Bansal Wire Industries Ltd

Bansal Wire Industries has recently secured a trial order from a major top‑four Indian tyre manufacturer.

This segment is historically dominated in India by the Belgian firm Bekaert.

Steel tyre cord is not used in all tyres—it is specifically the foundational reinforcement material for radial tyres.

Bansal Wire is currently the only and first Indian company to start manufacturing steel cord.

Tyres generally fall into two structural categories, each with distinct internal skeletons:

🌐Radial Tyres

🌐Bias-Ply (Cross-Ply) Tyres

Because steel cord is tied exclusively to radial tyres, the demand for it depends entirely on the "radialization" percentage of different vehicle segments.

Passenger Vehicles (PVs): Passenger cars and SUVs in India are nearly 100% radialized. Every standard PV tyre requires steel cord.

Trucks and Buses (Commercial Vehicles): This is the true heavyweight driver of steel cord demand. A heavy commercial radial tyre consumes far more steel than a car tyre. India’s commercial segment is currently about 65–70% radialized. Historically, trucks used nylon bias tyres for better overload handling, but regulations and highway expansion have accelerated the shift to fuel‑efficient radials.

Two‑Wheelers & Three‑Wheelers: These remain overwhelmingly bias‑ply. Bikes and rickshaws need flexible, low‑cost tyres suited to lower speeds, so nylon cords dominate. Steel cord is limited to high‑end performance motorcycles.

The structural shift in India from nylon bias tyres to steel‑belted radials—especially in heavy commercial trucks—is a multi‑decade mega‑trend.

Bansal Wire’s entry into the steel cord market positions it directly on this wave of increasing radialization across the Indian automotive landscape.

Tyre Bead Wire vs. Steel Tyre Cord

While both are high-carbon steel wires used in tyres, their applications, engineering requirements, and market dynamics are completely different.

Tyre Bead Wire

Anchors the tyre to the metal wheel rim to prevent it from slipping.

Steel Tyre Cord

Reinforces the tyre's tread area, providing puncture resistance and maintaining shape.

Based on the latest management commentary and the structural nature of tyre supply chains, commercialization is expected in the second half of this year.

Process:

Phase 1: Lab/Sample Approval (Completed): Bansal has cleared this stage, successfully receiving sample approvals from major Indian tyre manufacturers after rigorous laboratory testing.

Phase 2: Field Trials (Underway): The recently secured trial order is for this stage. The tyre manufacturer builds actual tyres using these cords and tests them under real‑world road conditions.

Challenges & Headwinds

Energy & Supply Chain Disruptions: In March, geopolitical tensions between Iran and Israel caused volatility in global energy markets. A temporary disruption in industrial natural gas supply forced the company to take a cut in production volume

Gas Pricing Impact: Natural gas prices surged, increasing costs by roughly ₹4,000-₹5,000 per ton. Due to the 30-40 day existing order book, these costs had to be absorbed momentarily, negatively impacting the EBITDA per ton during the last 15 days of Q4

Other than steel cords, Bansal wire also has forayed into -

IHT Wire (Induction Hardened & Tempered)

This is a specialized grade of high-carbon steel wire that undergoes a highly controlled heat treatment.

Showing strong momentum; operating at 25% capacity utilization as of March, which is expected to ramp up by 10-15% monthly

LRPC Wire (Low Relaxation Pre-Stressed Concrete)

Launched with an 18,000-ton capacity, which has already begun generating a positive EBITDA

Disclaimer: Not an investment advice. Informational note on steel cords.

79

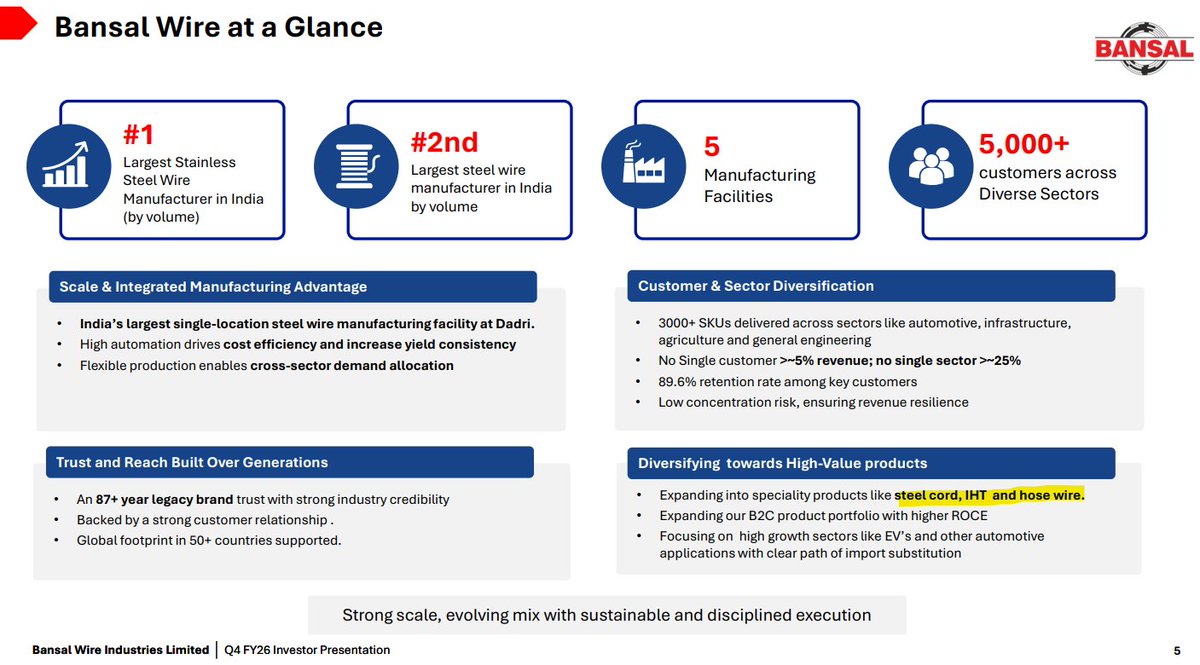

Bansal Wire Industries -

The company manufactures steel wires, stainless steel wires, spring wires, welding wires, LRPC wires, IHT wires and steel cords using steel wire rods as the main raw material. This is largely an industrial B2B business where branding plays a limited role, resulting in margins of around 7-8%.

A major listed competitor is Usha Martin, which is roughly having twice the margin of Bansal Wire.

Retail shareholding is very low. Fixed assets have increased sharply, indicating the company is still in a major expansion and capex phase.

Over the last three years, sales have grown about 20% annually while profits have grown about 40% annually. Current capacity is around 6.8 lakh MT and management aims to increase it to more than 8 lakh MT by FY27.

Management's strategy is to gradually increase the share of specialty products such as IHT wires, LRPC wires, specialty wires and steel cords to improve profit margin.

The biggest long term opportunity is steel cords, which are ultra high tensile steel reinforcements used inside tyres. India currently has very limited domestic production, creating a large import substitution opportunity. The business has high technological barriers, long customer approval cycles and a shortage of skilled manpower, making entry difficult.

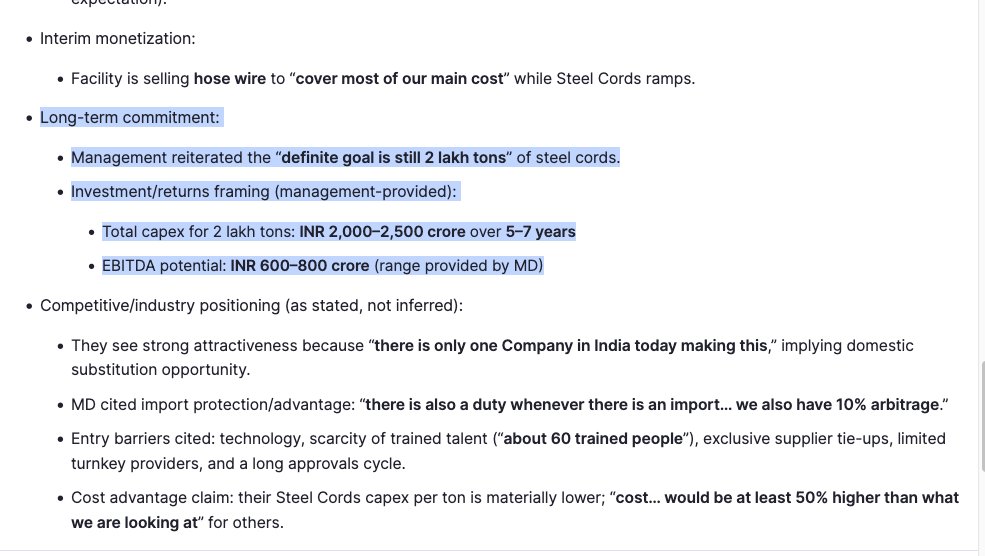

Management saying that they are building a 2 lakh ton steel cord business.

This would require 2000-2500 crore of capex over 5-7 years and could generate 600-800 crore EBITDA.

This is significant because Bansal Wire's current total EBITDA is only about 325 crore.

If executed successfully, the steel cord business alone could eventually generate more EBITDA than the company's entire current business today.

Steel cord capacity is currently around 40000 tons.

Management plans to scale this to over 1 lakh tons and eventually to 2 lakh tons.

At that level, steel cords could account for roughly one-fourth of total company capacity and potentially become one of the company's most profitable segments.

The most important challenge is not capacity creation but customer approvals.

In steel cords, building the plant is relatively easy, but getting tyre manufacturers to qualify and approve products is difficult and time consuming.

Future success depends heavily on these approvals.

Future potential depends primarily on successful execution of steel cords and specialty products.

The most important metrics to track are steel cord approvals, commercialization progress, specialty product contribution and improvement in EBITDA per ton.

1

9

621

May 6

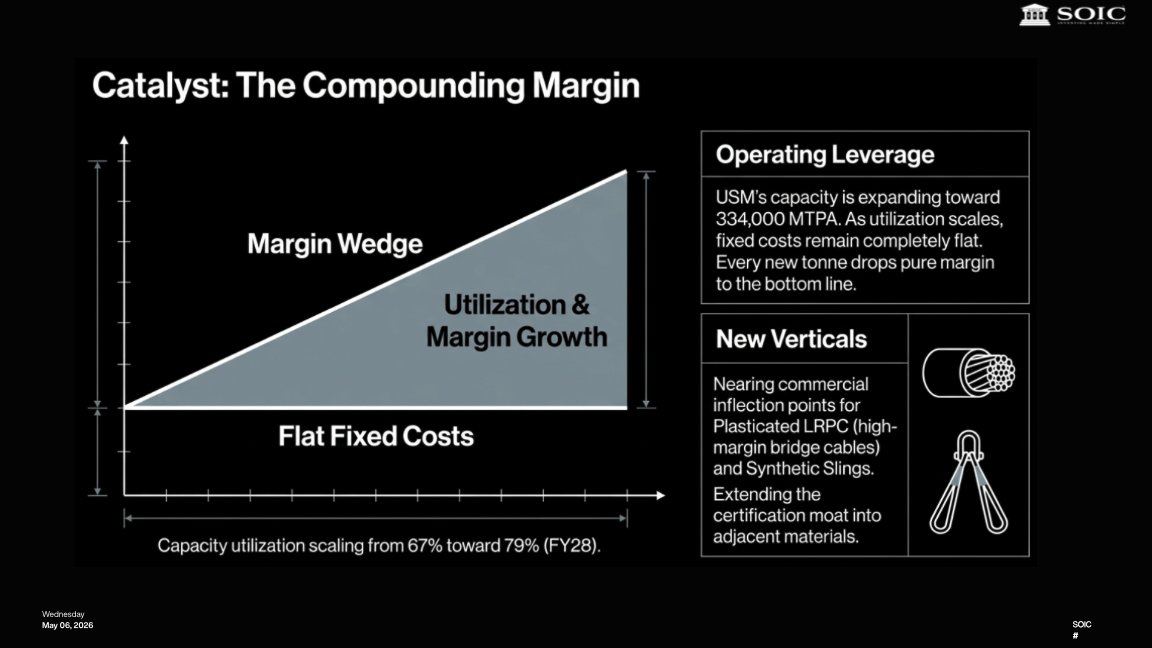

Trigger 3 - New Verticals Maturing: Plasticated LRPC and Synthetic Slings

Two adjacency businesses that USM has been developing are approaching inflection points.

Plasticated LRPC (Low-Relaxation Pre-Stressed Concrete strands with a polymer coating) is a specialty product used in bridge construction, metro viaducts, and infrastructure projects where corrosion protection is critical.

The realisation premium over standard LRPC is approximately 40,000-50,000 per tonne. USM has been working with several global players for approvals, and management indicated on the Q4 call that these approvals are nearing completion expected within weeks. Once secured, the company will have access to the global export market for plasticated LRPC, a segment where Indian manufacturers have had limited presence to date.

Synthetic slings represent a complementary product line to wire ropes used in applications where flexibility, corrosion resistance, or lighter weight is preferred. In its very first year, the ocean fibre synthetic business has already achieved customer approvals and repeat orders, suggesting genuine product-market fit rather than experimental dabbling.

Neither of these is large enough today to move the needle on consolidated numbers. But they represent the continuation of the same strategic pattern: climbing the value ladder by entering adjacent segments where certification barriers protect margins and customer qualification cycles create stickiness.

1

4

693

May 6

And with this mix shift happening the reflection is coming up on the margins of the company →

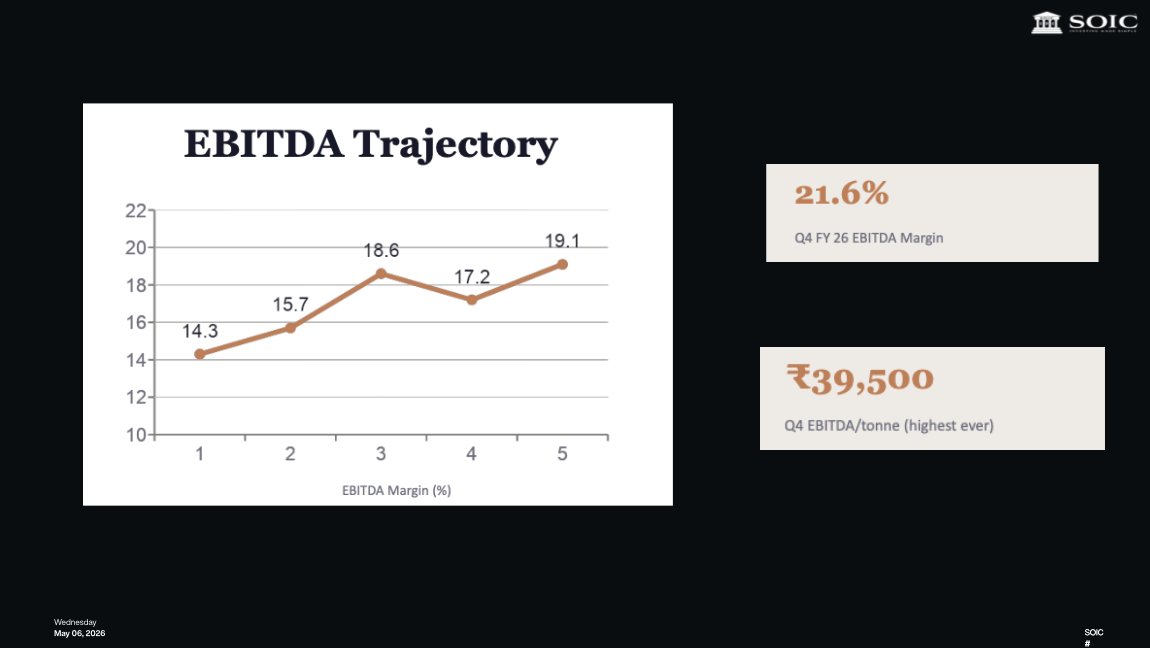

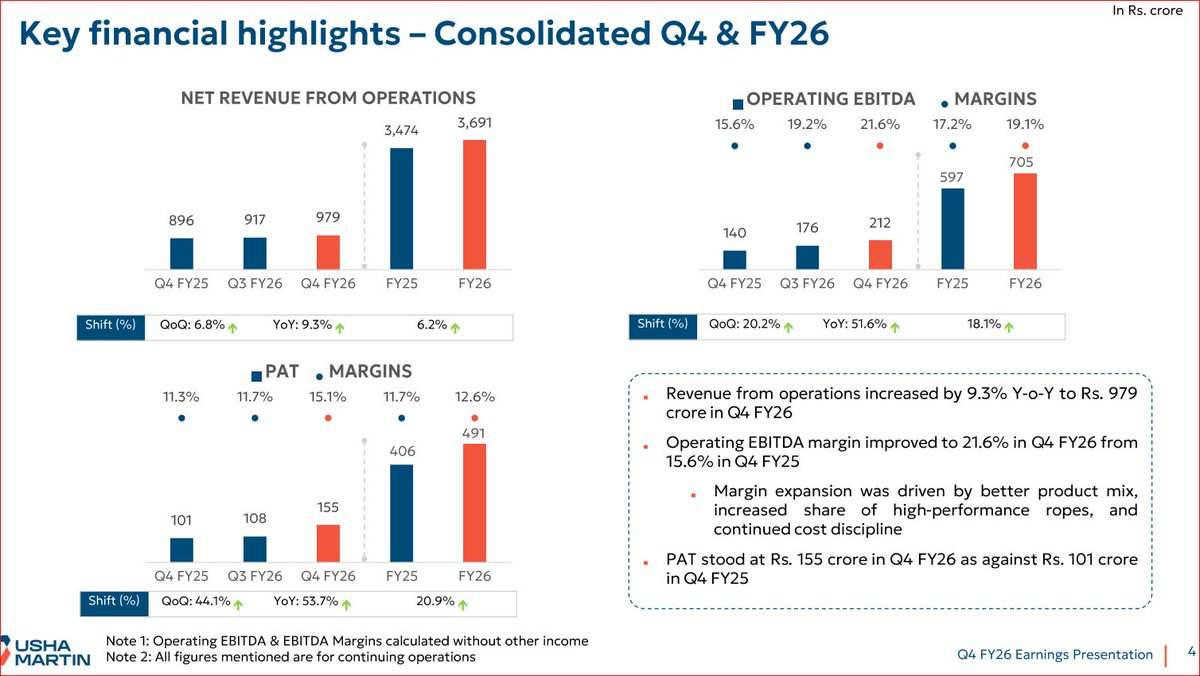

FY26 operating EBITDA was 705 crores, up 18% from 597 crores in FY25, with margins expanding from 17.2% to 19.1%. Q4 FY26 was the standout :- 212 crores of EBITDA at 21.6%, the highest operating margin since the sale of the steel business. EBITDA per tonne for the full year improved to approximately 34,100 from 30,100 in FY25, and hit 39,500 in Q4.

The margin expansion is structural, not cyclical. It is driven by three concurrent forces: the continuing shift from commodity wires and LRPC toward value-added ropes (which improves the revenue mix), the cost savings from the One Usha Martin initiative (which reduces the cost base), and improving capacity utilisation at the upgraded Ranchi facility (which delivers operating leverage on the fixed cost base).

Management has indicated that 20% EBITDA margin is now the operating benchmark, not an aspirational ceiling. Given the trajectory of Q3 and Q4 FY26, this appears credible.

1

6

773

May 6

With all this uniqueness in the business model the question that comes to mind is that does it translate into robust financial health of the business?

Short Answer - Yes but let me explain how

Starting of with understanding the revenue trajectory of the company →

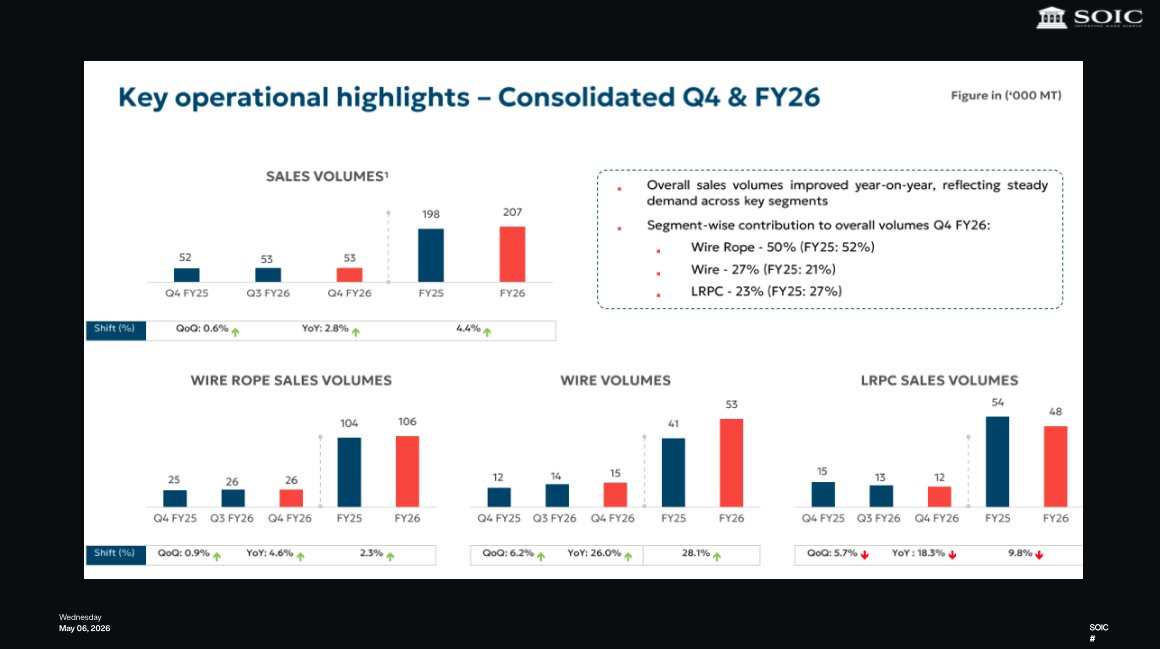

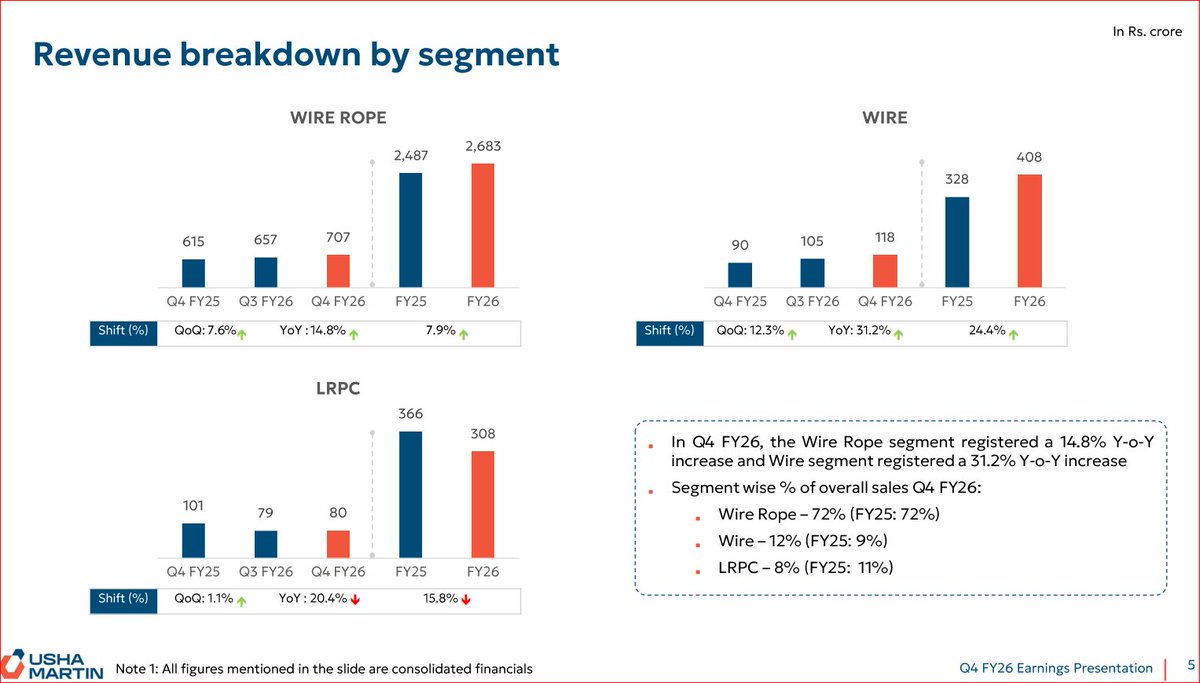

Consolidated revenue for FY26 came in at 3,691 crores, up 6.2% year-on-year. While headline growth appears moderate, the composition tells a more important story. Wire rope revenue, the highest-margin, highest-moat segment grew approximately 8% for the full year. Wire and strand revenue surged about 24%, reflecting the ramp-up of specialty wire products.

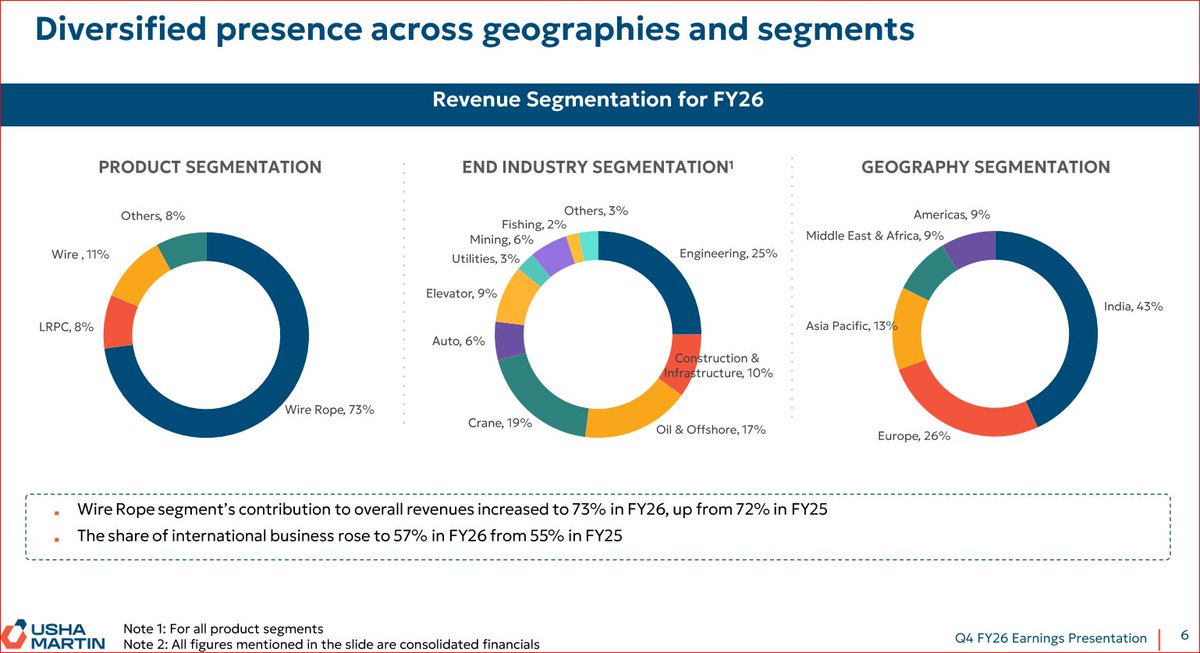

International revenue now accounts for 57% of the total, up from 55% in FY25 and 51% in FY22. Q4 FY26 was particularly strong at 979 crores, up 9.3% YoY, with rope revenues growing 14.8% a clear acceleration as new OEM relationships and market development efforts from the prior 2-3 years began converting into orders.

The full-year growth was moderated by a conscious 20% decline in LRPC sales (the lowest-margin segment) and softness in the Middle East due to geopolitical disruptions. Management has guided for 10-12% volume growth in FY27 and beyond, supported by new capacity commissioned at Ranchi and in Thailand.

1

4

826

May 5

Usha Martin Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Transition to high-margin specialty rope player

MANAGEMENT COMMENTARY

- Shift from foundation → execution phase

- Highest EBITDA post steel business sale

- Focus on specialized rope segments

- “One Usha Martin” driving efficiency

FINANCIAL PERFORMANCE

Q4FY26

- Revenue: ₹979 Cr

- EBITDA Margin: 21.6%

FY26

- Revenue: ₹3,691 Cr (↑6.2% YoY)

- EBITDA: ₹705 Cr (19.1%)

FUTURE OUTLOOK & GUIDANCE

- Volume growth target: 10–12%

- Margin benchmark raised to ~20%

- Healthy H1 order book visibility

INDUSTRY & MACRO TRENDS

- Energy security driving offshore demand

- Rising steel, gas, logistics costs

- Strong infra demand in India

COMPETITIVE POSITIONING

- Only rope manufacturer in GCC region

- Focus on value-added services

- Competes with global premium players

- Expanding US and Europe presence

RISKS & CONCERNS

- Middle East disruptions impacted volumes

- LPG costs sharply increased

- Long gestation infra projects

- Raw material availability tight

GROWTH DRIVERS & STRATEGY

COST OPTIMIZATION

- ₹65–70 Cr savings via efficiency program

CAPEX PLAN

- ₹300 Cr capex over two years

- Focus: elevator ropes, specialty wires

NEW SEGMENTS

- Growth in synthetic ropes (Ocean Fiber)

- Plasticated LRPC scaling up

PRODUCT MIX

- International revenue: 57% share

- Realizations crossed ₹3L per ton

- Shift to high-margin products

BALANCE SHEET

- Net cash: ₹332 Cr

- Debt-free standalone

KEY INSIGHT

- Premium mix driving margin expansion

OUTLOOK

- Strong double-digit volume growth ahead

- Margins sustaining above 20%

- Export demand key driver

CONCLUSION

- Successfully transformed into specialty player

- Strong cash flows and balance sheet

- Capex aligned to high-growth segments

- Execution on volume growth is key trigger

#Ushamartin @FI_InvestIndia @FundamentalGems

1

1

10

1,595

I think that was Hagenes in the front for Visma, Laporte I think had to slow down in the crash a bit. They didn't show it but I think Hagenes did a turn and when he was done Tim attacked (based on LRPC).

RBH were at least well positioned on the climb and in general in Omloop.

1

2

58

Feb 6

When I was member of the LRPC (London Regional Passengers Committee) and its successor LTUC (London Transport Users Committee) this was my bête noire.

It is ridiculous that a National Rail Station in Central London is not considered as such.

It simply makes no sense….

15

7

139

24,941

Incidence du régime LRPC élargi au Canada sur les secteurs de l’immobilier et des prêts hypothécaires jdsupra.com/legalnews/incide… | by @blakeslaw

96

U rubrici finansijska edukacija

Filipsova kriva

Filipsova kriva objašnjava kratkoročne odnose i zašto se ne može trajno rešiti niža nezaposlenost višom inflacijom – ali više nije onaj jednostavan alat za izbor između inflacije i nezaposlenosti kao što je izgledalo 1960-ih.

Filipsova kriva (Phillips curve) jedan je od najpoznatijih koncepata u makroekonomiji. Ona opisuje vezu između inflacije i nezaposlenosti.

**Originalna ideja (A. W. Phillips, 1958.)**

Novi Zelandski ekonomista A. W. Phillips analizirao je podatke za Veliku Britaniju (1861–1957) i otkrio jasan obrazac:

- Kada je nezaposlenost bila niska, plate su brzo rasle (visoka inflacija zarada).

- Kada je nezaposlenost bila visoka, rast plata bio je spor ili čak negativan.

Kasnije su ekonomisti tu vezu proširili na cenovnu inflaciju (ne samo plate), pa je nastala klasična ideja: postoji obrnuta veza (trade-off) između inflacije i nezaposlenosti – bar u kratkom roku.

Kriva se obično crta ovako:

Y osa: stopa inflacije

X osa: stopa nezaposlenosti

Kriva pada s leva na desno → niža nezaposlenost → viša inflacija.

U 1960-ima mnogi ekonomisti (posebno kejnzijanci) videli su to kao „meni“: država može stimulisati privredu (fiskalna/monetarna politika) → prihvati malo višu inflaciju → dobije nižu nezaposlenost.

**Kratkoročna vs. dugoročna Filipsova kriva**

**Kratkoročna Filipsova kriva (SRPC – short-run)**

- Pada nadole (obrnuta veza postoji)

- Uzroci: lepljive plate/cene, neočekivana inflacija, privremeni šokovi tražnje

- Kada tražnja poraste → ekonomija se kreće duž krive (niža nezaposlenost, viša inflacija)

**Dugoročna Filipsova kriva (LRPC – long-run)**

- Vertikalna linija na nivou prirodne stope nezaposlenosti (NAIRU)

- Nema dugoročnog trade-off-a

- Ako se nezaposlenost dugo drži ispod prirodne stope → inflacija ubrzava (očekivanja se prilagođavaju naviše)

- Kratkoročna kriva se pomera naviše kada očekivana inflacija poraste

Ovo su snažno zagovarali Milton Friedman i Edmund Phelps (kraj 1960-ih) – delom zbog toga dobili Nobelove nagrade.

Stagflacija 1970-ih (visoka inflacija visoka nezaposlenost) naizgled je uništila staru Filipsovu krivu – ali je zapravo potvrdila verziju sa očekivanjima.

**Savremeni pogled (2020-e – 2026.)**

Filipsova kriva se i dalje koristi, ali se smatra mnogo ravnijom nego ranije (inflacija slabije reaguje na promene nezaposlenosti ili output gap-a).

Razlozi:

- Dobro ukorenjena očekivanja inflacije (~2% kod kredibilnih centralnih banaka)

- Globalizacija i lanci snabdevanja

- Smanjena pregovaračka moć radnika

- Produktivnost, AI i drugi strukturni faktori

Ipak, kriva nije potpuno ravna – inflacija i dalje reaguje na slobodne kapacitete i šokove ponude (energija, tarife, poremećaji u lancima snabdevanja).

Centralne banke i dalje prate ovu vezu, ali više gledaju na očekivanja inflacije, šokove ponude i dugoročno sidrenje nego na iskorišćavanje kratkoročnog trade-off-a.

2

78

A landmark in modern bridge engineering, the Ambaragodlu–Kalasavalli Bridge in Sagar, Shivamogga, Karnataka stands as a testament to innovation and advancement in infrastructure development.

#UshaMartin #wirerope #lrpc #manufacturing #bridge #construction #infrastructure

2

124

🏗️ Steel Products Co's Q3 Updates

Steel demand is strong across the board.

But leadership differs sharply when you compare scale, growth, and value-added execution.

Growth & Mix Leaders

🏆Sambhv Steel Tubes

• Q3 volume: 97,472 MT | 34% YoY

• Value-added products: 90,612 MT | 63% YoY

• Stainless steel utilisation rising → highest operating leverage

Bansal Wire Industries

• Q3 volume: 121,702 MT | 31.7% YoY | 6.2% QoQ

• 9M FY26: 340,411 MT | 37.9% YoY

• Specialty wires (LRPC, IHT) scaling fast

Scale & Benchmark Leader

🥉 APL Apollo Tubes

• Q3 volume: 916,976 MT (all-time high)

• 9M FY26: 2.57 mn MT | 11% YoY

• Industry benchmark; growth steady, not explosive

Steady Executors

• JTL Industries

Q3 90,429 MT | 10.8% QoQ | 3.1% YoY, exports 11% YoY

• Hi-Tech Pipes

Q3 136,067 MT | 10% YoY | 9% QoQ

• Rama Steel Tubes

Q3 58,975 MT | 14% YoY, 9M FY26 23% YoY

Read

APL Apollo dominates scale.

But growth leadership re-rating potential currently sits with Sambhv & Bansal.

📌 Steel cycle is on — alpha shifts from size → execution.

Sambhv Steel Tubes Q3 FY26 Earnings Preview

Based on Q2 actuals management commentary Q3 volume update, Sambhv is set up for its strongest profitability quarter so far, despite flat headline volumes.

What changed in Q3?

• Total volumes largely flat QoQ

• Value-added products hit record levels

• Stainless steel volumes 16% QoQ

• Sharp reduction in low-margin intermediate products

→ Mix improvement, not volume growth, is the story.

Margin setup looks meaningfully better vs Q2

Q2 margins were impacted by:

• Monsoon-related raw material moisture

• Higher intermediate product share

Management has already indicated ~13% EBITDA margin as sustainable beyond Q2.

Q3 FY26 estimated financials (base case):

• Revenue: ₹600–620 cr

• EBITDA: ₹75–85 cr

• EBITDA margin: 12.5–13.5%

• PAT: ₹40–45 cr

(Compared to Q2: ₹580 cr revenue, ₹60 cr EBITDA, ₹30 cr PAT)

Why Q3 should outperform Q2:

• Stainless steel utilization approaching ~90%

• GP & structural pipes operating near peak efficiency

• Lower finance costs post IPO

• Seasonal margin normalization

This is shaping up as a margin expansion quarter, not a volume-led one.

Investor lens:

Sambhv continues to execute its shift toward higher-value, higher-margin steel products, with operating leverage now starting to show up in numbers.

Disclosure:

- Sambhv is part of my long-term portfolio.

- This post is not a buy/sell recommendation.

- Please do your own due diligence.

1

5

241

Jan 3

Project 2100 type Long Range Patrol Craft(LRPC) of the Brotherly Nations Cosmic Fleet (FKBN). It served mostly with the Exosphere Command and in several civilian roles. While it possessed a limited offensive capability, its main role was space surveillance and early warning

7

55

499

33,003

Jan 2

Follow @bigbullonnifty For Stock Updates :-

OLECTRA:

CO LOWER DELIVERY GUIDANCE LOWER TO 1500-2000 UNITS FROM 2000-2500 UNITS FOR FY26: NDTV

PETRONAS SETS MCO OIL OFFICIAL PRICE AT $69.53/BBL FOR DECEMBER

MUTHOOT FINANCE | MANAGEMENT COMMENTARY – CNBC-TV18

• Continues to see strong growth momentum in Q3

• May revisit FY guidance during Q3 results

• Loan-to-Value (LTV) at ~57%

• Comfortable with current LTV; comfortable even up to 75%

• Demand remains strong across both rural & urban markets

• Yields likely to stabilise as competition increases

• NIM can improve through tight cost control, even if yields don’t rise

• Regulatory environment supportive for gold loan business

BHARAT FORGE MGMT to NDTV PROFIT

Saw Many Unexpected Events In 2025

Have Chalked Out A Plan To Focus On Growth In 2026

Increasing Play In Industrials Sector Key Focus

Doubling Down Focus On Automotive Business

Looking To Build Defence Business Into One Huge Platform

Confident Of ₹2,000 Cr Revenue In Defence On 4-Quarter Basis

CHINA DEFENSE MINISTRY:

URGES RELEVANT COUNTRIES AND INSTITUTIONS TO STRICTLY ABIDE BY THE ONE-CHINA PRINCIPLE, STOP SUPPORTING "TAIWAN INDEPENDENCE" FORCES, AND "STOP STIRRING UP TROUBLE" ON THE TAIWAN STRAIT ISSUES

FROM ZEE BUSINESS

IREDA: IN BUDGET 25-30% INTELLECTUAL ASSISTANCE POSSIBLE FOR SMALL HYDRO PROJECTS

THE BUDGET CAN BE INCREASED BY 3X TO RS 40000 CR

QUANT MF ON DEFENCE

See Defence Story Playing Out Over 5-6 Years

Valuations For Defence Stocks Remain Expensive

Govt likely to stick to February 1 for Union Budget presentation: Sources to CNBCTV18

🚩Alert: Official announcement on Budget Session dates awaited

TATA Power: block deal of 46.9 Lk shares

ELECTRONICS COMPONENT PLI SCHEME

Govt Approves 22 Investment Proposals Under Electronics Component PLI

Approvals Of 22 Projs Likely To Result In Invst Of ₹41,863 Cr

Approvals Of 22 Projs Likely To Create Nearly 37,000 Jobs

Output From 22 Approved Projects Likely At ₹2.58 Lk Cr

SAMVARDHANA MOTHERSON, BPL ; BPL and Motherson Electronics' applications under the PLI scheme have been approved.

INDIGO , SPICEJET ; 68 Flights Cancelled As Of Now At New Delhi : Sources - NDTV PROFIT

DIXON TECH: Dixon Application For camera module PLI Also approved

TATA Steel: block deal of 10.1 Lk shares

IDBI BANK:

FINANCIAL BIDS FOR IDBI BANK DISINVESTMENT SOON - ZEE BUSINESS

IDBI BANK ; 11.3 LKH SHARES EXCHANGED VIA BLOCK DEAL

MINISTER ASHWINI VAISHNAW SAYS 4 COMPANY WILL START PRODUCING SEMICONDUCTOR CHIPS IN 2026 SAYS

KAYNES

MICRON

CG ELECTRONICS

TATA ELECTRONICS

NTPC :

Co Exploring International Collaborations In Tech & Fuel To Push Nuclear Plans: Sources To PTI

MARUTI SUZUKI Says Need EV-like policy push to make flex-fuel viable

Policy uncertainty clouding flex-fuel invest plans

SHREE CEMENT ; Corp Affairs Min Seeks Certain Info From Company, Which Will Be Provided In Due Course

Marico Q3 Update;

▶️Volume Growth In India Business In High-single Digits

▶️Intl Business Constant Currency Growth In The Early Twenties

▶️Cons Revenue Growth In The High Twenties YoY

▶️Copra Prices Corrected 30% From Highs, Expected To Move Lower Further

▶️Expect Operating Profit Growth To Touch Double Digits YoY

Punjab National Bank | Provisional Business Update (Dec 31, 2025)

• ₹28,92,630 Cr ↑9.57% YoY – Global Business

• ₹16,60,385 Cr ↑3.11% YoY – Domestic Deposits

• ₹11,67,801 Cr ↑8.32% YoY – Domestic Advances

• 74.21% – Domestic CD Ratio (as of Dec 31, 2025)

Summary:

Steady growth in global business and advances, while deposit growth remained modest. Figures are provisional and subject to audit review.

SEBI CHAIRMAN:

DEVELOPING AI TOOL FOR RISK BASED SUPERVISION OF MARKET INTERMEDIARIES

MARKET AT CLOSE

Market Hits New High, Nifty Is Back Above The Level Of 26,325

Broader Mkts Move In-line, Nifty Bank & Midcap Index At Life Highs

All The Sectors Except FMCG Post Gains, PSU Top Gaining Index

Sensex Rises 573 Points To 85,762 & Nifty 182 Pts To End At Life High Of 26,329

Nifty Bank & Midcap Index Post Record Highs, End With A Gain Of 1% Each

Nifty Bank Gains 439 Points Το 60,151 & Midcap Index 616 Points Το 61,366

UNION BANK: POSTS STEADY ADVANCES GROWTH IN Q3 FY26; CASA & RAM MOMENTUM STRONG

Gross advances rose 7.13% YoY to ₹10,16,805 Cr as of 31 Dec 2025.

Domestic advances up 7.42% YoY to ₹9,80,643 Cr, driven by retail and corporate segments.

RAM advances grew 11.49% YoY to ₹5,77,006 Cr, while CASA deposits increased 4.99% YoY, with CASA ratio at 33.95%.

Credit–deposit ratio improved to 80.94%, reflecting stronger credit deployment.

BANSAL WIRE Q3 BIZ : HIGHEST-EVER Q3 SALES VOLUME

• 1,21,702 MT ↑ 31.7% YoY | ↑ 6.18% QoQ — highest-ever quarterly volume

• 3,40,411 MT (9M FY26) ↑ 37.88% YoY

• Growth driven by expanded 6,18,000 MTPA capacity and strong auto & infra demand

• New capacities added: LRPC Wire 18,000 MT | IHT Wire 9,000 MT

🟢 Impact: Positive

DMART Q3 BIZ : STRONG SALES MOMENTUM CONTINUES

• ₹17,612.6 Cr revenue ↑ 13.2% YoY in Q3 FY26

• Store network expanded to 442 stores (1 under reconstruction).

• Steady revenue scale-up over 3 years, reflecting consistent execution.

CEIGALL INDIA: CO TO BUY 100% OF VELGAON POWER TRANSMISSION

RBI: Forex reserves at $696.6 bn in Dec 26 week, rise $3.29 bn

Tesla Q4 Deliveries 418,227 (est 440,907)

- Production 434,358 Vehicles (est 470,780)

- Model 3/Y Deliveries 406.585 (est 421,796)

- Model 3/Y Production 422,652 (est 452,494)

- Other Models Deliveries 11,642 (est 16,959)

- Other Models Production 11,706 (est 17,810)

- 2025 Total Deliveries 1.64Mln Units, Production 1.65Mln Units

2

9

239

18 Nov 2025

Proud to support Pune Metro’s new veena-shaped Pedestrian Cable-Stayed Bridge with our HDPE-coated LRPC strands.

A landmark design, Pune’s longest flyover, and the first cable-stayed pedestrian bridge over the Mutha River.

#UshaMartin #lrpc #infrastructure #engineering

4

333

12 Nov 2025

อันนี้เห็นด้วยค่ะ น้องพูดเบรคกิ้งฮาวได้เลยทุกงานเราก็ชอบแต่ก็อยากให้น้องพูดโมเม้นต่อด้วยว่ารู้สึกยังไงเหมือนในไลฟ์เมื่อวานของLRPC ที่น้องตอบคำถามมันยิ่งทำให้เราได้รู้จักและเข้าใจน้องมากขึ้น ได้รู้ถึงความอดทน ความพยายามที่น้องทำมาตลอด ยิ่งทำให้เรารักน้องมากขึ้นทุกวัน

1

1

7

1,912

2 Oct 2025

J0H5-WHSKK-H7QV

8YZ7-G9Y49-PFJV

D7PQ-30KRW-741W

93EW-YV516-5661

X4X6-RG5R7-7XBF

RKML-N23CB-LWSE

NQ7S-8LYYY-V70R

DHV0-3S2JQ-20Q3

0DHK-CSXD2-EH2H

RQ94-0T7Y2-4G01

DRSQ-0B059-B4NG

H20B-ZZ3PF-DYJN

NZH9-S37VJ-8ZM7

RSPQ-HT6DE-EBES

KWPY-ZVL38-2HX5

GD3W-1PDYC-S9G2

4V6J-T5BJD-0S4T

657N-79DV4-VKCX

VY02-JQWDX-L295

CSPW-HVXZ4-XSBP

GQ8C-PV10N-N6PS

79QX-ESQLG-H22Q

7GKJ-4E56S-FVD9

XXLK-6J8DW-S7Y8

82F7-N6H4D-BS0S

1V4L-XXM5K-L9SL

5T80-DF6SP-H9BL

NTZR-3DWVZ-RZZ6

C08R-BQ52S-T8RX

TYZ9-DZ1VK-CJDL

8J53-RGVV1-7DVL

K2FG-HSKC3-5SZ4

JQ12-BZ9QX-0RSV

SQNX-2PSW6-77EJ

RM8K-GS3NX-WB72

88TB-FFHWN-1K3Z

M4VN-JCKCP-M3HV

71H2-58PTM-JXM1

RV3Z-HK5NJ-QRTX

PLC8-GM1VN-2WR7

HZ8B-H7RH4-61KD

VD3V-L98G1-VDXJ

VZWC-63SEG-6XZ7

RZ60-TYC56-QT7V

5Q33-8YZ9Y-H11G

4CQL-HEJPT-VHQF

1ML1-VR4YX-12K0

T5QN-YFBWL-R134

E6T4-5K6SX-VC48

M8ZB-BF2PL-SX0Q

Y8WQ-SK5YK-8H68

BFVQ-E7GSJ-VSWB

0L2L-G0RS0-D4NR

FDR9-HBQ1T-BW9V

FE0P-5W0G8-HTHP

QGNN-KBE7Y-Y650

D38B-10SDL-Q075

KFKM-17BKP-P0WL

8EHD-8WHZH-JND6

XVBX-YFWFE-2SCB

99K8-TD64G-WP02

K98J-JZ861-DV16

8NY1-EKHVR-14EV

0QZ4-TK0GD-0YYG

GQEP-PJXRG-3FYX

LRPC-67SDC-TGJZ

3S62-NQETJ-8M3T

B8CS-DB5FQ-V5DQ

9HH6-00S9G-4H7N

E127-36FZC-PJZ7

D4TM-WLP5V-426F

0YL1-G9E83-6REF

LM29-7NJ95-MJHT

EXTS-HC6S9-HKFG

KQ26-TGM8R-4061

DRHS-6H2SL-KXC2

MR98-97ZP6-GYLH

PVHX-1SLSB-3CM1

XYPG-F0V40-GHML

FNHW-PK2CL-8EJ2

VCGY-R1ZWG-8Q4B

NRDL-Z1353-54JN

LDK4-JT4EM-KKVS

EPG1-36YEM-WV1E

4

717

26 Sep 2025

Seamec Limited – Q1 FY26 Investor Snapshot

Key Highlights:

- Revenue: Rs. 887 crore ( 7.4% YoY)

- Fleet Utilization: 93% efficiency, strong execution across vessels

- Segment Growth:

- Wire: Rs. 641 crore ( 32.3%) driven by auto & niche products

- Wire Rope: Rs. 639 crore, 7.9% YoY, core growth driver

- LRPC: Rs. 30 crore (-3.4%), shift to higher-margin plasticated LRPC

- EBITDA: Rs. 145 crore; Margin: 16.3% (down from Rs. 154 crore YoY)

- Net Profit: Rs. 101 crore (vs Rs. 104 crore YoY)

- Cash & Debt: Net cash Rs. 14 crore (vs Rs. 63 crore debt in Mar’25), now debt-free

Strategic & Operational Highlights:

- Fleet Expansion & Fleet Renewal: Acquisition of Nusantara on track; focus on younger vessels for efficiency & lower OPEX.

- Vessel Deployment: Long-term contracts with major clients (Saudi Aramco, UK, Middle East).

- International Focus: Expanding in Middle East (UAE, Saudi, Qatar); UK project delayed but minimal cost impact.

- New Ventures: Partnered with Arete Shipping (GIFT City JV) with 15-16% returns; strategic divestments of non-core assets ongoing.

Guidance & Outlook:

- Margin: Targeting 18% EBITDA margin for FY26, with potential 19-20% in FY27 through fleet renewal & margin accretion from high-value contracts.

- Growth: Sector tailwinds support continued strong offshore oil & gas cycle; focus on margin expansion and fleet optimization.

- Order Book & Visibility: Robust pipeline with long-term charters supporting revenue stability and growth.

Key Triggers:

1. Successful vessel acquisitions & deployment (Nusantara & Anant)

2. Expansion into high-margin Middle East & international markets

3. Fleet modernization & replacement to reduce OPEX & improve reliability

4. Continued focus on offshore support vessel (OSV, DSV) value-accretive contracts

5. UK subsidiary project completion & cost management

1

93

26 Sep 2025

Usha Martin Limited – Q1 FY26 Investor Snapshot

Key Highlights:

- Revenue: Rs. 887 crore ( 7.4% YoY)

- Volume Growth: 10.4% YoY across segments

- Wire Segment: Rs. 641 crore ( 32.3%) driven by auto & niche products

- Wire Rope: Rs. 639 crore (72% of revenue), 7.9% YoY, strong export prospects

- LRPC: Rs. 30 crore (-3.4%), shifting focus to higher-margin plasticated LRPC

- EBITDA: Rs. 145 crore; Margin: 16.3% (down from Rs. 154 crore YoY)

- Net Profit: Rs. 101 crore (vs Rs. 104 crore YoY)

- Net Cash: Rs. 14 crore (vs net debt of Rs. 63 crore in Mar’25), now net debt-free

Guidance & Outlook:

- EBITDA Margin: 18% target for FY26, with potential for 19-20% in FY27

- Capacity Expansion:

- Ranchi: 40,000 MT additional capacity by Q2 FY26

- Thailand: Rs. 60 crore investment ongoing

- Margin Drivers: Higher export mix, focus on high-margin products (elevator, crane ropes, synthetic slings), cost control, and capacity ramp-up

- Growth Targets:

- Revenue: 10–15% YoY growth incl. demand recovery

- Margin: Path to 18% EBITDA margin

- Product & Market Focus: US, Europe, Middle East, India

Key Triggers:

1. Oceanfibre Synthetic Slings: Rapid traction & demand across offshore & high-value applications, expected to be a significant vertical in 18-24 months

2. Global Market Expansion: Strengthening presence in US, Europe, Middle East with focus on high-margin segments

3. Cost Optimization & Transformation: Full benefit from Rs. 80-100 crore programme from Q3 FY26, improving margins & cash flow

4. Capacity & Product Innovation: Expanding high-margin product lines, ramping international capacity, and optimizing supply chain

Risks & Challenges:

- Tariff volatility & global trade tensions

- Cyclical/structural pressures on LRPC segment

- Competitive landscape in key markets, although Usha Martin leverages technical & R&D advantages

1

98

4 Sep 2025

Proud to power Pune Metro’s iconic Veena-shaped Cable-Stayed Pedestrian Bridge with our HDPE coated LRPC strands. A milestone in modern engineering, supporting 2 lakh daily commuters across the Mutha River.

1

3

98