From lab to factory. The twenty-year journey to recycle rare earth magnets

BBC Midlands Today video report from 3 February 2026, covering the opening of HyProMag's Birmingham commercial plant

🧲 Twenty years. One Birmingham lab. Now the UK's first rare earth magnet factory in 25 years is open — and it runs on hydrogen.

The BBC just covered HyProMag's commercial plant opening in Birmingham and it's one of the most important UK manufacturing stories of 2026. Here's why it matters. 🧵

⚗️ THE SCIENCE — hydrogen does what shredders can't [1/5]

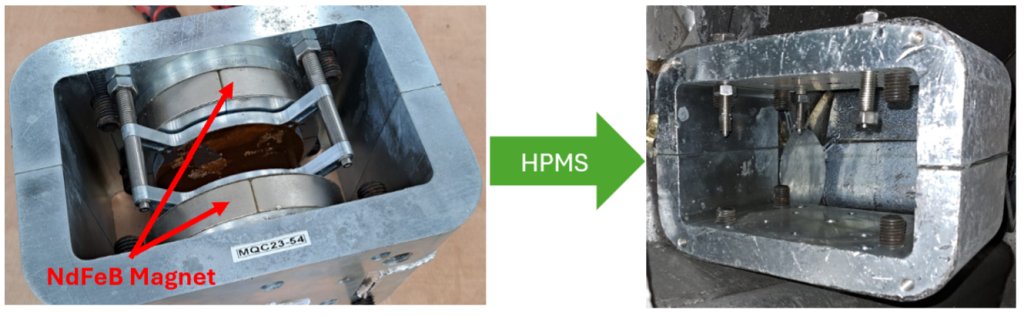

Here's the problem with recycling rare earth magnets the old way. You shred the product — the magnets pop out and stick to the shredder. The rare earths are lost forever into iron slag.

HyProMag's solution? Expose the magnet to hydrogen gas.

The magnet absorbs the hydrogen, the grain boundaries crack, and the whole thing disintegrates into a fine demagnetised powder — still in alloy form, ready to be pressed back into new magnets.

No acid. No smelter. No China.

That's HPMS — Hydrogen Processing of Magnet Scrap — 20 years in the making at the University of Birmingham. 🎓

🏭 THE MILESTONE — UK's first magnet production in 25 years [2/5]

The Birmingham plant is producing:

Up to 2 tonnes of recycled NdFeB powder per day at this scale

At just 10% of the energy cost of making brand new magnets from virgin rare earths

Powder that is pressed, heated and reformed directly into new sintered magnets — no separation required

Opened by a UK government minister — reflecting strategic national importance 🇬🇧

Prof. Allan Walton (University of Birmingham, HyProMag co-founder):

"We followed this idea for more than 10 years. 40–50 people developed this facility."

This isn't a lab. This is a commercial factory. Running. In the Midlands. Today.

🔗 THE CHAIN — HPMS powder flows straight back into magnets [3/5]

This is what makes HyProMag's short-loop process so powerful. Most recyclers dissolve everything down to oxides. HyProMag keeps the material as alloy powder throughout — skipping the most expensive and energy-intensive steps entirely:

♻️ Scrap EV motors / HDDs / wind turbines

⬇️ HPMS hydrogen process → demagnetised NdFeB alloy powder

⬇️ Press sinter → new high-performance magnets

No acid leaching. No solvent extraction. No rare earth oxide refining.

Result: 25% more output than primary production, 90% energy savings. ⚡

Partners feeding the chain: EMR Group (scrap supply), LCM (melt route alloys), Adey, Jaguar Land Rover, University of Birmingham — and multiple DRIVE35 / Innovate UK funded projects including REACT UK, SCREAM and REEmelt.

THE FUNDING & SCALE [4/5]

HyProMag isn't early-stage anymore. This is a company with:

🇬🇧 Multiple Innovate UK / APC / DRIVE35 grants

🇺🇸 HyProMag USA — scale-up in South Carolina Texas via CoTec/Mkango JV

🎯 US target: 10 facilities, 15,000 tpa within a decade

🔬 TRL 8–9 — demonstrated, commissioned, operating commercially

📋 REACT UK — £6.5m DRIVE35 project just announced April 2026 with JLR, EMR, LCM, University of Birmingham

🧲 SCREAM — UK short medium loop magnet recycling pilot

🌍 Mkango Resources (TSXV/AIM: MKA) — parent company with Malawi rare earth project feeding long-term HREE supply

🌍 THE BIG PICTURE — The West needs this [5/5]

The BBC reporter puts it plainly:

"Almost all of these magnets come from China. And that dependence makes politicians a bit twitchy."

80–90% of rare earth metals sourced from a single country. China banned export of magnet manufacturing technology in Dec 2023. US 25% tariffs on Chinese magnets hit in 2026.

HyProMag's Birmingham plant is the West's answer:

✅ Commercially operating — not a pilot

✅ UK-sovereign, China-free magnet production

✅ Replicable anywhere there is scrap — EVs, HDDs, wind, defence

✅ 20 years of University of Birmingham IP at its core

✅ Government minister opened the doors 🇬🇧

"From an idea in a lab to commercial rare earth magnets made in the Midlands." — BBC Midlands Today, Feb 2026

This is what the energy transition actually looks like. ⚡🧲

#HyProMag #RareEarths #MagnetRecycling @MkangoResources #NdFeB #CircularEconomy #UKManufacturing #Birmingham #HPMS #HydrogenProcessing #EVSupplyChain #WindEnergy #DefenceSupplyChain #ChinaSupplyChain #EnergyTransition #NetZero #InnovateUK #DRIVE35 #UniversityOfBirmingham @roblun1

1

12

52

8,227

Thanks for the positive feedback! You raise a valid point — and there is now peer-reviewed evidence from the University of Birmingham to support exactly this.

Published July 2025, "Tailoring magnetic properties of short-loop recycled NdFeB magnets" (University of Birmingham, research.birmingham.ac.uk) demonstrates precisely what you describe:

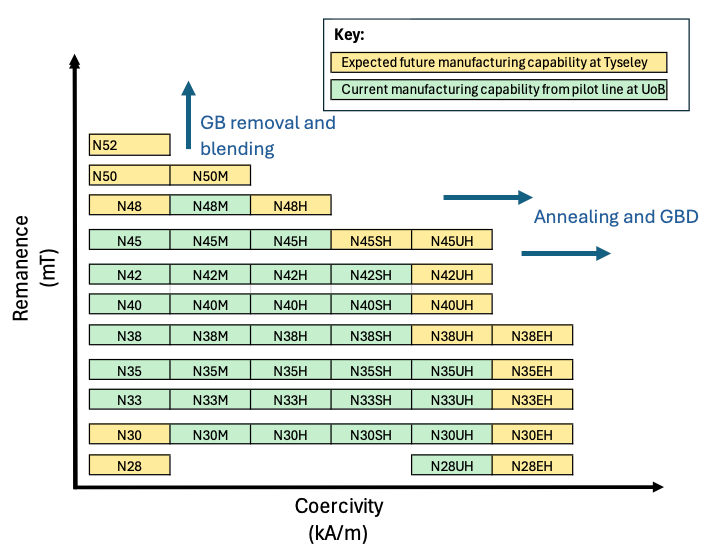

Two distinct recycled HPMS scrap feeds of different nominal compositions were processed, jet-milled and blended in varying ratios. Results showed:

✅ Material A alone: Br 1.23T | HcJ 1,136 kA/m | (BH)max 295 kJ/m³

✅ Material B alone: Br 1.14T | HcJ 2,254 kA/m | (BH)max 256 kJ/m³

✅ Blending A B: coercivity tunable continuously between those values by adjusting blend ratio

The paper confirms: "Blending recycled HPMS powders of different compositions unlocks the ability to alter the composition of the final magnet by varying the addition of a second recycled powder or blending with virgin material."

HyProMag's own June 2025 Technical Bulletin (hypromag.com) also confirms: "It is possible to substantially change the grade of the magnets compared to the starting magnets by blending with different scrap feeds, with rare earth elements, with primary strip cast alloys or alloys produced from long loop chemical processing."

A second January 2026 University of Birmingham study adds another dimension — a new spiral jet mill process separates the HPMS powder into a coarse low-oxygen, high-performance fraction and a fine oxygen-rich fraction, achieving coercivity of 1,466 kA/m — actually better than the original scrap input.

So you are correct — this is not a fundamental barrier. The science is solid, peer-reviewed and improving rapidly. 🎯

Sources:

🔬 research.birmingham.ac.uk — "Tailoring magnetic properties of short-loop recycled NdFeB magnets" (July 2025)

🔬 hypromag.com — Technical Bulletin June 2025

🔬 Rare Earth Exchanges — "From Scrap to Strategic Asset" (January 2026)

hypromag.com/executive-summa…

research.birmingham.ac.uk/en…

#HyProMag #HPMS #HydrogenProcessing #RareEarths #NdFeB #MagnetRecycling #CriticalMinerals #ShortLoop #CircularEconomy #CleanTech #EVs #WindEnergy #DefenceSupplyChain #UKManufacturing #MadeInBritain #GreenSteel #Tyseley #Birmingham

1

1

8

673

This infographic contains a lot of ground — so we've split it across three images for clarity and easier reading. Swipe through all three to get the full HyProMag story. 🧵👇

#HyProMag #HPMS #HydrogenProcessing #RareEarths #NdFeB #MagnetRecycling #CriticalMinerals #ShortLoop #CircularEconomy #CleanTech #EVs #WindEnergy #DefenceSupplyChain

1

6

330

📚 Part of a Bigger Series

x.com/roblun1/status/2033432…

This HyProMag breakdown is part of my ongoing series on the new magnet‑recycling and separation ecosystem — covering how different technologies and business models stack up across Ionic Technologies, Cyclic Materials, REEcycle, ReElement, Ucore, and HyProMag, comparing product purity, processing routes, scalability, and where each fits in the emerging circular magnet supply chain.

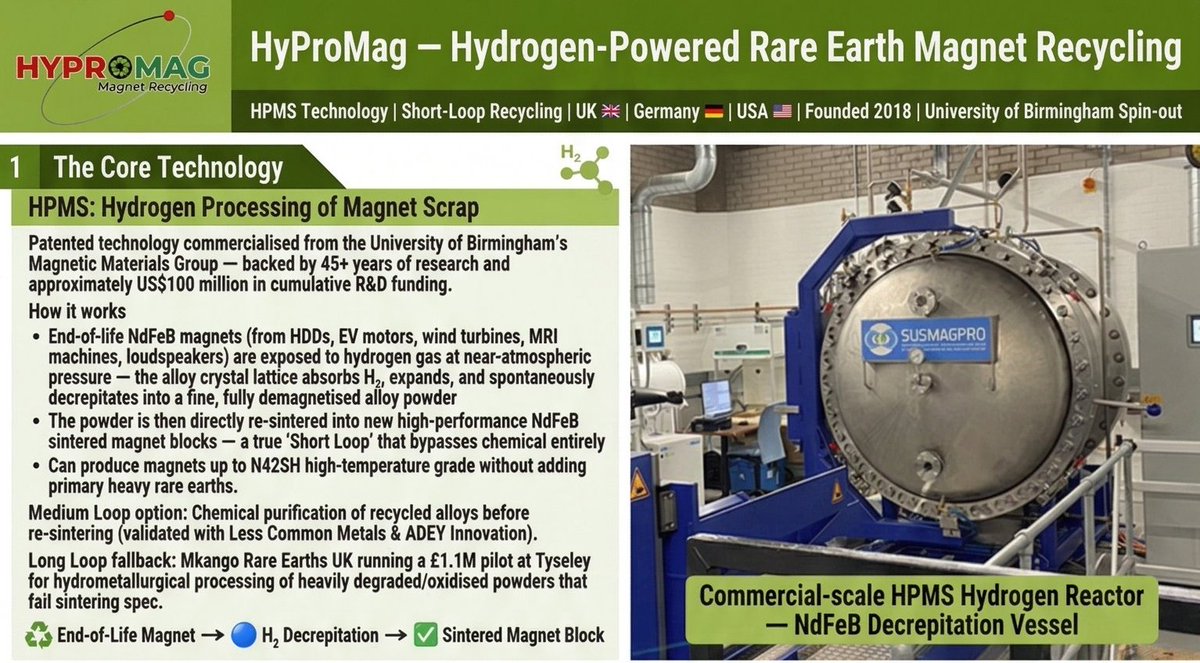

🧲 HyProMag — The World's Most Carbon-Efficient Rare Earth Magnet Recycler

While most recyclers dissolve magnets into chemicals and start again from scratch, HyProMag does something fundamentally different. Their patented Hydrogen Processing of Magnet Scrap (HPMS) technology — commercialised from 45 years of research at the University of Birmingham and backed by ~US$100M in cumulative R&D — simply exposes end-of-life NdFeB magnets to hydrogen gas at near-atmospheric pressure.

The alloy crystal lattice absorbs H₂, expands, and spontaneously decrepitates into a fine, fully demagnetised alloy powder in minutes. That powder is then pressed and re-sintered directly into brand new, high-performance NdFeB sintered magnet blocks — no acid baths, no toxic solvents, no smelting, no chemical destruction of the alloy. This is the "Short Loop" — and it is the cleanest, most energy-efficient pathway in the entire magnet recycling landscape.

HPMS is batch-based, which means every reactor run can produce powder with slightly different specifications depending on what went in. This is the key difference from continuous processors like Ionic Technologies, ReElements, Ucore and CyclicMaterials. It doesn't make the output unusable — but it does mean HyProMag's customers need robust incoming QC protocols and flexible sintering process parameters to accommodate batch-to-batch variation.

🏛️ The UK Government Is Quietly Subsidising HyProMag's Operating Costs

Two policy mechanisms most investors have missed:

⚡ British Industrial Competitiveness Scheme — reduces electricity prices by up to £40 per MWh from 2027

⚡ Network Charging Compensation Scheme — electricity relief increases from 60% → 90% by 2026

For a facility running hydrogen reactors, pressing lines and sintering furnaces 24/7, these subsidies are a direct, recurring reduction in Tyseley's OPEX — strengthening UK unit economics every single year from 2026 onward.

👨🔬 The Inventor — Professor Allan Walton

The man behind HPMS deserves his own moment. Professor Allan Walton, Professor of Critical and Magnetic Materials at the University of Birmingham and Co-Director of the Birmingham Centre for Strategic Elements and Critical Materials, has led the Magnetic Materials Group since 2011 — the only research group in the UK exclusively dedicated to the processing and recycling of permanent rare earth magnetic materials.

The technology he and his colleagues built rests on 45 years of continuous University of Birmingham research and approximately US$100 million in cumulative R&D funding — with the original HPMS concept co-developed alongside the late Professor Emeritus Rex Harris, former Head of the Magnetic Materials Group, and Honorary Fellows Dr. John Speight and Mr. David Kennedy.

Under Professor Walton's stewardship, more than £2.4 million in dedicated sustainable manufacturing research has been directly supervised, producing the postgraduate talent — including doctoral researchers Malik Degri (recycled sintered magnet characterisation) and Alec Durrant (microstructural processing) — who now form the scientific backbone of the Tyseley commercial operation.

This is not a startup that licensed a university patent and moved on. The inventors are still in the building, still publishing, still improving the process and that continuity of deep domain expertise is a structural moat that no amount of capital can quickly replicate🔬

♻️ Short Loop. Massive Impact.

The numbers are stark:

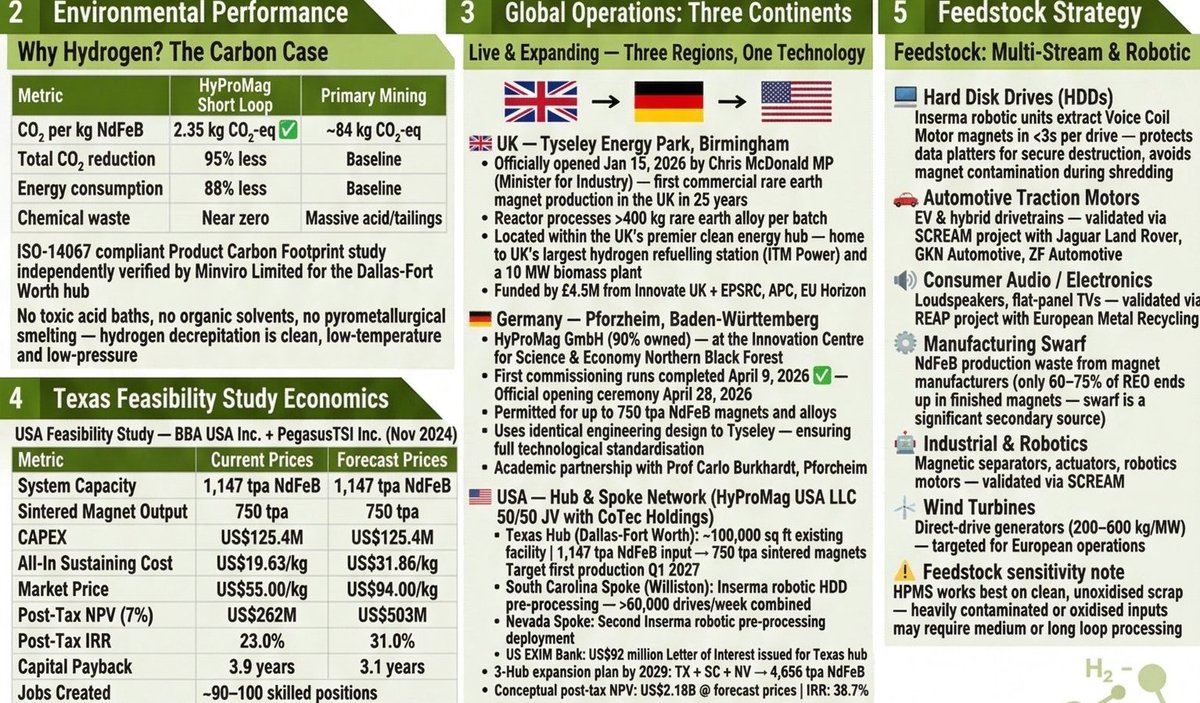

🌍 95% less CO₂ vs primary mining — just 2.35 kg CO₂-eq per kg of sintered magnet vs ~84 kg for virgin production (ISO-14067 verified by Minviro)

⚡ 88% less energy than the mine-to-magnet primary pathway

🚫 Zero acid waste | Zero organic solvents | Near-zero chemical footprint

✅ Can produce up to N42SH high-temperature grade magnets without adding primary heavy rare earths

🏭 Three Continents. Three Facilities. Right Now.

🇬🇧 Birmingham, UK — Tyseley Energy Park

Officially opened January 15, 2026 by the UK Minister for Industry

▪ First commercial rare earth magnet production in the UK in 25 years

▪ Nation's only commercial-scale sintered magnet plant

▪ 100 tpa single-shift → 300 tpa multi-shift capacity

▪ Reactor processes >400 kg rare earth alloy per batch

▪ Funded by £4.5M Innovate UK EPSRC Advanced Propulsion Centre EU Horizon.

🇩🇪 Pforzheim, Germany — HyProMag GmbH (90% owned)

▪ First commissioning runs completed April 9, 2026 ✅

▪ Official opening ceremony: April 28, 2026 🎉

▪ Permitted for up to 750 tpa NdFeB magnets and alloys

▪ Identical engineering design to Tyseley — full tech standardisation

▪ Academic partnership with Pforzheim University

🇺🇸 USA — HyProMag USA LLC (50/50 JV with CoTec Holdings, TSXV) Hub & Spoke network across three states:

▪ Texas Hub (Dallas-Fort Worth): ~100,000 sq ft | 1,147 tpa NdFeB input → 750 tpa sintered magnets | First production target Q1 2027

▪ South Carolina Spoke (Williston): Inserma robotic HDD pre-processing — <3 seconds per drive | >60,000 drives/week

▪ Nevada Spoke: Second Inserma robotic pre-processing deployment

▪ US EXIM Bank: US$92M Letter of Interest issued for Texas hub

💰 HyProMag USA — Texas Hub Economics

*(BBA USA Inc. PegasusTSI Inc. Feasibility Study)*

⚙️ Output: 750 tpa sintered NdFeB magnets

🏗️ CAPEX: US$125.4M

💵 All-In Cost: US$19.63/kg vs market US$55/kg

📈 Post-Tax NPV: US$262M → US$503M (forecast)

🔄 IRR: 23% → 31%

⏱️ Payback: under 4 years

🚀 3-Hub Expansion by 2029 (TX SC NV)

▪ 4,656 tpa NdFeB capacity

▪ Conceptual NPV: US$2.18B

▪ IRR: 38.7% at forecast prices

▪ Targeting 10–25% of total US NdFeB demand

🌐 hypromag.com | $MKA $CTH

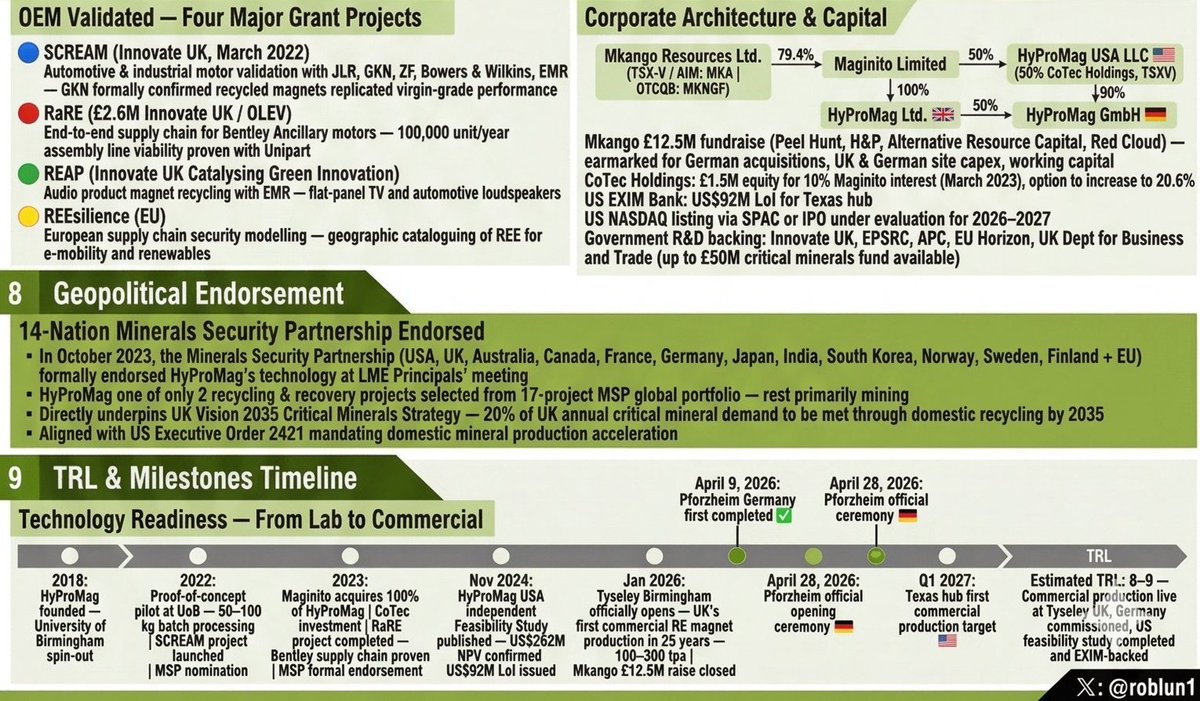

🤝 OEM Validated — Four Major R&D Consortia

🔵 SCREAM (Innovate UK): Automotive validation with Jaguar Land Rover, GKN Automotive, ZF Automotive, Bowers & Wilkins — GKN formally confirmed recycled magnets replicated virgin-grade motor performance

🔴 RaRE (£2.6M Innovate UK/OLEV): End-to-end supply chain for Bentley Motors ancillary motors — 100,000 unit/year assembly line viability proven with Unipart

🟢 REAP (Innovate UK): Consumer audio recycling with European Metal Recycling — flat-panel TVs and automotive loudspeakers

🟡 REEsilience (EU): European e-mobility supply chain security modelling

🏗️ Feedstock: Multi-Stream & Robotic

🖥️ Hard disk drives (HDD Voice Coil Motors — <3 sec/drive robotic extraction)

🚗 EV & hybrid traction motors

🔊 Consumer audio, flat-panel TVs

⚙️ NdFeB manufacturing swarf (only 60–75% of REO ends up in finished magnets — swarf is enormous)

🤖 Industrial robotics & actuators

🌬️ Wind turbine generators

🏛️ Corporate Structure

textMkango Resources (TSX-V/AIM: MKA)

└── 79.4% → Maginito Limited

├── 100% → HyProMag Ltd. 🇬🇧

├── 90% → HyProMag GmbH 🇩🇪

└── 50% → HyProMag USA LLC 🇺🇸

(50% CoTec Holdings, TSXV)

▪ Mkango £12.5M raise closed (Peel Hunt, H&P Advisory, Alternative Resource Capital, Red Cloud Securities) — funding German acquisitions, UK/DE capex, working capital

▪ US NASDAQ listing via SPAC or IPO under evaluation for 2026–2027

🌐 Geopolitical Endorsement

▪ 14-Nation Minerals Security Partnership (USA, UK, AU, CA, FR, DE, JP, IN, KR EU) formally endorsed HyProMag at the London Metals Exchange, October 2023

▪ One of only 2 recycling projects selected from the entire 17-project MSP global portfolio

▪ Directly underpins UK Vision 2035 — 20% of UK critical mineral demand from domestic recycling by 2035

▪ Aligned with US Executive Order 2421 — domestic mineral acceleration mandate

▪ UK Dept. for Business & Trade: up to £50M in critical minerals project funding available

📅 TRL & Milestones — TRL 8–9

✅ 2018 — Founded, University of Birmingham spin-out

✅ 2022 — Pilot: 50–100 kg batch processing proved | MSP nomination

✅ 2023 — Maginito acquires 100% HyProMag | Bentley supply chain proven | MSP formally endorsed

✅ Nov 2024 — US Feasibility Study: US$262M NPV confirmed | EXIM Bank US$92M LoI

✅ Jan 2026 — Tyseley Birmingham opens — UK's first commercial magnet production in 25 years

✅ April 9, 2026 — Pforzheim commissioning runs completed 🇩🇪

🔜 April 28, 2026 — Pforzheim official opening 🎉

🔜 Q1 2027/28 — Texas first commercial production 🇺🇸

🔜 2029 — 3-Hub USA: 4,656 tpa NdFeB

⚠️ The Honest Feedstock & Quality Caveat

HyProMag's HPMS technology is only as good as what goes into it — and that is both its greatest strength and its most important constraint.

⚠️ HyProMag Feedstock — The Real Talk

🔬 Quality in = Quality out

HPMS preserves the alloy — so the recycled powder inherits the exact chemistry of the input scrap

✅ Clean, unoxidised NdFeB in → High-grade sintered magnet out

⚠️ Degraded, oxidised or contaminated scrap → rerouted to Medium or Long Loop — slower & costlier

The Short Loop process works by preserving the original NdFeB alloy chemistry, which means the recycled powder will inherit the exact chemical composition of the input scrap — no more, no less. Feed it a high-grade, clean, unoxidised N42SH magnet and you get a high-grade powder back. Feed it degraded, heavily oxidised, or contaminated scrap and the output quality degrades accordingly, often requiring rerouting to the slower and more expensive Medium or Long Loop pathways instead. This is not a flaw unique to HyProMag — it is the fundamental thermodynamic reality of short-loop recycling.

🛡️ HyProMag's Answer: 3-Loop Architecture

♻️ Short Loop — clean scrap → direct re-sinter

🔄 Medium Loop — borderline material → chemical purification (with Less Common Metals ADEY Innovation)

🧪 Long Loop — heavily degraded powder → Mkango's £1.1M hydromet pilot at Tyseley

The company has been transparent about it, building a three-loop fallback architecture precisely to handle every grade of input: Short Loop for clean scrap, Medium Loop (with Less Common Metals and ADEY Innovation) for chemically borderline material, and Mkango's £1.1M Long Loop pilot at Tyseley for heavily degraded powders

📦 Feedstock Volume — Near Term vs Long Term

⚠️ HyProMag Feedstock.

On feedstock volume, the near-term pipeline is well-supported — HDDs, manufacturing swarf, consumer audio, and some early EV motors are already flowing. However, the big feedstock wave — the one that justifies 4,656 tpa US expansion by 2029 — depends critically on EV traction motors reaching end-of-life at scale.

The first mass-market EVs sold from 2017 to 2020 will not broadly hit the recycling stream until the late 2020s, meaning the Texas hub's ramp to full capacity is structurally tied to how quickly the EV fleet turns over. That is not a crisis — it is a sequencing reality — but investors and followers should understand that feedstock volume for the larger hubs grows with the EV scrappage curve, not ahead of it.

Now (well supplied):

🖥️ HDDs — robotic Inserma extraction, >60,000 drives/week

⚙️ Manufacturing swarf

🔊 Consumer audio / flat-panel TVs

🚗 Early EV & hybrid motors

The Big Ramp (timing-dependent):

🌊 Mass EV traction motor scrappage wave

— first mass-market EVs (2017–2020 vintage) won't broadly hit recycling until late 2020s

— 4,656 tpa US expansion by 2029 depends on EV fleet turnover accelerating

📌 Bottom Line

This isn't a crisis — it's a sequencing reality

HyProMag's feedstock ramp grows with the EV scrappage curve, not ahead of it, Near-term volumes are solid, The big numbers require the EV wave to arrive on schedule 🌊

🌐 hypromag.com

Mkango: $MKA | CoTec: $CTH

#HyProMag #HPMS #HydrogenProcessing #RareEarths #NdFeB #MagnetRecycling #CriticalMinerals #ShortLoop #CircularEconomy #CleanTech #EVs #WindEnergy #DefenceSupplyChain #UKManufacturing #MadeInBritain #GreenSteel #Tyseley #Birmingham #Pforzheim #Texas #CriticalMaterials #SupplyChainResilience #Neodymium #Dysprosium #Decarbonisation #MineralsSecurityPartnership #Mkango #CoTec

@roblun1

🧲♻️ Magnet Recycling Spotlight

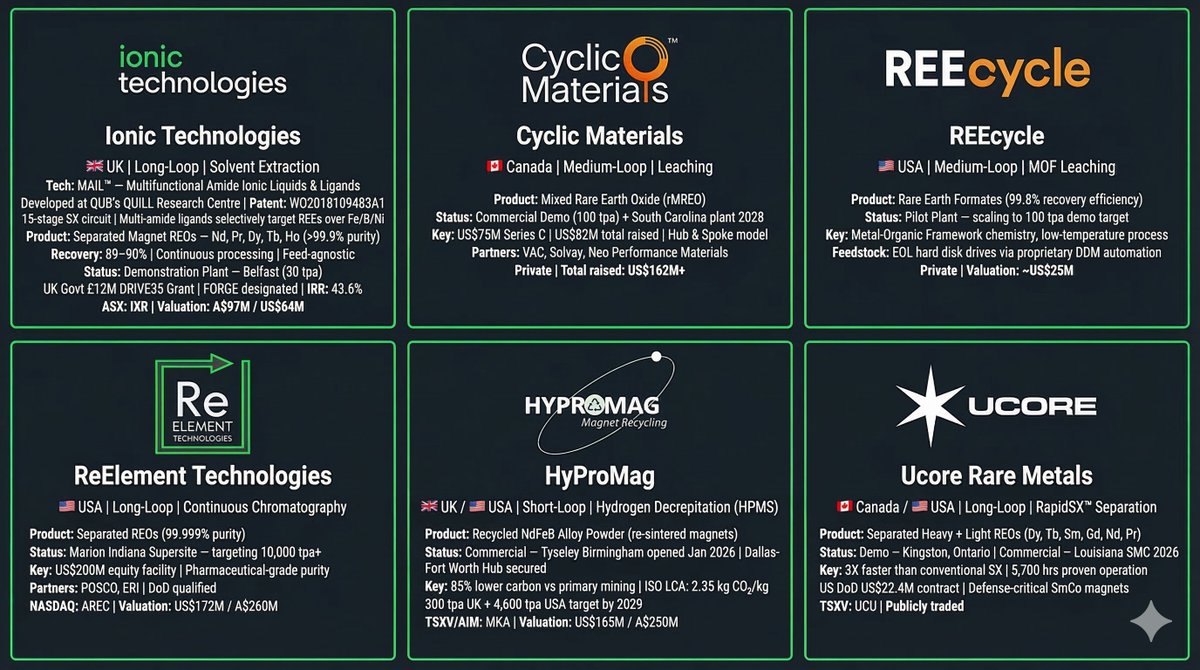

🚀 Over the next few weeks this series will cover different magnet‑recycling technologies and business models across players like, Ionic Technologies, Cyclic Materials, REEcycle, ReElement, Ucore and HyProMag, comparing product purity, processing routes, scalability and where each fits in the emerging circular magnet ecosystem.

🧲 Not all magnet recycling is created equal. These 6 companies represent 6 distinct technology business model combinations — and together they map the entire Western supply chain response to China's rare earth dominance, the 6 pure-play recyclers🧵👇

Tier 1 — Pure-Play Magnet Recyclers (the 6)

Ionic, Cyclic, HyProMag, ReElement, REEcycle, Ucore

→ Magnet recycling IS their entire business model.

Solvay lies in between, accepts recycled feedstock as one input stream among several.

REEtec of Norway sits alongside Solvay, it is building a large-scale separation facility at Herøya funded by LKAB specifically to accept recycled and mined mixed REO feeds and convert them into separated oxides for European magnet makers.

Tier 2 — Integrated Players with Recycling Arms

MP Materials, USA Rare Earth/LCM, Energy Fuels, Carester, Momentum, Geomega, S

→ Recycling is a strategic component within a larger mine-to-magnet or multi-metal business

Tier 3 — Established Asian Incumbents

Shin-Etsu, Proterial, Santoku

→ Commercial at scale for 15 years but within closed Japanese supply chains — the benchmark the West is trying to match

1️⃣ Ionic Technologies 🇬🇧

Long-loop Solvent Extraction using MAIL™ (Multifunctional Amide Ionic Liquids & Ligands)

→ Separated REOs (>99.9% purity) | Continuous processing | Lowest variability | Feed-agnostic

✅ Published LCA

✅ Feasibility Study

✅ UK Govt £12M Grant

✅ FORGE designated

The precision specialist — highest purity, proven IP, ready to license globally

2️⃣ Cyclic Materials 🇨🇦

Medium-loop Leaching (MagCycle REEPure)

→ Mixed Rare Earth Oxide (rMREO) | Hub & spoke model | Real plant operating NOW

✅ US$162M raised

✅ South Carolina plant confirmed (2028)

✅ VAC Solvay offtakes signed

The volume play — feedstock-agnostic, massively funded, scaling fast

3️⃣ REEcycle 🇺🇸

Medium-loop Leaching using Metal-Organic Frameworks (MOFs)

→ Rare Earth Formates | 99.8% recovery efficiency | Low-temperature chemistry

⚠️ Pilot stage | No LCA or feasibility study published | Dependent on downstream separators

The chemistry innovator — compelling science, still proving economics at scale

4️⃣ ReElement Technologies 🇺🇸

Long-loop Continuous Chromatography (pharmaceutical-grade)

→ Separated REOs (99.999% purity) | Marion Indiana Supersite targeting 10,000 tpa

✅ US$200M equity facility

✅ DoD qualified

✅ POSCO ERI feedstock partnerships

The purity champion — highest specification product, aggressive US scaling

NASDAQ: AREC

5️⃣ HyProMag 🇬🇧🇺🇸

Short-loop Hydrogen Decrepitation (HPMS)

→ Recycled NdFeB Alloy Powder | Re-sintered directly into new magnets

✅ Commercial Birmingham plant OPEN Jan 2026 ✅ Dallas-Fort Worth Hub secured

✅ ISO LCA: 85% lower carbon vs primary mining | 4,600 tpa USA target by 2029

The speed champion — shortest loop, lowest carbon, first to commercial in UK

TSXV/AIM: MKA

6️⃣ Ucore Rare Metals 🇨🇦🇺🇸

Long-loop RapidSX™ (Advanced Column Solvent Extraction)

→ Separated Heavy Light REOs (Dy, Tb, Sm, Gd, Nd, Pr) | 3X faster than conventional SX

✅ US$22.4M DoD contract

✅ 5,700 hrs proven operation

✅ Louisiana SMC commercial 2026

The heavy REE specialist — defence-critical SmCo magnets, filling the most acute Western gap

TSXV: UCU

The Western magnet recycling ecosystem is deliberately segmented. End-users — magnet makers, OEMs, and defence primes — will choose based on four dimensions:

🔬 Product spec — Separated oxide (Ionic, ReElement, Ucore) vs mixed oxide (Cyclic, REEcycle) vs alloy powder (HyProMag)

🌍 Geography — Feedstock proximity energy costs geopolitical mandate (US IRA, UK DRIVE35, EU CRM Act)

🌱 Sustainability — LCA proof required by OEMs (Ionic ✅ HyProMag ✅ others pending)

⚡ Scale timing — Who can deliver volume WHEN the EV and wind ramp demands it (2026–2030 critical window)

The US government is deliberately not picking one winner — it is funding across all three loops:

🔬 Long-loop separated REO → Ucore (DoD, US$22.4M), USA Rare Earth (Commerce, US$1.6B LOI)

🧪 Medium-loop recycling → REEcycle (DoD DPA Title III, US$5.1M)

🏭 Full supply chain → DOE US$134M open program US$1B broader critical minerals

The Demand Explosion

Adamas forecasts the global magnet rare earth oxide market will increase more than 7-fold by 2040, from US$9.7 billion today.

Critically, they project approximately US$7.3 billion worth of magnet REO demand will go completely unsatisfied by 2040 if supply doesn't grow beyond their base case — driven specifically by Dy, Tb, and NdPr undersupply.

adamasintel.com/global-marke…

@IONIC_RE @IONICTECH_UK @ussmetals @anduriltech @CMA_Minerals @IXR2THAMOON @timhorizonmet @ThalesDefence @northropgrumman @LockheedMartin @BoeingDefense @DeptofWar @DoWCTO @Viridis_VMM @ucore @LCM_Metals @CyclicMaterials

@MPMaterials @ReecycleInc @SolvayGroup @ReElementTech @EMRmetal #VIRIDION @EU_Commission @ENERGY @VulcanElements @RE_Exchanges @DiscoveryAlert @USRareEarths

@DeptofWar #MagnetRecycling #RareEarths #CriticalMinerals #CircularEconomy #SupplyChain #Sustainability #EVs #WindEnergy #NdFeB #IonicTechnologies #CyclicMaterials #HyProMag #ReElement #Ucore #REEcycle #MAIL #GreenTech

5

12

40

4,403

Less than 5 months until #EFCF2023. Will you be joining us? Inspiring talks, international industry & project updates, tutorials, a virtual exhibition, fun networking events and so much more. Register today EFCF.com/Reg #Electrolysers #HydrogenProcessing #CO2Reduction

1

3

123

A week to go until #EFCF2021. Will you be joining us? Inspiring talks, international industry and project updates, tutorials, a virtual exhibition, fun networking events and so much more. Register today EFCF.com/Reg #Electrolysers #HydrogenProcessing #CO2Reduction

7

14 Oct 2019

SUSMAGPRO also draws on the @eranetmin2 MaXycle project, which creates a #circulareconomy for #REE magnets by providing a labelling system, employing #HydrogenProcessing of #MagneticScrap, eliminating residue and facilitating scalability.

Find out more: bit.ly/33mSVPc

3

3

30 Sep 2019

In addition to a great idea, #innovation takes dedication and collaboration. SUSMAGPRO is also made possible thanks to other projects: one is #REMANENCE, funded under FP7, in which the #HydrogenProcessing of #MagneticScrap for #recovery and #recycling of #REE was developed.

27 Mar 2013

#FP7-funded project #REMANENCE aims to increase the amount of #RareEarth materials recovered from #ewaste. project-remanence.eu/

2

3