Virpi Sillanpää retweeted

🔸493 nm🔸 553 nm🔸 592 nm🔸 614 nm🔸 649 nm🔸 1761 nm🔸

Modern #Quantum systems require stable, narrow-linewidth laser wavelengths. Read about #SingleFrequency #VECSEL platform designed for Ba, Rb, and Yb applications:

modulight.com/papers/single-…

3

2

236

Terttu Uusimaa retweeted

Our latest publication in #SPIE Digital Library: 795 nm narrow-linewidth MOPA butterfly #laser for:

✔ Quantum sensing

✔ Magnetometry

✔ Raman spectroscopy

✔ Medical diagnostics

modulight.com/papers/integra…

#QuantumTechnology #QuantumSensing #Photonics #SemiconductorLasers

2

4

329

Jun 5

Sitähän se luultavasti. Siverssit oli katseltu sivusta ja luultavasti ajateltu, että Canatu, Aspocomp ja Modulight täytyy pian saada osansa. Aspolla on ihan samannäköinen kurssi.

4

328

Jun 1

Xioxia of course, and maybe Modulight, $BRUN and Canatu.

Not my ideas so can't verify the r/r but seeing them being discussed in some high quality circles.

1

2

428

May 31

如果你在 Serenity 之前买了 $SIVE,你赚了 1,800%。这周之前抓住 $XFAB,你一天赚 70%。

坐在真正瓶颈上的欧洲半导体公司,正被一个国家接一个国家地发现。美国涨了。瑞典涨了。德国涨了。芬兰还没。四家坐在同样咽喉要道、却仍横盘的芬兰公司:

$CANATU。每一颗先进芯片都要经过 ASML 的 EUV 光刻机,而每台机器里都有一个消耗性部件,随着机器越来越强大正撞上物理天花板。Canatu 做的就是下一代版本。真正的核心是它的模式:卖反应炉、卖只有自己能供应的专有原料,然后对每一个产出的单元永久收取版税。轻资产、经常性、高利润。2025 年 10 月通过韩国伙伴 FST 实现商业化,而三星持有 FST 股份。这不是垄断(三井在竞争),但它是没有晶圆厂想缺的可靠第二供应源。新任 CEO 来自 Soitec,正是从实验室到量产所需的能力。目前仍亏损,回报期推迟到 2030 年。多年期持有。

$ACG1V(Aspocomp)。AI 服务器里的一切都要落在 PCB 上,而高盛把 PCB 和覆铜板列为真正的瓶颈,价格每年涨 30% 以上,短缺持续到 2027 年。Aspocomp 是少数拥有国防和半导体认证的欧洲制造商,正是欧盟芯片法案想回流的。订单簿创纪录,延伸到 2027 年底。但规模很小(市值约 3000 万欧元),单一工厂,且波动大:订单创纪录的同时销售却下滑。这是一个回流押注,不是干净的复利标的。

$MODU(Modulight)。坦佩雷的激光制造商,垂直整合,自营晶圆制造、激光组装、光学校准全在同一屋檐下,对它的规模来说很罕见。目前核心收入来自医用激光,但它净现金、以股权为主、无被迫稀释,并正转向经常性的按次治疗收费模式。光子学、国防光学和量子方面的角度还只是早期期权,尚非核心。不确定的变数,但是一家位于北约国家的盈利公司。

$NOK。概念验证。沉睡了十年,直到收购 Infinera 光网络业务把它接入数据中心内部移动数据的网络后,市场把它重新定义为 AI 基础设施。从低点大约翻倍。已经被发现了,而这正是关键:另外三家还没。

注意力依次经过美国、瑞典、德国,每一步都触及了瓶颈标的。Nokia 是芬兰已经发生这一幕的名字。另外三家还在等待。同样的瓶颈,同样的顺风,关注度却只有一小部分。

更深入的拆解在 Substack 上。非投资建议,请自行研究,我持有部分。

8

4

70

18,403

For over two decades, we’ve pushed laser innovation to advance healthcare, #lifesciences, and beyond—from #oncology and #ophthalmology to #quantum tech. As Modulight turns 26, we celebrate the journey and impact. Let’s move forward together to #KillCancer. 🧡

3

2

379

May 29

Yes here they are.

$CANATU. CNT pellicle technology for next-gen EUV. Licensing model with FST live since Oct 2025, Samsung-owned. The "second door" the entire chip supply chain needs once power scales past where composite pellicles work.

$ACG1V (Aspocomp). Tiny Finnish PCB maker, ~€30M market cap, record order book in defense and semi. Right place as Europe re-shores, real warts on execution. Small and scrappy.

$MODU (Modulight). Tampere photonics, vertically integrated laser fab. Mostly medical today, real optionality on defense optics and quantum. Earlier in my work, but worth watching.

$NOK. Already found. Re-rated when the market connected it to AI optical networking via Infinera. Proof of concept for the whole pattern.

1

3

9

4,345

May 29

Nailed on $SIVE!

Check Modulight ($MODU). Ask yourself: how many genuine in-house semiconductor laser fabs are actually left in Europe?

EU Chips Act 2.0 is coming. This could give a real boost to the few companies that already have their own fab, IP, and European base.

2

2

6,236

May 29

Solid write-up on $SIVE and the InP laser momentum.

Quick one for you, take a look at Modulight. Then ask yourself: how many true in-house semiconductor laser fabs are actually left in Europe? EU Chips Act 2.0 is coming. That could be a real tailwind for the few players who already have the fab, the IP, and the European base.

2

721

May 28

You're missing Modulight $MODU.

• Core business: medical lasers (oncology, dermatology)

• But they also run their own semiconductor laser chip fab in Tampere (62k sq ft, $50M upgrade)

• Supplying quantum, defense, semiconductor companies

• EU Chips Act 2.0 prioritizes photonics → PIXEurope pilot line

• Finland's own hidden photonics bottleneck

Medical revenue now policy tailwind for the chip fab. Worth a look.

2

1

10

1,608

May 28

Most people look at $MODU and see a medical laser company.

They have their own semiconductor laser chip fab in Tampere, Finland. 62,000 sq. ft. Fully vertically integrated. $50M invested. ISO5 cleanrooms. This isn't a distribution deal, it's real manufacturing.

What do they actually build?

Lasers from UV to 3000 nm. Fiber lasers, VCSELs, DBRs, solid-state. Applications:

- Quantum computing

- Semiconductor metrology (wafer inspection)

- Flow cytometry, diagnostics, defense

The ML6600 platform powers it all

The financial picture: Q1 2026 sales €2.44M, net loss €0.96M (improved from €1.62M loss a year ago).

EBITDA margin hit 22% in Q1. Revenue declined 7% YoY but cost structure improved. Pay-Per-Treatment business grew >100%.

Strategy 2026–2027: strong revenue growth → return to profitability → positive cash flow.

The real tailwind: EU Chips Act 2.0 prioritizes photonics as a high-growth semiconductor technology alongside quantum, MEMS, and advanced materials.

Finland's "Chips from the North" strategy aims to triple semiconductor revenue to €5–6B by 2035, explicitly naming photonics as a core growth area.

Business Finland's chip program FiCCC helps local fabs like Modulight access pilot lines and EU funding.

Verdict: $MODU sits at a policy-driven intersection — semiconductor fab quantum exposure photonics in focus EU sovereignty push.

Not profitable yet. But the physical assets exist, the customers include Fortune 500s, and the EU is writing checks for exactly this sector.

If execution follows, the thesis holds.

Not financial advice. Do your own DD.

9

377

May 23

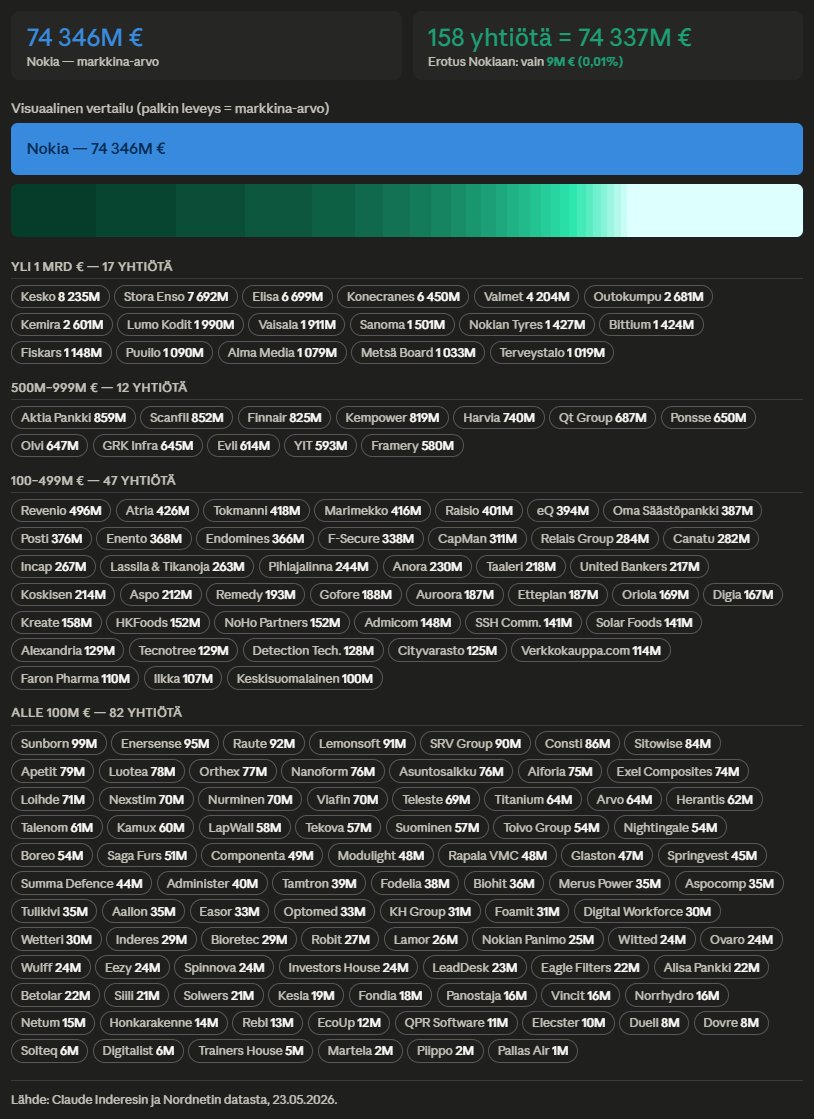

Nokia on Helsingin pörssin mittakaavassa melkoinen järkäle. Sen markkina-arvo on noin 74 miljardia euroa. Se on enemmän, kuin nämä Helsingin pörssin 158 yhtiötä yhteensä:

Kesko 8235 M€

Stora Enso 7692 M€

Elisa 6699 M€

Konecranes 6450 M€

Valmet 4204 M€

Outokumpu 2681 M€

Kemira 2601 M€

Lumo Kodit 1990 M€

Vaisala 1911 M€

Sanoma 1501 M€

Nokian Tyres 1427 M€

Bittium 1424 M€

Fiskars 1148 M€

Puuilo 1090 M€

Alma Media 1079 M€

Metsä Board 1033 M€

Terveystalo 1019 M€

Aktia Pankki 859 M€

Scanfil 852 M€

Finnair 825 M€

Kempower 819 M€

Harvia 740 M€

Qt Group 687 M€

Ponsse 650 M€

Olvi 647 M€

GRK Infra 645 M€

Evli 614 M€

YIT 593 M€

Framery 580 M€

Revenio 496 M€

Atria 426 M€

Tokmanni 418 M€

Marimekko 416 M€

Raisio 401 M€

eQ 394 M€

Oma Säästöpankki 387 M€

Posti 376 M€

Enento 368 M€

Endomines 366 M€

F-Secure 338 M€

CapMan 311 M€

Relais Group 284 M€

Canatu 282 M€

Incap 267 M€

Lassila & Tikanoja 263 M€

Pihlajalinna 244 M€

Anora 230 M€

Taaleri 218 M€

United Bankers 217 M€

Koskisen 214 M€

Aspo 212 M€

Remedy 193 M€

Gofore 188 M€

Auroora 187 M€

Etteplan 187 M€

Oriola 169 M€

Digia 167 M€

Kreate 158 M€

HKFoods 152 M€

NoHo Partners 152 M€

Admicom 148 M€

SSH Communications Security 141 M€

Solar Foods 141 M€

Alexandria 129 M€

Tecnotree 129 M€

Detection Technology 128 M€

Cityvarasto 125 M€

Verkkokauppa 114 M€

Faron Pharma 110 M€

Ilkka 107 M€

Keskisuomalainen 100 M€

Sunborn 99 M€

Enersense 95 M€

Raute 92 M€

Lemonsoft 91 M€

SRV Group 90 M€

Consti 86 M€

Sitowise 84 M€

Apetit 79 M€

Luotea 78 M€

Orthex 77 M€

Nanoform 76 M€

Asuntosalkku 76 M€

Aiforia 75 M€

Exel Composites 74 M€

Loihde 71 M€

Nexstim 70 M€

Nurminen 70 M€

Viafin 70 M€

Teleste 69 M€

Titanium 64 M€

Arvo 64 M€

Herantis 62 M€

Talenom 61 M€

Kamux 60 M€

LapWall 58 M€

Tekova 57 M€

Suominen 57 M€

Toivo Group 54 M€

Nightingale 54 M€

Boreo 54 M€

Saga Furs 51 M€

Componenta 49 M€

Modulight 48 M€

Rapala 48 M€

Glaston 47 M€

Springvest 45 M€

Summa Defence 44 M€

Administer 40 M€

Tamtron 39 M€

Fodelia 38 M€

Biohit 36 M€

Merus Power 35 M€

Aspocomp 35 M€

Tulikivi 35 M€

Aallon 35 M€

Easor 33 M€

Optomed 33 M€

KH Group 31 M€

Foamit 31 M€

Digital Workforce 30 M€

Wetteri 30 M€

Inderes 29 M€

Bioretec 29 M€

Robit 27 M€

Lamor 26 M€

Nokian Panimo 25 M€

Witted 24 M€

Ovaro 24 M€

Wulff 24 M€

Eezy 24 M€

Spinnova 24 M€

Investors House 24 M€

LeadDesk 23 M€

Eagle Filters 22 M€

Alisa Pankki 22 M€

Betolar 22 M€

Siili 21 M€

Solwers 21 M€

Kesla 19 M€

Fondia 18 M€

Panostaja 16 M€

Vincit 16 M€

Norrhydro 16 M€

Netum 15 M€

Honkarakenne 14 M€

Rebl 13 M€

EcoUp 12 M€

QPR Software 11 M€

Elecster 10 M€

Duell 8 M€

Dovre 8 M€

Solteq 6 M€

Digitalist 6 M€

Trainers’ House 5 M€

Martela 2 M€

Piippo 2 M€

Pallas Air 1 M€

2

2

98

10,498

🔬 Modulight Spotlights: LASER-SHARP RESEARCH – May 2026

This month’s spotlight goes to Nimit Shah and the team from Obaid mION lab at UT Dallas for advancing pancreatic cancer therapy with light-activated, verteporfin-containing liposomes enhanced with SM-102 technology.

1

3

2

394

Proud to sponsor the 43rd Biennial ASP Meeting in Scottsdale, AZ, May 16–19! 🌵✨ Supporting photomedicine and biophotonics is at the core of what we do at Modulight.

Join our webinar, Next-generation Photoactivated Therapies, on June 3, 2026🔬

Register: modulight.zoom.us/webinar/re…

1

2

317