A poignant deeply spiritual moment. 🙏🏾. The despiritualised hatefilled reprobate predatory incendiary supremacist cultists will be meeting Karma's distributive justice with Psalm 89-30 enacted

How sad 😔 that the father sees his son for the first time in 25 years 😢

1

15

Last month, the Hub wrapped up a training series with Christian County Public Schools in Kentucky, which included Teaming, Team Lead and Distributive Leadership trainings. We always love working with CCPS!

9

KEY BUSINESS LAW DEVELOPMENTS: JANUARY – JUNE 2026

U.S. Supreme Court • Fifth Circuit • Texas Supreme Court & Business Court

Federal and state courts this term aggressively curbed administrative agency overreach, reinforced strict textualism and four-corners contract enforcement, and clarified remedial boundaries in securities, bankruptcy, ERISA, tax, and intellectual property. Texas’s specialized Business Court has quickly established itself as a sophisticated, predictable forum for complex commercial disputes. Below are the developments with the greatest practical impact for corporate clients.

U.S. SUPREME COURT – SECURITIES, PATENTS, TARIFFS & BANKRUPTCY

• FS Credit Opportunities Corp. v. Saba Capital Master Fund, Ltd., No. 24-345 (U.S. June 11, 2026): Section 47(b) of the Investment Company Act creates no implied private right of action for rescission of contracts allegedly violating the statute. Only the SEC may enforce; private litigants (including activist funds targeting closed-end funds and BDCs) lose this federal weapon. Expect increased state-law fiduciary duty and corporate waste claims. Restores stability for fund governance structures approved via SEC exemptive relief.

• Sripetch v. SEC, No. 25-466 (U.S. June 4, 2026): The SEC need not prove that investors suffered concrete pecuniary loss to obtain disgorgement of a wrongdoer’s unjust gains. Traditional equitable focus is on stripping ill-gotten profits to preserve market integrity. Court left open whether disgorged funds must ultimately be distributed to victims or may remain in the Treasury (potential constitutional challenges if viewed as punitive).

• Hikma Pharmaceuticals USA Inc. v. Amarin Pharma, Inc., No. 24-889 (U.S. June 4, 2026): To state a claim for induced patent infringement under 35 U.S.C. § 271(b) in the generic “skinny label” context, a brand manufacturer must plausibly allege that the generic actively and purposefully encouraged infringing uses—not merely that physicians could interpret marketing statements as instructions. Compliance with federal labeling laws cannot be twisted into evidence of inducement. Major victory for generic competition and lower drug costs.

• Learning Resources, Inc. v. Trump, No. 24-1287 (consol. with No. 25-250) (U.S. Feb. 20, 2026): The International Emergency Economic Powers Act (IEEPA) does not authorize the President to unilaterally impose sweeping global tariffs. Article I, Section 8 reserves the taxing power to Congress; any delegation must be clear and unambiguous. Over $135 billion in collected tariffs invalidated. Exclusive jurisdiction lies in the Court of International Trade. Triggered 80 consumer class actions seeking refunds. Businesses facing these suits should evaluate standing, voluntary payment doctrine, and federal preemption defenses.

• Keathley v. Buddy Ayers Construction, Inc., No. 25-6 (U.S. June 11, 2026): Application of judicial estoppel to bar a debtor’s omitted civil claim requires a flexible totality of the circumstances inquiry. A rigid rule presuming bad faith from a mere hypothetical motive to conceal is inconsistent with equity. Protects honest mistakes, clerical errors, and the bankruptcy estate’s ability to recover assets for creditors rather than extinguishing claims to benefit tortfeasors.

FIFTH CIRCUIT (TEXAS • LOUISIANA • MISSISSIPPI) – ADMINISTRATIVE POWER, TAX & ERISA

• Intuit, Inc. v. FTC, No. 24-60238 (5th Cir. Mar. 20, 2026) (Jones, J.): The FTC’s in-house administrative adjudication of deceptive advertising claims under Section 5 of the FTC Act violates Article III. These claims share a common-law ancestry with fraud, deceit, and unfair competition and target private property/contract rights; they cannot be adjudicated by agency ALJs. The FTC’s “Section 19 workaround” is crippled in the Fifth Circuit. Companies should immediately challenge administrative proceedings and demand Article III adjudication and jury trials.

• Sirius Solutions, L.L.L.P. v. Commissioner, No. 24-60240 (5th Cir. Jan. 16, 2026) (Oldham, J.): Whether a partner qualifies as a “limited partner” for the self-employment tax exemption under IRC § 1402(a)(13) is determined by state-law limited liability status, not the IRS/Tax Court’s functional “passive investor” test. A limited partner who performs services may still exclude the distributive share (only guaranteed payments for services are taxed). Creates a circuit split; refund opportunities exist for Fifth Circuit taxpayers. LLC/LLP members have a strong argument to challenge IRS positions.

• Parrott v. International Bancshares Corp., No. 25-50367 (5th Cir. Feb. 10, 2026): An ERISA plan arbitration clause containing a class/representative action waiver and limiting the arbitrator to individualized relief (barring plan-wide remedies) is unenforceable under the effective vindication doctrine. ERISA § 502(a)(2) claims are inherently representative on behalf of the plan. Plan sponsors must include robust severability language or risk losing arbitration entirely and facing class litigation in federal court. The Fifth Circuit joins eight other circuits on this issue.

TEXAS SUPREME COURT & BUSINESS COURT – CONTRACT PRECISION & COMMERCIAL CERTAINTY

• Equinor Energy LP v. Lindale Pipeline, LLC, 2026 Tex. LEXIS 213 (Tex. Mar. 13, 2026): Texas courts enforce unambiguous contracts strictly within their four corners. Course-of-performance evidence is inadmissible to expand or rewrite clear terms. An attached map or exhibit is part of the contract only if expressly incorporated by reference for that purpose. Courts have “no business rescuing parties from contracts that turned out to be bad deals.” Drafting precision on exclusivity, geography, and scope is now more critical than ever.

• Clifton v. Johnson, No. 23-0671 (Tex. Mar. 13, 2026): A 1951 deed conveying “a 1/128 (1/16 of the usual 1/8 royalty)” successfully rebutted the Van Dyke floating-royalty presumption. Because both the granting clause and future-lease clause stated a single, stand-alone fraction that matched the arithmetical product, the interest was fixed, not floating. Decades of consistent treatment as fixed royalty reinforced the result under the presumed-grant doctrine. Provides a clear arithmetical roadmap for drafters and title examiners.

• S&B Engineers & Constructors, Ltd. v. Scallon Controls, Inc., No. 24-0525 (Tex. Mar. 13, 2026): A settling defendant’s contractual right to proportional indemnity from a non-settling co-defendant survives the underlying settlement. The common-law contribution bar of Beech Aircraft v. Jinkins does not apply to voluntarily negotiated contractual indemnity clauses that satisfy the express negligence doctrine. Settling parties may recover by proving the settlement was reasonable and in good faith and that a specific portion of liability is attributable to the indemnitor’s negligence.

• Enosis Investments, LLC v. Jensen, No. 25-BC03A-0008 (Tex. Bus. Ct. 3d Div. Apr. 23, 2026): In a manager-managed real estate LLC, there is no default fiduciary duty running from the manager or the LLC to non-managing members. An oral joint venture requires a specific agreement to share losses—a non-negotiable element under Texas law. Written LLC agreements with merger clauses supersede prior oral understandings. Corporate separateness is respected; personal liability of a corporate manager’s president requires independent veil-piercing grounds. Protects managers and minority equity holders from implied extra-contractual liability.

• GoSecure, Inc. v. CrowdStrike, Inc., No. 25-BC03A-0012 (Tex. Bus. Ct. 3d Div. Mar. 13, 2026): A non-resident corporation’s large Texas offices, substantial local workforce, and customer transactions do not establish general personal jurisdiction unless the company is “at home” in Texas (incorporated or maintains its principal place of business here). Specific jurisdiction requires the plaintiff’s claims to arise from or relate directly to the defendant’s Texas contacts. Exercising jurisdiction on these facts would constitute judicial overreach and discourage national companies from locating facilities and jobs in Texas.

• DK Trading & Supply, LLC v. Wink to Webster Pipeline LLC, 2026 Tex. Bus. 33 (Tex. Bus. Ct. 11th Div. May 27, 2026): Contractual notice deadlines are strictly enforced as non-negotiable conditions precedent. A party’s failure to deliver timely written notice of a billing dispute, as required by the contract, completely bars claims—even for otherwise valid disputes over deficiency payments or tank allocation. Unambiguous contracts are construed without resort to extrinsic course-of-performance evidence. Track every contractual notice window meticulously; missed deadlines are fatal.

ACTION ITEMS TO CHECK WITH YOUR ATTORNEYS

• Fund Governance & Activist Defense: ICA § 47(b) private rescission claims are foreclosed. Maintain robust defensive measures (control-share bylaws, etc.) but prepare for increased state-law fiduciary duty, corporate waste, and control-share act challenges in Texas and other states.

• Partnership Tax Planning (Fifth Circuit): Limited partnerships now offer clear self-employment tax advantages. Active limited partners can exclude distributive shares from SECA tax. Review entity structures for Texas, Louisiana, and Mississippi operations; consider refunds where statute of limitations permits. Monitor parallel cases in First and Second Circuits.

• ERISA Plan Arbitration: Individual-only remedy and representative-action waiver provisions are unenforceable. Audit all defined contribution and other ERISA plans; add or strengthen severability clauses or risk losing arbitration rights and facing class actions in federal court.

• Contract Drafting & Administration (Texas): Every commercial agreement must spell out exclusivity zones, geographic boundaries, notice procedures, and dispute timelines with absolute clarity. Incorporate exhibits by explicit reference. Missed notice deadlines will bar claims. Update templates and train deal teams immediately.

• FTC Enforcement (Fifth Circuit): Any company facing a deceptive advertising investigation or administrative proceeding in Texas, Louisiana, or Mississippi should promptly assert Article III and Seventh Amendment rights and seek transfer to federal district court.

• Tariff Refund Litigation: More than 80 consumer class actions are pending. Companies that passed through invalidated IEEPA tariff costs should document pricing decisions, review voluntary payment and standing defenses, and coordinate defense strategy across industries.

• Texas Business Court & Litigation Strategy: The specialized court is delivering predictable, contract-centric rulings at high speed. For complex commercial cases meeting jurisdictional thresholds, consider the Business Court for efficiency while adhering to its strict procedural and substantive standards.

This Alert is provided for general informational purposes only and does not constitute legal advice. It does not create an attorney-client relationship. The case summaries reflect publicly available opinions and developments as of June 18, 2026. Outcomes in specific matters depend on unique facts and applicable law.

Please contact your Jones, Davis & Jackson, PC attorney for advice tailored to your company’s situation. Past results do not guarantee future outcomes.

© 2026 Jones, Davis & Jackson, PC

• 15110 Dallas Parkway, Suite 300, Dallas, Texas 75248

• (972) 733-3117

• jonesdavis.com

79

The sick logic of Schiff is that a Somali style grifter NGO to Campaign donation deep state model of income distribution is somehow more efficient than a capitalist, “voluntary to end user & worker” distributive system that’s engineered by the most successful genius in the galaxy

1

24

🚀 Continua a crescere la grande famiglia di Confindustria Abruzzo Medio Adriatico: diamo il benvenuto a Laion S.r.l., nuova associata della nostra organizzazione.

L'azienda è specializzata nella consulenza per l'internazionalizzazione e supporta le imprese italiane nel percorso di accesso ai mercati esteri attraverso servizi di analisi commerciale, ricerca partner, sviluppo di reti distributive e assistenza alle attività di export.

🌐Tra i servizi offerti figurano inoltre missioni commerciali all'estero, attività di matchmaking internazionale, studi di mercato personalizzati e assistenza per la partecipazione a fiere ed eventi internazionali.

Laion S.r.l. entrerà a far parte della Sezione Servizi Innovativi e sarà rappresentata in Confindustria Abruzzo Medio Adriatico dal Dr. Nicola Di Mascio.

#ConfindustriaAbruzzoMedioAdriatico #NuoviAssociati #Internazionalizzazione #Export #ServiziInnovativi #Impresa #Abruzzo

1

10

That said prioritizing housing over the labor market (inflation induced lower real wages) is another wealth transfer from the working class and W2 crowd to aspiring home owners.

This is called resolving a distributive conflict in political economy speak.

10

1,503

binooo retweeted

Jun 11

Currently , Very hard Money making Environment

(Distributive Yellow Zone 🟨)

📌Characteristics of Distributive Yellow zone👇

✅ Breakout Failure

✅ Strong BO is not Followed by a Strong Follow Thru day

✅ Very High Volatility

✅ Stock showing Squat behavior

✅ Market Breadth number Reducing

Here's my Tweet link from 3rd June where I clearly mentioned from here markets will be choppy

x.com/pheonix_trader/status/…

# Market Environment is Supreme

Decisive crack of 20MA - Clear Indication of Upcoming sideways/Choppy market .

Better to Preserve your gains & don't be aggressive.

4

4

64

15,477

The dual philosophy balances Distributive Justice—ensuring fair wages and safe conditions—with Upskilling, making workers the core growth engine rather than treating them as disposable inputs. 2

🌞 OBSERVATION SHAPE REALTY 🌞

6

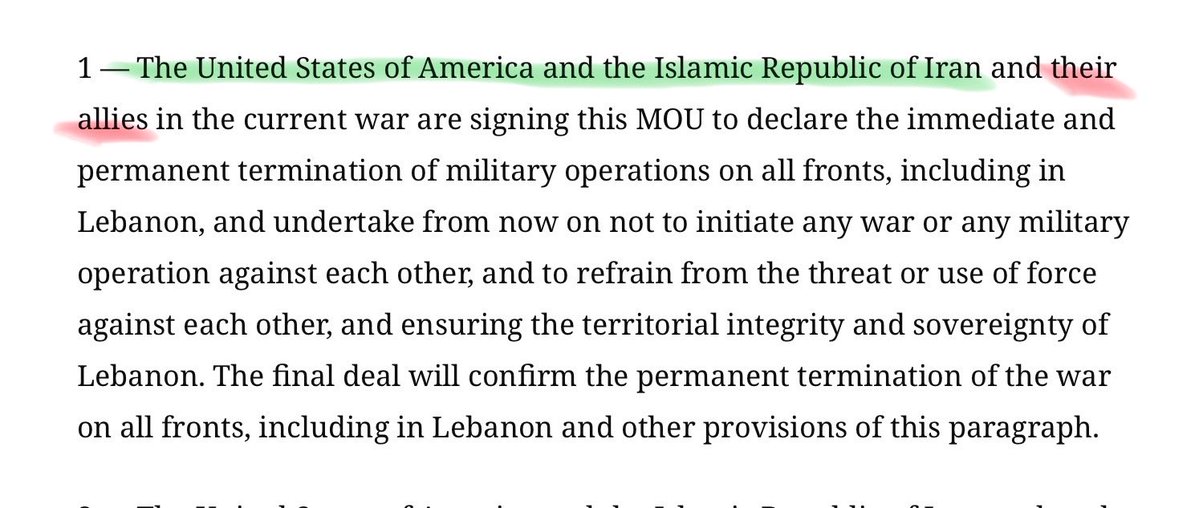

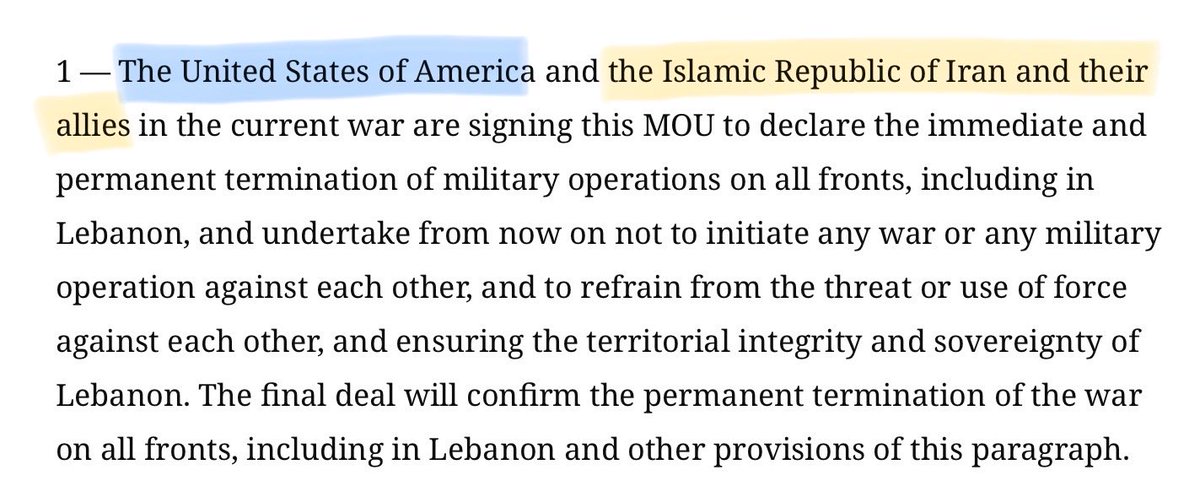

linguistic subtleties and ambiguities in US-Iran MoU: distributive vs collective reading of coordination.

((A and B) and C) --> Israel in

vs

(A and (B and C)) --> Israel out

1

6

1,521

Anthropic must be optimzing the distributive layer of Fable for a relaunch so that people don't connect maybe we were superlarping about safety due to not having enough compute.

45

🟣BULL Supportive / PRESSURE

Nakshatras:

Pushya (8): Stable.

Rohini (4): Euphoric.

Anuradha (17): Disciplined.

Punarvasu (7): Expansive.

U-Phalguni (12): Leading.

U-Ashadha (21): Resilient.

Dhanistha (23): Rapid.

U-Bhadrapada (26): Liquid.

Krittika (3): Aggressive.

Chitra (14): Creative.

Vishakha (16): Decisive.

Shukla Paksha

🔴 BEAR SUPPORTIVE

Nakshatras:

Mula (19): Destructive.

Bharani (2): Restraining.

Ardra (6): Turbulent.

Ashlesha (9): Deceptive.

Jyeshtha (18): Reversing.

Swati (15): Unstable.

Shatabhisha (24): Hidden.

P-Ashadha (20): Trapping.

P-Bhadrapada (25): Confusing.

Hasta (13): Distributive.

P-Phalguni (11): Stagnant. (Amavasya)

Fortnight:

Krishna Paksha

⚠️ REVERSAL (Turning Points)

Pratipada (1): New.

Ashtami (8): Indecisive.

Purnima (15): Peak.

2

8

916

I have studied political history for years and one lesson remains remarkably consistent, budgets are far more than fiscal blueprints. They are ideological manifestos that reveal a government’s priorities, convictions and strategic vision for the nation. My concern lies not in the magnitude of the trillions appropriated but in the widening chasm between official economic optimism and the quotidian realities confronting ordinary Ugandans. A budget unveiled amidst escalating fuel costs, persistent inflationary pressure and a gradual erosion of household purchasing power inevitably invites critical scrutiny regarding its equity, inclusivity and distributive efficacy.

Economic transformation is not a rhetorical enterprise. It cannot be proclaimed into existence through ambitious declarations, statistical projection or carefully crafted speeches. It must manifest in tangible improvements in livelihoods, expanded economic opportunities, enhanced productivity and greater social mobility. Otherwise, we risk celebrating statistical abstractions while normalizing material deprivation.

History has repeatedly demonstrated that sustainable prosperity emerges not from the eloquence of policy pronouncements, but from the ability of governments to cultivate an environment where enterprise flourishes, innovation is rewarded and citizens can meaningfully improve their circumstances.

Ultimately, the success of this budget will not be adjudicated by the grandeur of its presentation, but by its capacity to broaden prosperity, stimulate productive growth and restore public confidence in the economic stewardship of the state.

#UgandaBudget #EconomicPolicy

34

20h

The income bends in the benefit formula are structured to be downwardly distributive, similar to phase-outs for CTC other programs.

12

21h

corresponding to the point in the plane of the form (x,y). i is the point (0,1). i² = -1. so i³ = -1. addition and multiplication are commutative and associative and x is distributive over . sum and product of two complex numbers follows the same for thepoint system

1

1

11

23h

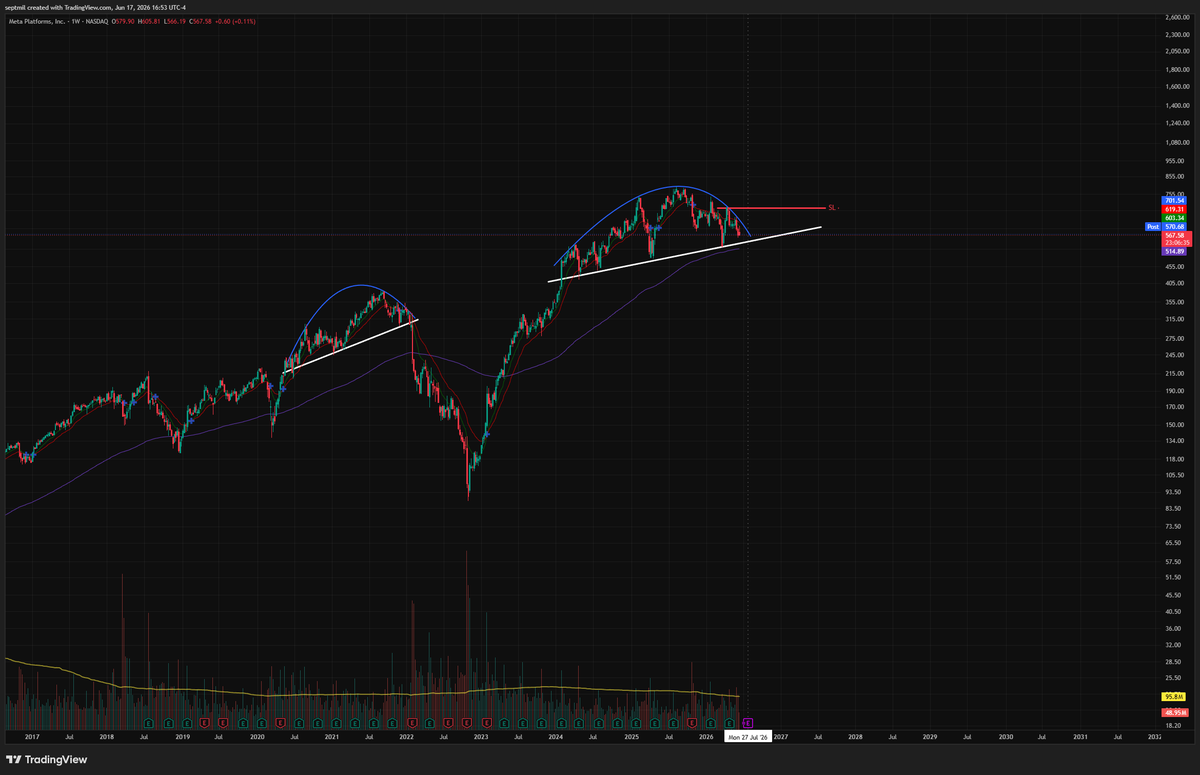

META weekly view, looks distributive but then again i got now idea, would be willing to short the trend line ema breakdown

20

Turlock Weather retweeted

Jun 17

Environmental Threat and the Nation: Earthquake Risk, Distributive Priority, and Expressive Attachment

Hector Galindo-Silva

arxiv.org/abs/2606.18087 [𝚎𝚌𝚘𝚗.𝙶𝙽]

1

1

22