Can UiPath stock recover as agentic automation revenue growth rebuilds the PATH story? business-news-today.com/can-… $PATH #UiPath #AgenticAI #AutomationSoftware #EnterpriseAI #NYSE #Deloitte #Databricks #SoftwareStocks

1

1

110

🚨 SOFTWARE STOCKS BLOODBATH IN 2026 😱

YTD Performance

- $INTU (Intuit) → -52%

- $ASAN (Asana) → -51%

- $HUBS (HubSpot) → -50%

- $TEAM (Atlassian) → -47%

- $MNDY (Monday.com) → -46%

- $WDAY (Workday) → -40%

- Figma → -39%

- $DUOL (Duolingo) → -38%

- $BILL → -34%

- $PATH (UiPath) → -33%

- $NOW (ServiceNow) → -33%

- $CRM (Salesforce) → -32%

- $ADBE (Adobe) → -30%

- $GTLB (GitLab) → -29%

- $DOCU (DocuSign) → -28%

- $SAP → -27%

- $FRSH (Freshworks) → -26%

- $SNOW (Snowflake) → -22%

The Reality Check:

Even the biggest and best-known software/SaaS names are down 30–52% this year. High valuations are getting crushed as growth slows and investors rotate into AI infrastructure plays.

Big contrast: While chips and AI hardware are booming, pure software is in a deep reset.

Are you buying any of these dips… or staying far away? 👇

#SoftwareStocks #SaaS #TechSelloff #Investing #2026Markets

1

1

195

Adobe (ADBE) posts record Q2 beat-and-raise, but stock falls on surprise CFO departure business-news-today.com/adob… $ADBE, #Adobe, #GenerativeAI, #AIsoftware, #SaaS, #Nasdaq, #TechEarnings, #SoftwareStocks, #USStocks #ADBE

33

🚨 SOFTWARE STOCKS BLOODBATH IN 2026 😱

YTD Performance

- $INTU (Intuit) → -52%

- $ASAN (Asana) → -51%

- $HUBS (HubSpot) → -50%

- $TEAM (Atlassian) → -47%

- $MNDY (Monday.com) → -46%

- $WDAY (Workday) → -40%

- Figma → -39%

- $DUOL (Duolingo) → -38%

- $BILL → -34%

- $PATH (UiPath) → -33%

- $NOW (ServiceNow) → -33%

- $CRM (Salesforce) → -32%

- $ADBE (Adobe) → -30%

- $GTLB (GitLab) → -29%

- $DOCU (DocuSign) → -28%

- $SAP → -27%

- $FRSH (Freshworks) → -26%

- $SNOW (Snowflake) → -22%

The Reality Check:

Even the biggest and best-known software/SaaS names are down 30–52% this year. High valuations are getting crushed as growth slows and investors rotate into AI infrastructure plays.

Big contrast: While chips and AI hardware are booming, pure software is in a deep reset.

Are you buying any of these dips… or staying far away? 👇

#SoftwareStocks #SaaS #TechSelloff #Investing #2026Markets

1

1

142

Adobe raises its 2026 outlook, but the stock drops as CFO Dan Durn exits

Winners: $FIG $MSFT $GOOGL $MRVL $AVGO $NVDA

Losers: $ADBE $ADSK $PTC $CRM $NOW $INTU

Listen to the Podcast - youtube.com/watch?v=JzpK130f…

Breaking News to Trading Moves

#StockMarket #Trading #Investing #DayTrading #SwingTrading #Adobe #ADBE #SoftwareStocks #AIStocks #TechStocks #Earnings #Figma #Marvell #Semiconductors #MarketSentiment

477

🚨 SOFTWARE STOCKS BLOODBATH IN 2026 😱

YTD Performance

- $INTU (Intuit) → -52%

- $ASAN (Asana) → -51%

- $HUBS (HubSpot) → -50%

- $TEAM (Atlassian) → -47%

- $MNDY (Monday.com) → -46%

- $WDAY (Workday) → -40%

- Figma → -39%

- $DUOL (Duolingo) → -38%

- $BILL → -34%

- $PATH (UiPath) → -33%

- $NOW (ServiceNow) → -33%

- $CRM (Salesforce) → -32%

- $ADBE (Adobe) → -30%

- $GTLB (GitLab) → -29%

- $DOCU (DocuSign) → -28%

- $SAP → -27%

- $FRSH (Freshworks) → -26%

- $SNOW (Snowflake) → -22%

The Reality Check:

Even the biggest and best-known software/SaaS names are down 30–52% this year. High valuations are getting crushed as growth slows and investors rotate into AI infrastructure plays.

Big contrast: While chips and AI hardware are booming, pure software is in a deep reset.

Are you buying any of these dips… or staying far away? 👇

#SoftwareStocks #SaaS #TechSelloff #Investing #2026Markets

1

206

Adobe (ADBE) reports fiscal Q2 earnings tonight as Wall Street treats the print as a referendum on AI and creative software business-news-today.com/adob… $ADBE, #Adobe, #AIsoftware, #SaaS, #GenerativeAI, #Nasdaq, #TechEarnings, #SoftwareStocks, #USStocks, #ADBE

40

Adobe has a $25bn buyback and famous software brands, so why is ADBE still under pressure? business-news-today.com/adob… Find out whether Adobe earnings can revive ADBE stock as AI disruption, CEO transition, and valuation pressure reshape investor sentiment. $ADBE #AdobeInc #AdobeFirefly #ArtificialIntelligence #SoftwareStocks #Nasdaq #CreativeCloud #ShantanuNarayen #USStocks #LargeCapStocks @Adobe

278

Jun 11

Adobe reports tonight. The AI question gets answered. 🎨

Q2 fiscal 2026 earnings drop after market close today—expected $5.81 EPS on $6.45 billion revenue. Wall Street wants one answer: can Adobe monetize generative AI, or is it eating the business alive?

The stock is down 8% in five days leading into this print. Down 30% year-to-date. Traders are pricing a big swing—either Adobe proves AI tools drive subscription growth, or the cannibalization thesis wins.

Here's the tension: Adobe's own AI destroyed its stock photo business. The company admitted it. Now the bet is whether Firefly and generative tools create enough new revenue to offset what they killed.

Analysts expect in-line numbers. The guidance is what matters. If Adobe can't show AI monetization path or subscription acceleration, this trades back to $400 support. If they nail it with raised outlook and conversion metrics, rally to $550 is in play.

The trade setup: cash position until the print. If earnings beat strong AI revenue guidance confirmed → long at $520 targeting $550 (stop $500). If soft guide or weak AI monetization → short to $400 (stop $525). Options pricing 8-12% move—respect that volatility.

Wait for the data. Don't guess.

#Adobe #ADBE #AI #ArtificialIntelligence #Earnings #TechStocks #GenerativeAI #Firefly #CreativeCloud #StockMarket #Trading #TechnicalAnalysis #EarningsReport #SoftwareStocks #DigitalMedia #CreativeSoftware #AITools #WallStreet

101

Jun 10

❗️I NEVER recommend low-quality stocks.

◆ Current Price: $103.61

◆ Complete Setup: 100 Shares

◆ Investment Required: $10,361

Why I'm watching:

Enterprise software spending remains resilient, and AI adoption continues creating new opportunities across industries. Companies positioned at the intersection of software and AI could be among the biggest beneficiaries of this long-term trend.

◆ Target Range: $248.58 – $250.72

◆ Potential Gain: $14,997 → $15,211

💥 Software remains one of the most important layers of the AI revolution. Access to the complete setup is 100% FREE — no fees, no subscriptions. Why? Because I believe investors should have the opportunity to evaluate quality setups before paying for anything.

👇 Drop a “SETUP” in the comments and like this post to get the full setup and target plan.

#SoftwareStocks #AI #Investing #Technology #Growth

14

🚨 SOFTWARE STOCKS BLOODBATH IN 2026 😱

YTD Performance (as of June 10)

- $INTU (Intuit) → -52%

- $ASAN (Asana) → -51%

- $HUBS (HubSpot) → -50%

- $TEAM (Atlassian) → -47%

- $MNDY (Monday.com) → -46%

- $WDAY (Workday) → -40%

- Figma → -39%

- $DUOL (Duolingo) → -38%

- $BILL → -34%

- $PATH (UiPath) → -33%

- $NOW (ServiceNow) → -33%

- $CRM (Salesforce) → -32%

- $ADBE (Adobe) → -30%

- $GTLB (GitLab) → -29%

- $DOCU (DocuSign) → -28%

- $SAP → -27%

- $FRSH (Freshworks) → -26%

- $SNOW (Snowflake) → -22%

The Reality Check:

Even the biggest and best-known software/SaaS names are down 30–52% this year. High valuations are getting crushed as growth slows and investors rotate into AI infrastructure plays.

Big contrast: While chips and AI hardware are booming, pure software is in a deep reset.

Are you buying any of these dips… or staying far away? 👇

#SoftwareStocks #SaaS #TechSelloff #Investing #2026Markets

1

216

🚨 SOFTWARE STOCKS BLOODBATH IN 2026 😱

YTD Performance (as of June 10)

- $INTU (Intuit) → -52%

- $ASAN (Asana) → -51%

- $HUBS (HubSpot) → -50%

- $TEAM (Atlassian) → -47%

- $MNDY (Monday.com) → -46%

- $WDAY (Workday) → -40%

- Figma → -39%

- $DUOL (Duolingo) → -38%

- $BILL → -34%

- $PATH (UiPath) → -33%

- $NOW (ServiceNow) → -33%

- $CRM (Salesforce) → -32%

- $ADBE (Adobe) → -30%

- $GTLB (GitLab) → -29%

- $DOCU (DocuSign) → -28%

- $SAP → -27%

- $FRSH (Freshworks) → -26%

- $SNOW (Snowflake) → -22%

The Reality Check:

Even the biggest and best-known software/SaaS names are down 30–52% this year. High valuations are getting crushed as growth slows and investors rotate into AI infrastructure plays.

Big contrast: While chips and AI hardware are booming, pure software is in a deep reset.

Are you buying any of these dips… or staying far away? 👇

#SoftwareStocks #SaaS #TechSelloff #Investing #2026Markets

1

236

Jun 9

#Oracle ( $ORCL) is seeing non-stop #institutionalinflows since mid-April!📈

Top 3⃣ AI #SoftwareStocks to Buy Now

📺WATCH➡️youtu.be/rUtRqlY-q8k

After a massive sell-off from $325, the stock is rebounding and approaching $250, making it a fascinating company that is back on the radar of #institutions.

Top 3⃣ AI #SoftwareStocks to Buy Now

📺WATCH➡️youtu.be/rUtRqlY-q8k

#Tech #AIstocks #Data #CloudComuting #Agentics

#StockMarket #Investing #Institutionalinvesting #StockRebound #Stocks #SaaS

3

274

Jun 8

#ServiceNow ( $NOW) is revolutionizing the business application layer with explosive 25% #earnings growth! 📈

Top 3⃣ AI #SoftwareStocks to Buy Now

📺WATCH➡️youtu.be/rUtRqlY-q8k

Instead of just helping workers, their embedded #AIagents are starting to actually do parts of the job, and #ChatGPT isn't replacing these ingrained workflows anytime soon.

#Tech #AIstocks #SaaS #Data #CloudComuting #Agentics #Enterprise #FutureOfWork #TechStocks #MoneyFlows #NOW

1

277

🚨 SOFTWARE / SAAS STOCKS – BRUTAL 2026 SO FAR 📉

Many leading software names are getting hammered this year amid higher rates, valuation resets, and growth slowdown fears:

📊 YTD PERFORMANCE

- Intuit $INTU → -52%

- Asana $ASAN → -51%

- HubSpot $HUBS → -50%

- Atlassian $TEAM → -47%

- Monday.com $MNDY → -46%

- Workday $WDAY → -40%

- Figma → -39%

- Duolingo $DUOL → -38%

- Bill.com $BILL → -34%

- UiPath $PATH → -33%

- ServiceNow $NOW → -33%

- Salesforce $CRM → -32%

- Adobe $ADBE → -30%

- GitLab $GTLB → -29%

- DocuSign $DOCU → -28%

- SAP $SAP → -27%

- Freshworks $FRSH → -26%

- Snowflake $SNOW → -22%

The theme?

High-growth SaaS names are under heavy pressure as investors rotate out of expensive growth stocks toward cyclicals, AI infrastructure, and value plays.

Quick Takeaways:

- Even blue-chip names like ServiceNow, Salesforce, Adobe & Snowflake are down 22–33%

- Smaller, higher-beta names (Intuit, Asana, HubSpot, Atlassian) have been hit hardest (-47% to -52%)

- AI-native or defensive software holding up better than pure growth plays

This contrasts sharply with the strength in AI infrastructure, semiconductors, and energy-related stocks we’ve seen recently.

---

👀 KEY QUESTION

Are you buying the dip in any of these software names, or staying away until the macro picture clears? Drop your thoughts below 👇

#SaaS #SoftwareStocks #Stocks #Investing #Tech #GrowthStocks

1

214

📉 BIGGEST LARGE-CAP LOSERS OF 2026 (YTD)

Not every stock is participating in the AI rally.

Several former market leaders are down double digits this year despite strong fundamentals.

🔻 HARDEST HIT STOCKS

🥇 $INTU — Intuit → -54.1%

🥈 $ZS — Zscaler → -39.9%

🥉 $INSM — Insmed → -39.7%

4️⃣ $CHTR — Charter → -38.2%

5️⃣ $CTSH — Cognizant → -35.3%

6️⃣ $TRI — Thomson Reuters → -34.0%

7️⃣ $WDAY — Workday → -31.1%

8️⃣ $DASH — DoorDash → -29.3%

9️⃣ $SHOP — Shopify → -27.9%

🔟 $PYPL — PayPal → -26.3%

🤖 AI STOCKS FEELING THE PAIN

📉 $ADBE → -26.2%

📉 $PLTR → -20.3%

📉 $APP → -17.1%

📉 $SNOW (not shown but widely watched)

Even some AI winners have experienced significant corrections as valuations reset.

💡 BIGGEST TAKEAWAYS

🔹 Software has been one of the weakest sectors

🔹 Cybersecurity names have seen major multiple compression

🔹 Consumer tech and fintech remain under pressure

🔹 Investors are becoming more selective on AI valuations

🔹 Quality businesses can still experience large drawdowns

👀 CONTRARIAN WATCHLIST

Some names now attracting value hunters:

🤖 $ADBE

🤖 $PLTR

🛒 $SHOP

💰 $PYPL

📊 $APP

☁️ $WDAY

⚡ $ZS

💭 THE QUESTION

Which of these beaten-down names has the best chance to stage a major comeback?

🤖 $PLTR

🛒 $SHOP

💰 $PYPL

📊 $APP

☁️ $WDAY

🎨 $ADBE

Drop your pick below 👇

#Stocks #Investing #StockMarket #GrowthStocks #AI #Fintech #SoftwareStocks 📉🚀

1

457

Can Autodesk’s $3.6bn MaintainX deal turn asset operations into its next growth engine? business-news-today.com/can-… Autodesk’s $3.6bn MaintainX deal pushes it beyond design into asset operations. Read why the valuation, AI data and workflow risk matter. $ADSK #Autodesk #MaintainX #Contech #IndustrialSoftware #AssetManagement #NASDAQ #AutodeskOperationsSolutions #DigitalTwins #SoftwareStocks @autodesk @maintainx

20

Jun 5

Think #AI will wipe out #Microsoft? Think again! 🛑

Top 3⃣ AI #SoftwareStocks to Buy Now

📺WATCH➡️youtu.be/rUtRqlY-q8k

$MSFT spans the entire AI stack—from #Azure cloud infrastructure to Office apps and AI #Copilot.

It is becoming the operating system of the AI era, making it a diversified bet across all layers of #enterpriseAI.

#AIstocks #SaaS #Data #CloudComuting #AIinfrastucture #Agentics #TechStocks #AIagents #MoneyFlows

4

210

Jun 5

Worried about an #AI-driven "#SaaSPocalypse"? 📉

Top 3⃣ AI #SoftwareStocks to Buy Now

📺WATCH➡️youtu.be/rUtRqlY-q8k

History says beware the panic! Just like the #dotcomcrash or #crypto winter, the true winners will survive, as #software remains completely essential for connecting our global world.

Are software companies going out of business? Absolutely NOT.

#SaaS #TechInvesting #TechStocks #TechHistory #AI #SoftwareSurvivors #AIstocks #ChatGPT #Bitcoin #GlobalFinancialCrisis #USDC #SoftwareMageddon

3

122

Jun 4

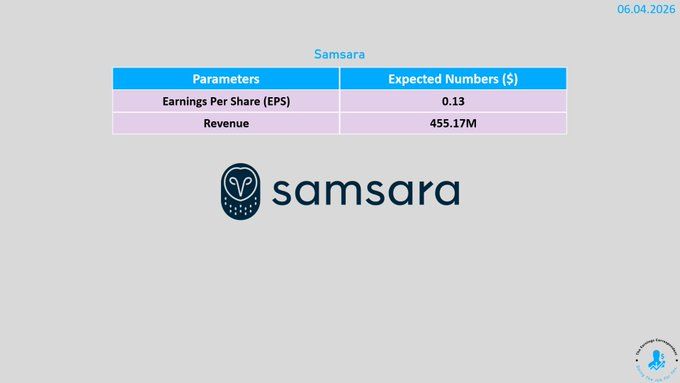

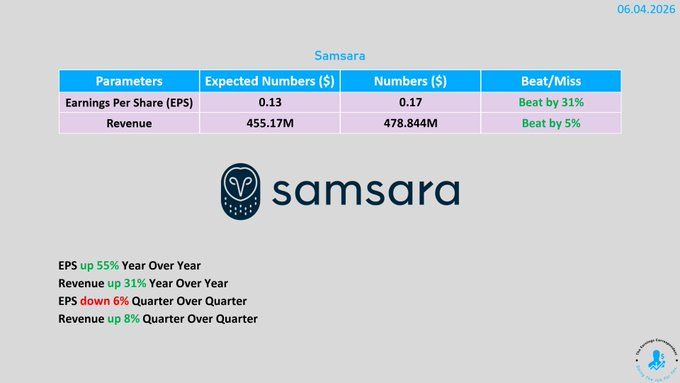

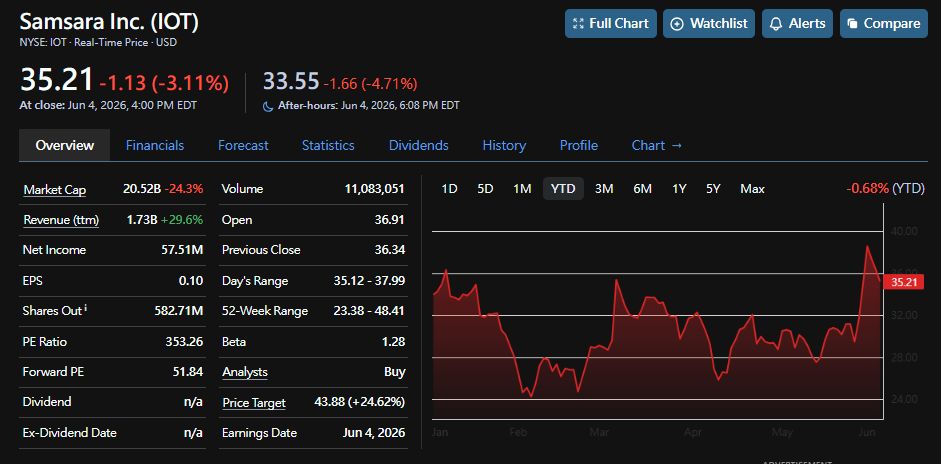

📡📉 $IOT is a perfect example of today’s software market: strong numbers are not always enough.

Samsara’s infographic shows a clean Q1 fiscal 2027 beat. EPS came in at $0.17 vs. $0.13 expected, beating by about 31%. Revenue was $478.8M vs. $455.2M expected, beating by about 5%. Revenue grew 31% year over year and 8% quarter over quarter, while EPS rose 55% year over year.

That is objectively strong execution. Samsara is still one of the best public examples of AI and IoT applied to real-world operations: fleets, logistics, construction, energy, field services, manufacturing, and safety. This is not just “AI chatbot” hype. It is connected physical operations, sensor data, workflow automation, and safety analytics.

So why did the stock fall after hours?

Because valuation and expectations matter. The screenshot shows a market cap around $20.5B, a trailing P/E near 353x, and a forward P/E around 51.8x. When a stock is priced like a premium compounder, a beat must come with enough guidance, margin expansion, ARR quality, and confidence to justify the multiple. In a risk-off tech tape, investors punish anything that is merely good instead of exceptional.

The bull case: Samsara is growing fast, has improving profitability, strong analyst support, and sits in a huge market where AI can improve safety, routing, compliance, and operating efficiency.

The bear case: the multiple is demanding, growth is decelerating from earlier years, competition is real, and any guidance caution can trigger multiple compression.

My read: $IOT remains a high-quality growth company, but the stock is not cheap. The post-earnings dip says investors want proof of durable profitable growth, not just headline beats.

📌 Watch: ARR growth, large customers, net retention, operating margin, FY27 guide, AI product adoption.

@Samsara @NYSE @Microsoft @nvidia @Salesforce

#IOT #Samsara #SaaS #AI #Earnings #SoftwareStocks

Not financial advice. ⚠️

1

3

538