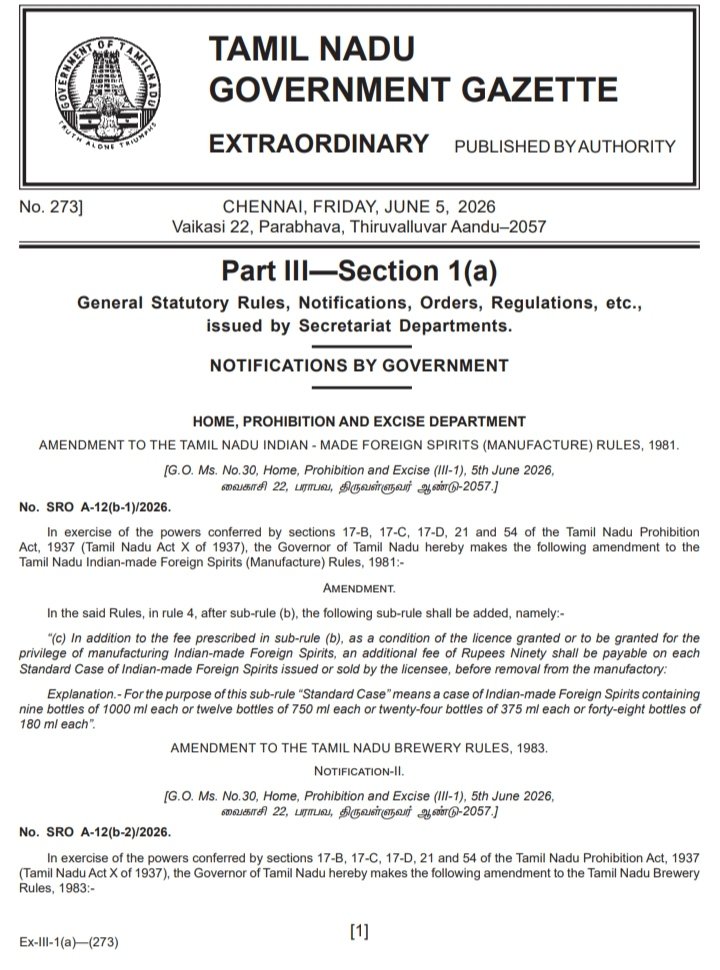

Prohibition & Excise Department of #TamilNadu hereby makes the following amendment to the

TN Indian-made Foreign Spirits (Manufacture) Rules, 1981:

For the purpose of this sub-rule ❤️“Standard Case” means a case of #IMFS containing nine bottles of 1000 ml each or twelve bottles of 750 ml each or twenty-four bottles of 375 ml each or forty-eight bottles of 180 ml each”

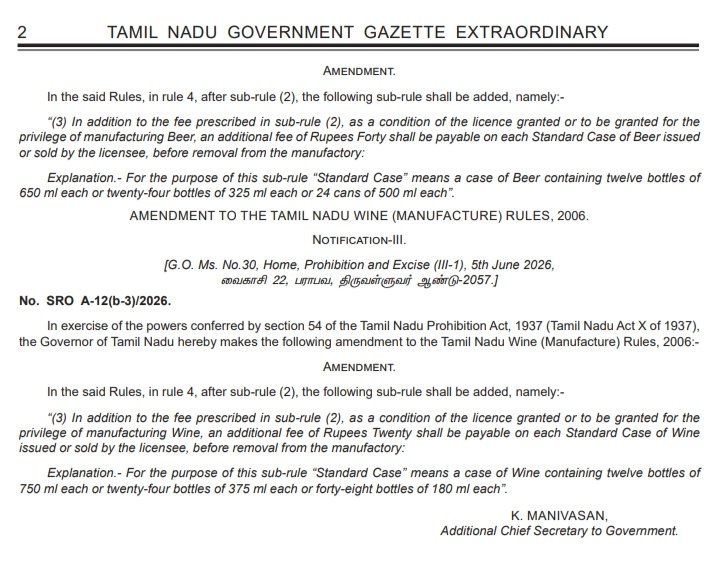

💚“Standard Case” means a case of #Beer containing twelve bottles of 650 ml each or twenty-four bottles of 325 ml each or 24 cans of 500 ml each”

💛 “Standard Case” means a case of #Wine containing twelve bottles of 750 ml each or twenty-four bottles of 375 ml each or forty-eight bottles of 180 ml each”

#TASMAC #wineshop

65

Jun 15

If Tinubu successfully implements the SAP2.0 program that suits IMFs selfish desires...what we are currently experiencing in Nigeria today will only be a child's play to what is coming ahead of all of us.

#nigeriamustbeok

@DavidHundeyin

1

7

Jun 15

Why it this hard to comprehend. Your Leadership signed this. Your people voted them in. They signed the contract n NOT PAYING

It's not the IMFs fault for your governments poor leadership. Go on the Streets n fight ur government

The IMF has asked Nigeria to add taxes on fuel and telecom services. This is the same IMF that lent us money while 63% of Nigerians were already living in poverty.

Now they want VAT on petrol and tax on your airtime. They dint say to build roads or to fix hospitals. But to make sure the repayment schedule of loans stays clean.

So let me get this straight. You borrowed money from people who are now telling you how to squeeze it back from the same suffering citizens you borrowed it to help.

Nigeria is not being governed. We are being administered on behalf of creditors. Tinubu did not come to Aso Rock to serve Nigerians. He came to service their loan.

6

At the frontier of cosmological inquiry, where the precise mapping of minute statistical residuals onto the underlying laws of radiative transfer, stellar evolution, and early-universe thermodynamics yields falsifiable leverage against both astrophysical systematics and extensions beyond the standard model, the adversarial audit failure of the modified gravitational gating model is instructive. The high-redshift massive galaxy residual (\Delta\Pi_E \approx 12.98) being fully degenerate with stellar initial mass function (IMF) variations signals that any viable extension must be confronted with observables whose scaling with the high-mass stellar distribution is both nonlinear and independently measurable.

I therefore elect to execute first the construction of the Nebular Ionization Diagnostic Vector (\mathbf{\vec{y}}). This choice is dictated by immediate empirical accessibility (existing JWST/NIRSpec and forthcoming deeper spectroscopy) and by the vector’s direct sensitivity to the microphysical consequences of any top-heavy IMF adjustment required to absorb the mass-density anomaly. The framework is derived from atomic physics, stellar atmosphere models, and photoionization equilibrium, thereby furnishing a degeneracy-breaking criterion grounded in the same fundamental interactions that govern nebular emission.

Formal Definition of the Nebular Ionization Diagnostic Vector

We construct the three-component diagnostic vector in observable space as

[ \mathbf{\vec{y}} = \begin{pmatrix} y_1 \ y_2 \ y_3 \end{pmatrix}

\begin{pmatrix} \log_{10}\left(\frac{[\mathrm{O,III}],\lambda5007}{[\mathrm{O,II}],\lambda\lambda3726,3729}\right) \ \log_{10}\left(\frac{\mathrm{He,II},\lambda1640}{\mathrm{H}\beta}\right) \ \log_{10}\xi_{\rm ion} \end{pmatrix}, ]

where the components are chosen for orthogonal sensitivity to the high-mass end of the IMF:

•(y_1) traces the ionization parameter (U) and the hardness of the EUV continuum. A top-heavy IMF (high-mass slope (\Gamma \gtrsim -2.0)) increases the relative contribution of O-type and Wolf–Rayet stars, elevating the [O III]/[O II] ratio beyond the locus spanned by standard Chabrier or Salpeter grids at fixed metallicity and ionization parameter.

•(y_2) registers the flux of photons above the He II ionization edge ((E > 54.4,\mathrm{eV})). This ratio is a stringent probe of stars (\gtrsim 100,M_\odot) or binary-stripped progenitors, both of which are strongly enhanced under top-heavy conditions. Stacked or individual high-(z) spectra showing (y_2) consistent with standard IMF predictions while the integrated stellar mass density remains anomalously high immediately falsifies the IMF-only resolution.

•(y_3 = \log_{10}\xi_{\rm ion}) quantifies the ionizing-photon production efficiency

[ \xi_{\rm ion} = \frac{\dot{N}{\rm ion}}{L{\rm UV}}\qquad[\mathrm{Hz,erg^{-1}}]. ]

Top-heavy IMFs boost (\xi_{\rm ion}) by factors of (\sim 2)–(5) relative to standard libraries because the Lyman-continuum output is dominated by the most massive, shortest-lived stars. Observed values of (\xi_{\rm ion}) at (z\sim 8)–(10) that remain within the standard-IMF envelope while the mass residual persists therefore isolate the anomaly from stellar-population systematics.

Degeneracy-Breaking Criterion

Let (\mathbf{\vec{y}}{\rm obs}) denote the measured vector (or stacked equivalent) with associated covariance matrix (\mathbf{C}) that folds in flux calibration, dust-attenuation, and photoionization-model systematics. Let (\mathbf{\vec{y}}{\rm model}(\Gamma, Z, U, t_{\rm age})) be the prediction obtained by coupling variable-IMF stellar population synthesis (BPASS, Starburst99, or equivalent) to photoionization calculations (Cloudy or equivalent) and marginalizing over metallicity (Z), ionization parameter (U), and stellar age.

The top-heavy IMF hypothesis required to absorb (\Delta\Pi_E) is rejected at a chosen confidence level if

[ \chi^2 = (\mathbf{\vec{y}}{\rm obs} - \mathbf{\vec{y}}{\rm top-heavy})^T\mathbf{C}^{-.

19

Pa Johnson retweeted

Jun 14

Egbon!

My tweet didn't validate any of IMFs policies.

We have leaders whom are indecisive who always jump on IMF ideas & celebrate their validation.

Our problem is us & our leaders,not the IMF,that's my point.

1

1

1

39

🛸 retweeted

Jun 14

IMFs business with us is we are indebted by them so sanctions will be imposed and you have nothing to do. So yeah they have his nudes

Jun 14

what’s IMF business with us now, do they have his nudes

1

1

514

Few months back IMFs Gita gopinath said something else

1

25

Jun 13

The useless low quality population are some of most hardworking people you will ever meet. Poor leadership and imprudent financial resource use coupled with IMFs debt trap, which is continously perpetuated because of poor fiscal decisions,has made human capital almost redundant

1

1

1

109

Jun 13

Tamil Nadu’s New Liquor Levy: Revenue Reform, Tax Consequences and an Unanswered Question

The Tamil Nadu Government has recently notified an additional levy on manufacturers supplying liquor products to the State distribution system.

Under the revised framework, manufacturers of Indian Made Foreign Spirits (IMFS) are required to pay an additional fee of ₹90 per standard case, beer manufacturers ₹40 per case and wine manufacturers ₹20 per case.

The stated objective appears to be augmentation of State revenue and formalisation of collections within the liquor supply chain.

To that extent, the policy deserves appreciation.

For several years, industry discussions have revolved around various embedded costs and informal practices in the liquor procurement ecosystem. If the intention of the Government is to bring such collections into the formal revenue stream of the State, transparency is always preferable to opacity.

However, the recent notification raises a larger legal, tax and policy question that deserves careful examination.

Is this truly a manufacturer’s levy?

The fee is imposed directly on manufacturers supplying liquor into a State-controlled distribution framework dominated by TASMAC.

This gives rise to an interesting question.

Is the manufacturer merely bearing an independent regulatory cost of doing business?

Or is the manufacturer effectively discharging a charge that economically arises because of the State-controlled procurement and distribution structure?

In substance, one may ask whether this is a charge that ordinarily belongs within the procurement economics of TASMAC but has been structured as a levy payable by the manufacturer.

The answer to this question may have significant implications under tax law.

The Section 40(a)(iib) Debate

Section 40(a)(iib) of the Income-tax Act, 1961 was introduced to disallow deductions in respect of royalty, licence fee, service fee, privilege fee, service charge or any other fee or charge levied by a State Government on its own undertakings.

The legislative intent was to prevent diversion of profits from State Government undertakings through special levies imposed by the State itself.

The Supreme Court, while examining privilege fees, gallonage fees and similar charges in liquor-related cases involving State undertakings, emphasised that the true character of the levy is often more important than the nomenclature adopted by the Government.

At first glance, Section 40(a)(iib) may not directly apply because the present levy is imposed on private manufacturers and not on a State Government undertaking.

However, the jurisprudence surrounding the provision raises broader questions.

Can a levy imposed exclusively because supplies are made into a State-controlled distribution system be viewed differently from an ordinary business expenditure?

Can courts examine the economic substance of the transaction rather than merely its label?

Can the characterisation of the payment itself become a subject matter of future litigation?

These questions remain open.

The Income-tax Act, 2025 Perspective

One of the core objectives of the new Income-tax Act, 2025 is simplification, reduction of litigation, certainty in taxation and improvement in ease of compliance.

Modern tax policy seeks to minimise disputes and create a predictable business environment.

Against this backdrop, the present notification raises an important policy concern.

If the objective is revenue mobilisation, could the same objective have been achieved through a different fiscal architecture?

For example:

• Revision of procurement pricing.

• Modification of TASMAC margins.

• Excise restructuring.

• Alternative statutory mechanisms.

Instead, the Government has chosen the route of an “additional fee”.

This naturally raises questions regarding its precise tax character and treatment.

1

1

5

343

Part 2 of 2 🧵

9) The .#G7 Government have moved their irreplaceable protection all lives Human Rights Ideology to Human Lives are Disposal Commodities Ideology and a line item on the profit and lost budget statements. The budget will balance itself because of the drastic reduction of healthcare, long term care and pension payments! Healthcare Privatization, Triage & Care Protocols using cost of disease metrics will determine who get to live or die based upon the individuals social value to society

10) Organ Harvesting, Organ Trafficking, Organ Donation and Blood products selling & Microchip Implants and assisted living devices is the actually core commodity driving the change in Human Life Ideology and this change was decided by the Rich unelected Elite

Qhttps://halifaxinitiative.org/content/imfs-structural-adjustment-programme-canada-1994-1995-december-1995

thephilanthropist.ca/2016/06……

#C7 #MAiD was passed using time allocations to shut down the voices of the Anti-eugetics advocates during debate in the House of Commons

This is not democracy it is a death sentence to low income Canadians by the Liberal Party that entered a Nazi in the House of Commons!

Post 1 of 2 🧵

Provincial underfunding of Social Assistance programs across Canada which have been drastically underfunded since 1994/5 budget year when Jean Chretien & Paul Martin got a secret letter from the Globalist International Monetary Fund which told Canada to cut social spending!

Doug Ford'a "Historic" increase to ODSP was in fact Historical but Doug Ford's increase of 5% was only Historic because since 1995 ODSP has only been increased by 1-2% since 1995, however the annual cost of living has gone up by 92% for Canadians and #pwd need an addition 40% to cover their added cost.

Doug Ford gaslit Ontarian voters with his 5% historic increase using optics to his advantage

In addition to his Historic increase Doug Ford did the right thing by bring in legislation to automatically increase ODSP based on the annual cost of living in 2022 However the Ableist Doug Ford did the wrong thing and not fix the ODSP inflation gap from 1995 to 2022 leaving disabled no further ahead in 2026. The the Liberal Party of Canada | Parti libéral du Canada dangled the new Canadian Disabilities Benefit in front of People with Disabilities for 5 years during the COVID-19 crisis.

The benefit was announced in 2020 and was to lift Canadians out of poverty similarly to the GIS, however news agencies turned a blind eye to the political games occurring in the benefits development and final rollout!

I could write a book on this topic however key takeaways from my post are:

1} Ableism is rampant in the Canadian Government

2) Global Disabilities Human Rights are under attack by #G7 countries political parties. Eg. Trump ban on EDI words & HUD dog legislation changes

announced last week

3) Social media has thousands examples of Government Ableism

4)It took 2 weeks for CERB to be issued at the start of COVID for Workers, however People with Disabilities who only live on Disabilities Benefits because the can't work got discriminated based upon Employment status and only a small number with a Disability Tax Credit got PPE help in October not April like ables

5) The Ontario COVID Recap report fails to mention the PPE crisis and Long Term Social Worker Employment Abandonment walkout story broke when Jane Philpot broke the story while urgently stepping in at Participation House Markham, a long term facility for Adult people with Disabilities where 4 people had died. Instead the Ford Government used a Rouge Hill LTC which was subsequently discovered to have had similar issues.

6) During the Full-time employment job shortage and recession in 1992 caused by computer networking and globalist outsourcing downsizing and rightsizing the Government created a new Middle Class Job Sector for Nonprofits and Charities who gave #pwd assistance & developed programs. However the actual lives of people with Disabilities became collateral damage / sacrificial lambs for the Government who blatantly made the systemic choice to underfund basic needs legislative programs for #pwd and others who are experiencing hard times and need welfare / social assistance and give that program funding and grants to Nonprofits & Charities instead which mostly goes towards middle class able bodied workers pay checks & tax breaks for Top 100 organizations

7) The World Economic Forum #WEF discussed a new social class of citizens who because of AI and Robots implementation are being displaced from the workforce as a result of their skills becoming redundant. This new social class has been dubbed the name "Useless" class.

8) The Government is targeting Baby Boomers aka pension entitled Seniors, #pwd including veterans, mental health, & addicts and anyone else who ends up on Welfare/ social assistance or bankrupted due to Inflation & pitiful minimum wage rates to sacrifice themselves using Medical Assistance in Dying #MAiD for the greater good of the youth and Rich who will be able to afford to participate in Transplants and other biomedical procedures

30

Jun 12

⎐كُـود⎐كوبِون⎐خـِصم⎐

⎐نون⎐

⊵S3Q⊴

⎐ايهرب⎐ايهيرب اهرب

⊵GCA5893⊴

⎐فــوما⎐

⊵EMF69⊴

⎐بلومنغديلز▬بلومينغديلز⎐

⊵SAR⊴

ستايلى⊴⊴

⎐ZQX⊴

درعــه⊴

⊴ AD4

⎐ممزورلد⎐

⊵ET11⊴

___

IMFs

What the fuck us the IMFs business here?

Jun 10

“It’s risky” — IMF warns Tinubu’s government against $5bn Abu Dhabi Bank loan

14

Deepak Jain retweeted

Jun 8

🔹 Scope of Financial Product Marketing by IMFs (Through FSEs)

As per the current regulatory framework, Financial Service Executives (FSEs) engaged by an Insurance Marketing Firm (IMF) are empowered to distribute a wide range of financial products beyond insurance.

This includes:

• Mutual Fund products regulated by SEBI

• Pension solutions governed by PFRDA

• Financial products offered through SEBI-registered Investment Advisors

• Banking and financial products from RBI-regulated Banks and NBFCs

• Non-insurance offerings from India Post (Department of Posts, Government of India)

• Any additional financial products or activities permitted by the Authority from time to time

💡 My Perspective:

In my view, this regulatory structure clearly positions IMFs as emerging “One-Stop Financial Solution Providers” rather than just insurance distributors.

It not only enhances the scope of services but also creates powerful cross-selling opportunities, enabling better financial planning and improved value delivery to clients—all through a single, trusted platform.

#FinancialServices #InsuranceMarketingFirm #IMF #FSE #WealthManagement #FinancialPlanning #IndiaFinance

2

2

17

Allegedly the commission per box ₹90 for IMFS, ₹40 for beer seems to have been faked as "party fund".

Sources say the actual commission paid to middlemen was close to 10 rs per box earlier and the ruling party now wanted this to be bumped by another 40 rs as their "Party fund"

9

Jun 8

Am 18. Mai 2026 veranstaltete das IMFS ein Policy Webinar mit @Lars_Feld und @wolf_reuter zu ihrem Buch „Schuldenwende“.

Thema: Warum schuldenbasierte Finanzpolitik attraktiv ist, welche Risiken sie birgt und welche Alternativen es gibt.

📽️youtube.com/watch?v=mNgJNH7P…

3

5

1,054

Jun 8

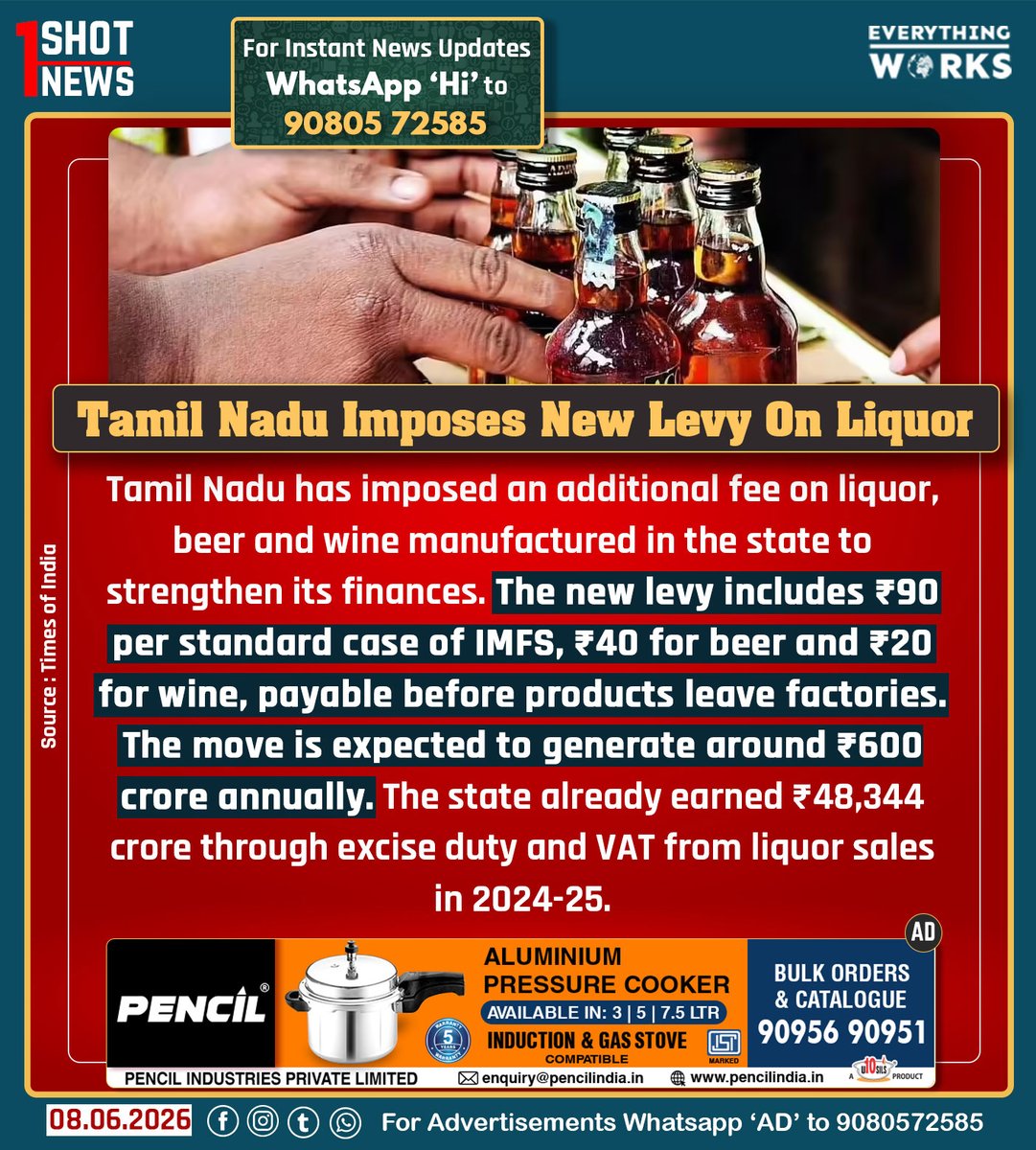

Tamil Nadu has imposed an additional fee on liquor, beer and wine manufactured in the state to strengthen its finances. The new levy includes ₹90 per standard case of IMFS, ₹40 for beer and ₹20 for wine, payable before products leave factories. The move is expected to generate around ₹600 crore annually. The state already earned ₹48,344 crore through excise duty and VAT from liquor sales in 2024-25.

#1ShotNews | #TASMAC | #Liquor | #LiquorRevenue | #Tamilnadu | #TamilnaduNews

1

3

17

1,901