Jun 11

\#interop26 #東陽テクニカ 出展製品紹介 ✨/

📍ネットワークフロー解析ソリューション #Flowmon を展示‼️

通信ログの可視化・分析にお悩みの方は、ぜひブースでご覧ください👀

toyo.co.jp/ict/products/deta…

📌2026/6/10(水)~12(金) 幕張メッセ ホール4

📌ブース:4H10 (ICTソリューション)

1

70

アイビーシー(3920)は、2026年6月17日(水)にウェビナー「System Answer G3 & Flowmon 活用事例」を開催すると発表しました。

1月に大阪で開催された自社イベントでの、テクノアソシエ社による事例講演のアーカイブ配信です。

死活監視の属人化や、トラブル原因の特定困難といった課題を、同社が「System Answer G3」と「Flowmon」の導入によってどう解決したかを解説。

障害分析に悩むネットワーク担当者向けの無料セミナーです。

257

【IBC_IR】System Answer G3 & Flowmon 活用事例(テクノアソシエ様による事例講演)に関するウェビナーを開催いたします!詳細はリンク先をご覧ください。

system-answer.com/seminar_20…

#IBC

#アイビーシー

#SystemAnswer

#性能監視

#IT障害ゼロ

#中央区

#猫

64

Jun 8

\#interop26 #東陽テクニカ 出展製品紹介 ⑭✨/

📍ネットワークフロー解析ソリューション #Flowmon を展示‼️

通信ログの可視化・分析にお悩みの方は、ぜひブースでご覧ください👀

toyo.co.jp/ict/products/deta…

📌2026/6/10(水)~12(金) 幕張メッセ ホール4

📌ブース:4H10 (ICTソリューション)

1

123

May 31

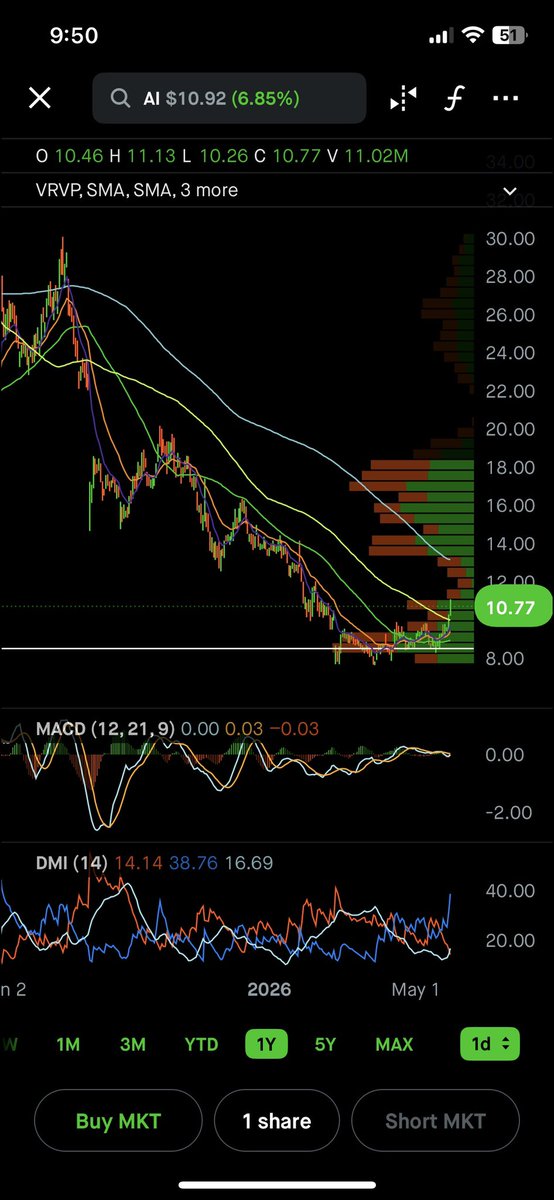

$AI $PRGS

Two artificial intelligence software companies with market capitalizations below $2 billion.

REPOST. BOOKMARK. SUBSCRIBE. KEEP EYES

Both have experienced significant declines.

Both are undergoing restructuring efforts.

Both are trading well below what many bullish investors believe to be their intrinsic value.

Up 9% 16% respectively last week.

Consider sharing, saving, and following for future updates.

$AI

Current Market Cap: ~$1.5B

Today, it trades near multi-year lows despite artificial intelligence emerging as one of the most significant technology themes globally.

Why?

• Revenue growth has slowed.

• Operating losses remain substantial.

• Investor confidence has deteriorated.

• The company has undergone multiple restructuring initiatives.

However, the market may be overlooking several important factors:

✅ $575M cash position.

✅ Founder-led leadership under Thomas Siebel.

✅ Established relationships with Microsoft, AWS, Google Cloud, Baker Hughes, McKinsey, PwC, Booz Allen, and various government agencies.

✅ One of the few publicly traded pure-play enterprise AI companies.

✅ Agentic AI, Generative AI, and predictive analytics solutions already deployed in production environments.

Instead, it focuses on addressing complex and costly enterprise challenges, including:

• Predictive maintenance

• Supply chain optimization

• Defense readiness

• Energy production

• Asset management

• Fraud detection

If enterprise AI spending accelerates over the next 24 months and C3.ai successfully converts more pilot programs into full-scale deployments, the resulting operating leverage could be significant.

However, the stock has already declined substantially from its historical highs.

Should revenue growth reaccelerate and management achieve its non-GAAP profitability objectives, the market may begin assigning a meaningfully higher valuation multiple.

$PRGS (Progress Software)

Current Market Cap: ~$1.3B

Yet it generates consistent earnings, strong cash flow, and serves mission-critical customers.

Q1 FY26 Highlights:

• Revenue: $248M

• ARR: $863M

• Non-GAAP Operating Margin: 41%

• Non-GAAP EPS: $1.60

• Free Cash Flow: ~$99M

Unlike many AI-focused software companies, Progress is already profitable.

Its product portfolio includes:

• OpenEdge

• MOVEit

• Chef

• Sitefinity

• Flowmon

• LoadMaster

• DataDirect

Key strengths include:

✅ Nearly $1B in annual revenue.

✅ Gross margins of approximately 80%.

✅ A strong recurring revenue model.

✅ 99% net retention.

✅ More than 200,000 organizations utilizing its software.

✅ Thousands of partners worldwide.

The company also continues integrating AI capabilities across its portfolio rather than relying on a single product strategy.

The valuation is particularly noteworthy.

Current metrics:

• ~1.4x sales

• ~16x earnings

• ~2.7x EV/revenue

These valuation levels are more commonly associated with mature industrial businesses than software companies generating gross margins above 80%.

If Progress were simply re-rated closer to typical software-sector valuations of 3–5x sales, shareholders could realize meaningful upside without requiring exceptional growth.

$AI

• Significant valuation compression has already occurred.

• The cash balance provides financial flexibility.

• AI adoption continues to accelerate globally.

• Founder-led leadership is once again a focal point.

• Market expectations remain exceptionally low.

$PRGS

• Strong profitability.

• Robust free cash flow generation.

• Stable recurring revenue.

• Attractive valuation.

• Consistent operational execution.

One represents a turnaround opportunity.

One represents a potential long-term compounder.

One requires growth to reaccelerate.

One primarily requires greater market recognition.

$PANW $CRWD $SNOW $NET $NOW $OKTA $OKLO $S $ZS $GOOG $U $VRNS $FTNT $DOCU $SHOP $TWLO

11

12

49

4,524

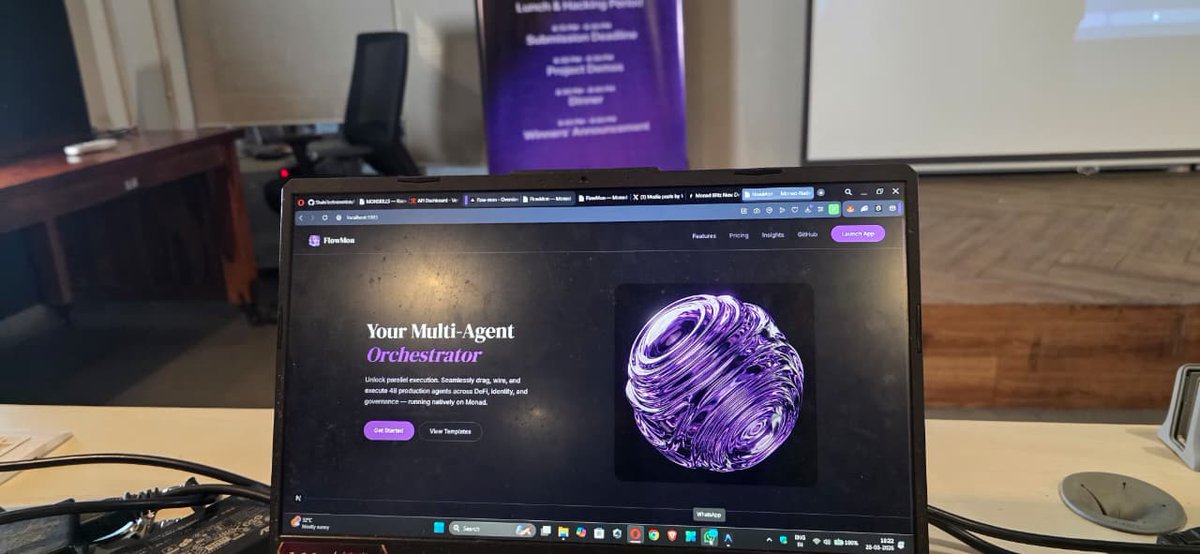

5x done 🎉

400$ 🏆

Built -> FlowMon - visual multi-agent orchestration platform .☠️

Thanks to @monad ❤️🔥 , @geeky_kartikey , @piyushJha__ , @itsNikku876 , @0xshukla

7

36

864

Mar 28

FlowMon is ready.

43 agents. 23 protocols.

n8n but for Web3 AI agents

drag, wire, hit run

your entire DeFi pipeline executes live on Monad

no SDK glue. no boilerplate. no code written.

see you at #monadblitzdelhi

cc: @geeky_kartikey @piyushJha__ @itsNikku876 @monad_xyz @MonadIndia @monad_dev @Monad_APAC

#monadblitz #monadblitzdelhi #monadblitzdelhi3 #monad #web3 #defi #onchain #buildinpublic

Mar 28

Cooking something on Monad

Exploring a new primitive around agent coordination, protocol glue, and parallel execution.

Feels obvious in hindsight, but everyone's still writing bash scripts

Drag → wire → execute → live data. No code written building with the team this time!

Still early

cc: @geeky_kartikey @piyushJha__ @itsNikku876 @monad_xyz @MonadIndia @monad_dev @Monad_APAC

#monadblitz #monadblitzdelhi #monadblitzdelhi3 #monad #web3 #defi #onchain #buildinpublic

1

4

138

Mar 10

🛡️Podobu kybernetických útoků zásadně mění AI. Filip Černý demonstruje, jak řešení Flowmon pomáhá identifikovat anomálie i v komplexních hybridních prostředích a zkrátit dobu reakce.

👉 Program a registrace: itsw.konference.cz/

#ITSecurityWorkshop #Kyberbezpecnost #NIS2

1

2

12

Jan 15

Progress Flowmon 13 is here!

Join our experts Filip Černý and Jan Střítežský for a live webinar where they’ll unveil the latest innovations in Flowmon 13.

👉 prgress.co/3YDDbGk

3

76

25 Nov 2025

From Prague to Brno 🇨🇿

Progress Flowmon Customer Days continued with another customer-only event packed with real use cases, security challenges and honest conversations.

Thank you to everyone who made it such a great day. 🙏🏻

2

77

20 Nov 2025

We’ve just wrapped up Progress Flowmon Customer Day in Prague — an exclusive event for our customers focused on network visibility, cybersecurity and real-world use cases.

🙏🏻Thank you to everyone who joined, shared feedback and made it a great day.

2

79

14 Nov 2025

⚡ Up to 7x faster performance with a redesigned backend engine!

That's what is new in Flowmon 13, and there's more.

👉 Learn more about what’s new: prgress.co/4r0LtF4

#ProgressFlowmon #NetworkVisibility #CyberSecurity

2

79

23 Oct 2025

🛡️ Big news! Flowmon is a 3x Technology Leader in NDR per the 2025 SPARK Matrix™️.

Download the report to know NDR market trends 👉 prgress.co/48IlRGn

#Cybersecurity #NDR #Flowmon #SPARKMatrix

2

99

CVE-2025-10239 In Flowmon versions prior to 12.5.5, a vulnerability has been identified that allows a user with administrator privileges and access to the management interface to ex… cve.org/CVERecord?id=CVE-202…

2

488

23 Sep 2025

Progress Software Flowmon ADS 12.5 simplifies threat detection helpnetsecurity.com/2025/09/…

3

747

2 Jul 2025

AI-powered SecOps starts here: Flowmon detects anomalies, hunts threats and automates response — across on-premises, hybrid & cloud 🚀

Uncover hidden breaches & fortify your cyber resilience 👉 prgress.co/4jtbfwA

#NetSecOps #NDR #CyberSecurity #AI

3

174

27 Jun 2025

Here’s the latest from:

⚪ Progress Kemp→ @KempTech

⚪ Progress Chef→ @chef

⚪ Progress Flowmon→ @FlowmonNet

⚪ Progress Sitefinity→ @Sitefinity

⚪ Progress OpenEdge→@_OpenEdge_

⚪ Progress MOVEit→ @ProgressMOVEit

💡 Follow our product channels to stay updated

1

2

171