BSB ATV 🍆 retweeted

@apple Aqui é a ANT rainha ADB que roubou nosso trabalhos por anos @Adobe @Photoshop @Lightroom @AdobeDesign @creativecloud

4

4

39

Lernen Sie professionelle Druck- und Online-Grafiken mit der Adobe #CreativeCloud zu gestalten! In unserem Einsteiger-Paketkurs vom 20. bis 22. Juli 2026 lernen Sie die Grundlagen von Illustrator, Photoshop und InDesign kennen.🎨💻📐Jetzt anmelden: wildkolleg.de/?wk=187

ALT Ein Laptop, auf dem ein Layout einer Broschüre zu sehen ist, welche mit Adobe Illustrator, Photoshop, InDesign und Adobe Acrobat gestaltet wurde. Darüber der Text „Adobe Paket Grafik-Schulung. Creative Cloud Bundle-Training vom 20. bis 22. Juli 2026.“

5

Adobe raises FY2026 outlook but ADBE selloff shows AI confidence gap is widening business-news-today.com/adob… $ADBE #Adobe #CreativeCloud #ArtificialIntelligence #GenerativeAI #SoftwareStocks #NASDAQ #AdobeFirefly #Canva #USStocks #ADBE

22

Here is a recopy of a good email I did for @creativecloud

I improved the subject line.

I made the hook stronger .

I made it more conversational

1

7

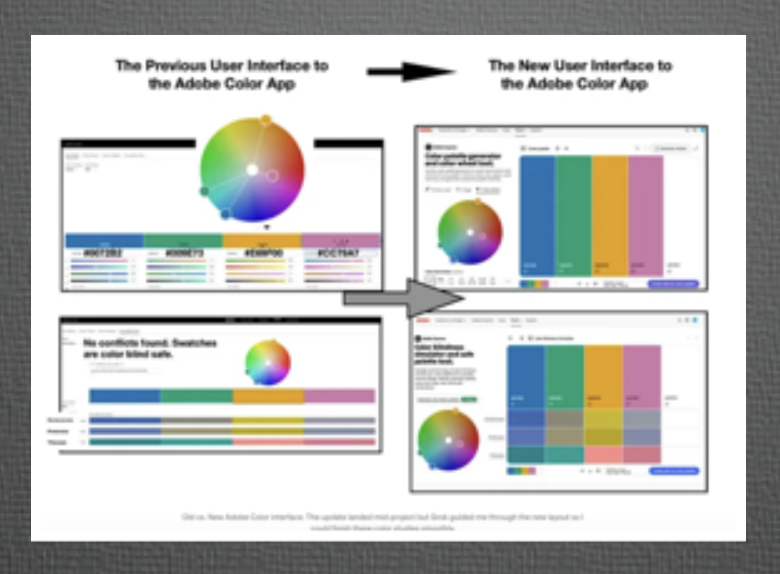

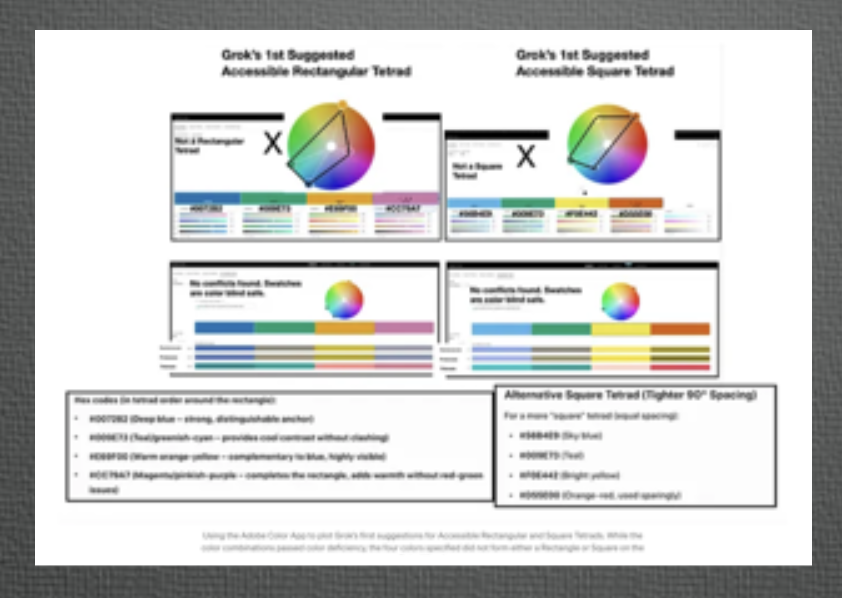

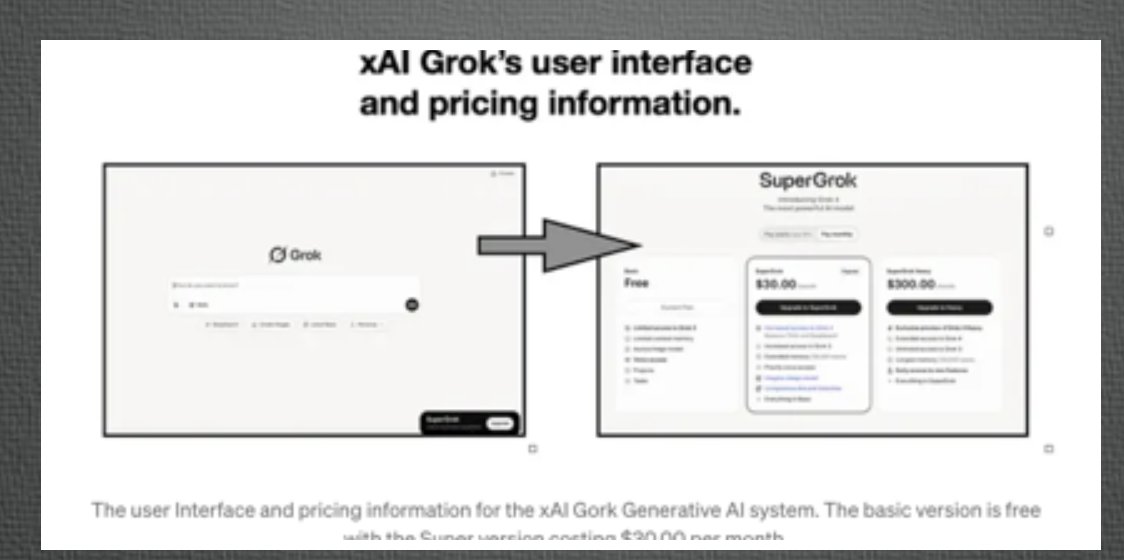

#Grok New Adobe Color Interface #uxdesigncc #medium #creativecloud #Adobe #ChatGPT #GoogleAI #MSFTCopilot #Color & #DeepSeek #generativeaihub #uxdesigncc #visualization #AntropicAI #Grok uxdesign.cc/how-grok-guided-…

15

@Adobe @creativecloud How do I peacefully cancel my subscription. Your chat bot cannot help me. I have followed the process but it keeps getting stuck and I seem to not be the only one having this challenge . Please help, I am getting anxious.

1

19

Maria retweeted

Hat's off to Ellie Warnke for designing her own ready-to-wear line with the help of Adobe Creative Cloud Pro. 🤠 From tech packs to design decisions, Creative Cloud is the perfect toolbox to have up your sleeve.

Save over 70% off student subscriptions when you sign up: adobe.ly/4xlza9n

🎨: IG | elliewarnke

11

1

2,085

. retweeted

Graphstorm's #AdobeIllustrator game design is next level. 👾 Watch them quickly create a scene using the Turntable feature to see their characters from multiple perspectives.

Side quest idea? Go try Turntable in Adobe Illustrator: adobe.ly/4vM7zN6

🎨: IG | graphstorm

2

8

2,113

Josie retweeted

Jacob Guerreo makes a splash with the latest additional to his portfolio, a summer-inspired video created with #AdobeIllustrator and #Premiere on iPhone. 🌊

Level up your portfolio with Adobe Creative Cloud Pro: adobe.ly/3S29QFm

🎨: IG | createdbyjacobg

3

3

1,885

Jun 12

進化し続けるアドビの最新ツール、しっかり追いきれていますか?🚀

Creative Cloudエバンジェリスト、アドビの仲尾毅さん(@tsuyon)が #ギークリ に登場!

アドビの最新技術情報をいちはやくお届けします。

CC道場(YouTube)以外で仲尾さんのお話が聞ける貴重な時間です👀✨

それも群馬県庁で聞けるなんてなかなかありません!

📅 7/25(土)群馬県庁32階「NETSUGEN」

🎟️ 参加無料👇 geekcreators2026gunma.peatix…

#Adobe #CreativeCloud #群馬県庁 #前橋 #NETSUGEN

8

18

2,557

Jun 11

Los agentes de @AdobeCare trabajan todos los días hasta las 14:00 horas, entonces uno no puede hacer cambios ni recibir ayuda hasta el día siguiente. @AdobeLat @CreativeCloud

20

Jun 11

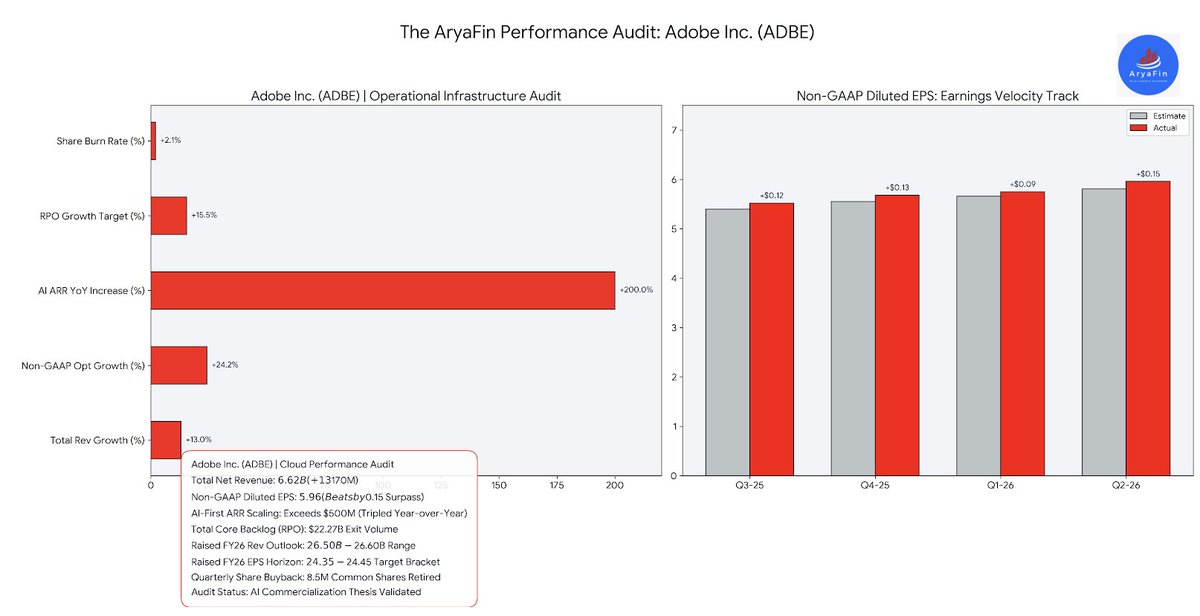

🎨 AryaFin Ticker Audit | $ADBE Q2 Fiscal 2026

Audit: Explosive AI Monitization and Enterprise Firefly Adoption Supercharge Adobe to a Dominant Top- and Bottom-Line Double Beat as Leadership Raises Full-Year Targets to Invalidate Churn Fears.

📊 Q2 Fiscal 2026 Core Financial HighlightsTotal Net Revenue: $6.62 Billion, reflecting a robust 13% YoY expansion (11% in constant currency) and outpacing consensus analyst models by a clean $170M.

* Non-GAAP Diluted EPS: $5.96, crushing Wall Street expectations ($5.81–$5.82) by $0.15. GAAP Diluted EPS: $4.25 (Reflecting a $0.17 per share non-cash goodwill impairment charge linked to its Publishing & Advertising division).

* Total Annualized Recurring Revenue (ARR): Exiting the quarter at an elite $27.10 Billion, including a $480M contribution from Semrush.

* Remaining Performance Obligations (RPO): Finished the quarter securely positioned at $22.27 Billion.

* Capital Return Allocation: Leveraged massive free cash flow to aggressively repurchase approximately 8.5 million common shares during the three-month window.

⚡ Operational Velocity & AI InflectionAI ARR Triple-Digit Scale:

The primary bear-case anxiety—the threat of generative AI disruption to Adobe's software monopoly—was fundamentally disproven. Adobe's AI-first ARR tripled year-over-year, surging past the $500 million landmark on rampant commercial demand for its generative workflows.

* Enterprise Infrastructure Gains: Momentum was amplified by strong creative cohort conversions and localized enterprise scaling of its newly deployed CX Enterprise AI agent framework.

* Raised Forward Guidance Blanket: Armed with robust execution, management raised its structural full-year fiscal 2026 outlook across all core categories:

* Q3 Revenue Forecast: Formally anchored at $6.67B–$6.72B vs. the $6.51B consensus.

* Full-Year FY26 Revenue Guidance: Raised to a range of $26.50B–$26.60B.

* Full-Year FY26 Non-GAAP EPS Guidance: Lifted to $24.35–$24.45 to eclipse the $23.56 Wall Street benchmark.

The Read: Short Invalidation via True Productive AI Monetization. Heading into this print, the market priced Adobe at a massive structural discount, holding it near multi-year lows under severe narrative anxiety. This report completely shatters that thesis.

By cleanly proving that generative toolsets are driving incremental subscription expansion—rather than cannibalizing seat counts—Adobe has cemented its position as a primary application orchestration layer.

The double-digit backlog scaling paired with an immediate tripling of its AI annualized recurring revenue establishes a rock-solid structural margin floor.

Portfolios are heavily rewarded by aggressively accumulating this tier-1 cloud anchor on any near-term broader index distribution shelves.

#Adobe #ADBE #CreativeCloud #GenerativeAI #Firefly #EarningsBeat #AryaFin

2

184