Jun 14

The copper market needs more operators in the conversation and fewer directional traders. ICSG (International Copper Study Group) puts the 2026 structural deficit at roughly 150,000 tonnes globally, with no major new mine supply filling the gap before 2027. The US tariff-driven import surge is masking a tighter ex-US market — Goldman revised its estimate to a 640,000-tonne ex-US deficit once you strip out pre-tariff positioning inventory. Physical premiums and extended lead times are already telling that story before the next macro catalyst.

15

Jun 14

A copper reversion to $5 from the current ~$6.40 would be a 22% decline — which historically happens in synchronized global slowdowns, not supply-constrained regimes. The structural counter: ICSG (International Copper Study Group) is projecting deficits through 2027, mine permitting timelines run 10 years, and AI data center buildout is not discretionary demand. The cycle can still correct short-term, but the mean reversion case is harder to sustain post-energy-transition.

34

Jun 12

Timing is right. ICSG puts the 2026 copper deficit at 150,000 tonnes — the first since 2009. Exploration capex is well below replacement levels. The critical minerals side is the supply story getting crowded out by oil headlines.

36

Jun 12

The mining sector was the canary. Copper at ~$13,800/tonne today reflects not just short-term logistics rerouting, but the structural deficit ICSG put at 150,000 tonnes for 2026—the first since 2009. Q1 marked the moment transition-metals stopped being a 2030 story and became a 2026 problem. The volatility isn't noise; it's the market repricing years of underinvestment in mine supply.

29

1. Structural Supply Deficit and Production IssuesCopper benefits from persistent supply constraints, unlike many other commodities where production can ramp up more easily

2. Chile (world's largest producer): Production has been the weakest in 23 years in some periods; Codelco reported an 8.1% drop recently. Cochilco revised 2026 output down to 5.3 million tonnes (a 2% decline and

300,000 tonnes shortfall from prior guidance).

3. Global refined copper market: ICSG forecasts a deficit of 150,000 tonnes in 2026 (reversed from earlier surplus expectations of 209,000 tonnes). Other analysts (e.g., J.P. Morgan) see deficits up to 330,000

4. Mine disruptions (e.g., Indonesia's Grasberg, Peru) and declining ore grades add further pressure. New projects require massive investment ($250 billion just to maintain current supply levels).

#copper #mines #supply #demand

58

Jun 11

📌 تأثیر ریسکهای ژئوپلیتیکی و محدودیت معادن بر #بازار_جهانی مس

🔴 گروه #بینالمللی مطالعات #مس (ICSG) در جدیدترین گزارش خود، پیشبینی رشد #تولید معدنی مس در سال ۲۰۲۶، از ۲.۳ درصد به ۱.۶ درصد کاهش داد.

⬅️ متن کامل #خبر در معدن پرس 👇👇👇

madanpress.com/?p=125815

1

18

Jun 8

𝗧𝗲𝗴𝗮 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗲𝘀 𝗙𝗬'26 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹 𝗦𝘂𝗺𝗺𝗮𝗿𝘆 📊 :

𝗧𝗲𝗴𝗮 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗲𝘀 reported its financial results for the Quarter & Financial Year ended March 31, 2026, with key highlights from the earnings conference call:

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 💰:

- 𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗲𝗱 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 (𝗙𝗬'26): ₹17,736 million, marking a 5% year-on-year growth.

- 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔 (𝗙𝗬'26): ₹3,967 million, with EBITDA margins at 22%. This excludes exceptional items.

- 𝗘𝘅𝗰𝗲𝗽𝘁𝗶𝗼𝗻𝗮𝗹 𝗜𝘁𝗲𝗺𝘀: ₹775 million towards Molycop acquisition costs & ₹64 million for Labour Code impact.

- 𝗚𝗿𝗼𝘀𝘀 𝗠𝗮𝗿𝗴𝗶𝗻𝘀: Remained healthy at ~60% of revenue from operations.

- 𝗤4 𝗙𝗬'26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲: Total income of ₹5,633 million with an adjusted EBITDA of ₹1,632 million (29% margin).

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗦𝗲𝗴𝗺𝗲𝗻𝘁 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 📈:

- 𝗘𝗾𝘂𝗶𝗽𝗺𝗲𝗻𝘁 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: Showcased strong momentum with full-year revenue of ₹2,688 million, a 25% YoY increase. EBITDA margin improved from 12% to 13%, and PBT margin from 4% to 8%.

- 𝗖𝗼𝗻𝘀𝘂𝗺𝗮𝗯𝗹𝗲 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: Revenue for Q4 FY'26 was ₹4,406 million (down 3.5% YoY). Full-year revenue remained flat due to order shifts towards end of Q3 & Q4. Significant order booking in Feb-Mar '26 led to an 18% YoY increase in pending orders.

𝗠𝗼𝗹𝘆𝗰𝗼𝗽 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻 🤝:

- The acquisition of Molycop in partnership with Apollo Funds was successfully completed on June 1, 2026. This is viewed as a transformational milestone, creating a stronger, more diversified global mining solutions platform.

- 𝗜𝗻𝘁𝗲𝗴𝗿𝗮𝘁𝗶𝗼𝗻: A key priority is the successful integration of Tega & Molycop, focusing on streamlined processes, unified operating standards, and robust governance.

- 𝗗𝗲𝗯𝘁: Approximately $838 million of debt will be added from Molycop. Parent level debt addition is ₹1,500 crores.

- 𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗶𝗼𝗻: Molycop will be consolidated from June 1, 2026, with the first consolidated results expected at the end of Q1 FY'27 (one month of consolidation).

- 𝗦𝘆𝗻𝗲𝗿𝗴𝗶𝗲𝘀: Focus on revenue synergies with Tega & cost synergies with Molycop, along with selling non-core assets.

𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸 & 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 🚀:

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: As of March 31, 2026, the order book stands at ₹12,060 million, with ₹9,060 million executable within the next 12 months, providing strong growth visibility.

- 𝗧𝗲𝗴𝗮'𝘀 𝗚𝗿𝗼𝘄𝘁𝗵: Consumable business expected to maintain a CAGR of ~15%. Equipment business expected to see similar growth as FY'26 (~25%).

- 𝗠𝗼𝗹𝘆𝗰𝗼𝗽 𝗢𝘂𝘁𝗹𝗼𝗼𝗸: High-level assumption of 3% growth for FY'27. Molycop's FY'26 revenue was $1,539 million with an anticipated EBITDA margin of ~12% (Note: Molycop's fiscal year ends June 30).

- 𝗠𝗮𝗿𝗸𝗲𝘁 𝗜𝗻𝘀𝗶𝗴𝗵𝘁𝘀: World Gold Council data shows record gold demand in CY'25. ICSG data indicates global copper demand growing at 3% YoY with constrained supply growth, projecting over 40% demand increase by 2040.

𝗖𝗮𝗽𝗲𝘅 & 𝗢𝘁𝗵𝗲𝗿 𝗨𝗽𝗱𝗮𝘁𝗲𝘀 🏗️:

- 𝗖𝗵𝗶𝗹𝗲 𝗣𝗹𝗮𝗻𝘁: Construction progressing as planned, with commissioning expected by early Q3 FY'27. Regulatory approvals are pending for commercial production.

- 𝗙𝗬'27 𝗖𝗮𝗽𝗲𝘅: Estimated at ~$55 million (including ~$25-30 million for Chile, ~$6 million for Tega maintenance, & ~$20 million for Molycop maintenance). Funded through internal accruals & borrowings.

- 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻 𝗖𝗼𝘀𝘁𝘀: Additional transaction costs of ~$30 million are expected in Q1 FY'27.

📊 TEGA INDUSTRIES LTD | 🏷️ Earnings Call Transcript

🌐 Details: wegro.app/oUzj5i

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

85

May 26

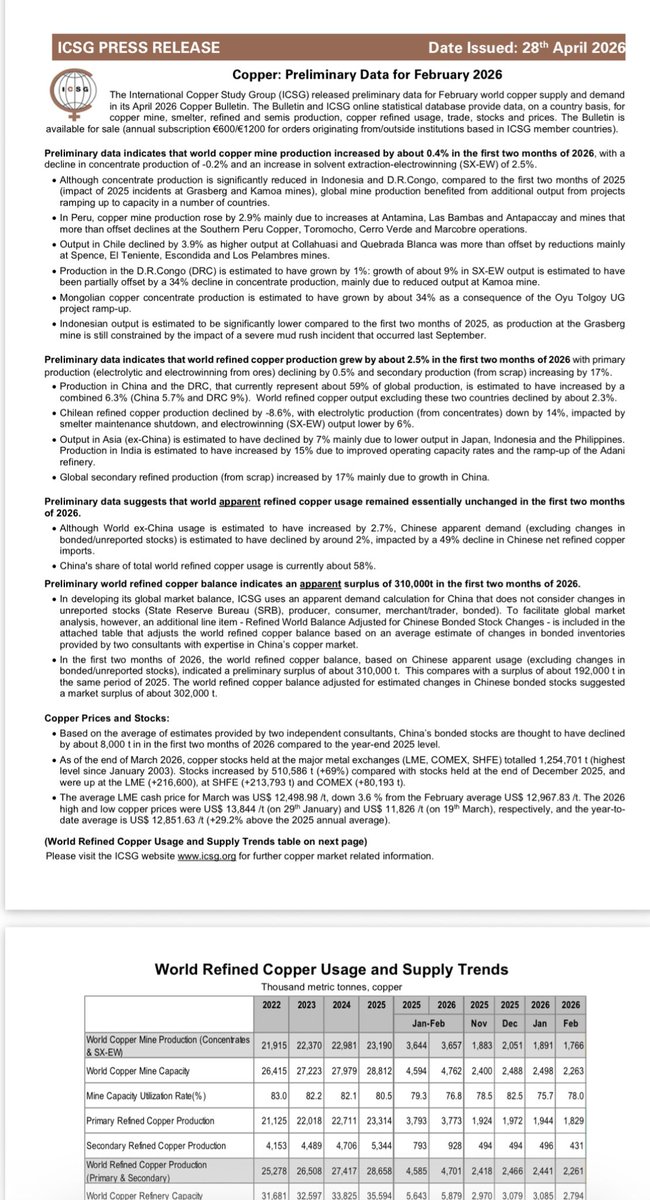

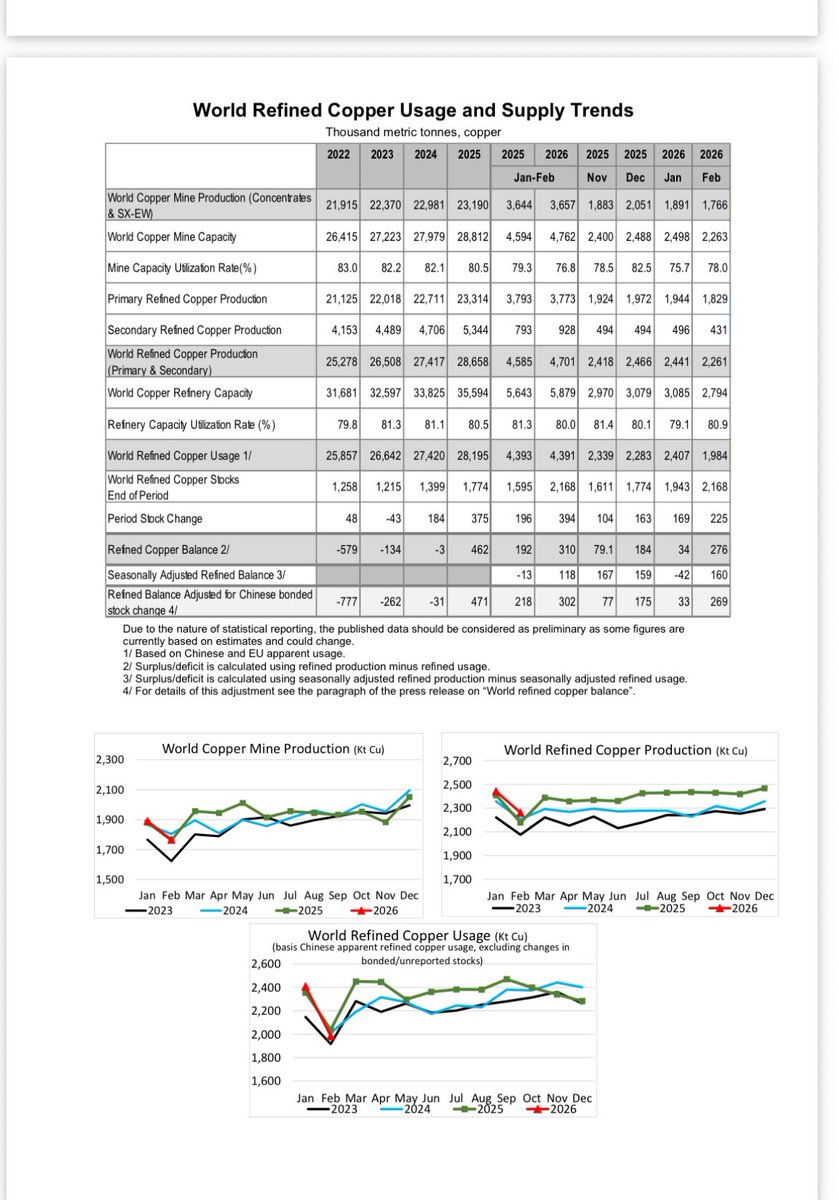

The world refined #copper market, based on Chinese apparent usage (excluding changes in bonded/unreported stocks), was in a 396,000-tonne surplus, ICSG says, vs a 135,000-tonne surplus YoY. Adjusted for estimated changes in Chinese bonded stocks, surplus was 386,000 tonnes

2

1

11

1,255

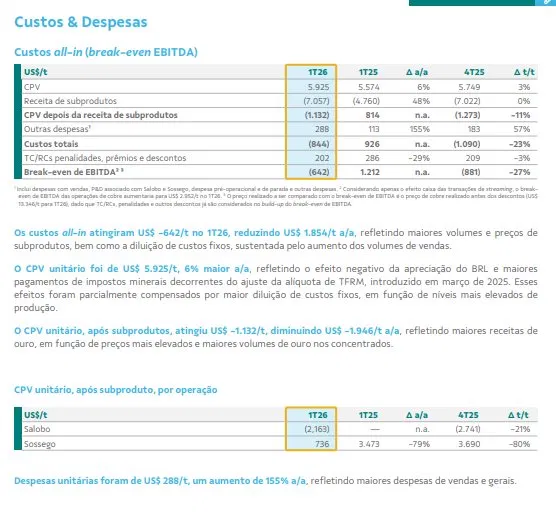

Em 28 de fevereiro de 2013, a $VALE assinou um contrato sem data de vencimento.

Salobo é uma mina no Pará que produz principalmente cobre, com ouro como subproduto.

Para financiar a expansão, a Vale precisava de capital. A solução foi vender o ouro antes de extraí-lo.

Esse mecanismo se chama streaming.

A Silver Wheaton (hoje Wheaton Precious Metals) pagou US$1,33 bilhão pelo direito de comprar 25% de todo o ouro que Salobo produziria pelo resto da vida da mina.

Preço fixo: US$400 por onça.

No dia da assinatura, o ouro estava a ~US$1.670/oz e o cobre a ~US$3,74/lb.

O desconto parecia razoável por capital imediato.

E o cobre, que a Vale estava retendo, era precificado como metal industrial cíclico qualquer.

A Vale não parou por aí.

Em 2015, vendeu mais 25% do ouro de Salobo à Wheaton por US$900 milhões.

Em 2016, os últimos 25% por US$800 milhões.

No total: US$3,03 bilhões em troca de 75% do ouro de Salobo, "para sempre", a ~US$400/oz com ajuste de inflação mínimo de 1% ao ano.

O ouro está hoje a ~US$4.550/oz.

A Wheaton continua comprando esse ouro a ~US$428/oz e vendendo a mercado.

Margem por onça: ~US$4.100.

A mina produz centenas de milhares de onças de ouro por ano.

Sobre um investimento de US$3,03 bilhões feito há menos de uma década.

O cobre, que a Vale decidiu manter, está a US$6,40/lb, ~70% acima do nível de 2013.

O all-in cost de produção de cobre em Salobo é de US$1.000–1.500/t conforme guidance da própria Vale.

Com ouro acima de US$4.500 hoje, esse custo cai ainda mais, colocando Salobo entre as operações de cobre mais competitivas do mundo.

E o ICSG projeta o primeiro déficit estrutural de cobre desde 2009.

A S&P Global estima crescimento de 50% na demanda até 2040, com eletrificação, veículos elétricos e infraestrutura de IA.

A Vale não quer ser mineradora de metais preciosos.

Ouro sobe por medo, por geopolítica, por política monetária.

Cobre constrói redes elétricas, motores, data centers.

A Vale usou o ouro de Salobo como capital para construir uma das operações de cobre mais baratas do mundo.

No 1T26, o CPV unitário de cobre após subprodutos em Salobo atingiu US$−2.163/t.

O ouro não apenas zerando, mas invertendo o custo do cobre.

O que parecia uma decisão de financiamento em 2013 foi, na prática, o primeiro passo de uma transformação de identidade.

A #VALE3 não é mais um play de minério de ferro puro tem tempo.

Salobo é hoje a expressão mais clara dessa transformação, e está acelerando a cada trimestre.

5

4

75

13,514

May 25

LME copper near $13,400/t. ICSG forecasts a 150,000-tonne refined deficit for 2026; J.P. Morgan calls it 330,000. Codelco — the world's largest producer — flatlined at 1.332Mt in 2025 despite a $2B cost program. AI buildout runs on wires. The wires are getting expensive.

1

2

113

May 24

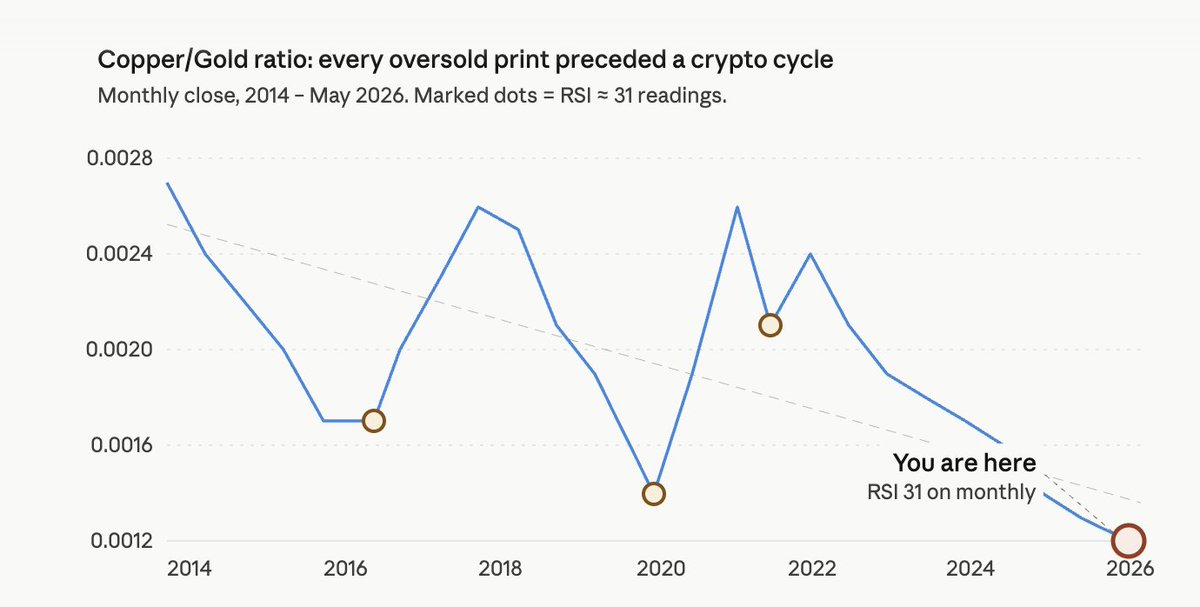

$COPPER/GOLD ratio just hit monthly RSI 31

The last three times it bottomed there ( Sep 16, Apr 20, Oct 21), crypto ripped face.

I'm long Copper and long $HYPE on @variational_io. Same cross-margined book.

Risk-on rotation → dollar weakens → real yields drop → crypto bid copper bid.

The macro fundamentals

✅ ICSG: 150k ton copper deficit in 2026

✅ AI datacenters: 475k tons consumed this year alone

✅ JPM, UBS, Citi all targeting $12k -$15k/ton by EOY (now $11.9k)

✅ HL: 97% of fees → buybacks

✅ HL ETFs: $69.6m inflows in 12 days

Where else can you express both legs on-chain in one collateral pool?

▪️ The chart is screaming

▪️ Variational is the only venue that pays you to listen

May 23

People kept asking how Variational actually gets institutional VIP rates on Binance, Bybit, HL.

1. Schuermann and Yu founded Qu Capital in 2017.

Barry Silbert's DCG acquired it in 2019.

2. The two then ran engineering and quant at Genesis Trading, one of the largest crypto desks ever.

Hundreds of billions in volume passed through their team.

They lived through 3AC FTX Genesis collapse from the inside.

3. Left in 2021. Spent the next 2 years running Variational as a market-making firm before Omni shipped a single line of code.

4. By the time Omni went live

- they already had taker volume history on every major CEX

- counterparty trust from every major desk

- a working risk hedging stack from years of prop trading.

The moat isn't the RFQ architecture.

It's everything the founders built before Omni existed.

You cannot fork this! You can only buy it!

▪️ structural moat

▪️ priced in only after TGE @variational_io

1

20

754

May 16

‘ICS is owned by ICS Healthcare Services Limited — which is owned by ICSG Limited — which is owned by Indigo Bidco Limited — which is owned by Indigo Cleanco Limited — which is owned by Indigo Intermediate Limited — which is owned by Indigo Parent Limited’

1

1

3

96

May 12

<需要側:AIデータセンターと送電網の二重圧力>

需要側の構造も見ておきたい。

レッドクラウド証券の試算で、ハイパースケールAIデータセンター1施設で銅は最大5万トン。配線・接地・冷却ループのすべてに銅が走る。

S&P Globalは、AI関連の銅需要が今後10年間で年平均40万トン、2028年にピーク57.2万トンに達すると見込む。

国際銅研究グループ(ICSG)の最新見通しでは、2026年の精錬銅は約15万トン不足。前回まで「供給過剰」予想だったのが、需給逆転に変わった。

世界の送配電網投資は2050年までに7.5兆ドル必要とされる。送電線・変圧器・モーターのすべてが銅で動く。

AIブームが電力ボトルネックを作り、電力が銅ボトルネックを作る。今回の硫酸ショックは、その「銅の細い供給ライン」のもろさを早回しで見せた格好だ。

1

54

May 12

国際銅研究グループ(ICSG)は従来の供給過剰予想を完全に撤回し、2026年は15万トンの供給不足になると予測しています。

$COPX

May 12

RANKED: The world’s top 10 biggest copper mines dlvr.it/TSVrCs

2

3

673

May 12

$copperinu was built as the on-chain, permanently deflationary version of physical $copper

ICSG (International Copper Study Group): Forecasts a 150,000 metric tonne refined copper deficit in 2026 — the first meaningful structural shortage since 2009. They recently reversed earlier surplus projections.

• J.P. Morgan: More aggressive, projecting a ~330,000 tonne deficit, largely driven by AI/data center demand.

• Other analysts (ING, etc.): See deficits as high as 400,000–600,000 tonnes.

This marks a sharp reversal from 2025, which ended roughly balanced or in a modest surplus.

Demand is growing due to multiple irreversible trends:

• AI & hyperscale data centers: One of the fastest-growing new sources. A single large AI campus can use tens of thousands of tons. Projections estimate AI/data centers alone could add ~475,000 tonnes annually by 2026–2028.

• Electrification & energy transition: EVs (3–4× more copper than ICE vehicles), renewable power installations, and grid upgrades.

• Other tailwinds: Defense spending, reshoring/deglobalization, and baseline industrial growth (~2–3% annual).

Global refined copper demand is currently ~28–28.7 million tonnes and rising.

Supply growth is very limited:

• Mine production: Expected to grow only ~1–2.3% in 2026. Many major mines are old, with declining ore grades (down ~40% since 1991).

• Long lead times: New mines take 10–17 years from discovery to production.

• Underinvestment: Decades of low capex (especially 2015–2020) mean the industry needs ~$250 billion just to maintain current production levels.

• Operational disruptions: Recent force majeure at Grasberg (world’s #2 mine), downgrades in Chile/Peru, labor/political issues, etc.

Refined production growth is also constrained (~0.9% expected in 2026).

May 12

*COPPER HITS $14,000 A TON ON LME, NEARING ALL-TIME HIGH

6

28

855

May 9

ICSGは4月末時点で2026年は9.6万トン(①)の供給過剰予測だった。

このグラスバーグ鉱山情報では生産目標が13.6万トン(②)引き下げられたので②ー①=4万トンとなり4万トンの供給不足となる⛰️

May 9

フリーポート・マクモラン、グラスバーグ鉱山のフル生産計画を2028年初頭と、従来の2027年末から延期。

去年の土石流発生からの復旧、想定していた作業量では無理との判断。追加作業の日数を加算。

>Freeport delays Grasberg full restart to early 2028

mining.com/freeport-delays-g…

6

359

Copper sitting just below the all-time high in NY today, above $6.20/lb after another 2% move higher. 📈

Chinese smelter inactivity still at 11.7%. ICSG now forecasts a 150kt deficit for 2026.

The supply side keeps doing #copper bulls a favor. ⛏️

mining.com/new-york-copper-p…

1

1

4

400