Fly the maxed out skies dailykos.com/stories/2026/6/…

cmoonshinez.. retweeted

Pineapple Fusion aka (Humboldt Pineapple x Lemon Tree) x Red Velvet s1 reversed

Way too much maxed out tropical pineapple terp profiles in these. Insane bag appeal and super unique. Leans heavy on the sativa side.

Shout out to @humboldt_csi for the mom used, always fun to search through his work.

Feel free to repost if you enjoy my work.

2

48

494

I think the only reason I'm okay with it in FF7R is because it expects you to be maxed level with all materia unlocked for its hard mode to function how it does (and tends to be more rewarding) but yeah they're weird about it sometimes.

3

Bro I agree. I can't even run 1 maxed out prompt on Claude free lmao

7

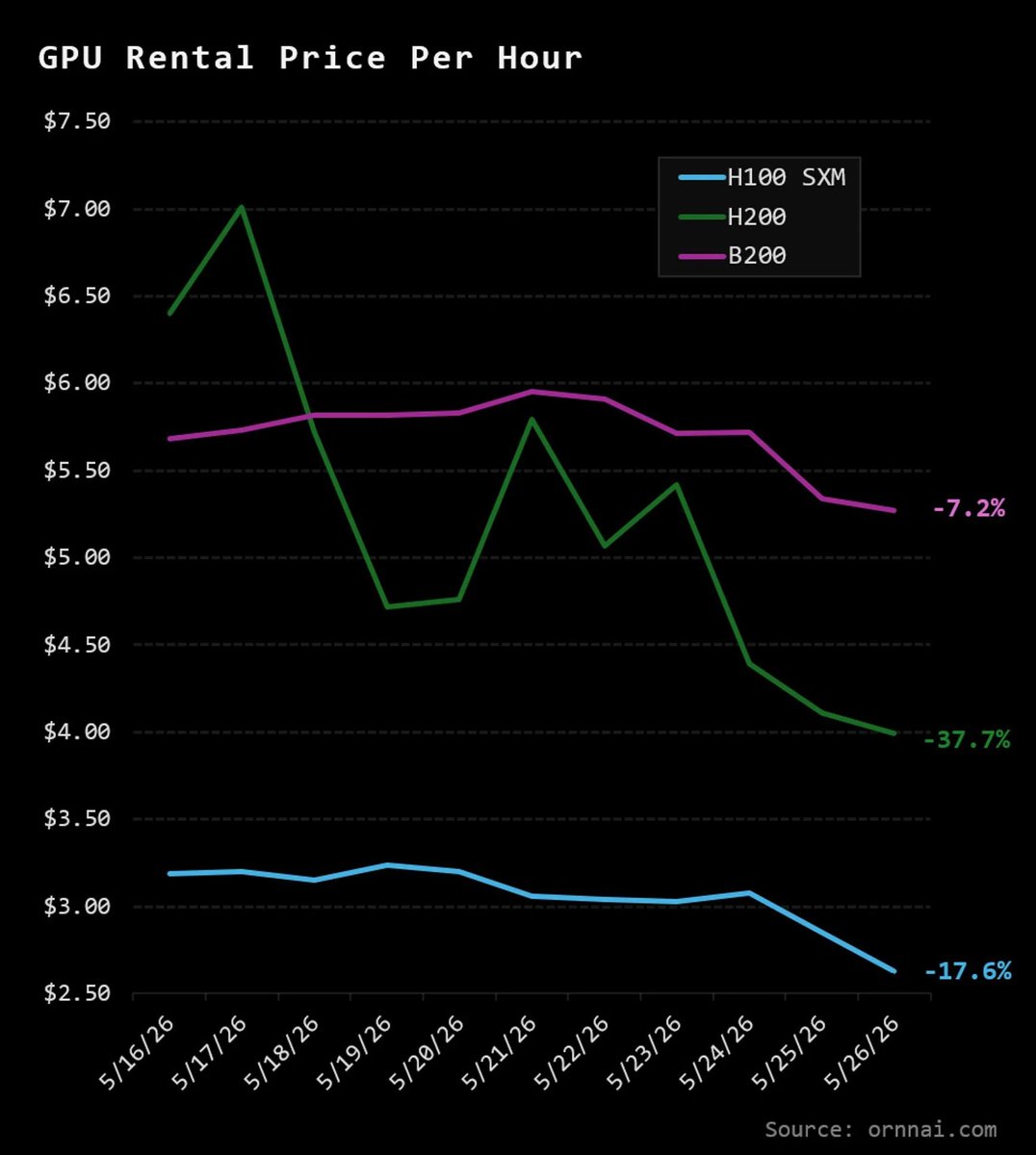

There's one number that quietly decides whether the entire AI buildout actually makes money — and once you see it, you can't unsee it. So let's do the math, with real figures.

Building a one-gigawatt AI data center costs about $38 billion. The chips — the Nvidia accelerators that do the work — are the single biggest slice: roughly $20 billion, over half. The rest is the building, the power, the cooling, the networking.

Here's the catch. The building and the power last 15-20 years. The chips? Effectively obsolete in about three. $NVDA ships a faster generation on a relentless cadence, and older chips lose 40-60% of their value within 18-24 months of the successor arriving.

So more than half of the most expensive thing humanity is building right now melts in three years. Picture a $38B warehouse where $20B of it is ice sculptures.

That used to be fine — because the rent was insane. In 2023-24, an Nvidia H100 paid for itself in under a year. Easy money.

Then everyone built. Capacity flooded in and the rent collapsed: H100 rental rates are down roughly 64-70% from their peak, to around $2-4 an hour. At those prices the payback period has stretched from under a year to seven-to-ten years — on an asset that's obsolete in three. You can't earn back a three-year chip over ten years of rent. At today's prices, the math just doesn't close.

Don't take our word for it — read the purest example's own filings. $CRWV does nothing but rent GPUs. Last quarter revenue grew 112% to $2.1 billion. Spectacular, right? Except depreciation alone — the chips wearing out — ate $1.15 billion, more than half of all revenue. The result: a $740 million net loss. Booming demand, losing money on every dollar, because the melting eats more than half the rent.

Then there's the accounting. Most big players write these chips down over five or six years, not three — which makes reported profits look fatter than the cash reality. One prominent short-seller estimates roughly $176 billion of "missing" depreciation across the industry through 2028 — enough to flatter the reported profits at names like Oracle by 20% .

The demand is unquestionable. But the returns, at today's collapsed rents and honest depreciation, are underwater for the pure players and propped up by generous depreciation schedules for the big ones.

This is exactly why our system keeps rejecting the debt-funded builders. $ORCL sits below our quality floor not because demand is weak — but because borrowing tens of billions to buy a melting asset whose rent is falling is a fragile way to make money.

To be fair to the other side — and we always try to be — this flips if a few things go right: if rental prices stabilize as demand finally outruns the supply glut, if the chips stay useful past three years (older ones still rent), and if utilization stays near-maxed. Any of those, and the math closes again.

But the honest read today: the prettiest demand story in tech is sitting on the fastest-melting asset in tech, and the rent is heading the wrong way. So forget revenue growth — everyone has that. Watch one thing: whether GPU rental prices stop falling. The day they stabilize is the day this becomes a business instead of a race.

Would you borrow billions to buy something half-gone in three years — while the rent keeps dropping?

10q.capital/feed

1

37

This fucking bitch on #loveafterlockup is pissing me off. She maxed out all of her boyfriend’s credit cards while he was in jail and purchased a new car. He got out of jail thinking he had money but she spent everything and said it’s his problem because their his cards

5

Thank you to my new followers, and 👋 I will follow everyone back as soon as possible. I’m maxed out for today

👋 I’m a watercolour artist trying to build connections on X. I’m looking for fellow artists and creatives to follow! Writers, songwriters, musicians, painters, game creators etc, please follow me I want to see your creativity!

I follow back!

1

7

Iya sih🥀 malaz ah, kukira main Enfield bkl buat gk bosan lg, ehhh dah lv 60, pabrik all maxed, akhirnya sama jg kek Wuwa 😂🤣 pengen pelan2 main, tp gk sabaran jg 🥀 last option adalah nunggu silver palace dan Ananta. Kamu keknya dah gk login 8 hari btw

1

1

11

Thank you, great shout! I will follow her soon as I can again, maxed out for today

3

lia . ꪆৎ 🍋 retweeted

Ningning maxed out the big-eye filter on live and was shocked by how it turned out.

During her Weibo live, Ningning said she wanted to max out the face-slim filter to see what it’d look like — and she got totally freaked out by the result😆

50

279

6,606

🐐👨🏾🦯 retweeted

Told yall... he's really 5'10 maxed out don't think we understand what we just watched

Btw Jalen Brunson absolutely 5’11 at the most so he one of the greatest we ever seen

18

65

729

83,800

That Time I Got Reincarnated As A Succubus And Maxed Out My Level💜🦇

#prowrestling #wrestling #wwe #professionalwrestling #aew

1

27

213

Me to stay on track and keep practicing when I felt like just leaving it all behind and not keep pushing forward to improve. My 2026 season ends with 560 points. Maxed locals, 1x 512, 2x 256, 1x IC 256, 1x IC T1024 as my major finishes. Looking toy improve upon these for next.

1

2

37