Jun 15

🧭 SJS ENTERPRISES — THE BUSINESS NOBODY NOTICES BUT EVERYONE TOUCHES

That logo on a bike tank, the speedometer dial, the chrome bezel on a fridge — fair chance SJS made it. India's only listed pure-play in decorative and functional aesthetics. SJS doesn't sell the car; it sells what makes the car look finished, and earns more per vehicle each year as those parts turn premium.

🏭 HOW THE MONEY GETS MADE

Three engines (Q2 FY26):

- SJS core (badges, decals, dials) — ~59%

- SJS Decoplast, old Exotech — chrome plating — ~23%

- Walter Pack India — in-mould labelling (IML/IMD) — ~17%

FY26 mix: PV ~42%, 2W ~38%, consumer/others ~20%.

The lever that matters is kit value per vehicle. A basic decal pack is a few hundred rupees; add illuminated logos, optical glass, IML dashboards and displays and content per PV moves from ~₹2,400–3,000 toward ~₹7,000–12,000. Content-led, not volume-led.

🔎 GOVERNANCE FIRST — THE PROMOTER QUESTION EVERYONE GETS WRONG

Looks alarming until you check the mechanism. Promoter holding is just ~21.56%, plus a huge "promoter sells stake" event in 2023. Two red flags.

The mechanism: SJS was incubated by a Singapore PE holder, Evergraph — financial capital with an exit clock, not an operating family. In Aug 2023 it sold ~29.5% for ~₹550 cr, fell to 4.63%, then offloaded the rest and reclassified from promoter to public in late 2024. It owns zero today. The selling was never the operator cashing out — it was a sponsor finishing a textbook exit. Left in the promoter slot: K A Joseph, co-founder and MD, three decades in this craft, with Group CEO Sanjay Thapar since 2015. The operator never left. The financier did.

What I like: clean FY26 audit by S.R. Batliboi (EY); growth via arm's-length buys — Exotech, then 90.1% of Walter Pack India (₹239 cr) — no promoter assets injected at fancy valuations. After my EFC scar, that's the first box I tick. Net cash ~₹244 cr, ICRA outlook lifted to Positive on AA-, ₹3.50 dividend.

Watching: a ~0.91% Joseph pledge to Bajaj Finance (monitored), and a low promoter block where alignment leans on incentives, not control.

📊 FY26 SCOREBOARD (consolidated)

- Revenue ₹955 cr ( ~24%), PAT ₹171.8 cr

- Q4: revenue ₹260 cr ( 30%), PAT ₹48.5 cr ( 45%), EBITDA margin ~29%

- ROE 19.5%, ROCE 35.5%

- Exports ₹91 cr ( 60%) — a record

- 26th straight quarter beating the auto industry; auto business 41% vs industry ~18%

🚀 NEXT LEG OF GROWTH

1. Premiumisation / kit value — the structural one.

2. Displays — a 5-year deal with BOE Varitronix for optical bonding and assembly of 4W displays in India; localisation prize ~₹4,000 cr.

3. Exports — record FY26, now on the ground in Turkey, Brazil, South Korea and Germany.

4. M&A — net cash and a team that hunts bite-size deals.

🎯 MANAGEMENT GUIDANCE

- FY27: grow 1.5x–2x the industry, with 85% of FY27 revenue already booked.

- EBITDA margin ~27%.

- Exports 14–15% of revenue by FY28 (from ~10%).

- Capex ₹220–230 cr, three projects done in FY27 — Bangalore expansion, a ₹100 cr Pune greenfield doubling chrome capacity, a Hosur unit.

⚠️ WHAT WOULD MAKE ME WRONG

- Valuation. Stock has roughly doubled in a year, high-30s trailing earnings. A great business can still be a poor entry.

- Displays: new, capital-hungry, leaning on BOE — unproven at scale.

- Key-man risk: Joseph and Thapar.

- Working-capital swings and auto-cyclicality.

One-line take: a clean, cash-generative compounder with a real premiumisation runway, where the gap between thesis and entry is mostly the price. The governance scare is a misread of a PE exit. The valuation isn't.

DYOR. My own analysis for discussion, not investment advice. Not SEBI-registered.

— The Antifragile Notebook | @ARNABKANTIDHAR1

#SJSEnterprises #StockMarketIndia #CorporateGovernance #AutoAncillaries #EquityResearch

3

175

Jun 9

The breach didn't start yesterday.

Most organizations discover threats weeks or months after the damage is already done. By then, you're not responding to an attack. you're recovering from one.

The difference between a close call and a crisis? Speed.

SOC AI shifts security from reactive to real-time, so your team acts before impact, not after.

Here's what that looks like in practice → exotech.com.sa/blog/when-sec…

#CyberSecurity #SOC_AI #RealTimeSecurity #ThreatResponse #BreachDetection #AIinCybersecurity #SecurityOperations #InfoSec #CyberRisk #Exotech

13

ExoTech - Dijiang [ Heavy Hauler ]

➡️ steamcommunity.com/sharedfil…

This ship is developed by ExoTech Heavy Machinery division [EtHM]. Ship made for interstellar cargo hauling and trading operations.

#SpaceEngineers #SteamWorkshop #NeedToCreate

25

1,214

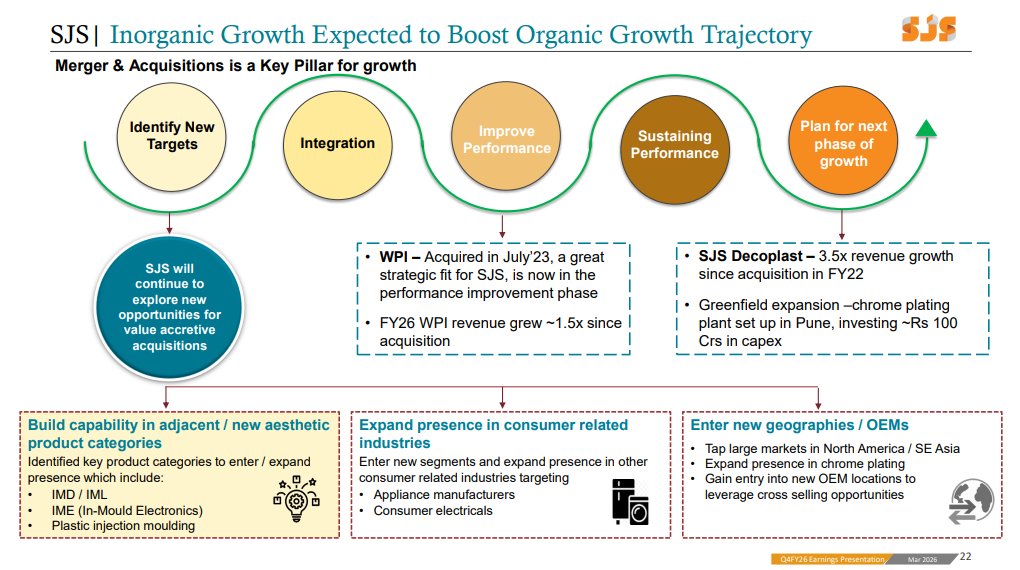

Why The Next Acquisition Could Matter More Than Earnings

Another point that stood out was management's commentary on acquisitions. With more than ₹240 crore of cash and negligible debt, the company is actively evaluating opportunities across India, North America and Southeast Asia.

What makes this interesting is that SJS has historically used acquisitions to add capabilities rather than merely add revenue. Walter Pack brought premium interior technologies. Exotech expanded the company's presence in chrome plating and painted parts. The next acquisition could potentially strengthen exports, add new technologies or deepen customer relationships.

Looking ahead, the bigger question may not be whether SJS can grow faster than the automotive industry. It has already demonstrated that repeatedly. The more interesting question is whether the company can successfully evolve from an automotive aesthetics supplier into a broader automotive technology platform. If the display business scales, exports continue to grow and another strategic acquisition is added to the mix, the SJS that investors see in FY28 could look very different from the SJS they know today.

2

290

I don't love mirage/ionia/stargazer but I understand what it adds to the game in terms of variety. Psionic/exotech does not actually add variety, it just adds a team planner check start of every game to see if you are allowed to play the units or not

16

988

May 9

I just realised it's the same set design team printing Inkshadow/Exotech/Psyonic every 3 sets hoping this time somehow it works out. Let us choose the items they give and balance them properly or stop printing the trait. I swear these traits singlehandedly make the set garbage

12

266

26,471

May 6

The SJS Enterprises M&A playbook is one of the cleanest case studies in mid-cap India 🧵

FY21: ₹250 Cr 2W decal & sticker company.

FY26: ₹955 Cr revenue, ₹172 Cr PAT, ~28.3% EBITDA margins, debt free, 24 quarters of industry outperformance.

What changed? Two acquisitions, one mental model 👇

Mental model: buy adjacent tech → cross-sell into customers you already own and leverage the premiumization trend post Covid

Exotech now SJS Decoplast (FY22) → 3.5x revenue since acquisition. Brought chrome plating. SJS walked it into PV OEMs they already supplied decals to.

WPI (Jul'23) → 1.5x revenue since acquisition. Brought IMD/IML/IME — premium in-mould decoration. Same customers, richer kit.

New-gen products in mix: ~16% (FY22) → ~23% (FY26).

Q4FY26: ₹260 Cr revenue ( 30% YoY). Stock 99% in 1 yr.

The lesson: don't buy revenue. Buy capabilities you can sell back into a customer book you already own.

Educational only. Not investment advice.

1

5

13

1,367

Apr 19

Set 8 A.D.M.I.N.

Set 17 Arbiter

Set 14 Exotech

Set 17 Psionic

Set 17 Stargazer is also conditional

I'm fine with a few conditional traits a set but there needs to be more traits/units you can play more often (Set 16 Demacia comes to mind).

8

1

309

29,263

EUROPE’S MOLTEN SALT REACTOR PUSH MOVES TOWARD DEPLOYMENT WITH THORIZON COALITION AND SITES

· PIONEER DEMONSTRATOR SITED

Eight parties signed an MoU on April 16 to deploy the Thorizon PIONEER MSR demonstrator at the NRG PALLAS Energy and Health Campus in Petten, Netherlands. Construction is targeted for 2028 with first operations around 2030.

· COMMERCIAL PATHWAY AT BORSSELE

The 100 MWe Thorizon One reactor is planned for Borssele. EPZ, operator of the Netherlands’ only commercial nuclear plant, is evaluating roles as owner, licensee, and operator.

· MSR DESIGN PROFILE

Low-pressure system with liquid fuel, designed to utilize long-lived nuclear waste streams. Also targets 550°C high-temperature heat for industrial applications alongside power generation.

· FRANCO-DUTCH LED SUPPLY CHAIN

Orano on fuel, CEA on materials and chemistry, Hyundai E&C, VDL Groep, and Schelde Exotech on manufacturing. Project is among the EU’s prioritized SMR Industrial Alliance initiatives.

· SCALE AND BACKING

Roadmap investment expected to exceed €1B. Thorizon is a spin-off from NRG PALLAS with backing from Invest-NL since 2022.

Thorizon now has a defined demonstrator site, a commercial follow-on location, and a named industrial stack. The key shift is from concept to early deployment pathway, with 2030 and 2034 as the milestones that matter.

$LEU $CCJ $LTBR

2

7

14

2,119

Mar 28

🪐Psyops: Você ganha itens Psiônicos que podem ser equipados em qualquer aliado. (Meio parecido com Exotech).

🪐Embalos no Espaço: Eles entram em um estado de baladinha, onde cada unidade possui um efeito diferente, sendo uma Característica Vertical

1

16

1,775

Mar 3

Well well! Hey everyone o7 tonight on stream we are going to continue our Modded Pirate Playthrough of #Starsector come join me at twitch.tv/cyn0_silva to discover more about ExoTech, and the secrets of the Domain! 19:00 GMT, as usual. Catch u later o/

3

102

Feb 26

Going live now at twitch.tv/cyn0_silva for more modded pirate #starsector playthrough! Come see the progression through ashes of the domain, and us diving more in to ExoTech! #indiegames

6

65

Feb 10

Gooood morning folks! At 19:00 GMT tonight I will be going live continuing our pirate playthrough of #starsector . Come join at twitch.tv/cyn0_silva and say hello! Continuing exotech questline and more general douchebaggery #indiegames

2

41

WTF. Ja znam levicaku dost (osobne i online) a muzu naprosto zodpovedne prohlasit, ze neexistuje jediny, ktery by mel nejake sympatie k teokratickem (a v mnoha ohledech klerofasistickemu) rezimu v Iranu.

Mozna ze takovy existuji (a nemluvim ted o exotech a nackomunistech ze Stacilo, kteri maji s levici spolecneho asi tolik...no jako rezim v Iranu).

Osobne tipuji, ze mnoho levicaku (tak jako to mam i ja) neciti takovou urgenci se vyjadrovat k Iranu, protoze neni potreba svadet souboj i o zakladni veci (typu, ze smrt civilistu neni dobra nikdy a za zadnych okolnosti). Po offline i online svete nechodi moc lidi, kteri by schvalovali to, (nejen), to co dela rezim v Iranu a kteri by vnimali vyveseni vlajky se sluncem a lvem jako projev automatického 'anti-peršanství'. A ti kteri ano, tak vetsinou maji i dalsi nazory, ktere vas donuti se jakekoli diskusi vyhnout.

Greta ma prave venovat jakym tematum chce (tak jako kazdy). Videt za nevyjadrovanim se afiliaci na rezim v Iranu, je bizarni.

7

191

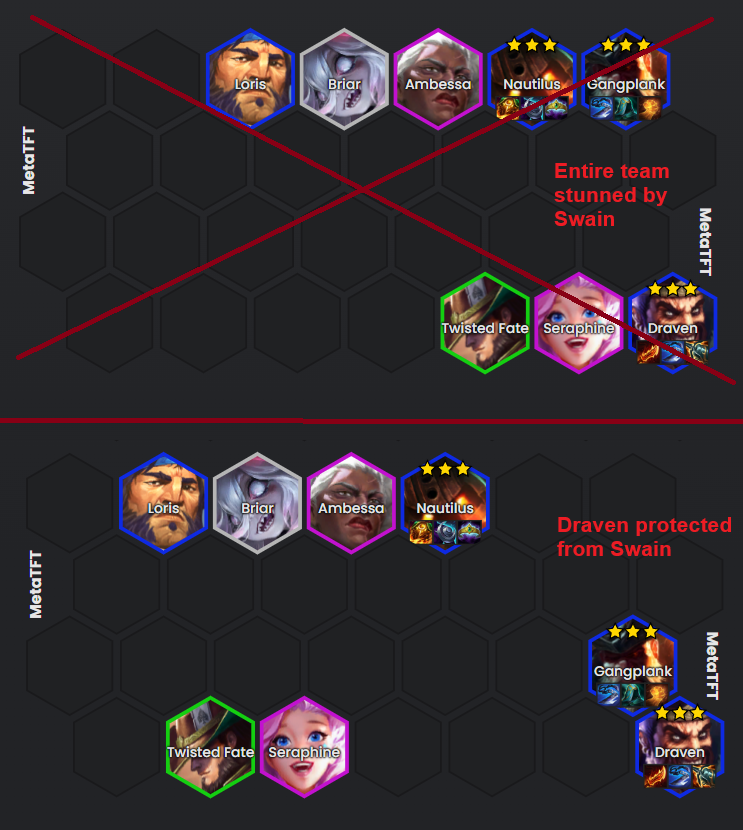

Swain Positioning

Swain is the 4 cost AoE CC unit of this set (successor to Mech Jarvan, Exotech Sej, Black Rose Elise, Arcana TK, etc.), and easily one of the most important units affected by positioning.

He can summon his eye (center of the stun) within 2 hexes and targets largest clump in a 3 hex radius.

I tend to default my Swain in the middle as he can reach both corners against unaware opponents; meanwhile, aware opponents can avoid Swain stun regardless of where I place him.

Against Swain, make sure your ranged carry is not in the largest clump. Placing ranged units next to each other is very important early game for focus fire. Late game, the other backliners who deal an insignificant amount of damage and mostly just provide synergies should be moved away.

11

20

825

78,077

Void and bilge are dominant yes, but you can succeed with SO many other lines.

Annie, Diana, Ionia, Mel, Ashe/Tryn are all very viable.

When you compare it to other metas, this is the best in terms of diversity in awhile.

It doesn't compare to GP, Syndra, Faerie, exotech etc

1

19

1,016

15 Dec 2025

Set16 TFT tip: Barknuckles works like set14 exotech chassis item. If you want to min max it put it 3 seconds before fight start! (For reference to chassis look on @PasDeBolTFT tweet from set 14)

2

11

426

58,945