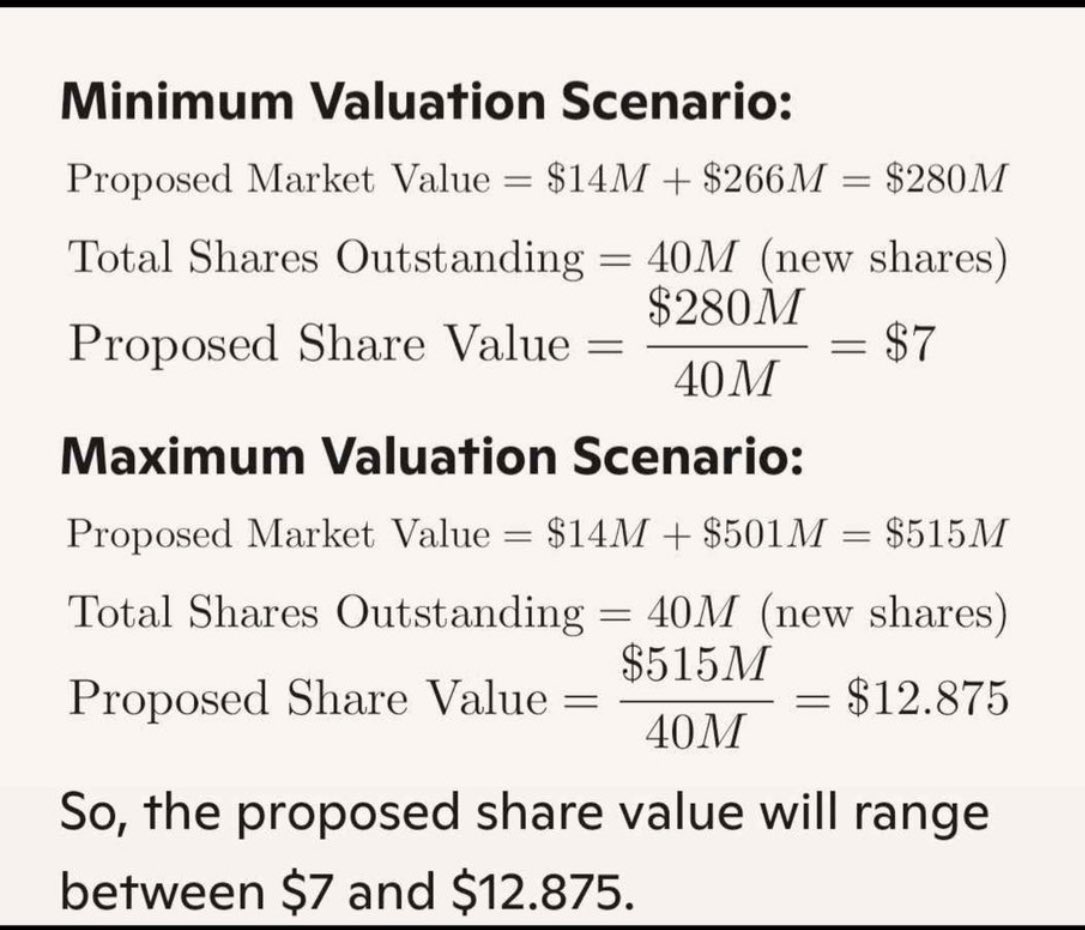

- 2024 Revenue $2.7M, 2025 Revenue expected $4.4M ; MC of $920M @ $3.23/share and 98M outstanding shares

- Strong potential revenue pipeline: $20M/year from CompuSystems acquisition, licensing deals like $2.5M NYIAX (ad tech) and GFT Rewards (Q3)

- $150M Scilex funding for scaling

- 2026 target >$50M (recurring from tokenization in biotech, energy, healthcare), focus on "data unions" for insurance/accounting

- Partnerships with IBM ($5M tech 20K engineer hours for AI boost), Wellgistics (blockchain drug tracking via PharmacyChain), Max International (Swiss RWA exchange for tokenized assets), Nature's Miracle (carbon credits), Burke Products (defense tech contracts)

- Patented DataScore®/DataValue® agents for secure data valuation, ADIO® inaudible tones for fan rewards/esports, new data unions tokenizing insurance/accounting data, quantum/AI centers

- Revenue exploding 200% YoY

- Nasdaq compliance regained

- Cash flow negative, large R&D expenses

- Convertible notes closings add debt pressure

- Potential Q4 IP lawsuits

Management/Talent: 6

Sector Potential: 8

Innovation: 7

Value (over/under): 8

Potential for 100% returns or more: 8

Sympathy Stock Plays: $YYAI $PXLW $ATCH $PHR $MARA

P/S Ratio: 200x (extremely high)

**My two cents**: Lots of momentum seen on this name by retail, and lots of partnerships with very interesting revenue pipeline. Beware of dilution, very volatile stock. Not sure I would enter this until under $2.50 or so. No position.

Not financial advice. Do your own DD.

2

4

1,491

21 Oct 2025

Here's Why Datavault AI's Deal-Making Precision Could Add Commas and Zeros to Its Revenue Future (NASDAQ: $DVLT)

BEAVERTON, OR / ACCESS Newswire / October 21, 2025 / Datavault AI (NASDAQ: $DVLT) isn't waiting around for the digital economy to arrive; it's building it. The company's latest partnership with Max International AG in Switzerland has officially shifted the conversation from "what if" to "what's next."

The collaboration centers on the launch of the Swiss Digital RWA Exchange, a platform designed to anchor real-world assets inside one of the world's most regulated financial environments. Switzerland, the land where 70% of global gold refining and trading happens, offers the perfect balance between trust and transformation. It's the same country that hosts the SIX Digital Exchange - NASDAQ's long-time tech ally and the world's leading infrastructure for digitized assets.

That's not a coincidence. It's precision.

The partnership also addresses three key issues that have deterred institutional investors: regulatory uncertainty, technological scalability, and fiduciary trust. By pairing Datavault AI's patented data infrastructure with Max International's licensed Swiss framework, they're building something far bigger than an exchange. They're building infrastructure for proof, where ownership, compliance, and value are verified before a single trade clears.

Factoring Guidance with Expansion

Datavault AI's growth story was already impressive. The company's guidance points toward $40 million to $50 million in 2026 revenue - an impressive leap from its earlier trajectory. But that was before a cascade of recent deals.

Consider the CompuSystems acquisition, an asset purchase that management anticipates will contribute up to $20 million in annual revenue by 2026. It gives Datavault not just scale, but immediate cash-flow visibility. Then there's the licensing deal with GFT Rewards, using Datavault's ADIO® technology to drive mobile-reward engagement systems. That agreement is already projected to generate measurable revenue in Q3 2025; not "someday," but soon.

And perhaps most impressive: a $150 million strategic investment from Scilex Holding Company, earmarked for rapid infrastructure expansion that allows the company's treasury to become a growth engine. For a company trading at small-cap valuations, that's not a check; it's an endorsement.

Each of these deals would be noteworthy on its own. Together, they form the blueprint for something exponential. Guidance becomes the floor, not the ceiling.

The Platforms Driving the Optimism

At the heart of all this is Datavault AI's proprietary technology. Its patented DataValue® and DataScore® systems utilize algorithmic intelligence to assess and validate assets that don't traditionally trade on open markets, including unmined minerals, intellectual property, and even name, image, and likeness rights. In a market that craves transparency, this tech doesn't just create data. It creates confidence.

The company's global patent portfolio spans the U.S., Europe, and Asia, covering data tokenization, digital twins, and automated compliance - a trifecta that makes it nearly impossible to replicate. Now pair that with a Swiss-regulated environment, and you have a fortress-grade foundation for institutional participation.

Zurich's financial gravity can't be overstated. The city doesn't just hold vaults; it defines the global rules of custody and capital. By embedding inside that ecosystem, Datavault AI and Max International gain more than a prestigious address. They gain credibility that few small-caps could accrue.

Their immediate milestone is to complete the first fully compliant trade on a regulated, stable-value digital platform, a move that could redefine how institutions interact with real-world assets. Once that proof point hits, expect the story to change from "potential" to "pipeline."

The Bigger Opportunity

This is where Datavault AI becomes more than a headline. Between the Swiss partnership, the Scilex capital injection, the CompuSystems acquisition, and a suite of licensing deals, the company has evolved into a full-spectrum player in the digitized-value economy.

Yes, risk remains; it always does. Execution, regulation, and timing will decide how quickly this story scales. But Datavault isn't chasing a trend. It's laying down tracks for the financial system's next layer of infrastructure.

And that's what makes this moment stand out. It isn't another tech buzzword play or speculative sprint. It's a disciplined, regulated, institutionally anchored leap toward something real. Datavault AI has already built the backbone of tomorrow's data-driven economy. With Max International AG, it's now wiring that backbone into the world's most trusted financial grid.

Because when Swiss precision meets patented intelligence, you don't just get a new market trend.

5

1,833

17 Oct 2025

Work with a team that supports you, and your community.

Auto-Star Compusystems is looking for a Sales Representative in Medicine Hat to help local small businesses grow with our ClearTEQ POS and Merchant Services solutions.

If you’re passionate about connecting with local business owners and being part of a community-minded, collaborative, and supportive organization, we’d love to hear from you!

📍 Location: Medicine Hat, Alberta

💼 Full-Time, Permanent

📩 Apply today: auto-star.com/careers

Be part of a team that’s been helping retailers across North America succeed for over 40 years, and growing right here in Medicine Hat.

1

3

90

20 May 2025

$DVLT Datavault AI To Finalize Strategic Acquisition Of CompuSystems Assets; Deal Expected To Drive 2H 2025 Revenue And Contribute $15M - $20M To 2026 Revenue Target And Growth Opportunities For Both Acoustic And Data Divisions

1

432

13 Feb 2025

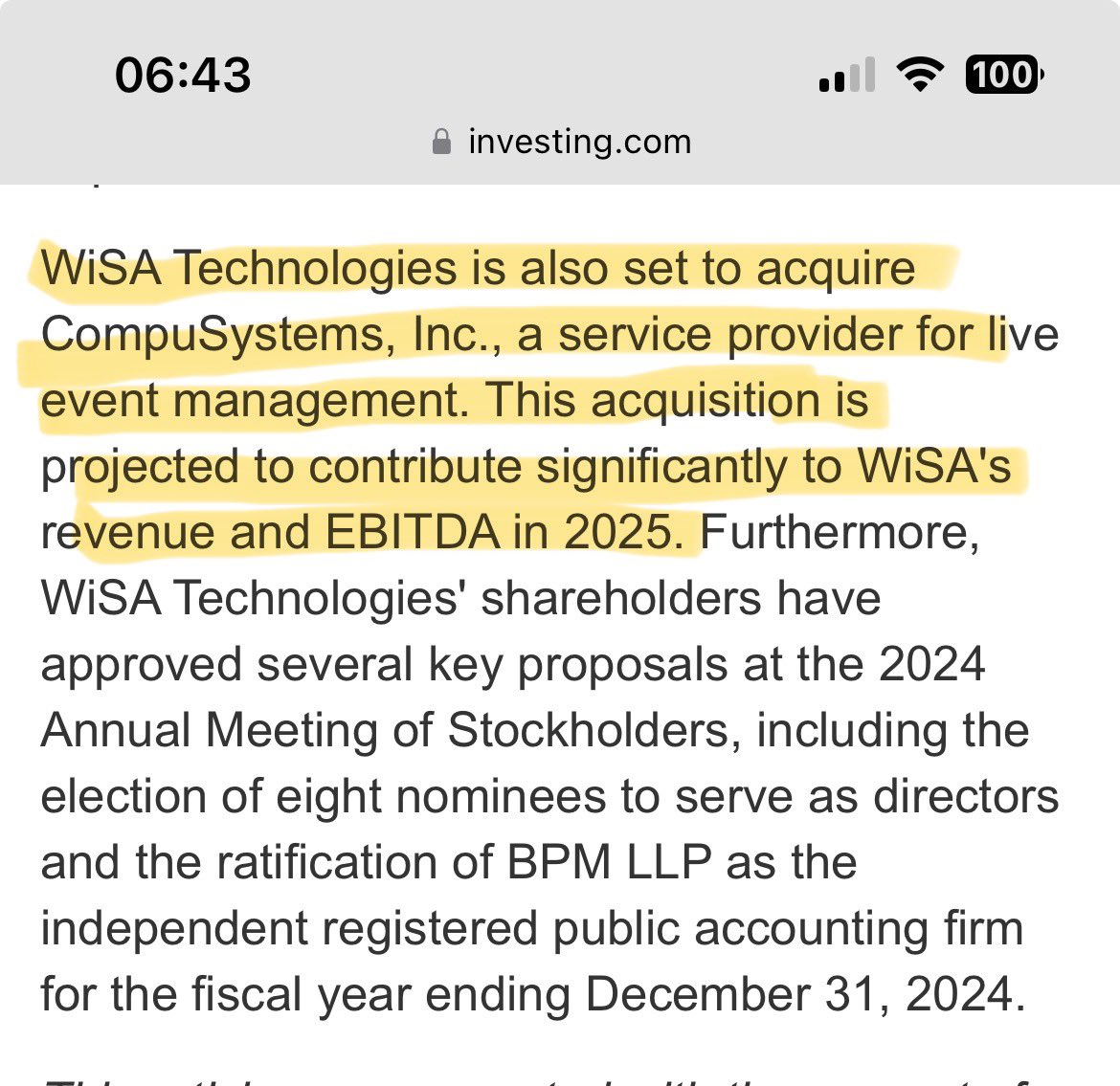

$WISA - NEWS!!!! Lets Go 📈 ⬆️

“WiSA Technologies is also set to acquire CompuSystems, Inc., a service provider for live event management. This acquisition is projected to contribute significantly to WiSA's revenue and EBITDA in 2025.”

1

436

13 Feb 2025

📢 $WiSA files Form 8-K

Includes audited financials of CompuSystems, Inc. and pro forma financials reflecting the acquisition. The new ticker change is coming soon! 🕒

#stockstowatch

#news #fyp #FollowMe #Investors #Finance #StockMarket $pev $avgr #MergersAndAcquisition

#wisa

2

502

8 Jan 2025

$WISA- 2025 business transformation in progress:

-Data Vault asset purchase and merger completed

-Restructuring of management completed

-Name changed to Data Vault with new ticker symbol ADIO coming soon

-Acquisition of Compusystems to close by EOM per management

1

2

5

5,324

3 Jan 2025

$WISA- You got that right! Starts with Data Vault, then add Compusystems to the portfolio at the EOM. A banner year coming for 2025? I think so, I know I will be holding a core position all year

1

3

376

31 Dec 2024

وقعت شركة WiSA Technologies اتفاقية نهائية للاستحواذ على CompuSystems، متوقعة إيرادات تتراوح بين 13 و15 مليون دولار و3 إلى 4 ملايين دولار قبل الفوائد والضرائب والإهلاك والاستهلاك في عام 2025؛ يعزز الاستحواذ تحقيق الدخل من بيانات الفعاليات وينشط تقنية ADIO لـ 1.4 مليون مشارك؛ من المقرر عقد مؤتمر عبر الهاتف

👇👇👇👇👇

في 30 ديسمبر 2024، الساعة 11 صباحًا بالتوقيت الشرقي؛ لم يتم الكشف عن الشروط المالية سعرها الان 2.51

ليست توصية شراء وبيع ولاكن للعلم 🌹

5

12

32,506

31 Dec 2024

وقعت شركة WiSA Technologies اتفاقية نهائية للاستحواذ على CompuSystems، متوقعة إيرادات تتراوح بين 13 و15 مليون دولار و3 إلى 4 ملايين دولار قبل الفوائد والضرائب والإهلاك والاستهلاك في عام 2025؛ يعزز الاستحواذ تحقيق الدخل من بيانات الفعاليات وينشط تقنية ADIO لـ 1.4 مليون مشارك؛ من المقرر عقد مؤتمر عبر الهاتف

👇👇👇👇👇

في 30 ديسمبر 2024، الساعة 11 صباحًا بالتوقيت الشرقي؛ لم يتم الكشف عن الشروط المالية سعرها الان 2.51

ليست توصية شراء وبيع ولاكن للعلم 🌹

2

3

7

23,701

30 Dec 2024

$WISA Technologies, Inc. (WISA) recently announced that it has entered into a definitive agreement to acquire CompuSystems, Inc. for an undisclosed amount.

1

1

371

30 Dec 2024

WiSA Technologies Hosts Conference Call Today to Discuss its Previously Announced Definitive Agreement to Acquire CompuSystems, Inc. $WISA crweworld.com/article/news-p…

2

350