Apr 23

You close a deal.

You send an invoice.

Client pays.

And then… nothing.

“Processing.”

“Pending.”

“3–5 business days.”

The value has already moved. The money didn’t.

That gap? That’s where businesses lose momentum.

Cash flow stalls. Opportunities get missed. Teams sit waiting.

Keyflo is built to remove that gap entirely.

When money is sent → it arrives.

When you earn → you can use it.

When you move → it keeps up.

No delays hiding behind “business hours.”

No friction between earning and accessing your own capital.

Because speed isn’t a luxury in modern business.

It’s the baseline.

1

4

42

Apr 20

This is exactly what Keyflo is built to eliminate.

No batching.

No dependency on legacy clearing windows.

No “wait until tomorrow.”

Money moves when it’s sent.

Because in 2026, your biggest financial risk shouldn’t be infrastructure from the 1970s lagging behind your business.

4

22

Apr 13

Online, everything happens instantly.

Messages send instantly.

Files upload instantly.

Trades execute instantly.

But money still moves in batches.

That’s because most banks still rely on legacy infrastructure built decades ago.

Keyflo runs on modern digital payment rails instead.

That means faster settlement, more predictable costs, and global access by default.

Money should move at the same speed as the rest of the internet.

1

2

6

101

Apr 2

Using a card abroad still feels unpredictable.

You tap.

You wonder what FX rate you got.

You wait to see the final amount.

#Keyflo is designed to make spending clearer.

Transparent conversion.

Real-time balance updates.

Controls built into the same system you use to send money.

So you always know where you stand.

Join the waitlist 👉 keyflo.app/

1

1

5

100

Mar 30

Imagine this.

You’re in a group chat planning a trip.

Someone books a boat.

You owe them your share.

Instead of opening your bank app, copying details, waiting for confirmation…

You switch to the Keyflo keyboard.

Send the payment instantly.

Conversation continues.

Payments should happen at the moment they’re needed — not interrupt your flow.

Join the waitlist now 👉 keyflo.app/

2

1

6

70

Mar 28

Modern banking shouldn’t feel like managing folders.

Checking account.

Savings account.

FX wallet.

Payment app balance.

All separate. All requiring transfers.

With #Keyflo, everything runs from one global balance.

You can send, spend, or allocate to savings without moving money between 'accounts.'

It’s a simpler way to think about money — and a calmer way to manage it.

1

3

60

Mar 27

Most people don’t hate their bank.

They just quietly work around it every day.

Waiting for transfers.

Moving money between apps.

Paying unexpected FX fees.

Checking if payments actually landed.

Banking still feels slower than the internet we live on.

Keyflo was built to change that.

One global balance.

Instant payments.

Clear controls.

Join the waitlist.

2

5

56

Imagine this.

You're in the middle of a conversation with a friend or family member. You owe them money for dinner last week.

Or maybe you want to send support back home.

Normally, you pause the chat.

• Open another app.

• Copy a long address.

• Double-check everything.

• Hope the transaction goes through.

It breaks the flow, especially for someone like me who hates distractions and stress 😂.

But what if you never had to leave the conversation?

You tap, type, confirm and the money is sent.

No back and forth.

No headache.

Just send.

That is what digital payments should feel like.

Yet today, sending crypto on mobile still feels stressful. The process was built for experts, not everyday people.

That is why millions own digital money but rarely use it for simple things like splitting bills or helping family.

This is where @KeyFlo_App comes in.

KeyFlo is a wallet built directly into your phone keyboard.

Currently on waitlist, but the idea is simple. Once it's live, you install it once, and it works inside the apps you already use like WhatsApp, Telegram, X, and other messaging apps.

While chatting, you can send or receive money without leaving the conversation.

No copying addresses.

No app switching.

Just send.

It turns payments into something as natural as sending a message.

It legit matters especially for everyday use:

- Friends splitting bills

- Families sending support

- Remote workers getting paid faster

- Cross-border payments without the usual friction

Turning your keyboard into a payment layer.

And if they get this right, sending money could finally feel as easy as sending a message.

41

11

53

1,479

Mar 17

This is why we are building a better way on #Keyflo

me copying my friend's wallet address character by character like I'm defusing a bomb

1

5

95

Mar 15

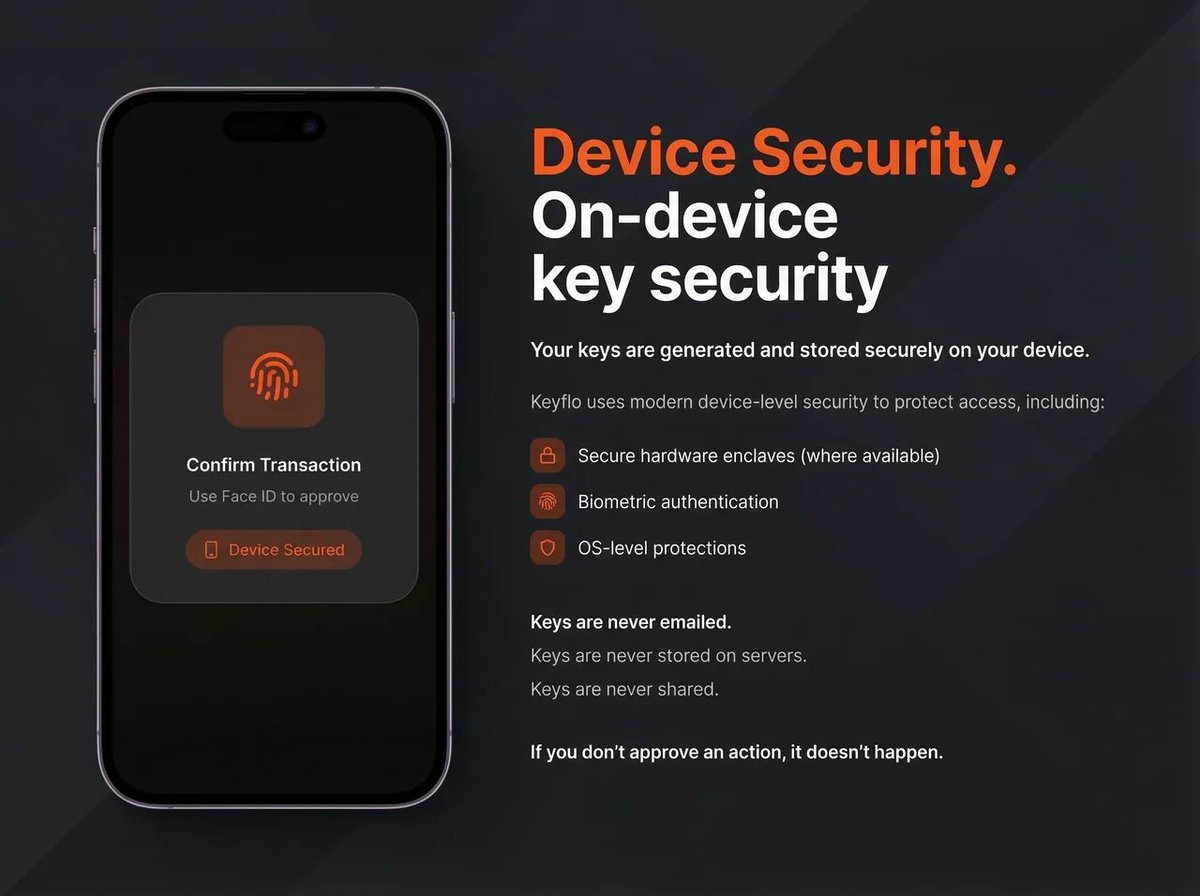

🔐 Security that lives where your life happens — on your device.

With Keyflo, your keys are generated and stored securely on your phone, not on external servers.

Every action requires your approval — powered by biometric authentication, secure hardware enclaves, and built-in OS protections.No emails.

No sharing.

No silent transactions.

Just simple, seamless control — exactly how modern payments should feel.

If you don’t approve it, it doesn’t happen.

✅#Keyflo #DeviceSecurity #OnDevice #Fintech #Web3 #Payments

1

1

5

98

This app I just found could change how we save, send, and receive crypto forever!

Imagine if your phone's keyboard could have a built-in crypto wallet

You install Keyflo once and give it keyboard permission

Just like that, you can send stablecoins directly inside chats

Just like typing a normal text message inside your favorite messaging app

You can get early access by joining the waitlist

Mar 10

Your keyboard is the most-used interface on your phone.

Messages. Searches. DMs. Everything runs through it.

So why don’t payments?

What if sending money were as easy as typing a message?

No new app. No switching tabs. Just your keyboard.

42

56

2,934

Mar 6

716 Million People Own Crypto. Only 70 Million Use It. Here’s Why.

Crypto never had a mobile moment. Not because the technology wasn't ready, but because the interface was broken from the start. Here's the data behind the drop-off.

716 Million People Own Crypto. Only 70 Million Use It. Here’s Why. Crypto has a mobile problem nobody wants to admit. 716 million people worldwide own some form of cryptocurrency. Only 40 to 70 million actively use it. The gap exists because sending money on a phone is a genuinely bad experience. Not complicated in a learning-curve way. Bad in a designed-to-fail way.

Here’s the truth: 78% of people access crypto on their phones. And yet, the entire crypto ecosystem was built for desktop power users, browser extensions, and people with 20 minutes to spare. The gap between those two realities is why crypto hasn’t gone mainstream. Friction.

A Paradox Hiding in Plain Sight

Let’s put real data to this feeling:

73% of first-time crypto users quit after their very first error. Not their second. Their first. The margin for error on mobile is zero, and nobody tells you that when you’re getting started. 37% of new wallet users make exactly one transaction, then disappear. 81% never reach ten. And here’s the stat that captures the whole problem in one line:

78% of people visit crypto sites on mobile. But MetaMask — the world’s most popular wallet — still gets 70% of its traffic from desktop browsers. People want mobile crypto. The tools just won’t let them have it. Meanwhile, desktop wallets have shrunk to just 9% of usage. The users moved to mobile.

What Actually Breaks the Transaction

It’s not one problem. It’s five.

1. App switching.

Send crypto on mobile and you’re immediately bouncing between your messaging app, your wallet, a block explorer to confirm, and back. A study of nearly 46,000 app reviews of the top five crypto wallets found that both new and experienced users consistently struggle with the same thing: the flow is broken before you even get to the transaction. Every switch is a micro-abandonment. Six times out of ten, the brain says: not worth it.

2. Transactions that fail silently.

Network congestion. Wrong chain. Gas set too low. Node errors. On mobile, these don’t produce clear error messages, they produce silence. Or a spinning loader that never resolves. The same study found users calling wallets ‘scams’, not because they were, but because a failed transaction with no explanation looks exactly like theft.

3. Gas fee confusion.

People from traditional payment backgrounds assume transactions are free, fast, and reversible. Gas is none of those things. MetaMask only introduced the ability to pay gas fees in non-ETH tokens in February 2025. That was a 2025 fix for a problem that’s existed since 2015.

4. Address complexity.

42 characters. Hexadecimal. Chain-specific formatting. One wrong character and the money is gone. Forever. This isn’t a crypto problem. It’s a UX crime.

5. Jargon overload.

Seed phrases. Gas. Wrapped tokens. EVM-compatible. Signing transactions. This is a foreign language, and nobody provides a dictionary at the door. The result: a 90% drop-off from people who own crypto to people who actually use it. Out of an estimated 716 million crypto owners globally, only 40–70 million are active.

The Infrastructure Is Finally Here

Here’s what makes all of this so frustrating: the underlying technology finally works. Stablecoins processed $33 trillion in 2025, a 72% year-over-year increase. USDC alone grew 78% in the same period. The stablecoin market crossed $314 billion and is projected to hit $1.9 trillion by 2030 according to Citi. Layer 2 networks like Base, Optimism, and Arbitrum bring transaction costs down to cents, sometimes fractions of a cent. A transfer that cost $20 in Ethereum fees three years ago now costs $0.01. The GENIUS Act was signed into law in July 2025, creating the first federal regulatory framework for stablecoins. Visa’s stablecoin settlement hit a $4.5 billion annualized run rate. Stripe acquired stablecoin infrastructure company Bridge for $1.1 billion. Visa. Stripe. Western Union. They are all building on stablecoin rails.

280 Million People Are Still Paying the ‘Stupid Tax’

Every month, 280 million people send money across borders. The global average fee for sending $200 internationally is 6.49%. Sub-Saharan Africa corridors average 7.7%. The UN set a goal to get this below 3% by 2030. Stablecoins already do it for under 1%.

Maria in New York sends $500 to her mom in the Philippines every month. Western Union charges her $40 in direct fees plus a hidden exchange rate markup: roughly $55 total. That’s 11% of the transfer. Over a year: $660.

With a stablecoin wallet, sending 500 USDC costs cents on a Layer 2 network, wallet to wallet. The real cost comes at the edges: converting dollars to stablecoins (on-ramp) and converting stablecoins back to local currency for her mom to use (off-ramp). With a good provider, that end-to-end journey lands between 1–3% in total fees, and still a fraction of Western Union’s 11%. Annual savings: $600.

However, Maria doesn’t use a stablecoin wallet. Because the one time she tried, she got lost between apps, confused by gas fees, and gave up. The product failed her. Not the other way around.

3 Billion People Already Know Where Payments Should Live

WhatsApp has 3 billion monthly active users. They open the app an average of 23 times per day. That’s 930 times a month. 930 moments where a payment could happen. If the tools were there. WeChat figured this out. WeChat Pay now has 1.3 billion users and processes over 1 billion transactions daily, totaling more than $15 trillion annually. Users didn’t download a separate finance app. They just started paying inside their conversations. The transition was invisible. The payment was already where the conversation was.

WhatsApp tried to replicate this. WhatsApp Pay launched in India in 2020. Five years later, it has about 10 million monthly active payment users, in a country with 500 million WhatsApp users. Google Pay has hundreds of millions more in the same market. WhatsApp Pay is available in just three markets — India, Brazil, and Singapore. It doesn’t support crypto or stablecoins, and has seen minimal product investment even after regulatory restrictions were lifted. In India, it has fewer than 10 million active payment users despite 500 million WhatsApp users in the country.

The opportunity is wide open. A cross-platform, stablecoin-native payment layer that works inside every conversation.

Your Keyboard Is Already There

You type on your keyboard 150 times a day. WhatsApp. Telegram. iMessage. Signal. Twitter. Every app where you communicate passes through the same keyboard. The keyboard is the most-used interface on your phone. Every message, every search, it all goes through it. So what if the payment layer lived there too? Not another app to open. Not another account to create. Not another reason to switch contexts.

You’re chatting with someone. You want to send $10. You tap your keyboard. A payment window appears. You type 10. Send. That’s it. Done in 5 seconds. You never left the conversation.

That’s what Keyflo is. A keyboard wallet. Stablecoin payments built into the one interface that’s already everywhere you are.

No gas confusion. No app switching. No seed phrase to lose. Just: type, tap, send.

Be Among the First to Use It

Keyflo is built for the 78% of people who already live on their phones, and for the 280 million who keep paying 6–11% in remittance fees because the mobile alternative was never good enough to trust.

We’re opening access in waves. Early users get first access to new features, priority support, and the chance to actually shape what gets built next.

The keyboard is already in your hand. Join the waitlist at keyflo.app.

1

1

5

171

Mar 3

This is why businesses need to use keyflo to make payments - you will know exactly who you are sending money to.

2

15

Feb 25

Imagine money moving like messages.

Instant. Borderless. Invisible.

That’s where we’re going with #Keyflo

1

1

7

123

Feb 20

Bank transfer: 2–3 days.

Crypto card: inconsistent.

KeyFlo: seconds.

Access your wallet inside your keyboard.

5

119