Shotgun Susie retweeted

Gold & Silver Legal Tender: States Embrace Precious Metals as Legal Tender! Do you stack Goldbacks? Behind the Stack with HERO Bullion CEO Jake Haugen! @HEROBullion

1

5

212

Ok, kids. Grandpa Brian here with a little story.

Back last century whilst in high school, an economics teacher of mine was talking about inflation.

He said movie ticket prices would be $9-$12 by the Year 2000 (which seemed an eternity away when time was measured by a clicking clock on the front of the classroom wall). We were taught back then that putting money into a savings account, with compound interest (we used to have to solve for that by hand, sans calculators) was the SOP of average, everyday Americans.

Tickets for “loge” seating was the premium price of $4.50 back then, for reference.

Inflation used to be the headline report on the local news 40 to 50 years ago. Nowadays, people don’t even question QEx (ongoing Quantitative Easing). Me thinks economic literacy today is a ravine that divides us, and is widening. Like, why do people need an app to tell them what subscriptions they’re paying? Don’t they know how to “balance a checkbook”?

If I were 15 again, I’d be converting a portion of my income/gifts/etc. into Bitcoin, and I’d get my parents to set up 2 brokerage accounts—one for an IRA, one for a rainy day— with $SPY, $QQQ, $JEPQ, et cetera, and cash average my inputs.

I’d probably pick up some Goldbacks as well—my teenager self back then would have thought they were bitchin’ rad, as well as being a tangible asset.

So, kids, just remember: the buying power you think you have today will not be the same “tomorrow”. Plan for decades down the road now, whilst you have the compounding interest time to do so.

You can’t wait & think this is something old people worry about.

The old people that didn’t start early enough are the worrying olds—don’t be one of them when it’s your turn.

@ZubyMusic

14

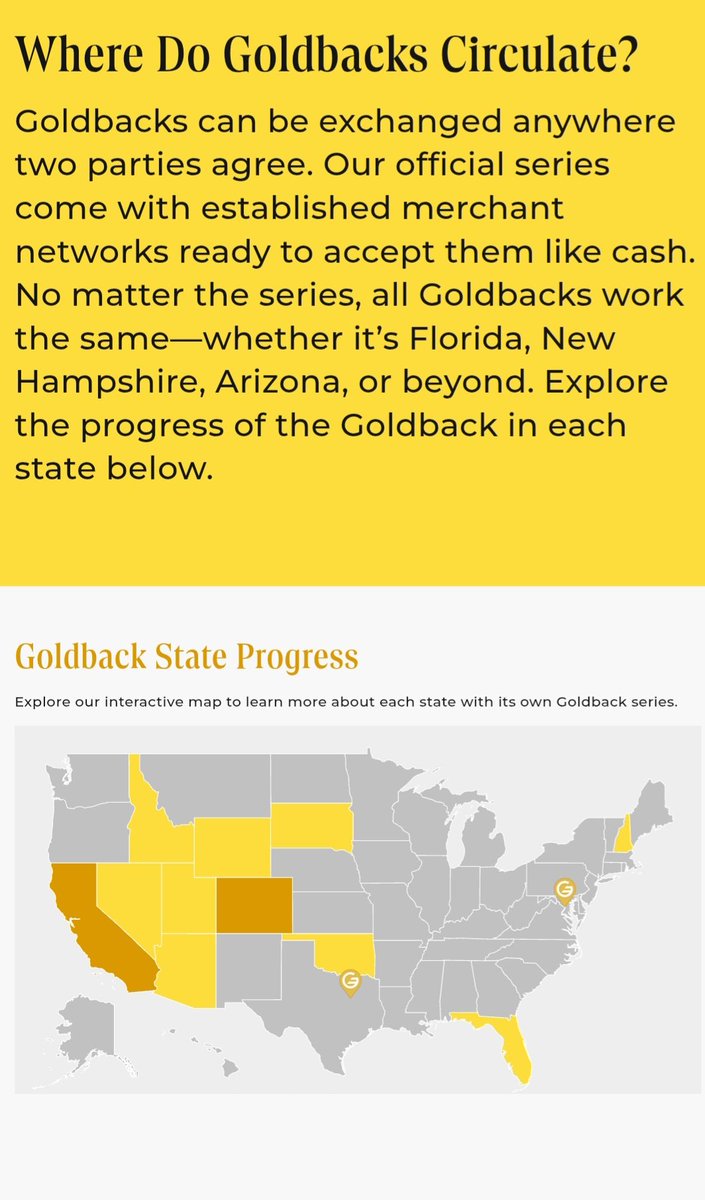

Hello Megan on the goldbacks website there is a map and Nevada is included

11

I owe the people on the r/Gold subreddit a huge apology over Goldbacks. Here is a list of everything wrong with Goldbacks.

8

376

Jun 15

39

Jun 12

Outstanding presentation. Thank you!

Hopefully, Goldbacks will be accepted worldwide soon. Gold is real money.

1

2

16

Jun 12

🫡🦅 Build Parallel society while fighting.

Use cash or Goldbacks 💪🏻😃👍🏻

Garden 🌱 👩🏻🌾🌳🌻🏵️🍇🥦🌽🍊

May 28

If they insist on pushing us out, we must build another way, think Amish & Goldbacks, we buy & sell only/mainly amongst ourselves, get making lots of beautiful babies 👶🏻 & bear one another's burdens joyfully as we build up our parallel society from scratch

226

Jun 12

Goldbacks have a built in anti counterfeiting system just like the dollar bill, and you can always melt it down to make sure it's real.

1

3

23

Jun 12

🚨 We're LIVE on eBay starting at 12PM EST! 🚨

Join Beantown Coins for our HUGE all-day auction, running into the evening!

🔥 US Coins

🌎 World Coins

🏛️ Ancient Coins

💵 Paper Money

🪙 Silver

🏔️ Goldbacks

📦 FREE SHIPPING

Whether you're a seasoned collector or just getting started, we've got something for everyone. Expect great deals, fresh inventory, and plenty of surprises throughout the day!

📍 ebay.com/ebaylive/events/Xtg…

#eBayLive #CoinAuction #RareCoins #CoinCollecting #Numismatics

1

1

12

Jun 11

Some advice and caution. Goldbacks are ONLY good in States registered for Goldbacks. Do not buy them. You’re throwing money away in high premiums with nothing in return.

15

Jun 11

Goldbacks aren’t worth shit in California. Get your head together. There’s only a few states accepting Goldbacks. Nobody wants them. I wasted my money. There’s no return like coins and bullion. Don’t buy them. You’re wasting money on high premiums.

2

1

23

Jun 11

What's the diff between live gold prices and the 1/1000th oz content?

I wouldn't mind, but with gold so high, there's no way I'm parting with my goldbacks. I almost filled out your offer to buy back my notes. So close.

1

26

Jun 11

Cancelation of debt through inflation. Then replace with a new state and federal metals backed script like the Utah goldbacks.

Imagine how expensive everything will get if tomorrow everyone got a million bucks. In a month the treasury dollar as we know it would devalue by half

69