29 Sep 2025

Invoice Management System| What are the invoice requirements?

#GrowingGautengTogether #IMS #InvoiceManagementSystem

2

147

17 Feb 2025

Understanding the New Invoice Management System (IMS) in GST: A Step Towards Simplification and Transparency kvstax.com/blog/understandin…

#KVSTAX #KVSTAXCONSULTANCY #GST #InvoiceManagementSystem #IMS #GSTIndia #TaxReforms #GSTCompliance #BusinessCompliance #Taxation #InputTaxCredit

2

38

20 Jan 2025

Our Founder and MD, Mr. @reachShriram, has written an article for @moneycontrolcom discussing the introduction of the Invoice Management System (IMS) and how it will affect India's Micro, Small, and Medium Enterprises (MSMEs).

Even though this introduction of IMS represents a significant step forward in strengthening GST compliance in India, MSMEs nationwide will face challenges in transitioning into this new system. This article highlights the need for extended timelines for MSMEs to adapt to these systems due to factors such as limited access to credit, technological constraints, and the complexities involved in digitalization. The article also explores proactive steps the government could take to assist MSMEs in implementing IMS effectively.

Read the full article here:

moneycontrol.com/news/opinio…

#InvoiceManagementSystem #IMS #MSME #GSTCompliance #DigitalIndia #MSMESupport #IndianEconomy #BusinessInsights #TaxReforms #GovernmentPolicy #ReachShriram #MoneyControl

1

2

318

12 Jan 2025

🚨 IMS to Become Mandatory Soon!

🔗 Prepare for these changes now to stay ahead of compliance obligations.

#GSTwithSaradha

#GSTUpdate #InvoiceManagementSystem #IMS #GSTR2B #InputTaxCredit #UnionBudget2025 #FinanceBill #TaxCompliance #GSTCouncil #CreditNotes #GSTIMS

1

4

158

17 Dec 2024

#GST Council likely to approve rules for Invoice Management System to tackle fake invoicing, tax evasion

Read More👇

moneycontrol.com/news/busine…

#GSTCouncil #InvoiceManagementSystem #TaxReform #FakeInvoicing #TaxEvasion #GSTUpdates

1

3

2,681

18 Nov 2024

Karneeti Part 570 - Understanding new Invoice Management System on GST Portal

#GSTUpdates #InvoiceManagementSystem #TaxCompliance #GSTPortal #Karneeti #ITCEligibility #TaxpayerAwareness #GSTIndia #InputTaxCredit #GSTSimplified

2

232

17 Nov 2024

Saying again👇🏻

Infosys has the biggest testing team across the universe ,

which includes you,Me and Millions of Tax Payers/Professionals!!😟

@Infosys_GSTN

#InvoiceManagementSystem #IMS #Infosys #GST #GSTR3B #GSTR2B

11

65

208

15,748

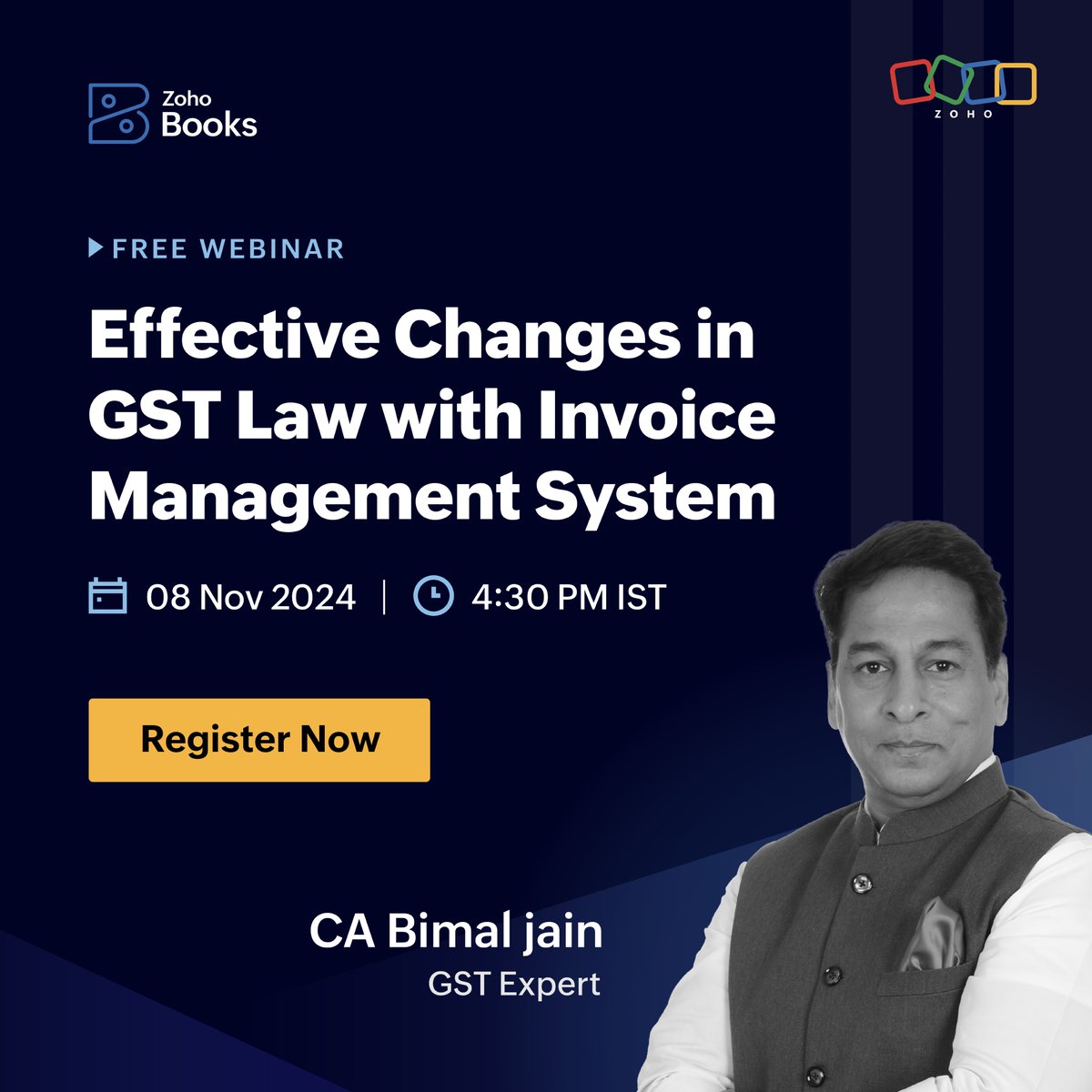

23 Oct 2024

Join our webinar with CA Bimal Jain (@BimalGST) on the latest GST Law changes & the new Invoice Management System (IMS)!

Date: 8 November, 2024

Time: 4:30 PM

Register: meet.zoho.com/zl9rgcxNGW

#GSTUpdates #BimalJainWebinar #ZohoFinance #InvoiceManagementSystem

2

6

949

1 Oct 2024

🟥💥 Much Awaited Video on:

✅ All about Invoice Management System (IMS) under GST || CA (Adv) Bimal Jain

🎥 Watch Complete Video at: youtu.be/WBelbKutIr0

#InvoiceManagementSystem #IMS #GST #a2ztaxcorpllp #GSTwithBimalJain #advbimaljain

2

4

972

6 Sep 2024

Invoice Management System - The Potential Issues That Could Arise - It Is An Update, Nobody Asked For

The GST Authorities have issued an Advisory which seeks to implement the Invoice Management System (IMS) from 1st October 2024, wherein it is stated that the Assessee's will have the option to accept, reject, or keep pending, the invoices reported by their suppliers through an IMS Dashboard.

Further, it states that if the Assessee has not taken any action, it will be deemed that the assessee has accepted the invoices so uploaded by their suppliers

Questions To Ponder Upon:

👉 Why do we need an accept, reject, or pending system in connection with invoices in GSTR 1 when we already have a GSTR 1A in place, which provides for making amendments in case there is a mistake in GSTR-1.

👉 What is the Department trying to achieve by putting the onus on the receiver of supply to accept, reject invoices.

👉 Can this potentially lead to a situation wherein the supplier makes a mistake, and the receiver is denied benefit or is penalized at a later stage stating that no action was taken by such receiver and therefore there was a deemed acceptance, and having accepted the invoice, the receiver cannot come and dispute the anomaly in the invoice

Example:

Assuming my supplier has raised an invoice for Rs.1,00,000/- which ought to have been Rs.90,000/-. For whatever reasons I missed taking any action on the invoice and it is now deemed to have been accepted.

Later I tell my supplier that a credit note ought to be issued for Rs.10,000. Upon issuance of such credit note I as the supply receiver ought to reverse credit proportionately.

Now can the Department say, that I accepted the invoice earlier and now that I am reversing ITC on account of a credit note, I am liable to reverse the same along with interest on account of not rejecting or keeping the invoice pending at the time it was uploaded.

What is mentioned above is only an example and there could be numerous other issues wherein benefits are denied or supply receiver is penalized for having accepted or deemed accepted the invoice at the time it was uploaded.

Shifting the onus on the service receiver could therefore do more harm than making it easier for them. Again this may or may not happen.

The crux of the matter here is that the GST Authorities have suddenly decided to put the onus on the supply receiver for no justified reason through a system that does not exhibit any major benefit through its implementation.

The real problem businesses are facing is the non-uploading of invoices by suppliers and not the invoices that have been uploaded, as such invoice reflects in GSTR-2B and there are enough options to correct mistakes in such invoices.

Why then implement another layer of checking by placing the onus on the supply receiver through IMS.

Views Welcome!

#GST #InvoiceManagementSystem #IMS #GSTN

1

7

2,223

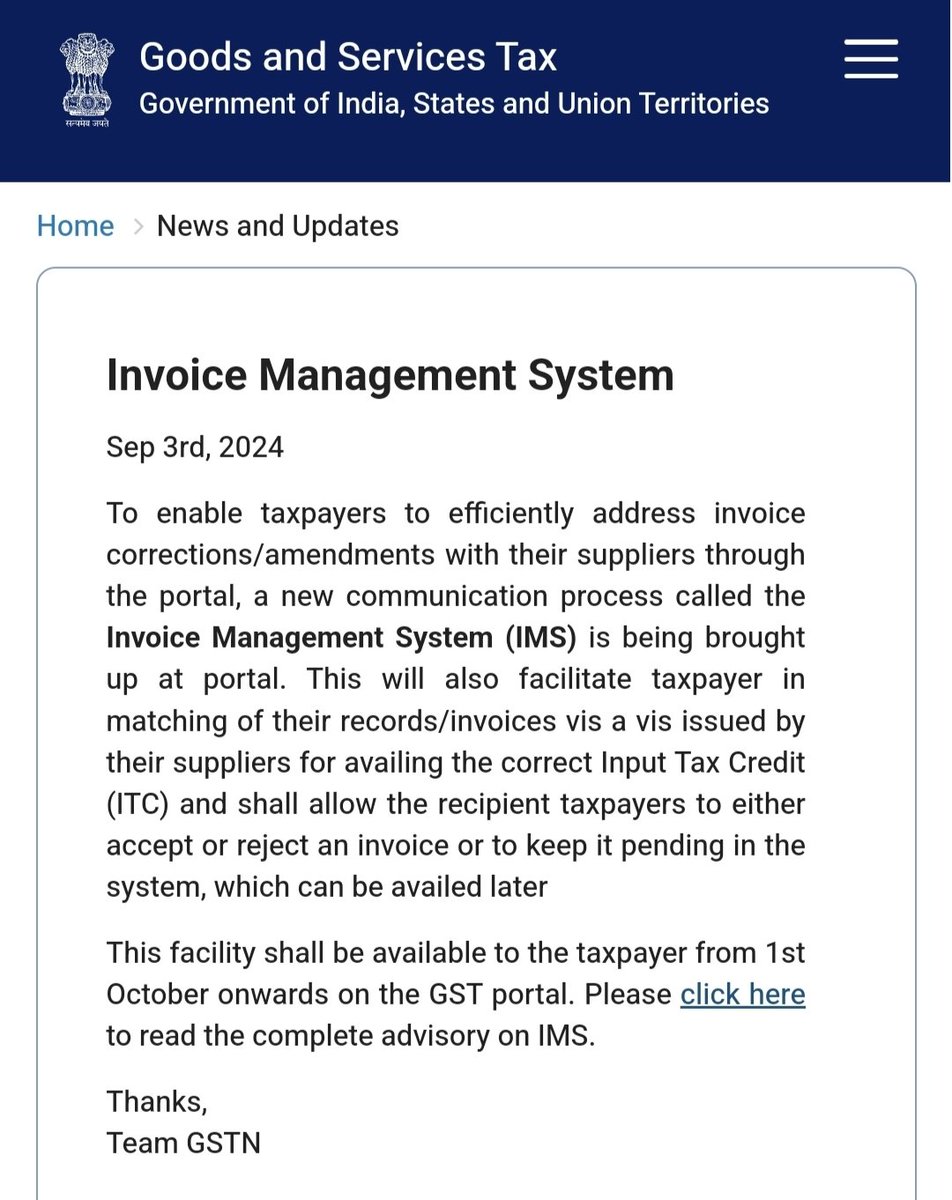

3 Sep 2024

𝗜𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝗚𝗦𝗧𝗡 𝗨𝗽𝗱𝗮𝘁𝗲: To enable taxpayers to efficiently address invoice corrections/amendments with their suppliers through the portal, a new communication process called the 𝗜𝗻𝘃𝗼𝗶𝗰𝗲 𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗦𝘆𝘀𝘁𝗲𝗺 (𝗜𝗠𝗦) 𝗶𝘀 𝗯𝗲𝗶𝗻𝗴 𝗯𝗿𝗼𝘂𝗴𝗵𝘁 𝘂𝗽 𝗮𝘁 𝗽𝗼𝗿𝘁𝗮𝗹 𝗳𝗿𝗼𝗺 𝟭𝘀𝘁 𝗢𝗰𝘁𝗼𝗯𝗲𝗿 𝟮𝟬𝟮𝟰.

The complete advisory can be accessed here 👇

🔗gst.gov.in/newsandupdates/re…

#GST #InvoiceManagementSystem #Advisory

4

1,281

31 Dec 2021

#InvoiceMate Wishes you a very happy new year

#InvoiceManagementSystem #Fintech #InvoiceProcessing #Blockchain

2

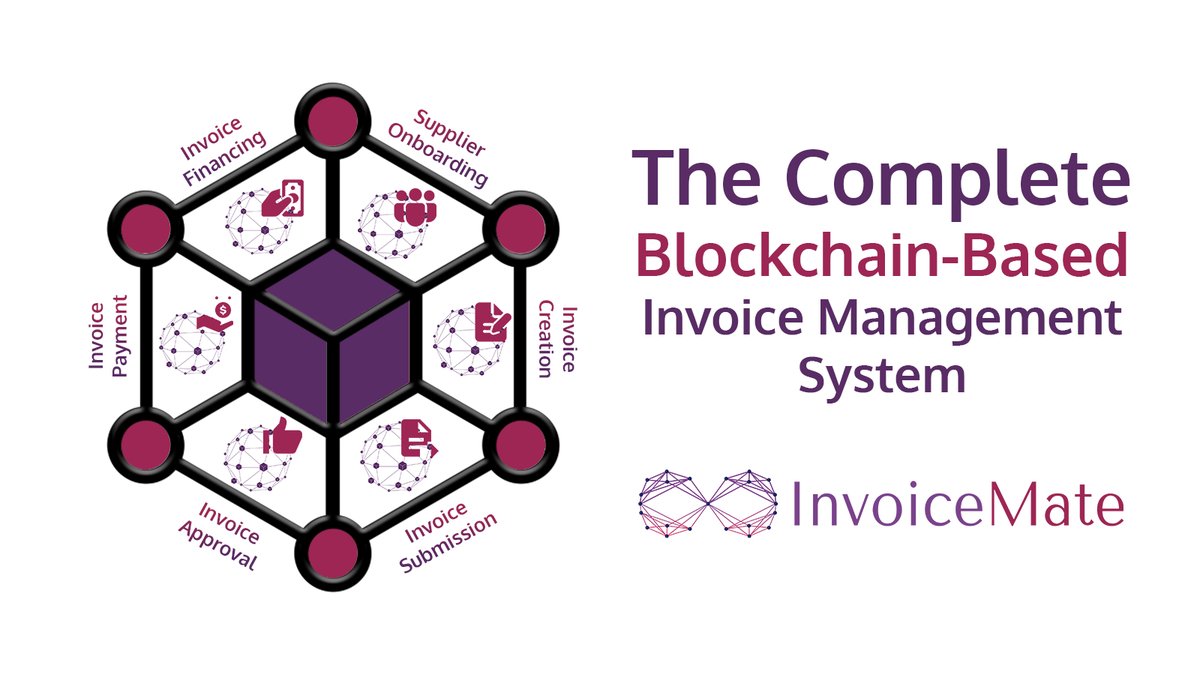

6 Dec 2021

#InvoiceMate is the first #Blockchain Based #InvoiceManagementSystem

The Six Sides of The Block:

•Supplier Onboarding

•Invoice Creation

•Invoice Submission

•Invoice Approval

•Invoice Payment

•Invoice Financing

For More Details

invoicemate.net/

#Fintech

3

9

30 Jul 2021

78% of #Fitness enthusiasts are now switching to #OnlineFitnessSession to keep themselves fit

Planning to start your own #OnlineFitnessClasses? #Invoicera can help

Contact us for your #OnlineInvoicingSystem

bit.ly/3ca0EH7

#BestBillingSoftware #InvoiceManagementSystem

2

3

1 Apr 2021

Running an #onlinebusiness requires a broad variety of expertise & information📃

#Invoice creation is one of many such roles that require accuracy & precision.

Check how to create an #InvoiceManagementSystem for your #woocommerce store!

#MakeWebBetter

bit.ly/3ubkaJN

2

5