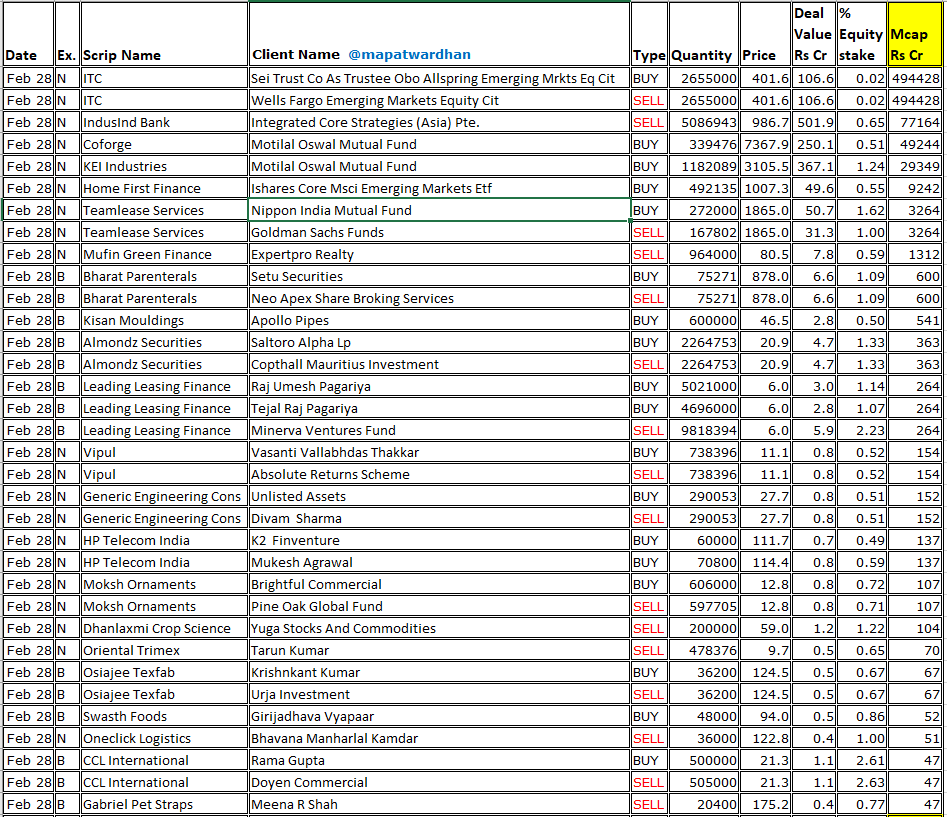

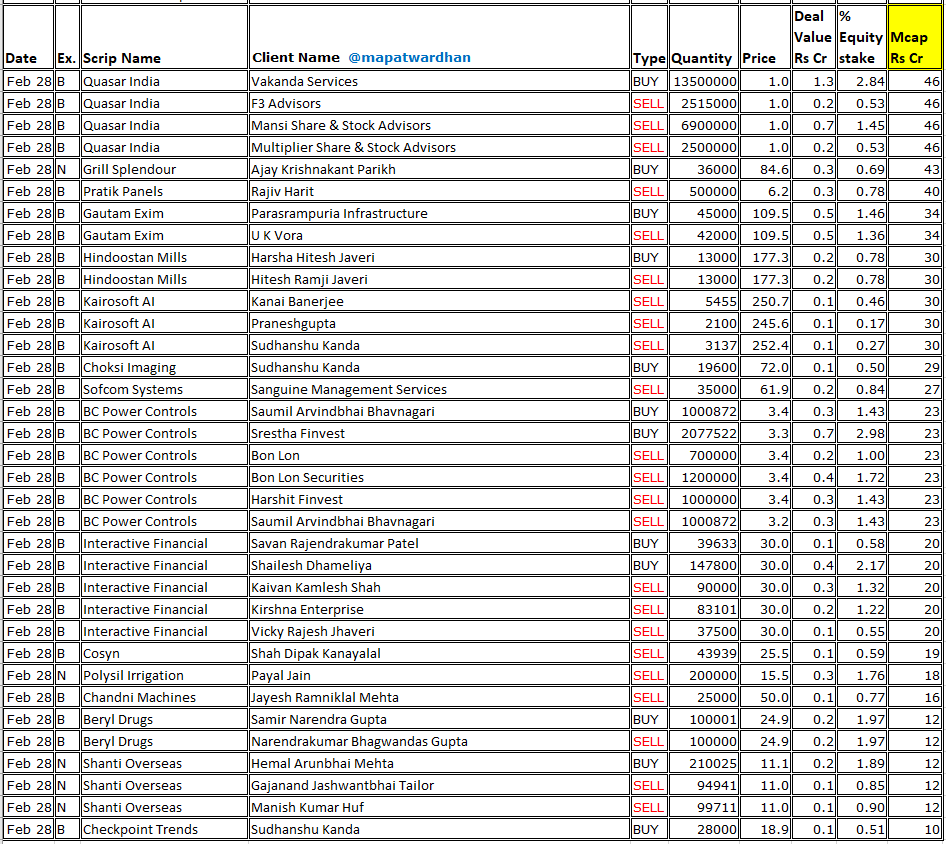

28 Feb 2025

*Today's bulk / block deals*

#ITC #IndusIndBank #Coforge #KEIInds #HomeFirstFinance #Teamlease #MufinGreenFinance #BharatParenterals #KisanMouldings #AlmondzSecurities #LeadingLeasingFinance #Vipul #GenericEngineering #HPTelecom #MokshOrnaments #DhanlaxmiCropScience #QuasarIndia

2

1

13

1,992

24 Feb 2025

HP Telecom India IPO Alert!

Check latest subscription status, GMP of HP Telecom India IPO.

Is the public issue over-subscribed or under-subscribed on Day 3.

Check allotment details and price band of the IPO

moneydaily.in/hp-telecom-ind…

#ipoallotment #HPtelecom #gmp #IPO

2

87

24 Feb 2025

Today ( 24 - 02 - 25 ) , 2 SME IPOs are closing -

I am avoiding both SME IPOs as the chances of listing gains are very low.

The analysis is available on my X account, and you can check it out using this link -

Swasth Foodtec India Limited -

x.com/Ashishkafunda/status/1…

HP Telecom India Limited -

x.com/Ashishkafunda/status/1…

I am Not Sebi Registered ...Views are Personal . DYDD

#Swasth

#Hptelecom #Smeipo #Ipaalert

20 Feb 2025

Swasth Foodtech India Limited ( BSE SME IPO ) Analysis -

IPO Details -

IPO Date: 20 - 24 Feb 2025

Issue Price: ₹94 ( Fixed Price )

Lot Size: 1,200 Shares

Face Value: ₹10

IPO Size: ₹14.92 Crores ( Full Fresh )

Lead Manager: Horizon Management Private Ltd

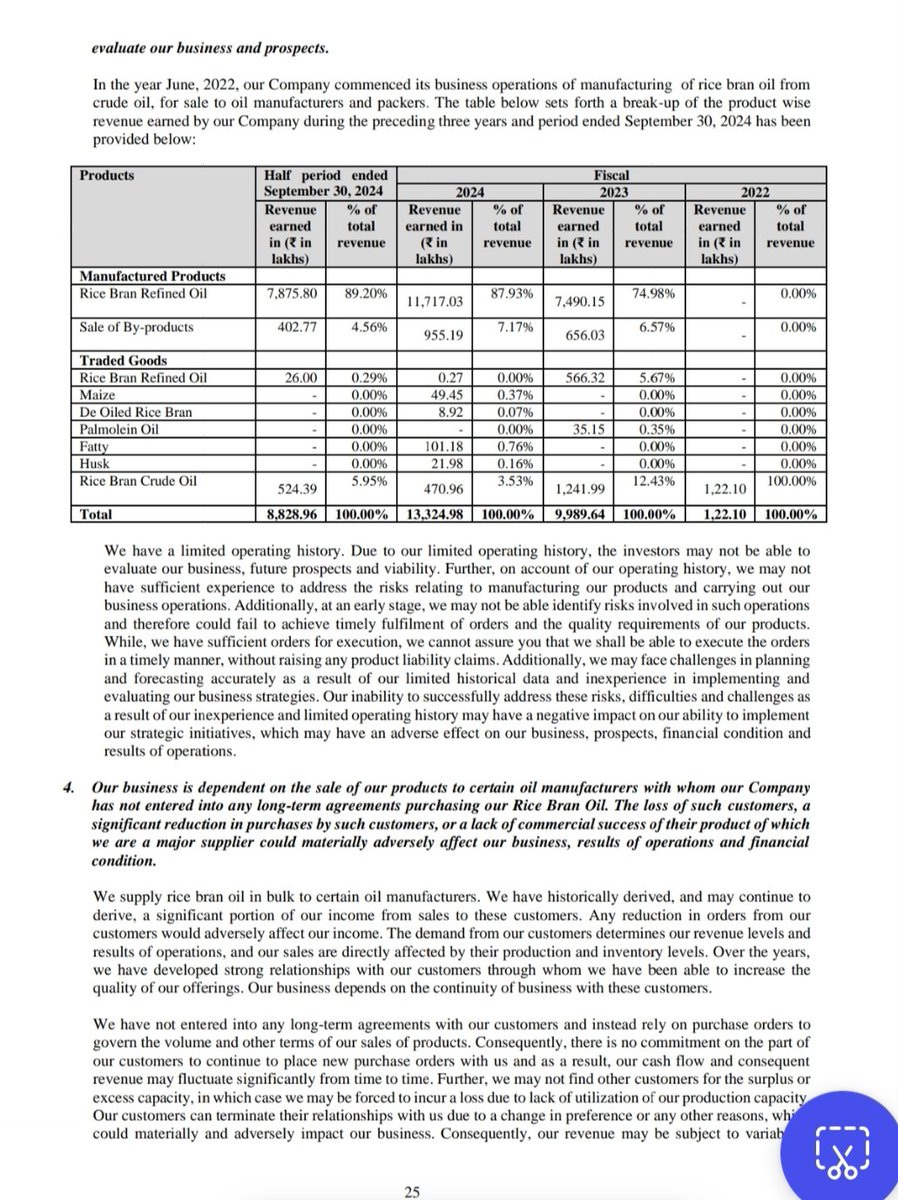

1. Business Overview -

Core Business Activity -

The company processes edible rice bran oil from crude oil.

Supplies to edible oil manufacturers and packers.

Business Model -

Generates revenue from -

Primary Product: Rice Bran Refined Oil.

By-products: Fatty acids, gums, spent earth, wax.

Proposed Use of IPO Funds -

Packing Line Setup – ₹3.29 Crores

Working Capital – ₹7.5 Crores

General Corporate Purposes – ₹2.2 Crores

2. Financial Overview -

Net Worth -

H1FY25: ₹8.07 Crores

FY24: ₹6.24 Crores

FY23: ₹3.03 Crores

Revenue from Operations -

H1FY25: ₹88.29 Crores

FY24: ₹133.25 Crores

FY23: ₹99.90 Crores

Profit After Tax ( PAT ) ( Crore ) -

H1FY25: ₹1.83 ( Margin - 2.07% )

FY24: ₹1.93 ( Margin - 1.44% )

FY23: ₹0.03 ( Margin - 0.03% )

Earnings Per Share ( EPS ) -

H1FY25: ₹4.28

FY24: ₹5.03

FY23: ₹0.09

Net Asset Value ( NAV ) per Share -

H1FY25: ₹18.90

FY24: ₹14.62

FY23: ₹10.13

Debt & Borrowings -

H1FY25: ₹23.60 Crores

FY24: ₹23.39 Crores

FY23: ₹23.82 Crores

Return on Net Worth ( RONW ) -

H1FY25: 22.67%

FY24: 30.97%

FY23: 0.89%

Debt-Equity Ratio -

H1FY25: 2.92

FY24: 3.75

FY23: 7.87

Pros / Strengths -

Growth in Revenue & Profitability -

Revenue increased from ₹99.90 Crores ( FY23 ) to ₹133.25 Crores ( FY24 ).

PAT increased from ₹0.03 Crores ( FY23 ) to ₹1.93 Crores ( FY24 ).

Reasonable Valuation -

P/E Ratio post-IPO is around 15.05x, making it fairly priced.

Improvement in Debt-Equity Ratio -

Reduced from 7.87 ( FY23 ) to 2.92 ( H1FY25 ), indicating better financial management.

Positive Cash Flow from Operating Activities ( Recent Years ) -

H1FY25: ₹43.80 Lakhs

FY24: ₹36.08 Lakhs

Cons / Weaknesses & Risks -

Revenue Concentration Risk -

92% revenue from just 4 states ( H1FY24 ) -

#West Bengal: ₹44.55 Cr ( 50.46% )

#Rajasthan: ₹17.24 Cr ( 19.53% )

#UttarPradesh: ₹11.75 Cr ( 13.31% )

#Bihar: ₹8.69 Cr ( 9.85% )

High dependency on key customers -

Top 10 customers contribute 61.33% of revenue.

Top 3 customers alone contribute 35% of revenue.

Major Customer Dependence -

Vijay Solvex Limited: ₹16 Cr ( 18.52% )

Gokul Agri International Limited: ₹11.58 Cr ( 13.13% )

Shree Narsingh Udyog: ₹4.72 Cr ( 5.35% )

If any major customer stops buying, the company may face huge losses.

History of Negative Cash Flow -

FY23: Significant negative cash flow ( -₹12.27 Crores ).

Commodity Price Risk - Rice bran oil is a commodity product, subject to price fluctuations due to:

Global supply & demand changes.

Raw material price variations.

Weather & crop yield impacts.

Government policies & trade disputes.

High Debt Levels -

Debt-Equity Ratio: 2.92 ( H1FY25 ), though improving, still high.

Total Borrowings: ₹23.60 Crores.

Limited Workforce - Only 17 employees managing the entire business.

Single-Product Dependency -

Manufactured Rice Bran Oil contributes 89.20% of revenue ( H1FY25 ).

Highly vulnerable to competition in the edible oil market.

Conclusion -

Ideal for High-Risk Investors - If you are comfortable with sector risks, customer concentration risks, and debt levels, this IPO might be worth considering due to its reasonable valuation and revenue growth.

❌ Avoid if You Prefer Stability - The company depends too much on a few customers & regions, faces commodity price risks, and has high debt.

Edible oil is a highly competitive industry, making long-term sustainability uncertain.

High-risk, high-reward IPO – suitable for investors with risk appetite but not for conservative investors.

I am Not Sebi Registered ...Views are Personal . DYDD

Apply Or Avoid Final Decision Upto 24 Feb ,,, 2 P.M

#Swasth #Edibleoil #Smeipo #Ipaalert

4

554