ANI NYONG BASSEY retweeted

people go doubt.. most of them no even sabi say them papa run fortification give them when them small, especially those wey popsy guide.

1

1

2

10

JOB ALERT

GAIN is seeking to recruit a Project Manager, Fortification and School Feeding to lead the implementation of the Grain to Gains Wholegrain Project.

The starting gross salary on offer for this role is from UGX 94,217,556 – UGX 107,742,240 gross per annum

Apply Now: jobslinking.com/project-mana…

1

36

40m

If you come in to my house unasked and I shoot you in the face, that’s in you.

We also need to do away with anti-fortification laws. They were put in place in an effort not o prevent bikie gangs from fortifying their club houses, but so what, let bikies and home owners fortify.

If law enforcement wants in, they can get a warrant.

5

51m

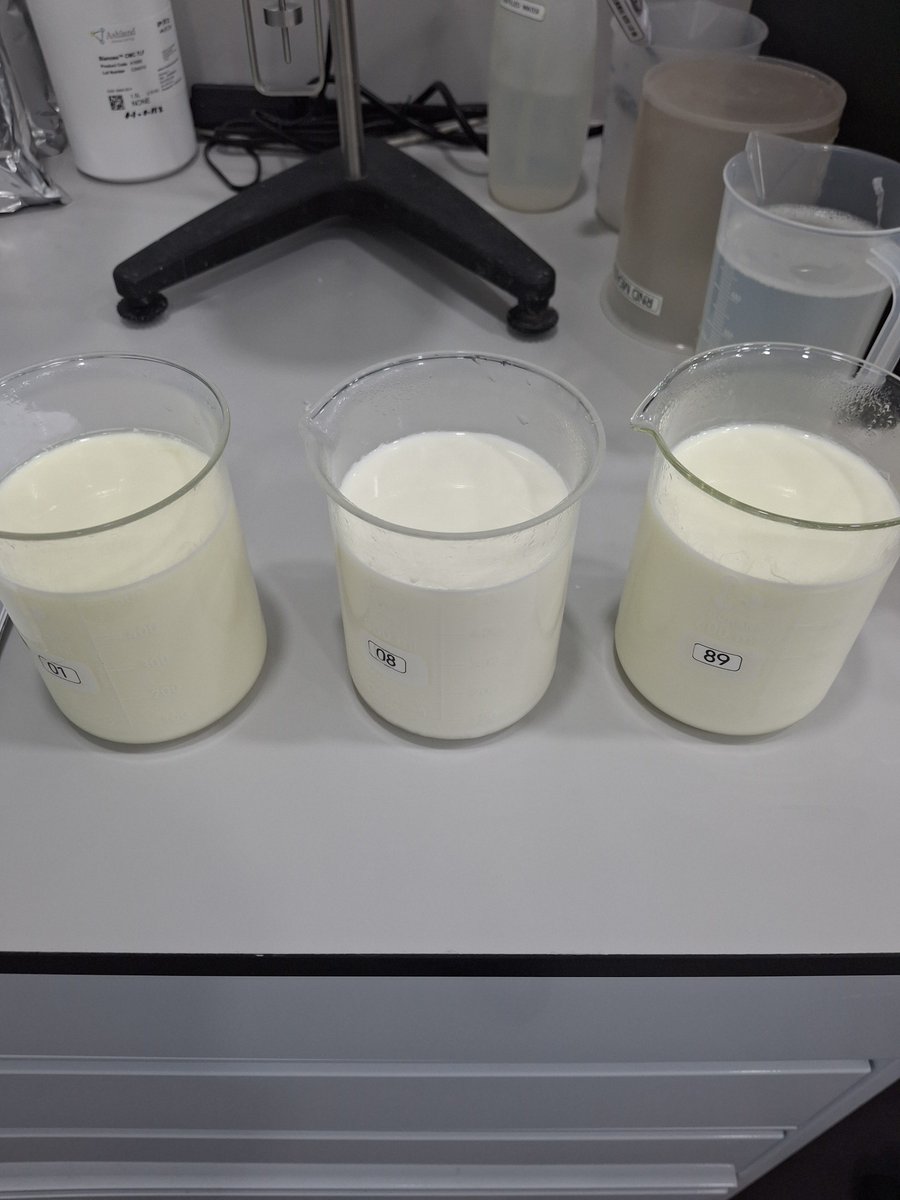

making a typical greek yoghurt applies?

Did you not know that this is a commercial product and not a yoghurt brand as such, fortification can apply to meet the targeted protein value?

Now look at the below picture, 1st, 2nd & 3rd beaker was fortified with SMP, WPC and WPI ...

1

25

Udo_Annang retweeted

This fortification cost like mad..One other thing be say, make your family people sha gree especially the paternal side.. else the juju go too face resistance..

1

2

3

52

Julius Lumansi retweeted

GAIN Uganda is hiring Project Manager, Fortification and School Feeding

Salary: UGX 107,742,240

Details: jobadverts.ug/job/project-ma…

#JobsInUganda

1

6

830

5/5

The engineers of the 91st Brigade work in rain, in snow, under enemy drone surveillance — pausing twice during a single hour-long visit by ArmyInform journalists, once for an FPV drone passing close by, once for a Shahed intercepted almost directly overhead.

Their work is invisible in the way that foundations are invisible. Nobody photographs the obstacle belt after a Russian infantry assault fails. Nobody counts the Shaheds that hit an anti-drone net instead of a truck.

But the kill zone that slows enemy infantry for 90 seconds — those are the 90 seconds in which a Ukrainian drone operator acquires the target and fires.

The fortification that absorbs a 152mm direct hit — that is the shelter that returns a soldier to his position the next morning.

The anti-drone net that catches a Shahed on a metal support — that is the truck, the driver, and the ammunition load that reach the front line.

Modern warfare is decided in the air. It is sustained on the ground.

Ukraine's engineers are building both.

Source: Oleksandr Marchenko ArmyInform, June 16, 2026

#Ukraine #UAF #ModernWarfare #LearnFromUkraine #DefenceTech

5

13

424

Health risks and ethical violations of UK mandatory flour fortification with folic acid expose-news.com/2026/06/15/f…

6

The island, which was originally not much more than a rocky outcrop, was used as a prison after the First Fleet arrived in the 18th century. It was converted to a fortification in the 19th century to help protect Sydney Harbour from attacks by foreign vessels…

1

95

DID YOU KNOW? Sanku has created one of the world's largest food fortification IoT networks. #EndHiddenHunger #TechForGood #NutritionSecurity

1

Focus the "election fortification" efforts in a few Blue counties with the population statistics that could make it feasible. The counties win the states over, and those state's electoral votes wins the country.

You can win the presidency with a handful of blue counties in a handful of swing states. Literally just a few thousand votes here and there.

2

20

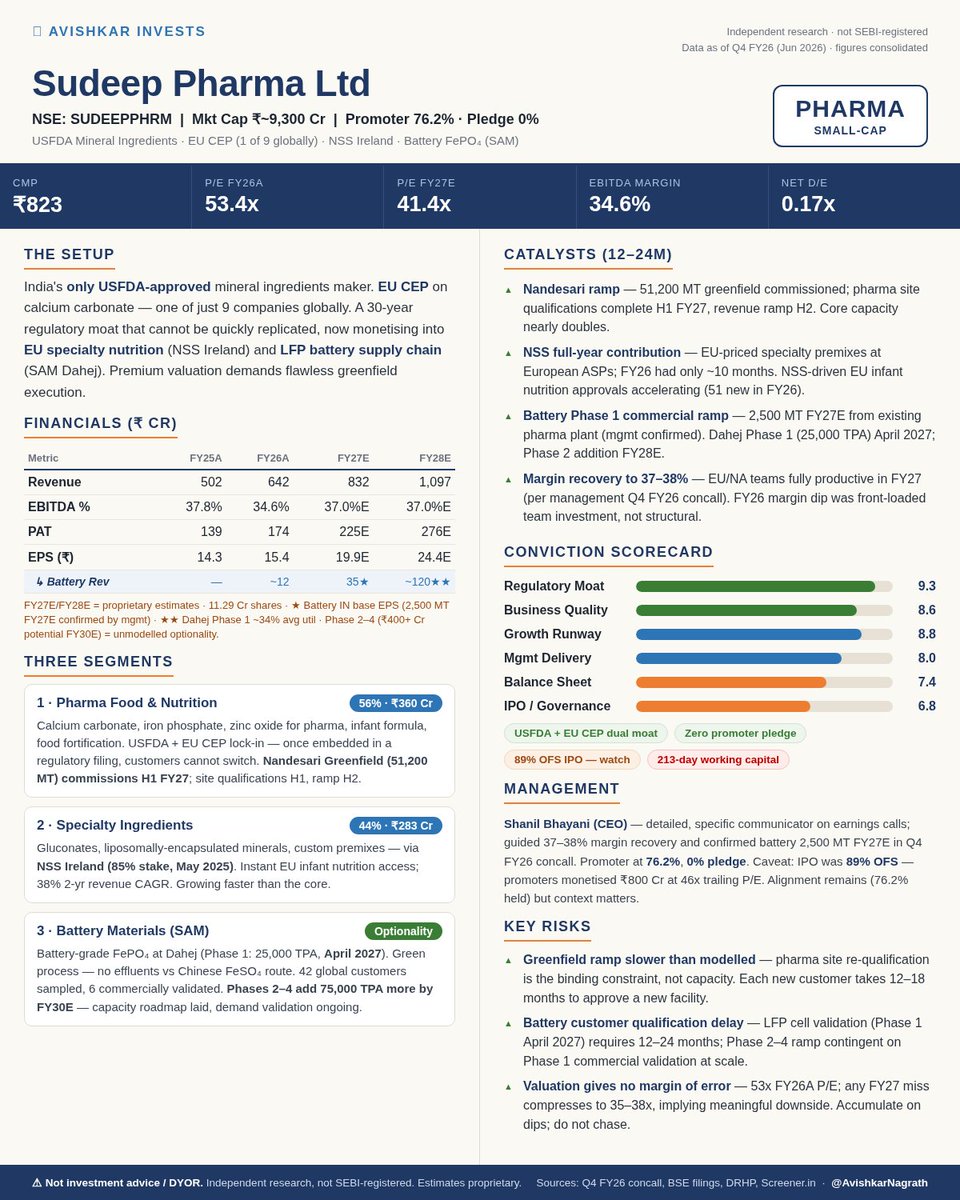

Sudeep Pharma Business Deep Dive:

There's a company in Vadodara that spent 30 years quietly building a regulatory moat that almost no one can replicate. And it's now using that exact moat to enter the LFP battery supply chain.

Sudeep Pharma makes mineral-based specialty ingredients — calcium carbonate, iron phosphate, zinc oxide, magnesium oxide — for pharmaceutical formulations, infant nutrition, and food fortification. Boring description. Extraordinary defensibility. It is India's only company with USFDA approval for mineral-based pharmaceutical ingredients. It holds an EU CEP certification for calcium carbonate — one of just 9 companies globally. Those approvals took 30 years and cannot be copied quickly. The business has run at 34–40% EBITDA margins for three consecutive years. Listed at the IPO in November 2025 at 24% premium; QIBs subscribed at 213x. Here's what the next two years look like ↓

What it does

Three segments. The core is Pharma & Food Ingredients — calcium carbonate, iron phosphate, zinc oxide for pharma, infant formula, and food manufacturing. Premium pricing because buyers cannot switch easily once a supplier is embedded in their regulatory filing. The second segment is Specialty Ingredients — gluconates, liposomal preparations, encapsulated minerals, custom premixes — through the NSS acquisition in Ireland (85% owned, May 2025), giving EU market access for infant and clinical nutrition without the usual 4–5 year regulatory filing wait.

And then there's the third segment. Already partially in our base EPS — with Phase 2 through 4 (FY29–30E) as the unmodelled optionality.

The unmodelled optionality

Sudeep's subsidiary, Sudeep Advanced Materials (SAM), is building a 25,000 TPA battery-grade iron phosphate plant in Dahej, Gujarat. Target commissioning: early CY2027. The connection to the core business is direct — Sudeep has been making food-grade iron phosphate for 30 years. Battery-grade is a purer, more controlled version of what they already make. The difference is the process economics and the end market: LFP (Lithium Iron Phosphate) batteries, used in EVs and energy storage, and increasingly in demand from US and European battery makers who cannot or will not use Chinese supply.

Sudeep's process produces iron phosphate without effluents — a green process vs the standard Chinese ferrous sulphate route, which generates significant waste. That matters because EU battery regulations increasingly require lifecycle disclosures and non-toxic manufacturing. 42 global customers have been sampled. 6 have completed commercial validation. Revenue from this segment is expected at roughly ₹35 Cr in FY27E (2,500 MT from existing pharma plant — management confirmed in Q4 FY26 concall), scaling to ₹120 Cr in FY28E (Dahej Phase 1 at ~34% avg utilisation - my estimate). Both are in our base EPS estimates. Phase 2 through 4 — another 75,000 TPA commissioned FY28–30E, potential ₹400 Cr revenue — is what's unmodelled. That's the optionality.

Why the core business is also inflecting

The Nandesari greenfield (51,200 MT additional capacity) comes online in FY27. The first half goes through customer site approval processes — the regulatory process for a new manufacturing site — and then the second half ramps revenue. That's the driver behind our 30% FY27E revenue estimate of ₹832 Cr, with EBITDA margin recovering back to 37% from 34.6% in FY26. The FY26 dip was explicitly explained by management: "We invested significantly in building out teams across Europe and North America — they will start to positively contribute this year." Front-loaded cost, back-loaded revenue. NSS adds EU-priced revenue on top of that.

FY26 delivered ₹642 Cr revenue ( 28%), ₹174 Cr PAT ( 25%), EBITDA 34.6%. Net D/E 0.17x. The business generates cash and doesn't need external funding for the core. Battery capex (₹300 Cr Phase 1) is partly funded via the IPO proceeds and internal accruals.

The honest pause

Two things to sit with. First, valuation: the stock trades at 49x trailing P/E. Any FY27 earnings disappointment — greenfield ramp slower than expected, NSS taking longer to contribute — and the multiple compresses to 35–38x, implying meaningful downside. This is a name to accumulate on dips, not chase.

Second, the IPO was 89% OFS. Of the ₹895 Cr raised, ₹800 Cr went to existing promoters. That's a meaningful monetisation event at 46x trailing P/E. The promoter still holds 76.2% post-IPO, so alignment remains. But it's worth knowing the context: insiders sold heavily at the listing valuation.

The regulatory moat is real, durable, and took three decades to build. The battery optionality is genuine — built on an existing chemistry advantage, not a pivot. The question is whether the current price reflects it correctly or front-runs it.

Disclaimer: Not investment advice. Independent research, not SEBI-registered. Please DYOR.

#SudeepPharma #SUDEEPPHRM

1

11

37

2,037

FAGGOT, noun / A bundle of sticks, twigs or small branches of trees, used for fuel, or for raising batteries, filling ditches, and other purposes in fortification. The French use fascine, from the Latin fascis, a bundle; a term now adopted in English.

29

While I agree that this type of fortification is closely associated with the steppe, I would note that the term "сѣчъ" (also "засѣка"), denoting a field fortification or a small fortified camp enclosed by a stockade, predates Ruthenian Cossackdom itself.⬇️

1

14

Health risks and ethical violations of UK mandatory flour fortification with folic acid expose-news.com/2026/06/15/f…

I've been sitting on this for a few days. Wasn't sure whether to share it, honestly.

But someone has to say it.

There's a creature in a field at the edge of a Slovenian forest with the most remarkable trick I've ever seen.

It takes, into its mouth, all the salad I personally cannot stomach. Grass, clover, dandelions, weeds, leaves I couldn't name if you offered me money. Chews through it slowly, calm as anything, like it has all the time in the world.

And then, somehow, it processes the entire green nightmare through four stomachs and converts it into ribeye.

Complete protein. Haem iron. B12. All the fat-soluble vitamins. No oxalates. No ingredients list. No fortification required.

I hesitated to post this because if word gets out, the fake meat startups collapse, the oat milk aisle empties by Friday, and half the wellness industry has to find a new product to flog by next Tuesday.

But I think the people deserve to know. The salad problem has already been solved. It's been solved for ten thousand years.

It's just been standing quietly in a field this whole time, waiting for someone to notice.

Sama Hoole

@SamaHoole

8