12 Dec 2025

$AVGO Q4 and FY'25 Earnings Report from Moneyvize.com.

#AVGO Q4 & FY’25 earnings beat estimates and the market reaction has been wild.

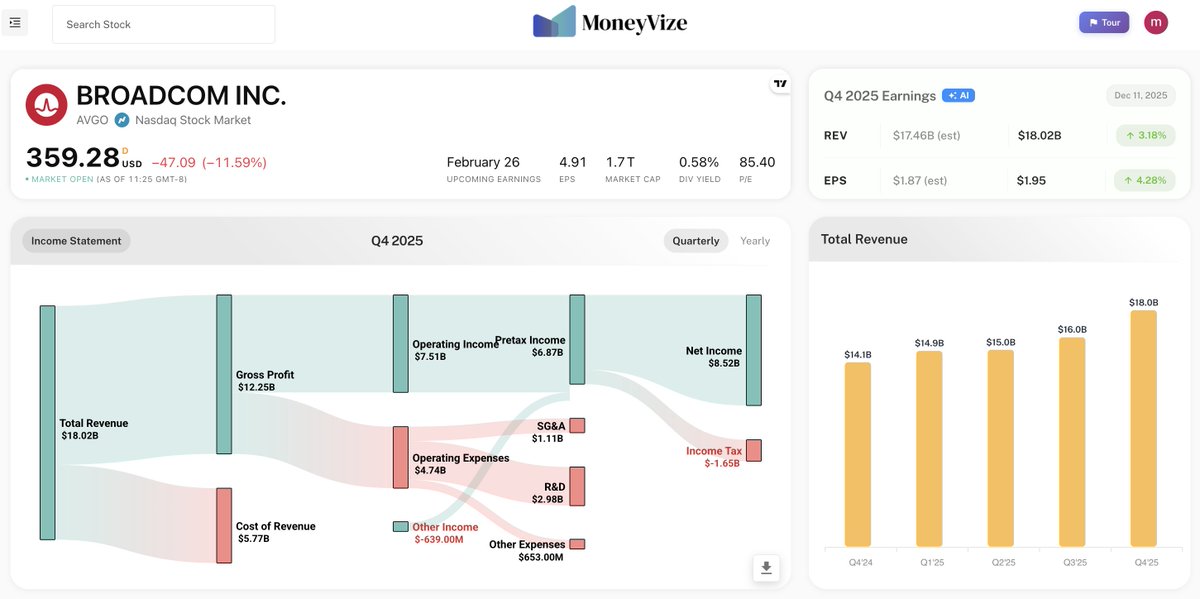

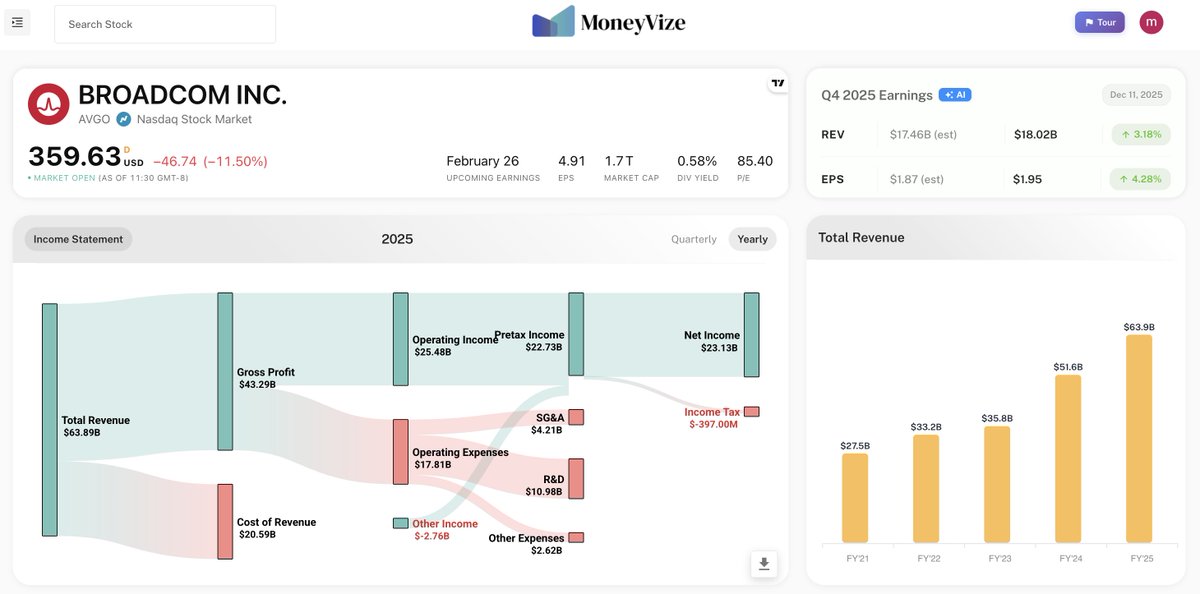

#Broadcom reported Q4 revenue of ~$18.02 B, up ~28% YoY, and non-GAAP EPS of $1.95, both beating Wall Street expectations substantially. The company also raised its quarterly dividend by 10% and delivered record FY 2025 revenue of ~$63.9 B with strong free cash flow and earnings growth. AI semiconductor sales were a standout, with revenue up sharply and Broadcom forecasting those products to double year-over-year next quarter to ~$8.2 B.

The official guidance for Q1 FY’26 calls for ~ $19.1 B in revenue (also above consensus) and adjusted EBITDA around 67% of sales. That paints a picture of continued growth against a backdrop of strong secular demand.

So why did the stock drop more than 11%?

The short answer is expectations vs reality.

Even though #Broadcom beat on the quarter and issued solid near-term guidance, investors seemed disappointed by margin commentary and forward outlook tone. Management highlighted that AI system/server revenues carry lower gross margins, and while overall guidance was strong in absolute terms, it didn’t satisfy the super-charged expectations priced into the shares after a massive run to new highs this year.

There was also some investor consternation that the AI backlog (~$73 B) and customer disclosures weren’t as jaw-dropping as some had hoped, especially given how much the stock had rallied on AI narrative. Analysts saw this as a signal that margins could compress and growth might be a bit slower than the “AI hypergrowth” story implied.

In short, #AVGO delivered strong beats and healthy guidance, but investors punished the stock because the tone around profitability trends and long-term cadence felt more measured than expected. This is a classic case of a beat & guide that was good — just not good enough for a hype-driven market. As always, the numbers look solid, but the stock market looks forward — and that makes a huge difference.

Bull Case:

Broadcom is positioned to benefit from strong AI infrastructure demand, with AI chip revenue expected to double and a multibillion-dollar hyperscaler backlog supporting visibility into 2025. Q1 guidance above consensus indicates continued top-line strength, and recurring software revenue from VMware adds stability. If AI ASIC wins expand and margins stabilize, AVGO could sustain double-digit growth and multiple expansion.

Bear Case:

Rising AI system revenue carries lower margins, creating pressure on gross profitability even as sales grow. Heavy reliance on a small number of hyperscaler customers increases concentration and cyclicality risk. Competition from NVIDIA and AMD in AI silicon and ongoing VMware integration challenges could slow earnings growth, leaving AVGO vulnerable to valuation compression.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#AVGO #Broadcom #Semiconductors #AIBuildOut #CustomAIChips #HyperScalers #AIInfranstructure #AIValuations #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize #MSFT #AMD #NVDA #GOOGL

Not investment advice.

1

2

213

💥OpenAI partners with Broadcom for custom chips - ditches Nvidia dependency in massive supply chain power shift! 🚀

From GPU dependency to silicon independence. AI arms race escalates! 🧠

#OpenAI #Nvidia #CustomAIChips #SupplyChain #Integration #DailyDoseOfAI @genspark_ai👇

1

2

56