Now parang gusto ko umorder ng #FinancialStatements netong #TropicalHut at #MercuryDrug from SECExpress.PH lol. I so remember how someone in discord sais Mercury wont ever list in the PSE coz hindi nila kailangan : i.e. the business is THAT profitable

The Pinoy love for silog is unmatched. 🤝

Samahan mo pa ng Daing na Bangus? Take my money🙋♀️💸

31

Why Clean Financials Matter Before a Business Sale

For full episode : youtu.be/Csq3v8ZqAH0 #businesssales #exitplanning #financialstatements

Perhaps it's time we order their ( ** THE ** AreNeOw ) #AUDITED #financialStatements from SecExpress.PH and publicize them !

( naku naku #elitePH #elitesPH a lot of whom overlap w/ #Ateneo would be even more subject of the seething anger of d "na-a api" #massesPH )

Jun 11

I have had my own misgivings about Ateneo conduct not simply on this matter. Mediocrity reigns supreme among senior officials in the different campuses.

58

a few trading days na lang before $MM #TenderOffer supposedly ends, still suspended. #AnnualReport #QuarterlyReport #AUDITED #FinancialStatements #NowhereToBeSeen. May18 "wiLL bE abLe to fiLe nO LatEr tHan tJe PeriOd peRmiTted bY d SRC ruLes" #AnongPetsaNa ?! @SEC_Philippines..

Self dealing shouldn’t get the benefit of the doubt.

Is this the best use of cash for DD investors?

1

119

Jun 8

Businesses must declare a Balance Sheet along with their tax return, showing the company's assets, liabilities, and equity as of the end of the tax year.

#BalanceSheet #TaxReturn #BusinessTax #IncomeTaxReturn #FBRPakistan #TaxFiling #FinancialStatements #TaxationPk #FBR

1

1

25

Jun 7

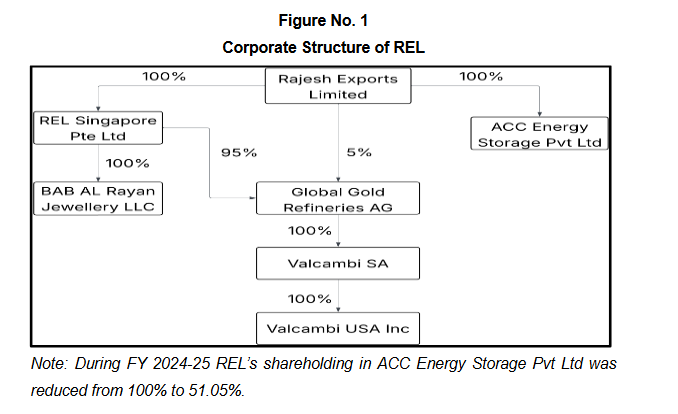

Rajesh Exports: How an alleged ₹15.15 lakh crore accounting scandal was built, missed, and exposed

This is not just a fraud story.

This is a lesson in revenue, cash flow, auditors, banks, institutional investors, board failure and corporate governance.

Let us understand it in simple sequence.

1. The big growth story started with Valcambi

In 2015, Rajesh Exports acquired Valcambi SA in Switzerland.

Valcambi is a precious metal refiner.

A precious metal refiner means a company that takes raw or semi-finished gold, removes impurities, improves purity, and converts it into refined gold bars or other acceptable forms.

Example:

A customer gives gold to Valcambi.

Valcambi refines it.

Valcambi earns a processing fee.

Valcambi does not necessarily own the gold.

This point is very important.

Because if Valcambi does not own the gold, the full value of gold should not automatically become its revenue.

2. The corporate structure made the story look global

The structure was:

Rajesh Exports India

owned a Singapore subsidiary

which owned Global Gold Refineries AG in Switzerland

which owned Valcambi SA.

This is called a layered corporate structure.

Layered structure means a parent company owns one company, which owns another company, which owns another company.

Such structures are legal.

But they can become difficult to understand for investors, auditors and regulators if transparency is weak.

3. The alleged revenue inflation happened through consolidation

Consolidated financial statements mean the combined financial statements of the parent company and all its subsidiaries.

Rajesh Exports reported huge consolidated revenue.

SEBI alleges that between FY21 and FY25, around ₹15.15 lakh crore of revenue was misrepresented.

Now understand the simple trick alleged by SEBI.

Suppose a customer gives ₹1,000 crore worth of gold to Valcambi for refining.

Valcambi earns only ₹5 crore as refining charges.

Correct accounting logic:

Revenue should be ₹5 crore.

Because Valcambi only provided a service.

But SEBI alleges that the group showed the full ₹1,000 crore value of gold as revenue.

This is the heart of the issue.

A service fee business was allegedly shown like a massive gold trading business.

4. Why this matters

There is a big difference between:

Processing revenue

and

Trading revenue.

Processing revenue means the company earns only a fee for doing work on someone else's material.

Trading revenue means the company buys and sells goods on its own account.

If I polish someone else's gold and charge ₹5,000, my revenue is ₹5,000.

I cannot say my revenue is ₹10 lakh just because the gold was worth ₹10 lakh.

That is the simple explanation of the alleged revenue inflation.

5. Why investors believed the story

Valcambi was real.

Gold was real.

Switzerland was real.

The refinery was real.

The problem was not whether Valcambi existed.

The problem was whether the revenue shown represented real economic revenue of Rajesh Exports.

That is where SEBI found serious issues.

6. The Indian standalone books also had red flags

Standalone financial statements mean the financial statements of Rajesh Exports India alone, excluding subsidiaries.

SEBI found large sales and purchases with Affluence Shares and Stocks.

Sales were around ₹11,486 crore.

Purchases were around ₹11,488 crore.

This means the company showed huge transactions, but sales and purchases were almost matching.

When sales and purchases are almost identical, the question is:

Where is the real profit?

Where is the real business value?

Where is the cash?

Even more serious, the counterparty reportedly denied those transactions.

Counterparty means the other party in a transaction.

If a company says, “I sold goods to X,” then X is the counterparty.

If X says, “We never did this transaction,” then it becomes a major red flag.

7. The receivables exposed the weakness

Trade receivables mean money customers owe to the company for goods or services already sold.

Example:

Company sells goods worth ₹100 crore.

Customer has not paid yet.

That ₹100 crore becomes trade receivable.

Now the key question:

If sales are real, why is money not coming?

A shareholder reportedly noticed that large receivables were sitting for a long time.

This triggered the complaint.

This is the most powerful lesson for investors:

Revenue is not enough.

Cash collection matters.

8. Personal F&O trades allegedly entered corporate books

F&O means Futures and Options.

These are derivative contracts used for trading or hedging.

Derivative means a financial instrument whose value depends on something else, such as gold price, stock price, index value or currency rate.

SEBI alleges that company funds were used for promoter Rajesh Mehta's personal gold derivative and F&O trades.

Promoter means the person or group controlling the company.

If company money is used for personal trading, it becomes a serious governance issue.

Company money belongs to the company and its shareholders.

It is not the promoter's personal wallet.

9. The African gold mine investment also raised questions

The company allegedly moved around ₹1,035 crore claiming investment in African gold mines.

Investment in mines means putting money into mining assets, mining companies, or mining rights.

Such an investment should have documents.

There should be agreements.

Board approvals.

Bank trails.

Ownership proof.

Valuation reports.

Mining licence details.

SEBI reportedly did not find adequate traceable proof.

So the simple question is:

If ₹1,000 crore left the company, where exactly did it go?

10. The adjustment of receivables against payables

Payables mean money the company has to pay to suppliers.

Receivables mean money the company has to receive from customers.

SEBI questioned adjustment of receivables against payables.

Adjustment means reducing one balance against another.

This can be valid only when there is legal right, agreement and proper support.

Otherwise, it can become a method to clean up suspicious balances.

In simple words:

If customers are not paying, the company cannot casually remove receivables from books by adjusting them against payables without strong legal basis.

11. Where auditors failed

Auditors are expected to verify whether financial statements give a true and fair view.

True and fair view means accounts should reasonably reflect the actual financial position of the company.

Basic questions auditors should have asked:

If Valcambi only earns refining fees, why is full gold value shown as revenue?

Why are receivables pending for years?

Why are huge sales and purchases almost matching?

Why are confirmations from parties not available?

Why is bank-level evidence weak?

Why is cash flow not matching revenue?

This is why NFRA scrutiny becomes important.

NFRA means National Financial Reporting Authority.

It is the regulator that examines audit quality and auditor misconduct in India.

12. Where the board failed

The board of directors is responsible for supervision.

Independent directors are supposed to protect shareholders, especially minority shareholders.

Audit committee is supposed to review financial statements, internal controls, related party transactions and audit issues.

If such large red flags existed, the board and audit committee should have asked hard questions much earlier.

Corporate governance is not attending meetings.

Corporate governance is asking uncomfortable questions before regulators arrive.

13. Where banks failed

Banks lend money based on financial strength, business model, cash flow and collateral.

If revenue is huge but cash collection is weak, banks should become alert.

Canara Bank reportedly initiated debt recovery proceedings.

Debt recovery means the bank is trying to recover money lent to the company.

Banks should not depend only on turnover.

They must test whether turnover is supported by cash flow.

14. Where institutional investors failed

LIC reportedly held around 10.8% stake.

LIC is not an ordinary investor.

LIC manages public money and policyholder funds.

The question is not whether LIC created the fraud.

The question is whether LIC performed enough due diligence.

Due diligence means detailed checking before and after investment.

For a company like Rajesh Exports, due diligence should include:

Revenue quality

Cash flow quality

Receivables ageing

Auditor observations

Subsidiary financials

Promoter conduct

Related party transactions

Debt position

Governance quality

When public money is invested, the standard of questioning must be much higher.

15. How SEBI finally acted

SEBI means Securities and Exchange Board of India.

It regulates India's securities market and protects investors.

SEBI issued an interim order in June 2026.

Interim order means a temporary regulatory order passed before final conclusion, usually to protect market integrity while investigation continues.

SEBI barred promoter Rajesh Mehta from accessing the securities market.

Barred from securities market means restriction from buying, selling or dealing in listed securities.

The investigation is still ongoing, and final findings will decide the next legal consequences.

16. The biggest lesson

This case teaches one simple thing:

Do not worship revenue.

Revenue can be inflated.

Profits can be adjusted.

Subsidiaries can confuse investors.

Audited accounts can still miss red flags.

Big investors can also make mistakes.

But cash flow tells the truth.

If a company reports huge sales but cash does not come, investors must stop and ask:

Where is the money?

That one question can expose what glossy annual reports try to hide.

The Rajesh Exports case is not just about one company.

It is a warning to promoters, auditors, boards, banks, institutional investors and retail shareholders.

Numbers are not enough.

Substance matters.

Cash matters.

Governance matters.

sebi.gov.in/enforcement/orde…

#SEBI #RajeshExports #CorporateGovernance #AccountingFraud #Audit #Investing #LIC #FinancialStatements #RiskManagement #StockMarket

2

3

4

1,609

tanggala ang kapal lakas ng apog magpa #TenderOffer wala pa rin pala #AUDITED #FinancialStatements for /&/or d latest #AR #AnnualReport and #QR #QuarterlyReport?? $MM { $DD $DDMPR }

indeed, maybe In the $MM #annualReport already, w/c i haven't been to, yet.

1

4

1,827

May 28

Government Ministries, Departments and Agencies (MDAs) are recording significant progress in the implementation of the International Public Sector Accounting Standards (IPSAS), a key pillar of Zimbabwe’s Public Financial Management Reform Agenda launched in 2018.

@Zimtreasury has recorded a commendable improvement in the submission of Financial Statements, with the 2025 submission rate rising to 91 percent from 66 percent recorded in the prior year. The milestone reflects the growing commitment by the 280 reporting entities towards enhanced compliance, transparency, and accountability in public sector financial reporting.

Officially opening the 2025 Financial Statements review session on behalf of the Accountant General, Deputy Accountant General responsible for Aid Accounting, Funds and Parastatals, Mr Shumbaimwe, urged reviewers to assess the extent to which entities have addressed prior-year findings and identify outstanding compliance gaps requiring corrective action before final consolidation.

The improved quality, clarity, and completeness of the 2025 Financial Statements continue to strengthen Zimbabwe’s path towards full IPSAS compliance and internationally aligned public financial management systems.

Zimbabwe remains committed to a transformative agenda aimed at building modern, credible, and transparent public financial management systems in support of the attainment of Vision 2030.

#IPSAS #Transparency #FinancialStatements #Accountability

1

8

840

May 16

RAMP RISE Accelerator Maverick Program Week 5 | Session by CA Ujjawal Modi on 16 May focused on understanding financial statements, interpreting business numbers and making smarter financial decisions for startups #RAMP #StartupIndia #FinanceForStartups #FinancialStatements

3

22

May 12

The one clan has been running the Tangentyere Council for over 20 years. This rorting is happening everywhere across the Nation.

There has been no Audit of the Aboriginal Billions for decades. Some organisations are well run but too many just dont even deliver end of year financialstatements, and yet still get Funding the following year. #Aboriginal #Audit #Fraud

May 12

As further evidence of dire town camp living conditions is published today, and demands grow for greater accountability on funding arrangements, The Australian can reveal the Tangentyere Council Aboriginal Corporation spent $24m on staff costs, its 2025 financial statement shows, while the Alice Springs Town Council, which services about 11,000 households, outlaid $22m in the same period. Both have a similar number of employees. Read the latest: bit.ly/48Qiaxv

4

46

May 9

الفرصة الأخيرة للاستفادة من الخصم

اليوم تبدأ دورة إعداد القوائم 🔥وبخصم P 🔥

يُقدمها المدرب:

🎓 خالد صيرفي، CMA | CertIFR | CIA

استشاري ومحاسبي | بخبرة تتجاوز 10 سنوات في العمل الاستشاري والمحاسبي في مختلف القطاعات التجارية والخدمية، بالإضافة إلى خبرة في تقديم الدورات التدريبية الاحترافية .

✨ الدورة مشمولة شهادة حضور ✨

⚠ لا تفوّت فرصة الجمع بين التطوير المهني والتوفير الكبير

🔴احجز مكانك الآن قبل انتهاء الخصم

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

وسجل الآن عبر الرابط التالي👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة #تحليل_مالي

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements #AccountingTraining

3

404

May 8

إذا كنت تعمل في المحاسبة وتريد الانتقال من التنفيذ إلى الفهم والتحليل…

فهذه فرصتك لتطوير مهاراتك العملية في إعداد القوائم المالية بثقة واحتراف

🔻استغل خصم P حتى بداية الدورة🔻

يُقدمها المدرب:

🎓 خالد صيرفي، CMA | CertIFR | CIA

استشاري ومحاسبي | بخبرة تتجاوز 10 سنوات في العمل الاستشاري والمحاسبي في مختلف القطاعات التجارية والخدمية، بالإضافة إلى خبرة في تقديم الدورات التدريبية الاحترافية .

🎥 الجلسات أونلاين مباشر (ZOOM) تسجيلات

📚 مادة PDF اختبار نهائي

💬 مجموعة واتساب للمتابعة

✨الدورة مشمولة بشهادة حضور ✨

🚀 إذا أردت أن تتحول من منفذ إلى محلل… هذه هي الخطوة التي تؤخرها

🔴احجز مكانك الآن قبل انتهاء خصم P

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

وسجل الآن عبر الرابط التالي👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة #تحليل_مالي

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements #AccountingTraining

2

446

May 7

إعداد القوائم المالية ليس مجرد معرفة نظرية…

بل مهارة عملية تصنع فارقك المهني

في هذا المقطع من الجلسة الافتتاحية، يوضح الأستاذ خالد الصيرفي كيف سيكتسب المشتركون فهمًا عمليًا حقيقيًا لإعداد القوائم المالية وتحليلها خطوة بخطوة

🎯 تدريب تطبيقي مباشر، إعداد عملي، تحليل مالي، فهم أعمق للأرقام

💡 لأن الفهم الحقيقي يبدأ بالتطبيق

اكتشف تفاصيل الرحلة التدريبية

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

🔴احجز مكانك الآن قبل انتهاء خصم P

وسجل الآن عبر الرابط التالي👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة #تحليل_مالي

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements #AccountingTraining

3

13

1,480

May 5

🔻خصم P 🔻

فرصة حقيقية للاستثمار في مهارة قد تغيّر مستواك المهني بالكامل

✨ دورة إعداد القوائم المالية✨

يُقدمها المدرب:

🎓 خالد صيرفي، CMA | CertIFR | CIA

استشاري ومحاسبي | بخبرة تتجاوز 10 سنوات في العمل الاستشاري والمحاسبي في مختلف القطاعات التجارية والخدمية، بالإضافة إلى خبرة في تقديم الدورات التدريبية الاحترافية .

ستتعلّم عمليًا:

✔ إعداد القوائم المالية

✔ تحليل الربح والخسارة

✔ فهم التدفقات النقدية

✔ إدارة إقفالات نهاية العام

✔ التعامل المهني مع المدقق الخارجي

🔴احجز مكانك الآن قبل انتهاء الخصم

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

وسجل الآن عبر الرابط التالي👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة #تحليل_مالي

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements #AccountingTraining

5

428

May 3

💡الفرق الحقيقي في السوق

ليس في عدد سنوات الخبرة… بل في عمق الفهم

📌 هذا التدريب… ليس للجميع

فشرط أساسي وجود معرفة بالمحاسبة وموجه:

✔ للمحاسب الذي يعمل… ويريد فهمًا أعمق

✔ لمن يشعر أن خبرته لا تعكس ثقته

✔ لمن يريد الانتقال من التنفيذ إلى التحليل

✔ لمن يسعى ليكون له "رأي مالي"

❌ ليس لمن يبدأ من الصفر

❌ وليس لمن يبحث عن معلومات سطحية

✨ الورشة مشمولة بشهادة حضور ✨

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

احجز مكانك الآن 👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة_مالية

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبين AccountingTraining#

#FinancialStatements #Accounting

5

345

May 1

المهارة التي تصنع فارقك المهني في سوق العمل… ليست مجرد تسجيل القيود

بل قدرتك على فهم القوائم المالية وتحليلها

📊 لأن القيمة الحقيقية للمحاسب تظهر عندما يستطيع:

✔ تحديد الربح والخسارة بدقة

✔ تحليل التدفقات النقدية

✔ فهم حقوق الملكية

✔ إدارة إقفالات نهاية العام

✔ التعامل مع المدقق الخارجي بثقة

💡 الفرق ليس في المعرفة… بل في القدرة على التحليل

والتدريب العملي هو الطريق الأقصر لبناء هذه المهارة

✨ الورشة مشمولة بشهادة حضور ✨

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

احجز مكانك الآن 👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة_مالية

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسب AccountingTraining#

#FinancialStatements #Accounting

1

5

326

We are pleased to announce the publication of our Unaudited Financial Statements for The Period Ended March 31, 2026.

Kindly click the link below to view the full statements:

zenithbank.com.gh/media/o2pf…

#ZenithBankGhana #FinancialStatements #InYourBestInterest

1

1

7

293

Apr 29

دورة إعداد القوائم المالية

يُقدمها المدرب:

🎓 خالد صيرفي، CMA | CertIFR | CIA

استشاري ومحاسبي | بخبرة تتجاوز 10 سنوات في العمل الاستشاري والمحاسبي في مختلف القطاعات التجارية والخدمية، بالإضافة إلى خبرة في تقديم الدورات التدريبية الاحترافية .

الدورة موجهة لـ:

✔ المحاسبين العاملين ومهتمون برفع مستواهم

✔ من لديه أساسيات في المحاسبة ويريد التطبيق العملي

✔ من يسعى للترقية أو الانتقال لمستوى تحليلي أعلى

✔ من يشعر أنه يعمل… لكنه لا يفهم الصورة كاملة

❌ غير مناسبة لغير المختصين أو المبتدئين تمامًا

احجز مكانك الآن 👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go#

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements

3

303

Apr 28

ليست كل القوائم المالية… تعني فهمًا ماليًا

كثير من المحاسبين يستطيعون إعداد التقارير…

لكن القليل فقط يفهم ماذا تعني هذه الأرقام فعلًا

📊 لأن القوائم المالية ليست جداول

بل "قصة الشركة" بلغة الأرقام

الفارق الحقيقي يظهر عندما تنتقل من:

❌ تنفيذ الأرقام

إلى

✅ فهم ما وراء الأرقام

من خلال تطبيقات عملية واقعية، يمكن بناء هذا الفهم عبر:

✔ ربط العمليات بالتقارير

✔ قراءة الصورة المالية الكاملة

✔ تحليل النتائج وليس فقط عرضها

💡 لأن التطور في المحاسبة… يبدأ من تغيير طريقة التفكير

✨ الورشة مشمولة بشهادة حضور ✨

📅 الموعد: السبت 9 مايو 2026.

- التوقيت: 7:30 مساءً بتوقيت السعودية

احجز مكانك الآن 👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go# #محاسبة

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسب AccountingTraining#

#FinancialStatements #Accounting

6

306

Apr 21

الكثير يعملون في المحاسبة لسنوات…

لكن عند إعداد القوائم المالية أو تحليلها، يظهر التردد.

🎯 دورة إعداد القوائم المالية صُممت لتغلق هذه الفجوة

يُقدمها المدرب:

🎓 خالد صيرفي، CMA | CertIFR | CIA

استشاري ومحاسبي | بخبرة تتجاوز 10 سنوات في العمل الاستشاري والمحاسبي في مختلف القطاعات التجارية والخدمية، بالإضافة إلى خبرة في تقديم الدورات التدريبية الاحترافية .

ستتعلم عمليًا:

✔ إعداد ميزان المراجعة المعدل بعد الإقفالات

✔ تحديد الربح والخسارة بدقة

✔ تحليل التدفقات النقدية وفهم حركة الأموال

✔ إعداد القوائم المالية بطريقة احترافية

✔ إدارة إقفال نهاية السنة بكفاءة

✔ التعامل مع المدقق الخارجي بثقة

💡 الأهم:

ستبني طريقة تفكير تحليلية… وليس مجرد مهارة تنفيذ

🚀 إذا أردت أن تتحول من منفذ إلى محلل…

هذه هي الخطوة التي تؤخرها

احجز مكانك الآن 👇

bit.ly/learninggo-fb

#ليرنينغ_غو #وجهتك_الأولى_للنجاح learning_go#

#خالد_الصيرفي #إعداد_القوائم_المالية Khaled_AlSayrafi# #محاسبة AccountingTraining#

#FinancialStatements

4

521