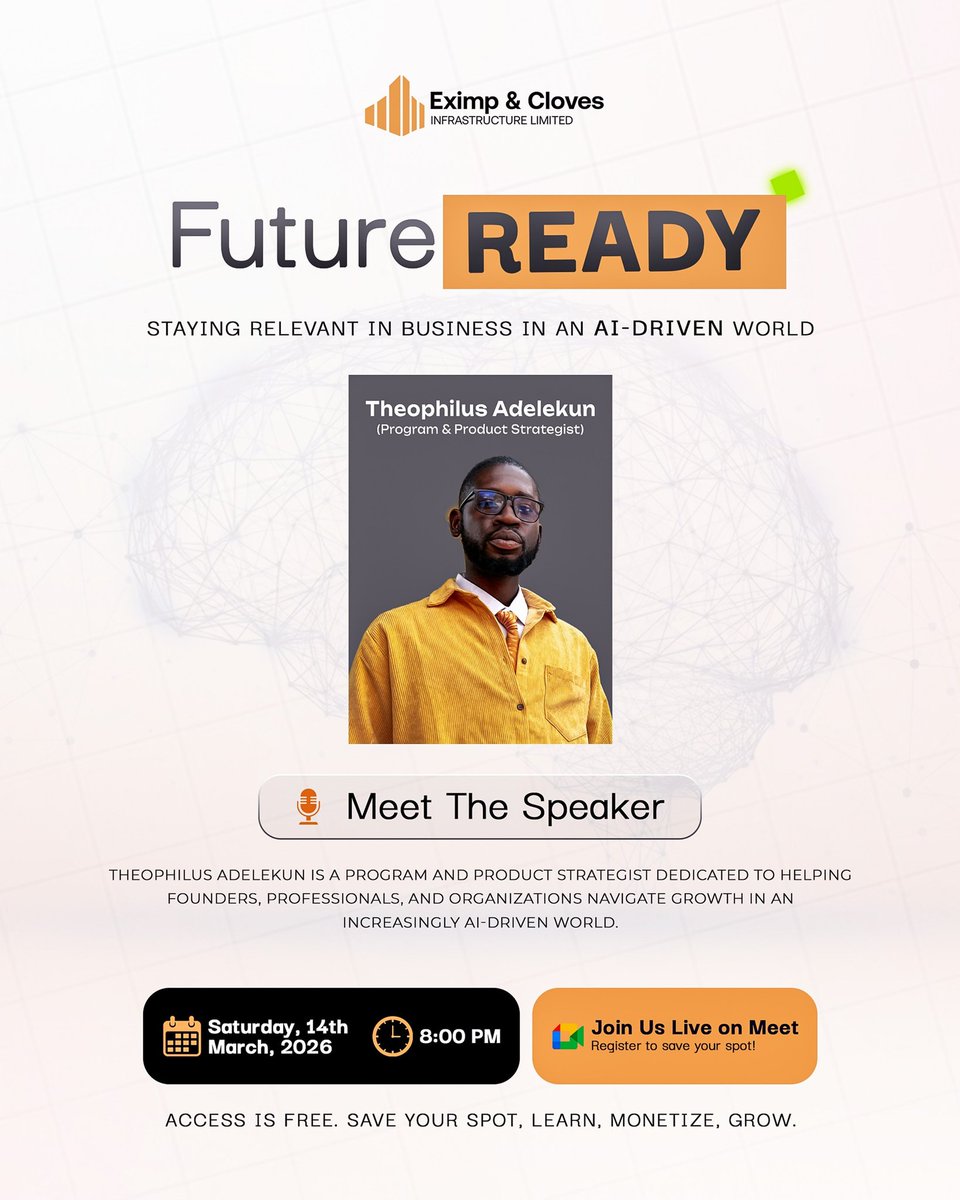

AI is the new standard, are you adapting or falling behind?

Join Eximp & Cloves for a free session with Theophilus Adelekun on building AI systems that attract and convert leads.

March 14 | 8 PM | Google Meet

Register here: forms.gle/V4L3LzSfVCavtD7x5

#FutureReady #AI #BusinessGrowth #EximpAndCloves

1

2

59

If you go to the market at 6:00 AM, you get the farm price, but if you go at 12:00 PM when the noise is loud and the crowd is full, you pay the market price. The goods are the same but the timing is what costs you.

You need to be the person who buys before the noise starts. Once the tractors move in and the development is obvious to everyone, the wholesale price disappears, and you are forced to pay retail.

Baclay Estate is currently in the 6:00 AM phase. Eximp & Cloves is inviting you to enter at the raw price of ₦3.5M before the market heat drives it up.

Buy early. Buy smart. DM us now to secure your plot.

#EximpAndCloves #Baclay #Ogun #realestate #landinvestment

1

4

3

113

THREAD 🧵

1️⃣ Introducing Baclay Estate

A new opportunity to invest early in land 📈

- Located in Agbowa Ikorodu, Ogun State

Developed by Eximp & Cloves Infrastructure Ltd

This is one for smart, forward thinking investors.

1

3

3

109

4 Dec 2025

@sulemaniya_ bhai, it is always a pleasure to hear from you, here are my thoughts:

1. In terms of satellite technology, it is stated that satellite technology has a different use case scenario than cell towers, the cost dynamics are different, and overall transmission of data is cheaper over cell towers as compared to transmitting through satellite, the cost is incremental as per data usage, and using satellite technology can be challenging in densely populated areas. Esim will still require use of cell towers, there are alternatives to cell tower but I feel the technology is unlikely to disrupted in the near future because all the technologies that exist at the moment cannot be mass adopted to replicate coverage of cell towers and be cost effective as cell towers.

2. The Deodar asset acquisition is likely to yield better results, the deal has an escalation clause which is linked to USD prices and inflation hence growth in revenue is likely to above inflation, and ROI is likely to be way above 5%, the increase in tenancy ratio will have a very a positive effect, I think the tenancy ratio is around 1.2x something.

3. Enrgo has good amount of cash, around Rs. 77 bn on consolidated basis, I believe the cash will be used utilized to pay the remaining installments, which are around $20 million per month. I think the Deodar acquisition is a block buster project, and taking on another project before fully paying of Deodar will not be desirable.

4. In terms of FFC and Fatima, both are excellent companies, and it is less known fact that I am a shareholder in both in FFC and Fatima, I was one of the very first on X to recognize the potential in Fatima but you have to take into account that both FFC & Fatima are conglomerates and have a concentrated portfolio, mostly in fertilizer sector, and both have benefitted tremendously from increase in fertilizer prices and stable supply of feedstock gas. Whereas, Engro also a conglomerate but it is more diversified hence positive impact of EFERT is somewhat offset by underperformance of EPCL. EFERT also gets more expensive gas than FFC, they have a clear advantage in that respect.

5. I have a highly concentrated position in EnrgoH for one reason is that I believe Engro is undervalued, it is trading below SOTP, and they can continue to grow earnings effortlessly through tower business, and earnings can be reinvested in setting up new towers, the need for new towers still exist. An undervalued stock even with low growth can still outperform the market in the long run as opposed to an overvalued stock with high growth as per my understanding.

6. In terms of ties to Pakistan, EngroH is heavily invested in Pakistan, as per my understanding except for a Engro Eximp FZE and a business entity in Africa, the majority of the businesses are concentrated in Pakistan, and I am not aware of their plans to invest outside Pakistan yet, there were proposals but I don't see it as a negative, it would be a negative if majority of their business was outside Pakistan, in terms of physical presence of top management in Pakistan, EngroH believes more in empowering individuals with autonomy to take decisions than top management micro-managing every aspect of the business, I did ask the management how much involvement the top management has in day to day operations.

So far, as a shareholder of EngroH, I have satisfactory returns in EngroH. You cannot agree 100% with every decision of the management but I found the management to be open to constructive criticism, and forthcoming about the good and the bad parts of the business.

On a personal note, @sulemaniya_ your insights are always very helpful, I remember you asked very pertinent questions in their last CBS.

2

9

405

26 Oct 2025

Understand Engro Holdings in 500 Words – This Sunday

1️⃣ Transformation at the Core

2025 marked a major shift: Dawood Hercules became Engro Holdings Limited, now owning 100% of Engro Corporation. The move simplifies structure, improves transparency, and turns Engro into a focused investment holding company—designed to grow shareholder value through disciplined capital allocation.

⸻

2️⃣ Headline Numbers (Jan–Jun 2025)

•Consolidated Profit: PKR 73.3bn

•Profit to Engro Shareholders: PKR 35.6bn

•EPS: PKR 29.54 (vs 8.09 LY)

But this jump mainly reflects one-off accounting reversals, not core operations.

Ex-these, underlying PAT ≈ PKR 9bn, showing steady but realistic performance.

⸻

3️⃣ What Really Changed

•Thermal Energy Assets: Sale canceled → impairment of PKR 53.8bn reversed.

•Telecom Tower Business: Completed Deodar Towers acquisition (~10,600 sites).

•Share Base Expanded: 481m → 1.2bn shares post-merger.

These moves make comparisons tricky but position Engro for diversified cashflow growth.

⸻

4️⃣ Segment Snapshots

Fertilizers: Reliable cash cow; softer farmer demand & water scarcity pressurize volumes, but strong operations keep it stable.

Polymers (EPCL): Global margin collapse, high gas cost—tough phase. Focus on cost control until cycle turns.

Telecom Towers: Engro’s newest growth bet. Now ~15k towers post-acquisition. Aim: improve tenancy ratio & efficiency, core to Pakistan’s digital rollout.

Energy: Thar coal plant (EPTL) delivers cheapest baseload power; EPQL under review for sale; SECMC expanding for energy independence.

Foods: Faces policy distortions favoring informal dairy sector, yet long-term upside via FrieslandCampina partnership & formalization.

Terminals: Quietly consistent, gas & chemical terminals ensure stable, regulated cashflows.

Trading (Eximp FZE): Expanding volumes & regional footprint; gateway for future international partnerships.

⸻

5️⃣ Dividend Pause, Not a Problem

No interim dividend this year; cash is being conserved to integrate the tower business. Management’s philosophy: compound value first, distribute later.

⸻

6️⃣ Macro View

Pakistan’s economy shows cautious recovery; lower inflation, better reserves but still wrestles with policy uncertainty & energy costs. Engro’s diversified exposure gives it resilience across cycles.

⸻

7️⃣ The Bigger Picture

Engro aligns its businesses with Pakistan’s core needs:

🌾 Food & fertilizer for productivity

⚙️ Energy for affordability

📶 Telecom infrastructure for digital access

🚢 Terminals & trading for industrial stability

It’s not just diversification..it’s national relevance with financial discipline.

⸻

8️⃣ Takeaway for Investors

Engro Holdings is morphing into a cashflow-compounding platform, shifting from legacy assets to future enablers like towers, Thar coal, and trading. Short-term accounting noise aside, it remains one of Pakistan’s few companies balancing scale, prudence, and purpose.

⸻

In one line:

Understand the business this Sunday, invest with perspective

Engro Holdings is simplifying structure today to compound value tomorrow.

1

3

47

4,119

20 Aug 2025

Opportunity is knocking, but only for a limited time.

Eximp & Cloves is offering a unique chance to secure a strategic investment at our pre-launch prices. This is your first-mover advantage, providing access to prime real estate before the market value adjusts.

Our pre-launch offers end on SEP 30TH, 2025.

- Secure Your Plot: Start your investment journey with an initial deposit of just ₦500,000.

- Unbeatable Value: Enjoy significant discounts with plots available from as low as ₦2,000,000.

- Guaranteed Security: Your investment is fully protected with a Deed of Assignment, Survey, and a C of O (in view).

We invite you to make a smart, strategic move that sets the foundation for your future wealth.

from buyer to builder - a legacy upgrade of distinction

1

5

471

7 Aug 2025

Why is your digital wealth sitting on an invisible foundation?

You’ve built your fortune in crypto, NFTs, and code. You trade the charts, run the bots, and stack capital in wallets and on exchanges. But while your digital assets grow, your life needs a real-world anchor.

Introducing Coinfield Estate in Epe, Lagos—the first real-world asset designed for the digital hustler. This isn't just land; it's a community built by Eximp & Cloves for those who speak your language.

We’re talking about an estate where your neighbor is a tech founder, your community hosts DAO meetups over barbecue, and the estate WiFi actually works. It's the IRL version of your online edge.

But it gets better. This isn't just a vision; it's an opportunity. We're currently in our pre-launch phase, which ends on SEP 30TH, 2025.

Here's why you need to move now:

Massive Discounts: Get up to 63% off prelaunch prices! A 200SQM plot is just ₦2M (down from ₦5.5M).

Accessible Entry: Secure your plot with an initial deposit of just ₦500,000

Flexible Payment: Spread the balance over 6 months or up to 12 months with a small premium.

Secure Titles: Your investment is fully secured with a Deed of Assignment, Survey, and a C of O (in view).

This is how people build legacy wealth. Not by waiting for the market to dip, but by getting in early on an asset that appreciates silently and powerfully.

Don't let this be your "I'll invest later" moment. Later is when the prices go up.

coinfield Estate | by @Eximp_cloves from buyer to builder - a legacy upgrade of distinction

#CoinfieldEstate #EpeLagos #TechAfrica #CryptoAfrica #Web3 #RealEstateNigeria #SmartInvestment #Prelaunch #Epe

1

1

7

175

27 May 2025

Happy Children’s Day from Coinfield Estate

A subsidiary of Eximp & Cloves

At Coinfield, we’re building more than estates, we are shaping spaces where the digital generation can grow, dream and thrive.

Today, we celebrate the future visionaries, builders and innovators.

3

29

12 Mar 2025

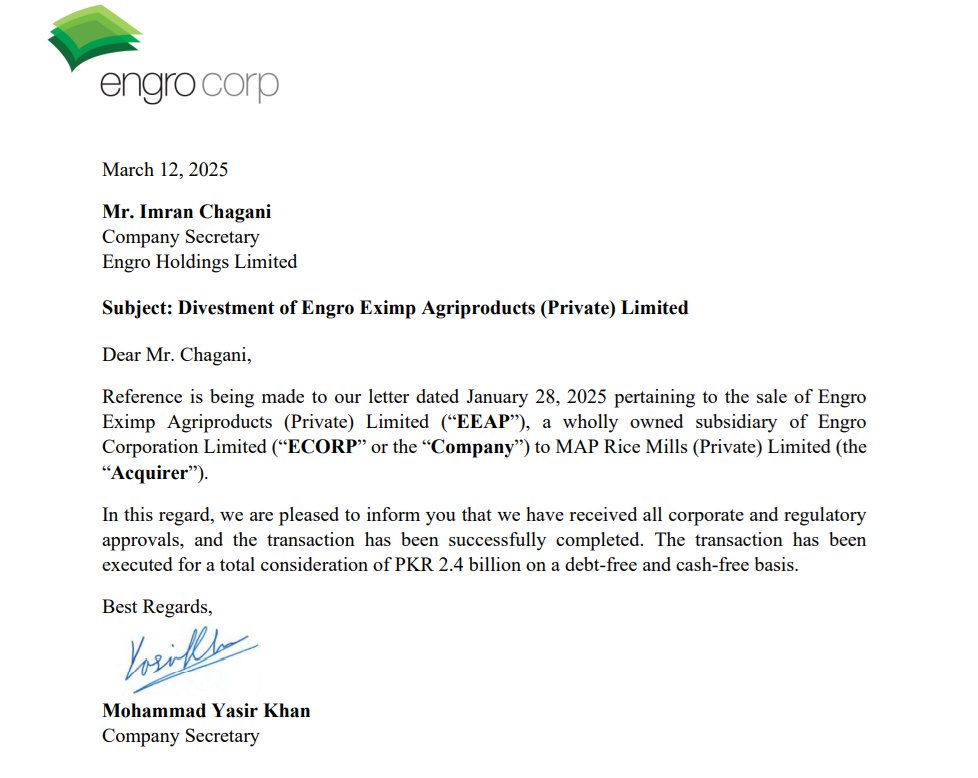

🚨 Engro Corporation Completes EEAP Divestment 🚨

Engro Corporation has successfully completed the sale of Engro Eximp Agriproducts (EEAP) to MAP Rice Mills for PKR 2.4Bn (debt-free & cash-free). All corporate & regulatory approvals secured.

#Engro #MergersAndAcquisitions #Pakistan

1

14

1,010

12 Mar 2025

Engro Holdings Limited has received a notification about the divestment of its subsidiary, Engro Eximp Agriproducts, as announced on March 12, 2025. mettisglobal.news/engro-hold…

2

131

7 Feb 2025

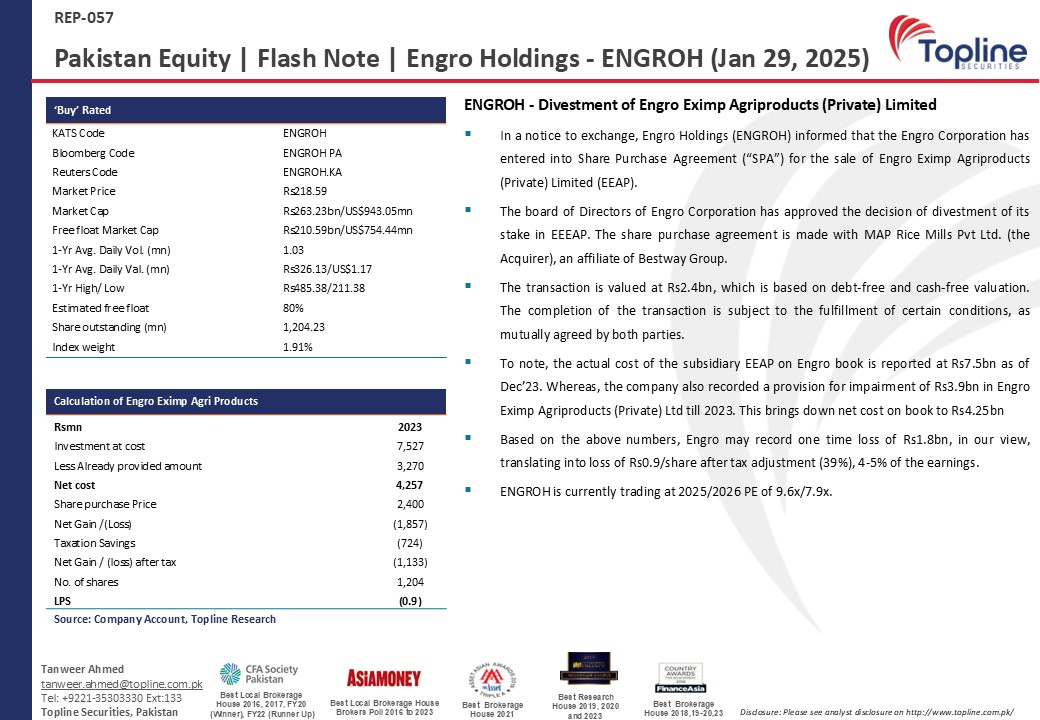

Investors are also expecting special dividend from the proceeds of thermal and ENGRO EXIMP Agriculture assets. Market expects a special dividend of Rs. 25-30 while some investors expect these proceeds can be used to fund the acquisition of VEON reducing debt requirements.

2

3

521

1 Feb 2025

EPS excluding extraordinary items would be around Rs. 14- 18.

But do keep in mind that sale of thermal assets would mean an EPS of Rs. 28.

Sale of rice mill means EPS of around 1.99 (likely to conclude in the CY).

Things can change if EPCL becomes profitable again, and if FCEPL starts paying dividend.

Overvalued, if we exclude the extraordinary events but there is a lot of cash coming in ENGROH this year hence I would hold, and hope for a big dividend.

ENGROH is a conglomerate and trading at a premium, no doubt about that but there is possibility of unlocking shareholder value, and that is why I am still holding ENGROH.

The sale of rice mill, ENRGO Eximp Agriproducts will roughly unlock 8-10 years of earnings through sale.

2

4

332

29 Jan 2025

The Board of Engro Corporation (PSX: ENGRO) has authorized the Company to enter into a Share Purchase Agreement (SPA) for the sale of its wholly owned subsidiary Engro Eximp Agriproducts (Private) Limited.

“Further to the above, an SPA has been executed with MAP Rice Mills (Private) Limited (the Acquirer) for a transaction consideration of PKR 2.4 billion on a debt-free and cash-free basis. The Acquirer is an affiliate of the Bestway Group,” the filing stated.

pakeconet.com.pk/

#Engro #EngroEximp #BestwayGroup #BusinessDeal

2

48

29 Jan 2025

Engro Holdings (ENGROH) - Divestment of Engro Eximp Agriproducts (Private) Limited

(Jan 29, 2025)

6

497

29 Jan 2025

Engro Eximp Agriproducts (EEAP) is a wholly owned subsidiary of Engro Corporation, established with an investment of USD 55 million.

EEAP’s market value isn’t publicly disclosed or readily available.

In 2023, EEAP generated a revenue of USD 9.4 million through exports of

1

2

482

29 Jan 2025

Engro Holdings Limited has received the enclosed letter from Engro Corporation Limited dated January 28, 2025, pertaining to the divestment of its wholly owned subsidiary Engro Eximp Agriproducts (Private) Limited (EEAP)

What can be the possible outcome of this transaction? 🧵

3

2

38

4,092

29 Jan 2025

Engro Corporation (#ECORP) to divest Engro Eximp Agriproducts (EEAP)!

✅ SPA signed with MAP Rice Mills (Bestway Group affiliate)

💰 PKR 2.4Bn deal (debt & cash-free)

📜 Subject to corporate & regulatory approvals

#Engro #Pakistan #MergersAndAcquisitions

1

23

1,585

26 Nov 2024

ஸ்டிக்கர் ஒட்டுறவன்க கிட்ட online-ல இருந்தா ஆச்சரியம்

இவன்க ஏதாவது மத்திய அரசு சைட்லேர்ந்து எடுத்து ஸ்டிக்கர் ஒட்டியிருக்கவே அதிக சான்ஸ் இருக்கு

Department of Commerce site-ல டாஷ்போர்ட்ல பொதுவா ExImp details கிடைக்கும்

1

2

18

4 Nov 2024

The star is still #EFERT.

Engro Vopak Terminal Limited provided stable earnings.

Growth may come from Engro Eximp FZE, their rice exports division is doing well, and should continue to do well, and hopefully due to lower interest rates, we may see better profitability.

2

10

712