May 25

#SME #ForcasStudio #Forcas

Forcas Studios H2 FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️ Management remains optimistic and guided 25-30% revenue growth for FY27

💠Noted a historical practice of conservative guidance (previously communicated 25-35%) to understate and over-deliver

▫️ Multi-brand strategy as the core growth engine:

💠FTX (economy fast fashion, Gen Z focus, price point ₹199-599): Scale driver, targeting ~₹160-170 Cr in FY27; expanded into women’s wear (formal/casual trousers, comfort wear).

💠Tribe (premium bottoms – men & women, ₹599-1,499, avg. ASP ~₹899): Premiumization and margin lever; tested successfully (3.5x growth in FY26 over testing phase); aggressive expansion via distribution, marketplaces, and Quick Commerce.

💠Fitness Exchange (new separate brand – athleisure, activewear, sports-inspired, accessories; semi-premium affordable): Targeting rapidly growing health & fitness segment; 50-50 clothing accessories mix; expected to scale gradually in FY27 with product-market fit testing.

💠 Quick Commerce positioned as the “next large opportunity” and future of fashion retail in India (wide SKU, option-based buying, Gen Z smartphone preference).

💠Already live on Zepto and Myntra M-Now; Flipkart Minutes paperwork closed and expected live shortly.

💠FY26 Quick Comm revenue ~₹7.5 Cr; targeted mix 10-15% in FY27, scaling to 30-40% over the next couple of years.

▫️ Overall focus:

💠Scaling brands, Quick Commerce expansion, strengthening omnichannel distribution, margin improvement

💠 White labeling to be maintained at ~20% (±5%) of revenue for learning and clean margins without inventory risk.

💠Long-term (3-5 years): Digital/online to 50-60% of non-white-label revenue, distribution 30-40%.

💠Asset-light model, existing sourcing/warehousing/marketplace infrastructure, and omnichannel relationships in focus

👉 Current Order Book / Projects and Future Pipeline

▫️ White labeling (B2B) contributed ~20% of FY26 revenue (~₹39-40 Cr) with a order book of ₹178 Mn at year-end.

💠Strategy is to keep it steady (not exceed 20-25%) while leveraging it for design/forecasting insights and relationships with major retailers.

💠 Quick Commerce pipeline: Expansion from current platforms (Zepto ~120 stores, Myntra M-Now) to Flipkart Minutes and others.

💠Requires higher initial inventory for 10-15 min availability but drives faster rotation and superior margins as the channel matures.

💠 Brand pipeline: Tribe scaling in FY27 with men’s/women’s premium bottoms; Fitness Exchange launch and market testing in FY27 (athleisure accessories).

💠Continued hero product development and new launches under FTX (double-digit hero SKUs already driving growth).

💠Offline reach expanding from 8 to 10 states; retail network >18,000 retailers; serviceable pincodes >21,000; warehouse expanded to 60,000 sq. ft. in Kolkata

👉 Other Notable Points

▫️ Margins:

💠Gross margins expected to improve via

(1) Quick Commerce logistics savings

(2) Higher ASP/margin mix from Tribe & Fitness Exchange

(3) Maturing FTX product portfolio with better acceptance and selective price hikes.

💠Digital gross margins currently highest (30-35%), distribution ~22-23%, white labeling 19-21%.

💠EBITDA margins already improved in FY26; further uplift targeted in FY27 through premiumization and operating leverage.

💠Ad & promotion spend ~3-4% (mainly marketplaces/Quick Comm visibility).

▫️ Balance sheet & cash flow:

💠Inventory rose sharply (to ~₹50 Cr) due to Quick Commerce stocking requirements, new brand launches (Tribe/Fitness Exchange), and ensuring availability for impatient Gen Z customers.

💠Cash conversion cycle lengthened but expected to normalize as brands strengthen, inventory turns faster, and higher-margin products scale.

💠Management expects gradual improvement in cash flows over the next couple of years with brand maturity.

▫️ Differentiation & resilience:

💠Purely asset-light (no own stores or factories for FTX; third-party MBOs marketplaces Quick Comm).

💠Omni-channel at economy price points with fast delivery (15 min to 24 hrs).

💠No direct national brand competition in core FTX range.

💠Repeat rates: ~29-30% online, 65-70% offline retailers reorder within 4-6 months.

💠Hypothetical competition from Zudio/Westside in Quick Comm addressed by their retail/franchise model constraints and massive market size (no single winner possible).

▫️Challenges/Bottlenecks:

💠Talent acquisition (hiring experienced people for scaling) and brand-building process (iterative learning curve).

💠No major manufacturing or distribution bottlenecks cited due to asset-light model and existing infrastructure.

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

1

1

11

2,901

2 Dec 2025

3️⃣Forcas Studio Ltd 🔖

💰Market Cap ~ 222 Cr

🔥ROE ~20.6 %

💥ROCE ~21.7 %

🪴OPM ~10%

👉Stock P/E ~19.6

🔮Revenue Guidance ~ 27%

🔸Company has guided FY26 revenue of 190–200 Cr, with 30–40% CAGR over the next 2 years.

#forcasstudio #stockstobuy #StocksToWatch

1

2

462

27 Nov 2025

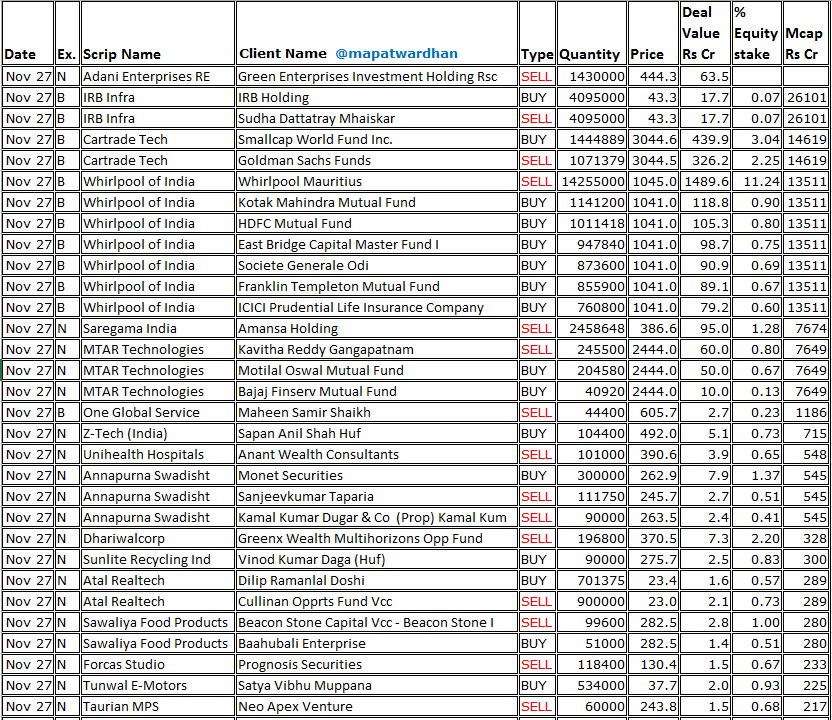

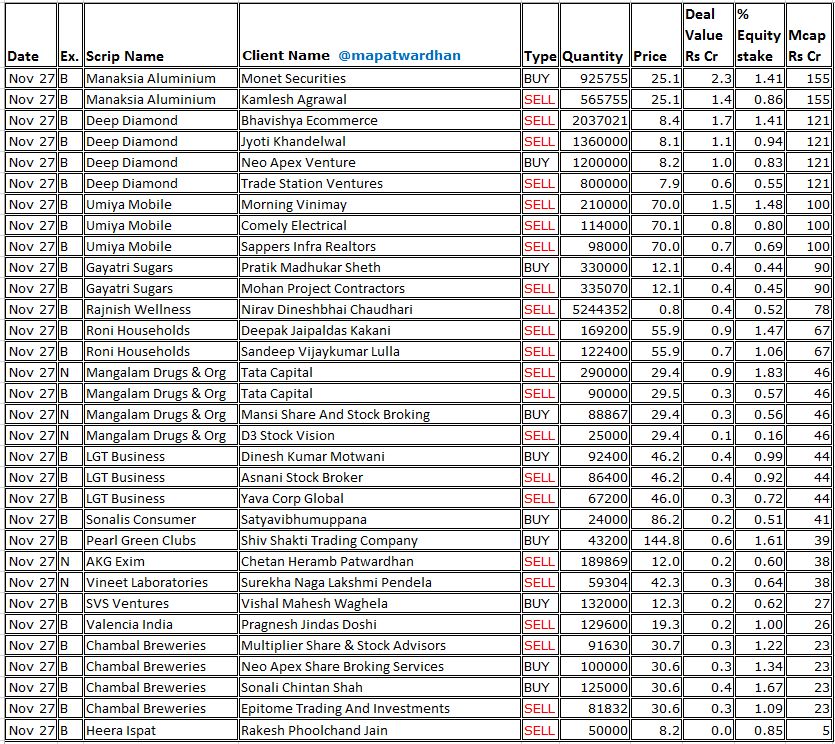

*Today's bulk / block deals*

#AdaniEnt #IRBInfra #CartradeTech #WhirlpoolIndia #SaregamaIndia #MTARTech #OneGlobalServices #ZTechIndia #DhariwalCorp #AnnpurnaSwadisht #SunliteRecycling #SawaliyaFood #ForcasStudio #TunwalEMotors #TaurianMPS #ManaksiaAluminium #DDIL #UmiyaMobile

1

14

1,454

16 Nov 2025

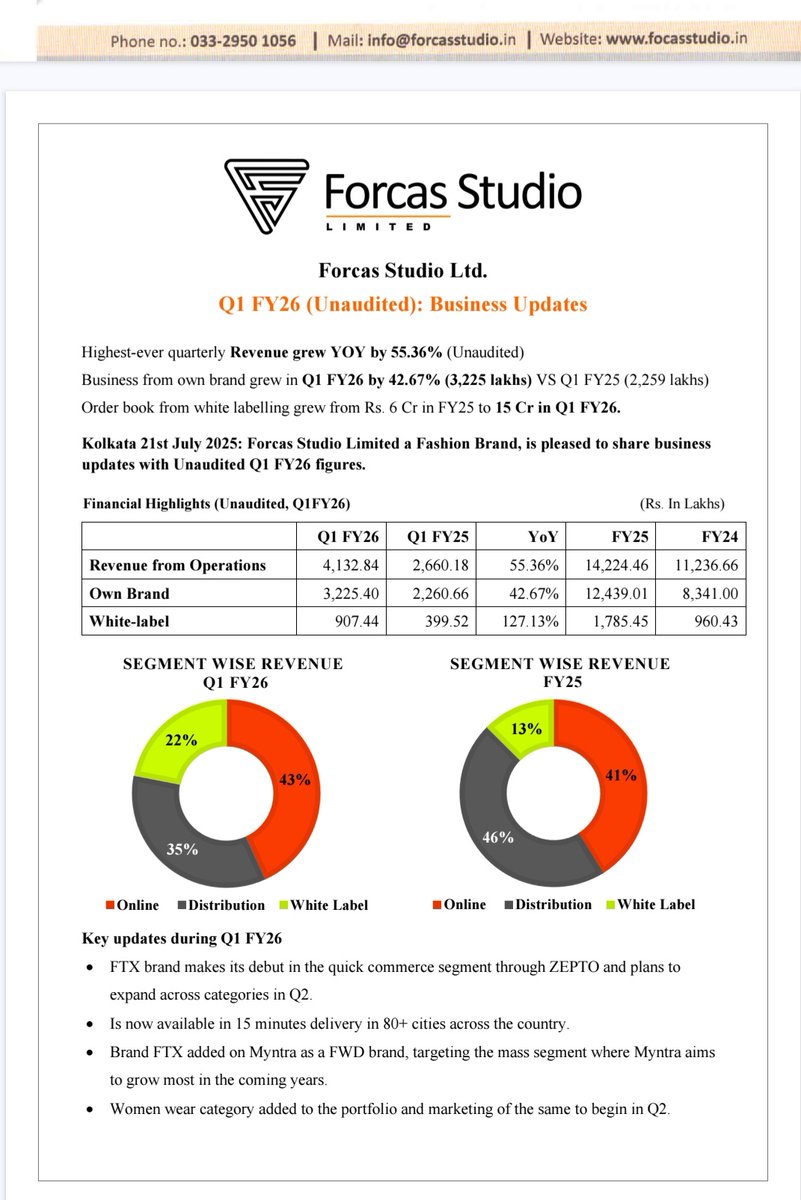

#SME #Forcas #ForcasStudio

Forcas Studio H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️Emphasized a core target of ~35% YoY revenue growth, but as actuals exceeded this, expectations are now revised to 30-40% YoY for FY26

💠Own-brand revenue: ~₹72 Cr, with FTX at ~49% and TRIBE at ~35% growth

▫️EBITDA margins are expected to sustain and improve

💠Supported by higher-margin categories like women's wear (20-30% better than men's) and kids' wear (10-15% better than men's)

💠Rising ASPs (from ₹350-370 to ₹450) due to increased bottom wear sales

💠Net profit margins are projected to expand further, with H1 nearly doubling YoY profits, aided by channel diversification and low return rates (<12% vs. industry 18-19%)

👉Projects and pipeline:

▫️Quick commerce expansion: Stocked on Zepto across 17-18 cities (dark stores), delivering to 50-60 towns; added 7 new categories (e.g., kurtas, jackets, sweatshirts, trousers) since July, with rapid traction (e.g., kurtas driving sales in Hyderabad, Lucknow, South India; winter wear via 10-min delivery)

▫️E-commerce: Live on Myntra FWD with ~2,000 options; generated initial orders for shirts and denims from quick commerce platforms

▫️New categories: Women's and kids' wear under FTX launched offline first (₹5.5 Cr revenue to date); Varanasi warehouse added for UP/North India coverage

▫️Inventory pipeline: 2M units holding capacity (up from 600K); 90% is "set" inventory for proven SKUs, with intentional build-up for Q3 winter (e.g., sweatshirts, kurtas)

▫️Pipeline:

💠 Q3 launches: Online rollout of women's/kids' wear; new women's sportswear line (₹299-599 price band)

💠Expansion: Add 1-2 more quick commerce/e-commerce sites; deepen women/kids' lines; summer product pipeline with new options/channels

💠Growth Strategy: Data-driven stocking (pincode-level insights from 15 years experience); omni-channel push (9 states for e-commerce, 15-16 cities for quick commerce); target 5-10% revenue mix from quick commerce by FY27 (rapid scaling expected post-3-month testing)

👉 Others :

▫️Customer acquisition: Added ~1mn customers in H1 via B2C platforms; strong repeat ratios and 4 /5 ratings on marketplaces

💠Asset-light (outsourcing manufacturing, no in-house production); lean omni-channel

💠No D2C for FTX due to high ad costs at low ASP ~₹400; prefer marketplace commissions of 30-33% only on sales)

💠Data / Algo optimization (views → clicks → conversions → low returns → availability) ensures visibility

▫️Working capital: Receivables down; inventory up 30-40 days due to 50% H1 growth/seasonality (Durga Puja shutdown, Punjab raw material crisis—strategic bulk buying in Aug-Sep)

💠Payables shortened (13 days) for supplier loyalty (earlier 124 days: FY24 / 47 days: FY25)

▫️Stake ownership: Promoter group subscribed 70-80% to warrants, increasing stake; no further dilution/debt planned

▫️Risk management: Low returns (tops <7%, bottoms 14-15%, avg. <12%) via quality focus and data (e.g., starting women's with low-return bottoms/athleisure); inventory write-offs <2% (test 100 new options/month at small depths, fail fast via discounts)

1

16

2,210

11 Nov 2025

9️⃣Forcas Studio Ltd🔖

🔶Revenue Guidance ~ 27%

🔹Company has guided FY26 revenue of INR 190–200 Cr, with 30–40% CAGR over the next 2 years.

#forcasstudio #StockMarket #StocksToWatch

1

1

235

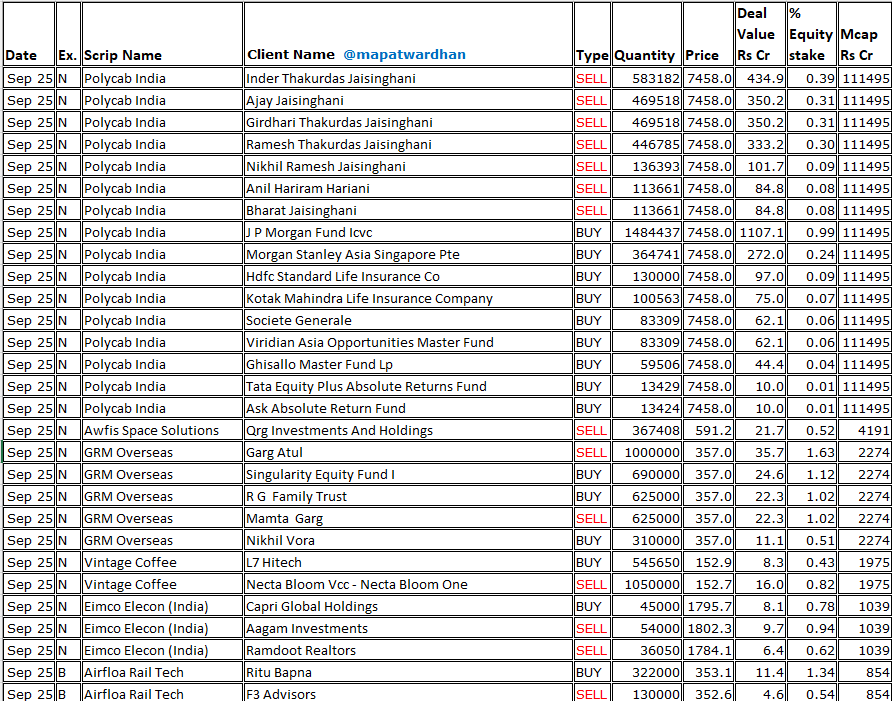

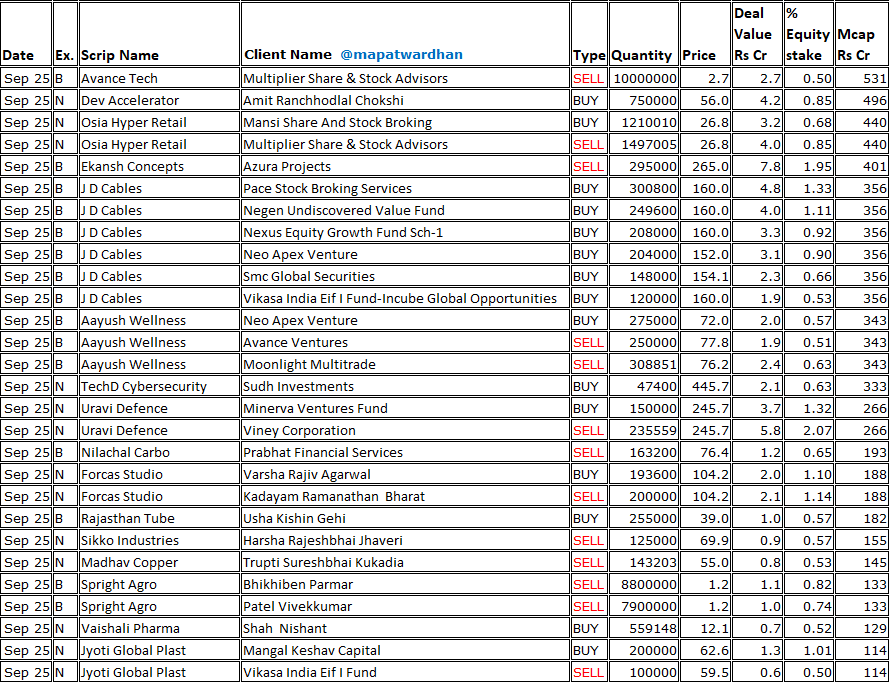

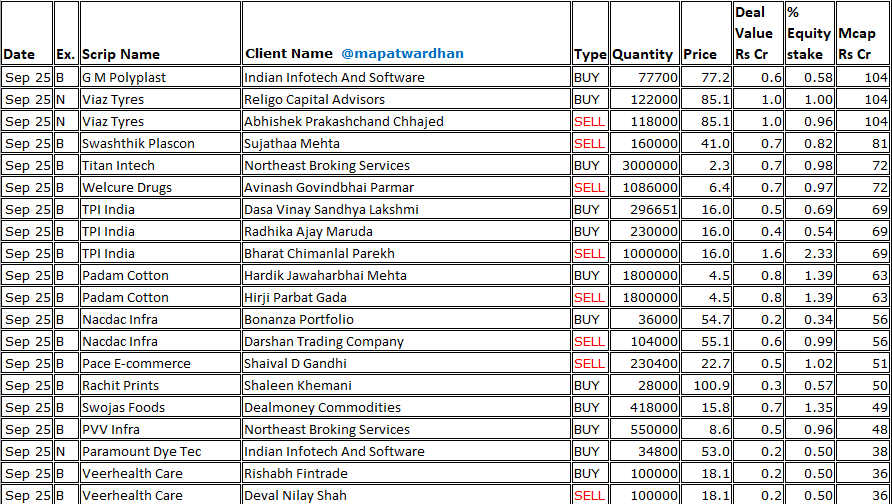

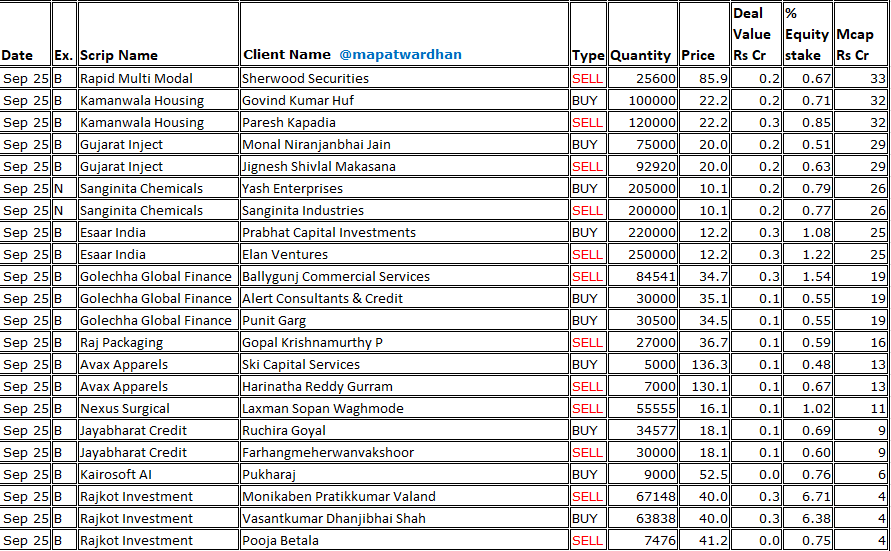

25 Sep 2025

*Today's bulk /block deals*

#PolycabIndia #AwfisSpace #GRMOverseas #Vintagecoffee #EimcoElecon #AirfloaRail #AvanceTech #DevAccelerator #OsiaHyperRatail #EkanshConcepts #JDCables #AayushWellness #TechD #UraviDefence #NilachalCarbo #ForcasStudio #RajasthanTube #SikkoInds

2

1

25

2,477

24 Sep 2025

#Forcasstudio

- Sells garments under brand FTX, TRIBE for men, women & kids

- 50k sq ft warehousing & dark stores across 8 cities

- FY25 = 153/9cr

- FY26e = 200/13cr ; Q1 = 40cr

- Online marketplace- 41%

- White label mfg for landmark, V2 retail- 22%

- 85-90% from Tier 2/3

1

13

4,284

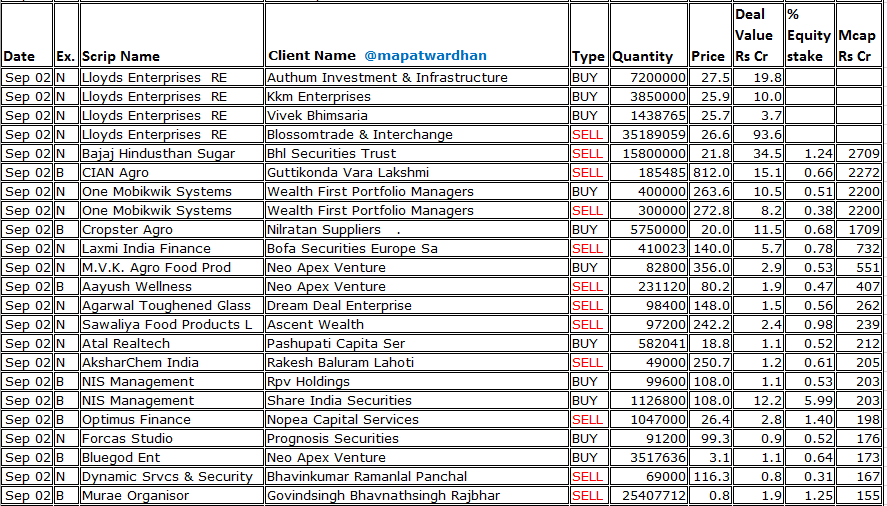

2 Sep 2025

*Today's bulk / block deals*

#VertisInfra #LloydsEnt #BajajHindusthanSugar #Onemobikwik #CIANAgro #CropsterAgro #LaxmiIndiafinance #SawaliyaFood #AayushWellness #MVKAgro #AtalRealtech #AksharChem #NISManagement #OptimusFinance #ForcasStudio #BluegodEnt #DynamicServices

2

1

32

3,417

26 Jun 2025

*Today's bulk / block deals*

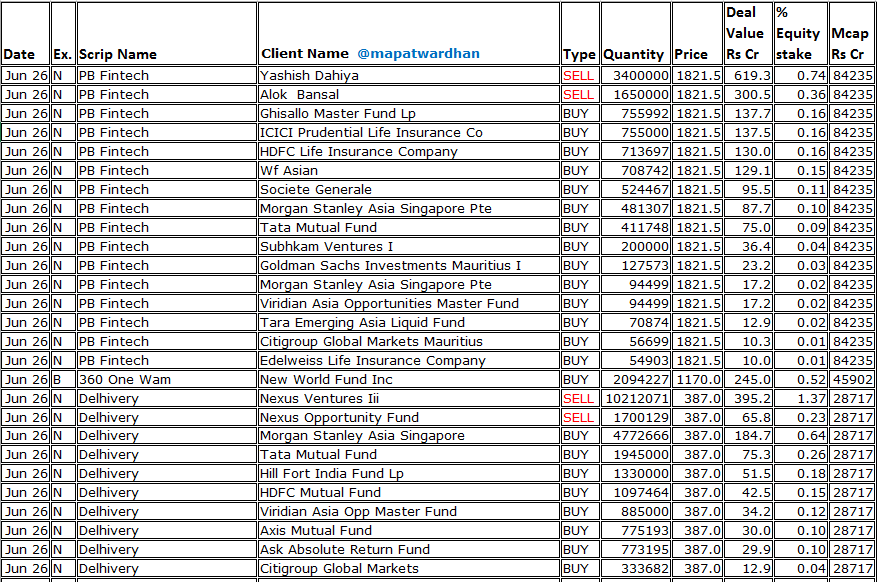

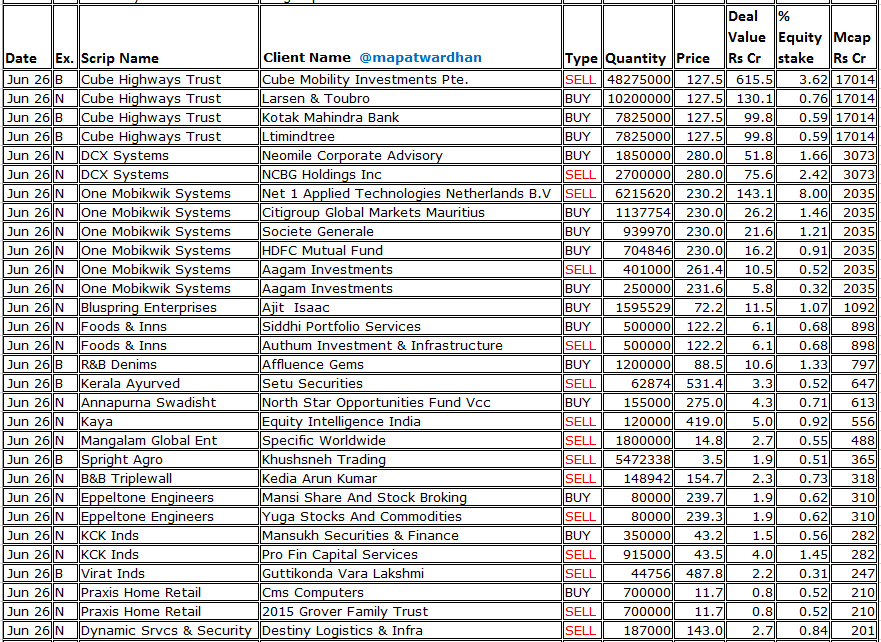

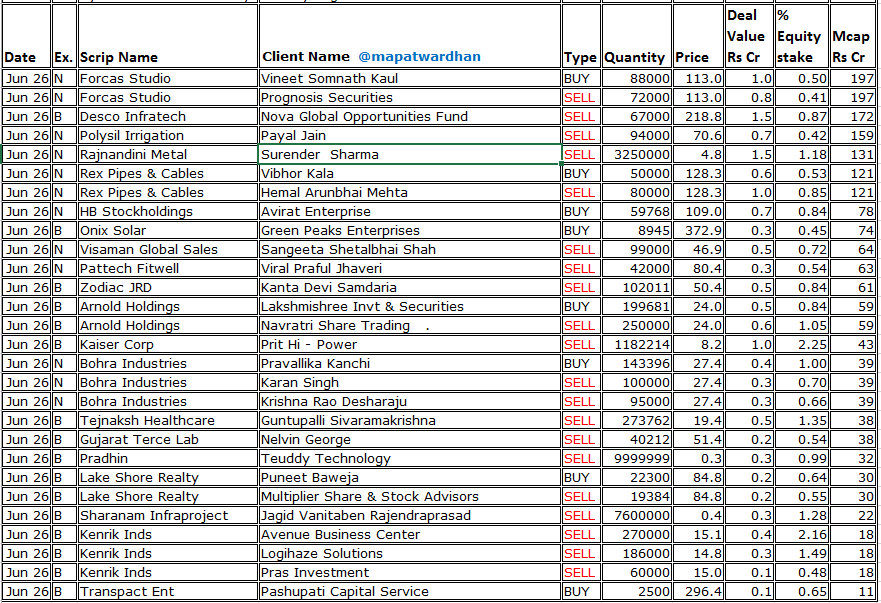

#PBFintech #360OneWam #Delhivery #CubeInvIT #DCXSystems #Mobikwik #Bluspring #FoodsInns #RNBDenims #KeralaAyurved #Kaya #MangalamGlobal #SprightAgro #Eppeltone #KCKInds #ViratInds #PraxisHome #DynamicServices #CapitalTrust #ForcasStudio

2

1

25

4,139

24 Jun 2025

Forcas Studio Ltd🔖

💰Market Cap~ ₹ 199 Cr.

💫PE Ratio~ 23.1

⚡ROCE ~ 21.4 %

🔥ROE~20.6 %

🔥OPM~9%

🤵Promoter Holdings~ 60.3 %

🗽Revenue Guidence ~35% Target 🎯 over the next two years

#forcasstudio

#StocksToWatch #StockMarketIndia #earnings

1

1

3

1,152

12 Jun 2025

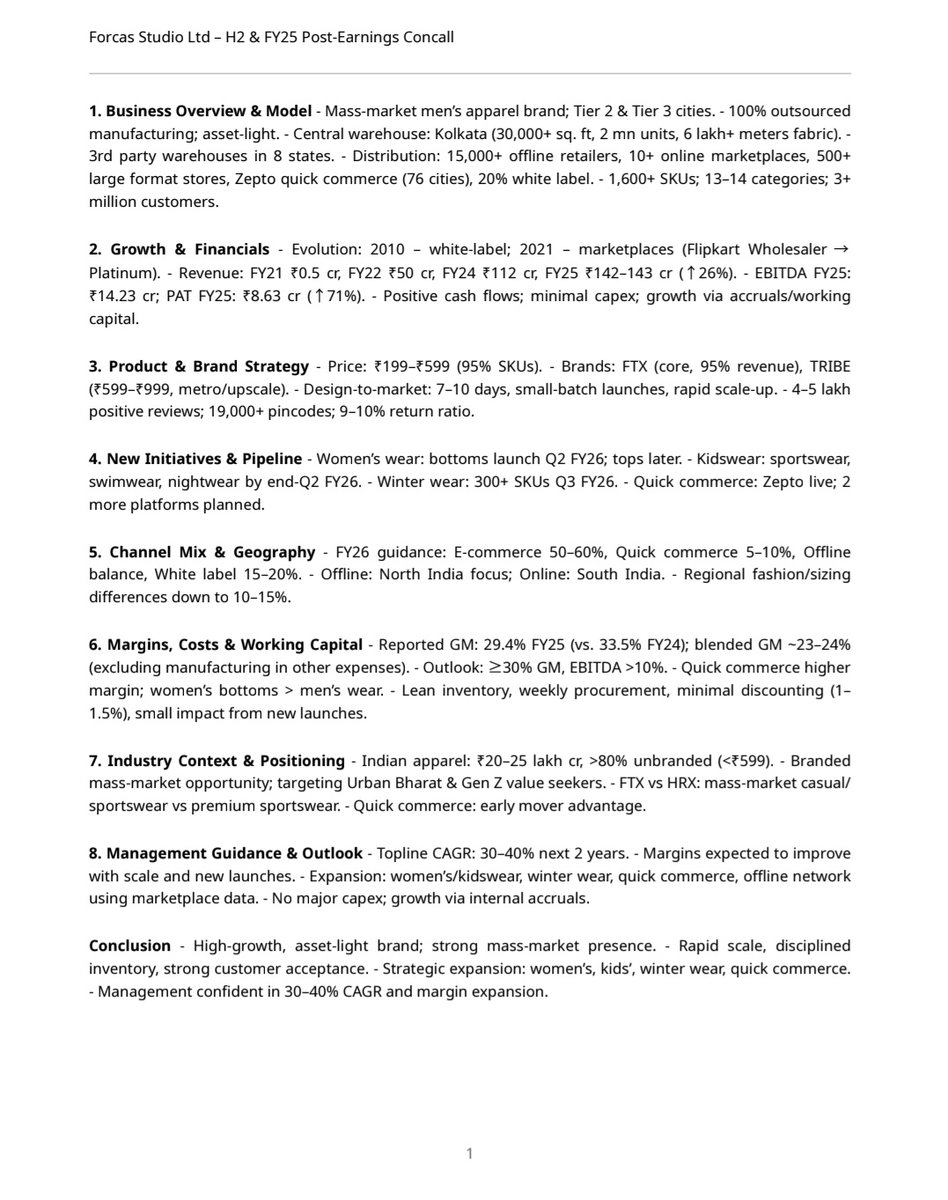

#SME #ForcasStudio #Forcas

Forcas Studio FY25 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️ Targets 30-40% YoY revenue growth for next two years

💠Expansion in quick commerce (expected to contribute 5-10% of revenues)

💠Launch of women’s bottom wear and kids’ sports/nightwear in Q2 FY26

💠Scaling offline distribution in high-demand regions (e.g., Tamil Nadu) and deepening e-commerce presence (50-60% of revenue)

▫️EBITDA Margins: Improve beyond FY25’s 10%

💠Higher margins in quick commerce (lower return costs, premium pricing)

💠Better inventory optimization reducing dead stock (only 1-1.5% inventory liquidated at discounts)

💠Maturing product lines (men’s wear now spans 14 categories, reducing experimentation costs)

▫️Women’s Wear Margins: Expected to be slightly better than men’s wear due to less frequent fashion rotation in bottom wear, though top wear (planned later) may see lower margins due to higher experimentation

▫️Margin pressure possible during initial launches of women’s and kids’ wear due to small-batch testing, but mitigated by low quantities (200-300 units per style)

👉Current product outlook and pipeline:

▫️E-commerce (50-60% of Revenue):

💠Present on 10 marketplaces (e.g., Myntra, Flipkart, Amazon, Snapdeal, JioMart)

💠FTX brand dominates (95% of FY25 revenue), with 1,600 SKUs in men’s wear

💠Strong performance with 4 ratings, 4-5 lakh positive reviews on Amazon/Flipkart, and low return rates (9-10% vs. industry ~20%)

💠Serving 19,000 pin codes, delivering within 24-72 hours

▫️Quick Commerce (Recently Launched):

💠Launched on Zepto in 76 cities, delivering within 20 minutes

💠Initial success with one design (7-8 colors), showing good numbers in first month

💠Focus on basic apparel (e.g., swimwear, gym wear) tailored for quick commerce customers (metro, convenience-driven)

▫️Offline Distribution (Balance of Revenue):

💠Supplies 15,000 retailers across 8-9 states, primarily North India (Delhi, Punjab, Rajasthan, Madhya Pradesh, Bengal, Assam)

💠Present in 500 large-format stores (DMart, Reliance, Vishal Mega Mart)

💠Data-driven allocation of inventory to high-demand regions

▫️White-Label Manufacturing (~20% of Capacity):

Continues for large-format stores, providing stable cash flows but not a growth focus

▫️Current Product Lines:

💠Men’s wear (13-14 categories: boxers, shorts, cargos, denims, trousers)

💠Tribe brand (5% of revenue, targeting metro customers at ₹599-₹1499)

💠Winter wear: 70-80 options in FY25

▫️Pipeline:

▫️New Product Launches (Q2 FY26):

💠Women’s Bottom Wear: 70 styles (denims, trousers), small quantities (200-300 units per style) to test demand. Focus on stable products to minimize margin hits

💠Kids’ Sports/Nightwear: Targeting swimwear, gym wear, and nightwear with cartoon/trendy designs, avoiding core fashion to reduce risk

▫️Quick Commerce Expansion:

💠Plans to launch 50 new options in 30-60 days on Zepto

💠In talks with two additional quick commerce platforms to scale to 100 cities

▫️Winter Wear Push:

💠Scaling to 300 options in FY26 (200 with high quantities), backed by data from experimentation

💠Targeting unbranded segments like windcheaters and light jackets under ₹500-600

▫️Hiring sales teams in eight states to scale retailer network

👉 Others :

▫️ Gross Margin Volatility: Management attributed this to experimentation with new men’s wear categories (from 4 to 14) and use of COVID-era inventory which inflated prior margins. No expense reclassification occurred; manufacturing costs are in “other expenses.”

💠For FY25 intra-year variability (H1 35% to H2 25.8%), cited new product launches in H2 as the driver, with no clear explanation for why other expenses remained flat despite outsourcing

💠Management promised to share detailed schedules to help in other expense analysis

▫️Inventory Management:

💠Lean model with weekly procurement based on real-time data (daily run rate available per SKU across ~9,000 unique SKUs); ensuring no single SKU ties up excessive capital or warehouse space (30,000 sq ft in Kolkata, plus 8 third-party warehouses)

💠Quick commerce inventory limited to 30-40 days, replenished weekly, minimizing working capital strain

▫️Competitive Positioning:

💠Targets the unbranded sub-₹599 market (80-95% of 20-25 lakh crore apparel market), where no national brand exists

💠Differentiates from HRX by offering casual wear (vs. HRX’s sports focus) and targeting mass customers (90-95% of FTX products below ₹599 vs. HRX’s 10-15%)

💠Social media and travel have reduced regional taste differences (from 50% to 10-15%), enabling standardized designs with minor regional tweaks

▫️Capital Requirements:

💠Asset-light model (outsourced manufacturing, no owned stores) minimizes capex needs

💠No plans for in-house manufacturing, preferring outsourcing to stay asset-light and focus on brand-building

💠Working capital manageable due to low inventory for new launches and quick commerce. Bank financing available if needed

▫️Sustainability:

💠Limited focus on eco-friendly fabrics as mass-market customers prioritize affordability. Some recycled yarn used for cost benefits, but not a core brand proposition

1

5

1,440

12 Jun 2025

*Today's bulk /block deals*

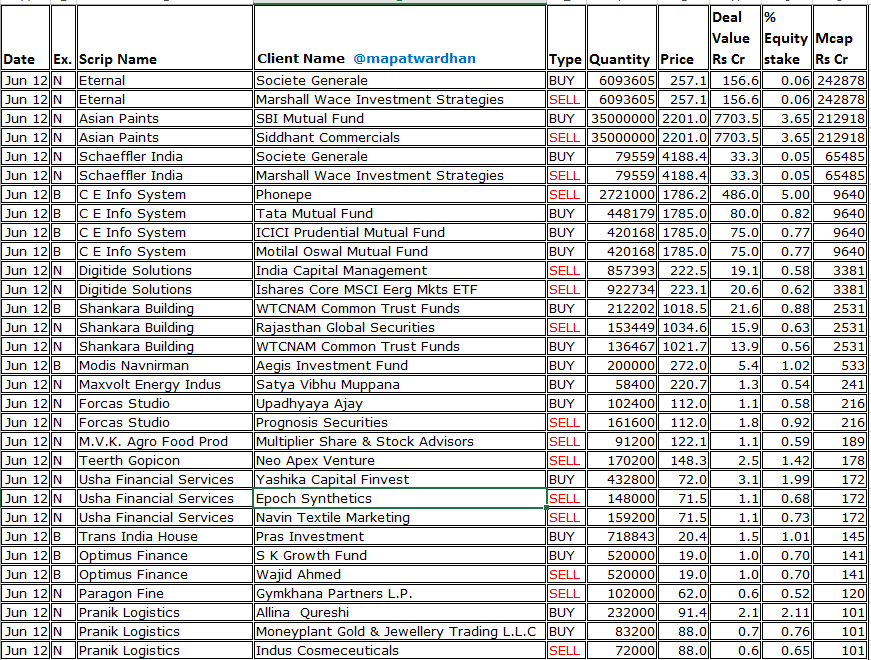

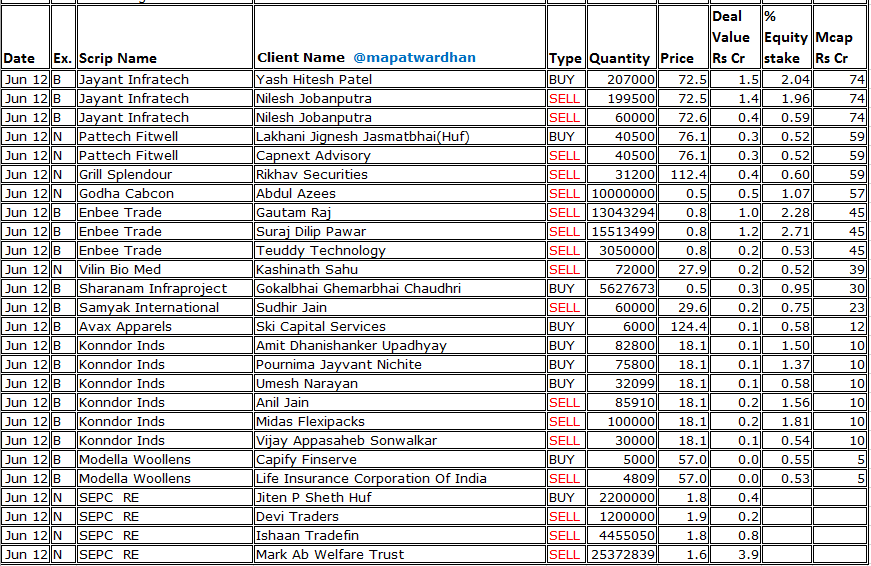

#Eternal #AsianPaints #SchaefflerIndia #MapMyIndia #Digitide #ShankaraBuilding #ModisNavnirman #Maxvolt #ForcasStudio #MVKAgro #TeerthGopicon #UshaFinancial #TransIndiaHouse #ParagonFine #OptimusFinance #JayantInfratech #PattechFitwell #GrillSplendour

1

1

26

6,599

12 Jun 2025

🧵 Forcas Studio Ltd | FY25 Earnings Call Breakdown 👕💼 | 12th June 2025

A detailed session covering revenue growth, margin trends, Q-commerce, and new category launches (women's & kidswear).

Let’s dive into the full thread 👇

#ForcasStudio #TRIBE #StockMarketIndia #EarningsThread

1

6

975

30 May 2025

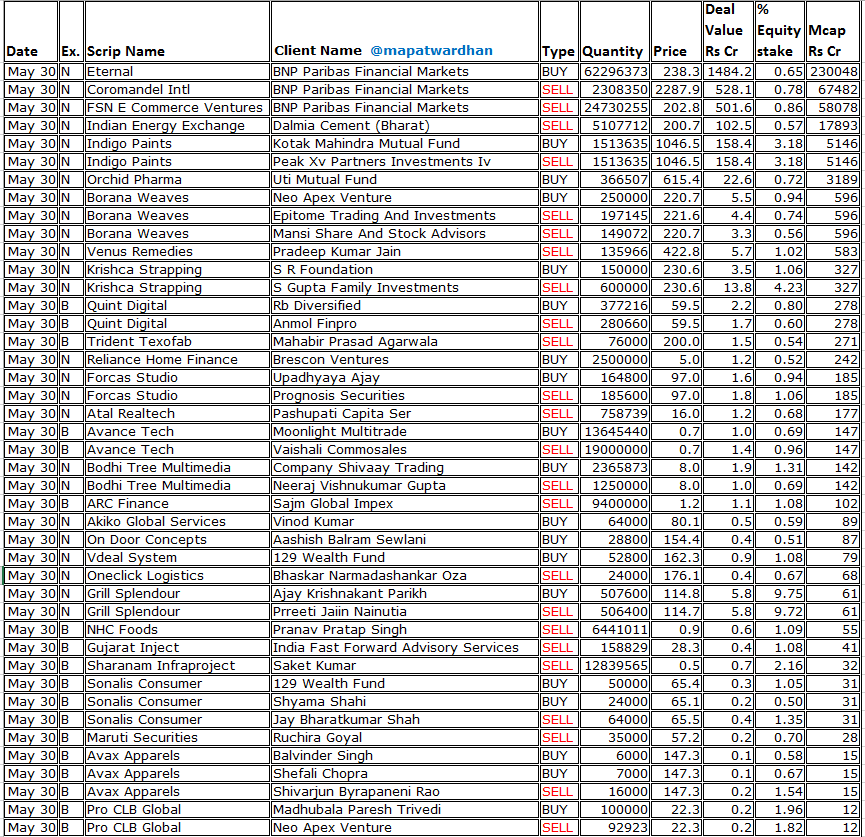

*Today's bulk / block deals*

#Eternal #Coromandel #FSNECommerce #IEX #IndigoPaints #OrchidPharma #BoranaWeaves #VenusRemedies #KrishcaStrapping #QuintDigital #TridentTexofab #ReliaceHomeFinance #ForcasStudio #AtalRealtech #AvanceTech #BodhiTree #ARCFinance #AkikoGlobal

1

1

17

3,038

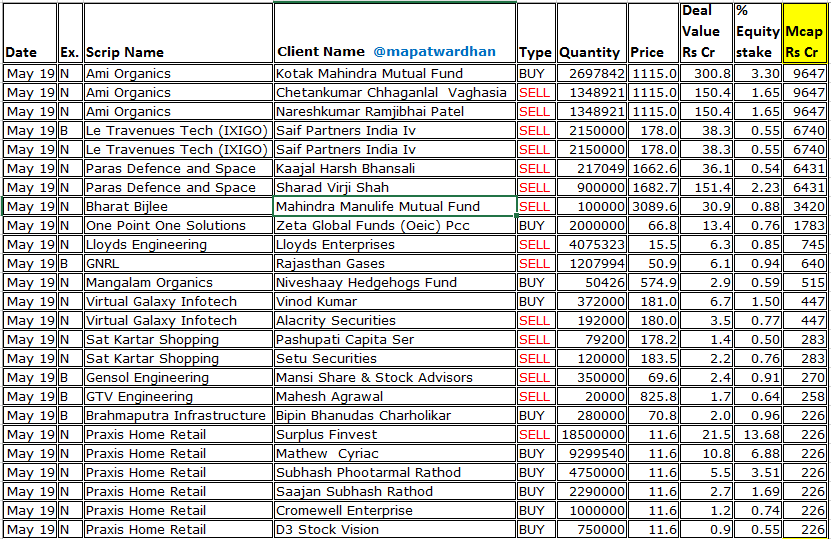

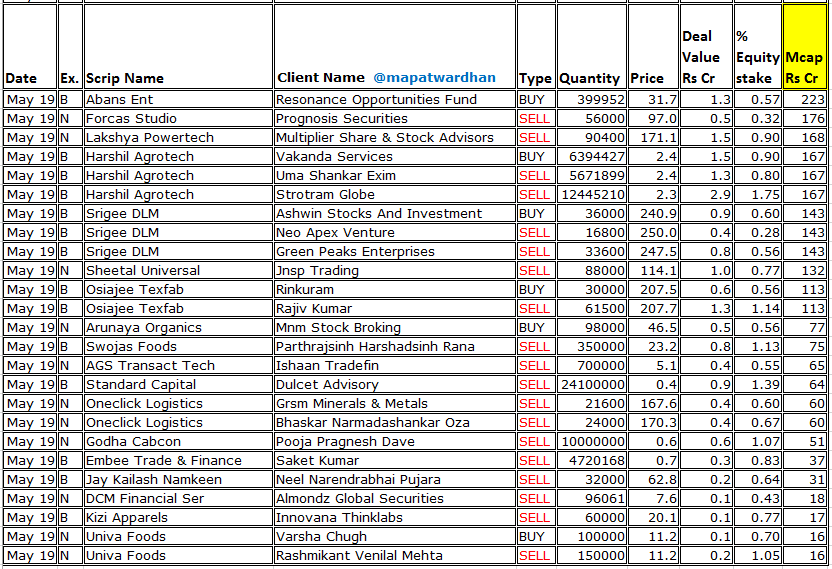

20 May 2025

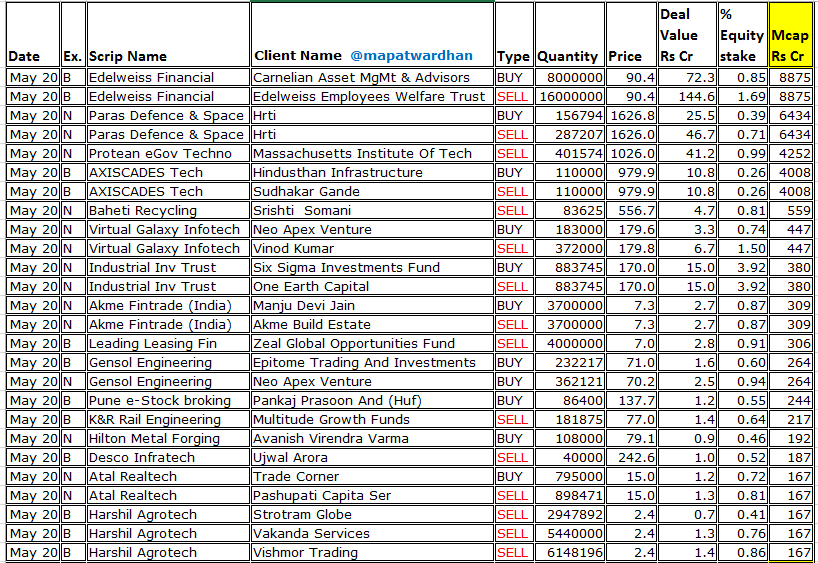

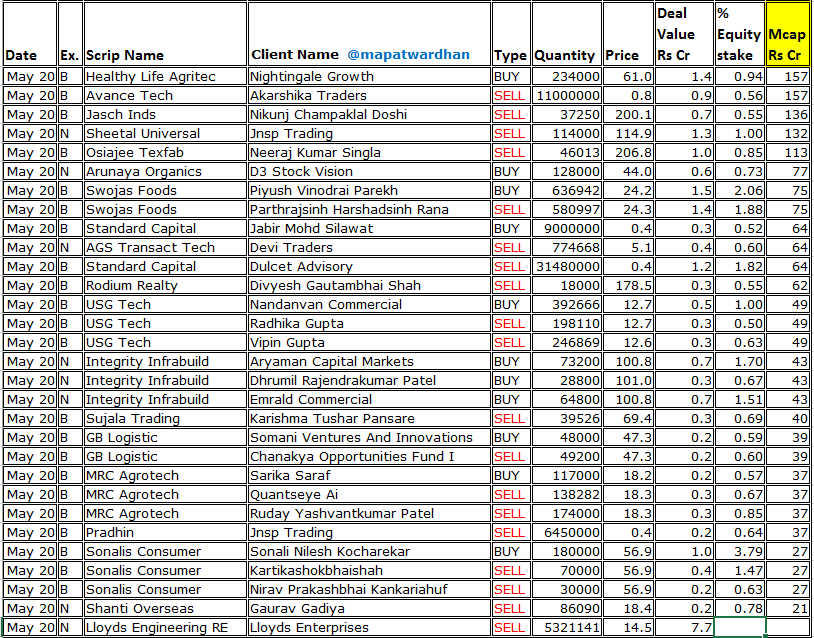

*Today's & Yesterday's bulk / block deals*

#AbansEnt #AGSTransact #AKMEFintrade #AmiOrganics #ArunayaOrganics #AtalRealtech #AvanceTech #Axiscades #BahetiRecycling #BharatBijlee #BrahmaputraInfra #DCMFinancial #DescoInfratech #EdelweissFinancial #EmbeeTrade #ForcasStudio

1

25

2,949

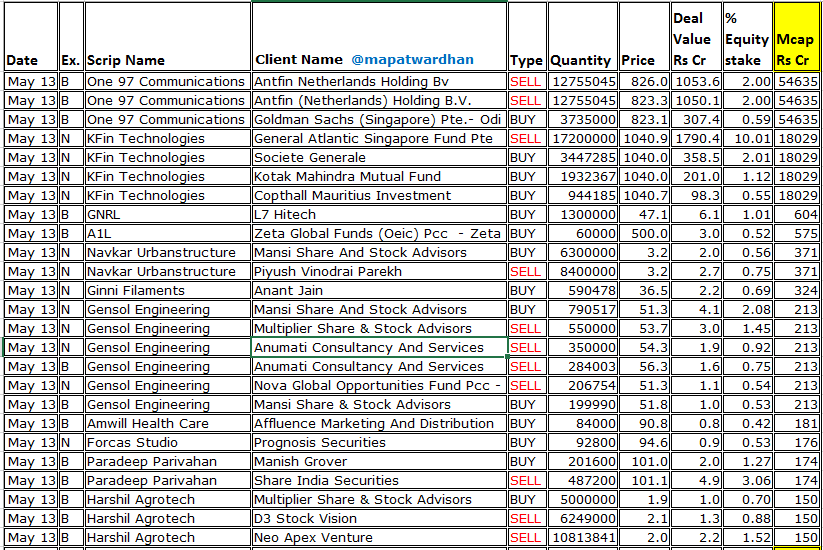

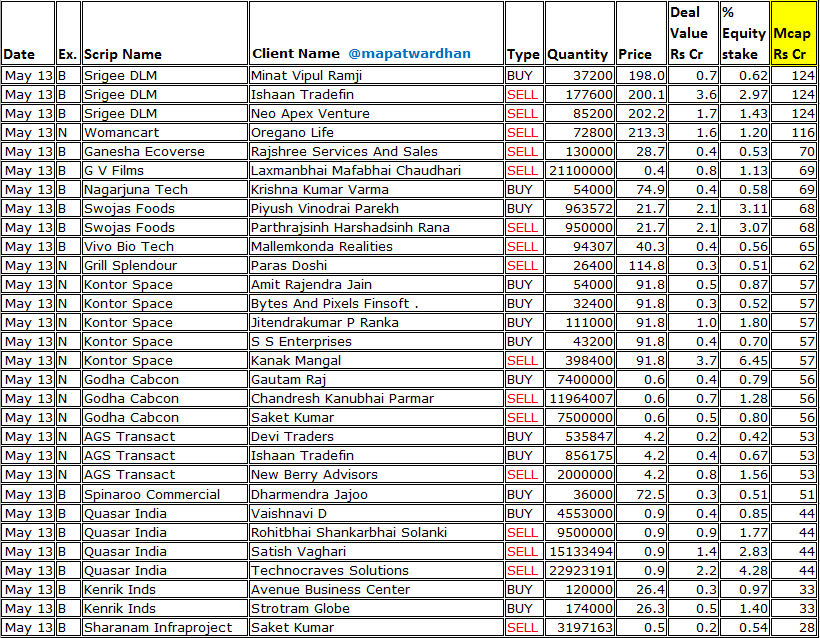

13 May 2025

*Today's bulk / block deals*

#One97Communications #KFinTechnologies #GNRL #A1L #NavkarUrbanstructure #GinniFilaments #GensolEngineering #AmwillHealthcare #ForcasStudio #ParadeepParivahan #HarshilAgrotech #SringeeDLM #GaneshaEcoverse #GVFilms #GrillSplendour #KontorSpace

2

1

17

2,558

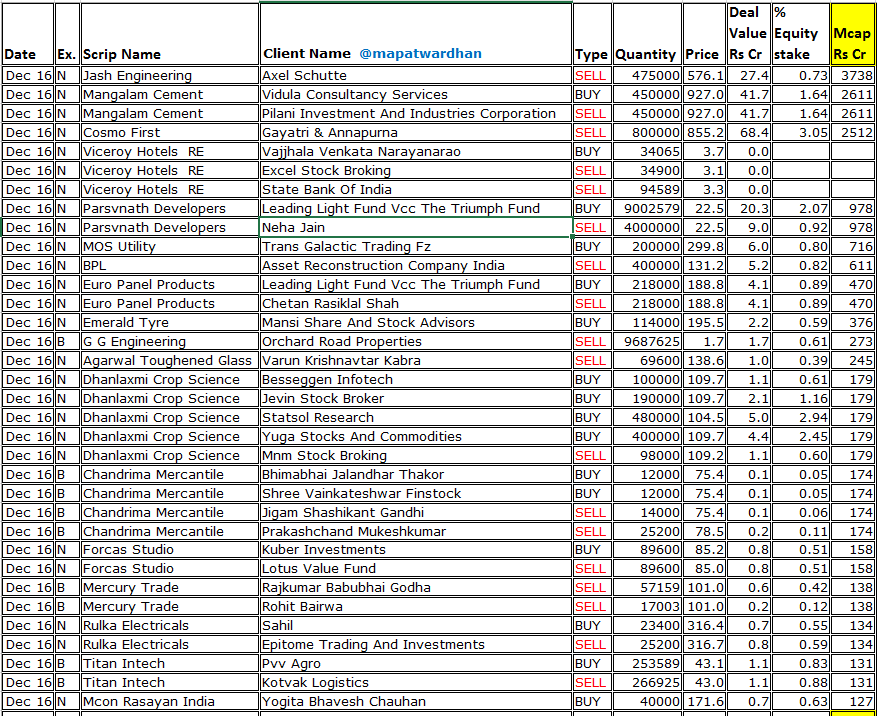

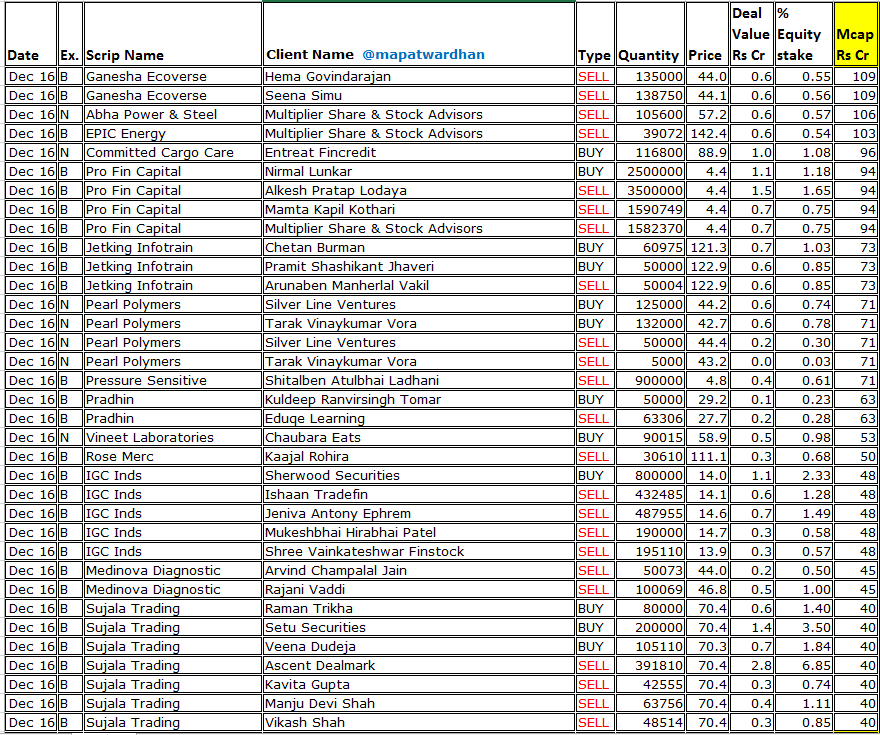

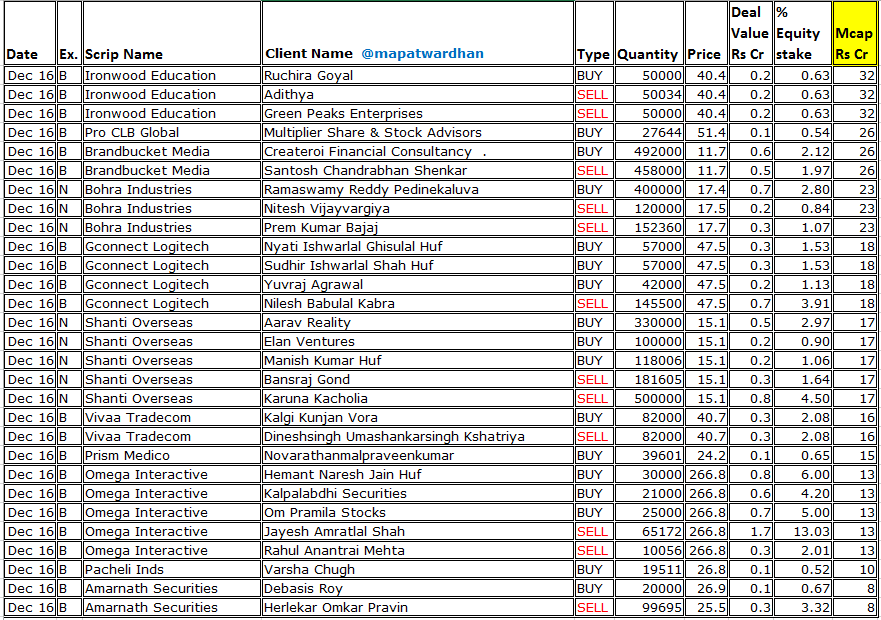

16 Dec 2024

*Today's bulk / block deals*

#JashEngineering #MangalamCement #CosmoFirst #ParsvanathDevelopers #MOSUtility #BPL #EuroPanelProducts #EmeraldTyre #GGEngineering #AgarwalToughenedGlass #DhanlaxmiCrop #ChandrimaMercantile #ForcasStudio #MercuryTrade #RulkaElectricals #TitanIntech

1

1

19

3,000

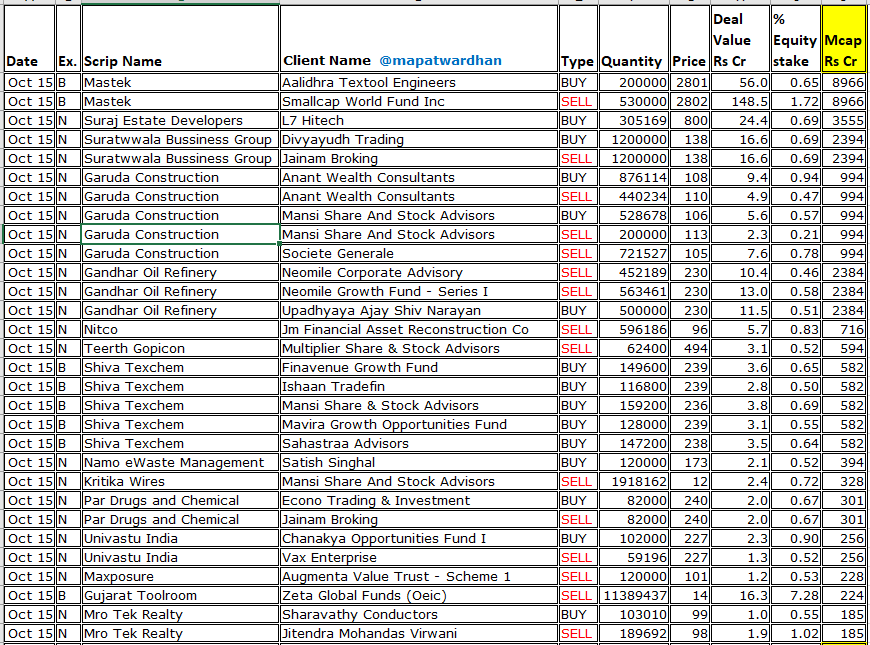

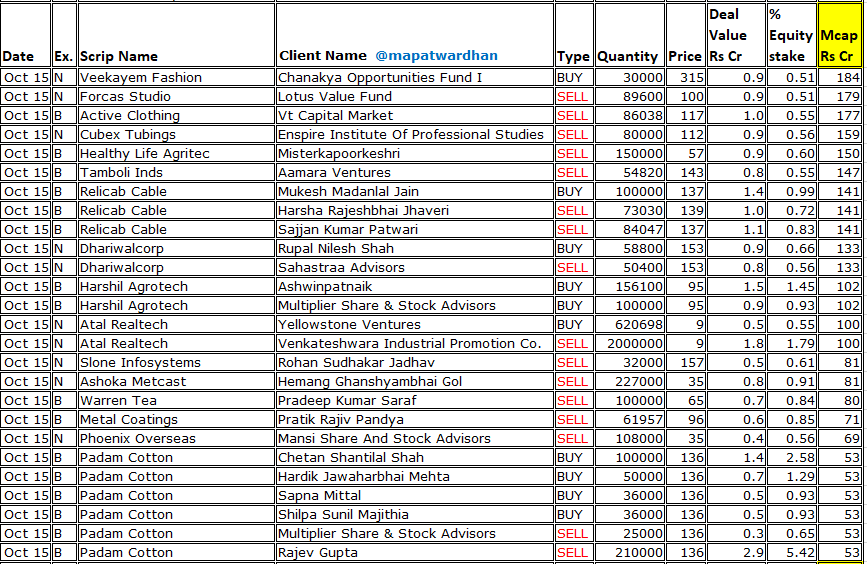

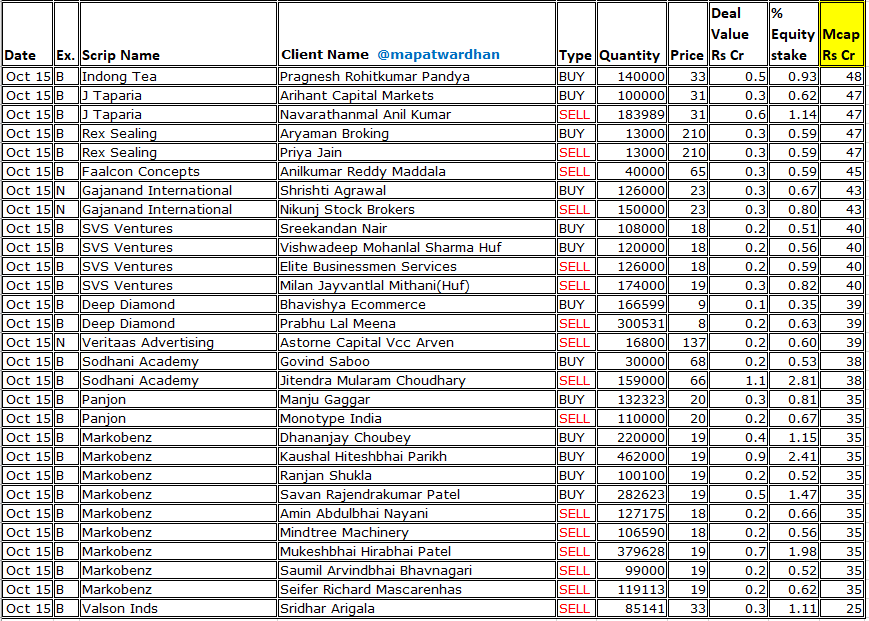

15 Oct 2024

*Today's bulk / block deals*

#Mastek #SurajEstate #Suratwwala #GarudaConstruction #GandharOil #Nitco #TeerthGopicon #ShivaTexchem #NameWaste #KritikaWires #ParDrugs #UnivastuIndia #Maxposure #GujaratToolroom #MroTekRealty #VeekayemFashion #ForcasStudio #ActiveClothing

1

3

19

5,622

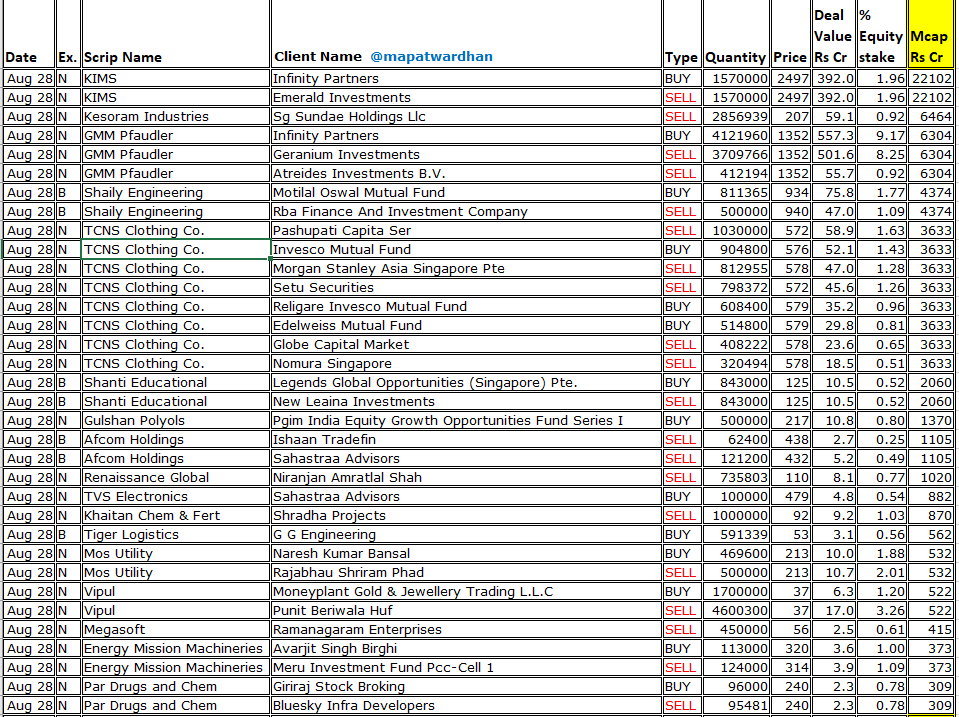

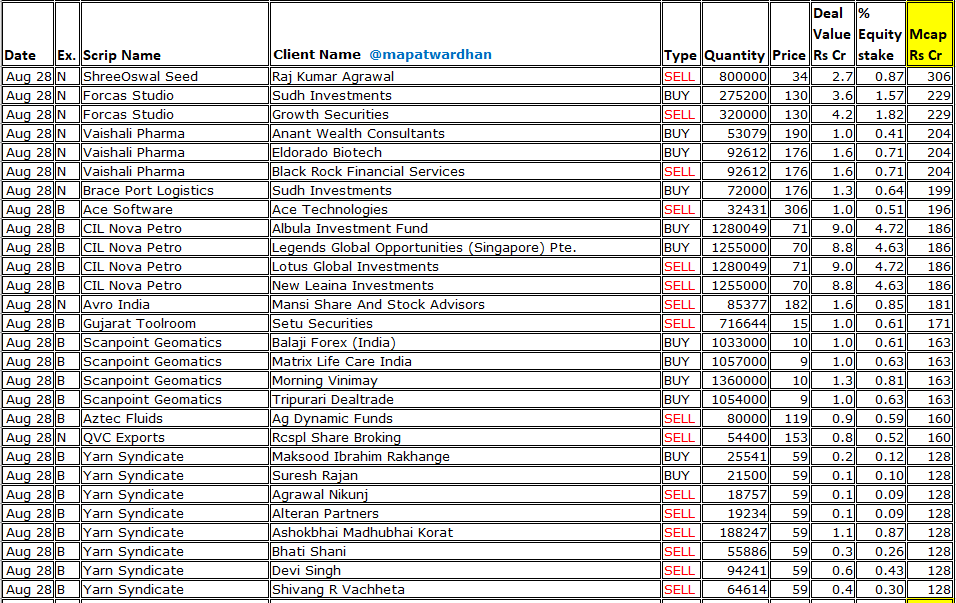

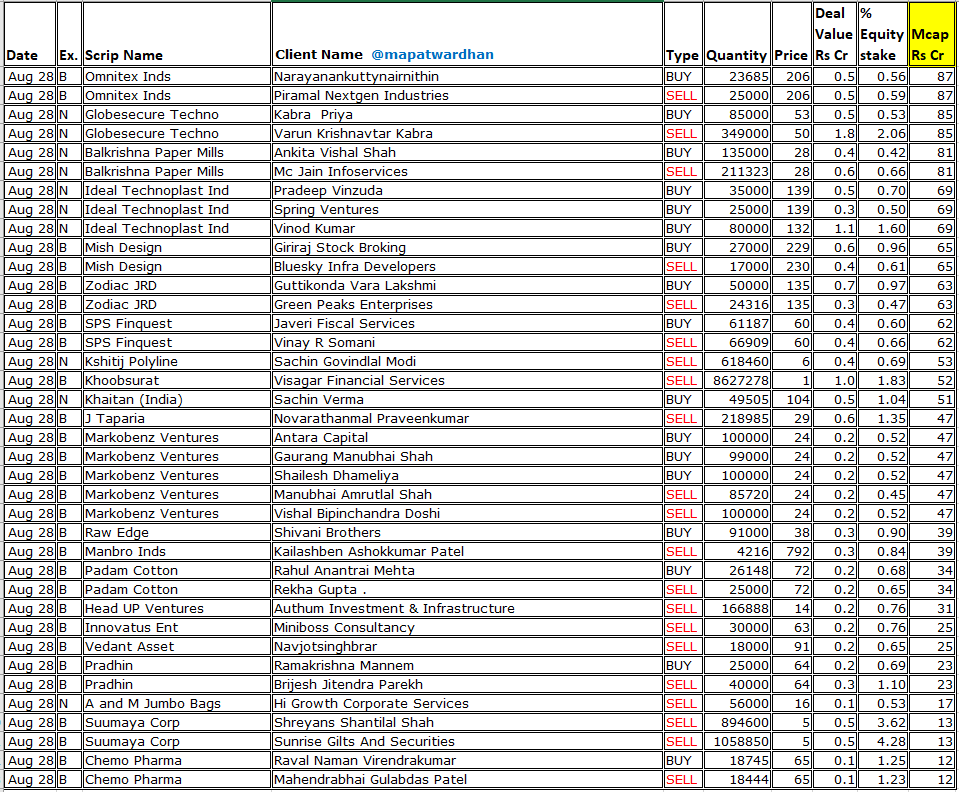

28 Aug 2024

*Today's bulk /block deals*

#KIMS #Kesoram #gmmpfaudler #ShailyEng #TCNSClothing #SEIL #GulshanPoly #AfcomHoldings #RenaissanceGlobal #TVSElectronics #KhaitanChem #TigerLogistics #MOSUtility #Vipul #Megasoft #EnergyMission #ParDrugs #ShreeOswalSeeds #ForcasStudio #VaishaliPharma

1

21

6,814