15)As BANDRA LABOUR ADMIN can't given priority towards HC-Lower Court JUDICIALS & ADMIN LIABILITY Norms Fulfilling on LIABILITY a layer as ADVOCATEs r weak to build well Rating values r SEXSEX when in DEPART outsources in priority than Gvt NECESSITY inbuild Layers NIFTY... @RBI

1

Rajiv📈 retweeted

Weekend Market Analysis

✅Overall Market view for 2026 - #Nifty #Banknifty #Smallcap #Midcap #Dowjones and #Nasdaq

✅View on #NiftyEnergy Sector, #Crude, #Gold, #Silver and #Bitcoin

✅Levels and opinions shared are only only learn #Elliottwave and not any buy or sell recommendations. Thanks

✔️English Link - youtu.be/_IS82Kc-c9Q

✔️Tamil Link - youtu.be/i2eww_CG5yM

✅EW and TA Courses - magicfibs.com/

8

7

27

1,669

Two comparisons of #Nifty & Vix are pretty revealing.

Nifty falls from 23296 to 23072. Vix unchanged. Fall was corrective. Confirmed by the rise.

Nifty rises from 23321 to 23645. Vix up by ~3%. Again makes it a corrective rise. Vix should get crushed during an impulsive rise.

1

12

CA Pavan Kumavat retweeted

1

3

168

🚨 HURRY! Price Drop on Portronics 71W Triple Fast Car Charger

Price: ₹610 (MRP: ₹999)

Grab it before it's gone 👇

amazon.in/dp/B0D3DJKVDM?tag=…

#FastCharging #CarCharger #Portronics #PhoneAccessories #nifty #trending #deals #India

4

This is a nifty, actually useful idea.

"Single point of failure" has been an issue for apps in Web3 for as long as I can remember. You should consider adding @Ankr RPCs to this router if you haven't already.

1

7

#KOTAKBANK Long-term Market Analysis | 12 June

Kotak Mahindra Bank shares rose 7% this week, driven by strong trading volume, a bullish technical crossover, and positive sentiment surrounding its status as a blue-chip banking performer.

Key points:

- The stock price rose by 7% over the week, closing at 403.

- Trading volume increased by 28% compared to the previous week, reaching 88,311,531 shares.

- The RSI increased to 67, and the MACD indicator showed a bullish crossover.

Details: faxioms.com/stocks/kotakbank…

#Nifty #Sensex #DalalStreet #IndianStockMarket

1

Dimaag se paidal hi ho ya nifty ke levels dekh dekh k pgla gaye ho..

Middle seat wala agar din mein seat khadi kar de , toh chalega ?

7

500 points can be, but nifty already gained some for that news .so expect 200

27

2/4. In short, the pessimism surrounding the Nifty is unmistakable.

But amid all this gloom and doom, if we are to assess the likely trajectory of the Nifty going forward, we first need to understand how liquidity conditions are evolving across global financial markets.

1

15

WHAT'S NEXT FOR NIFTY: A MELT-UP OR A CRASH? | INDRAANIL GUHA ENGLISH

youtube.com/watch?v=KkoczSG6…

1/4. The Nifty continues to be weighed down by the conflict in the Middle East, relentless FII selling, surging oil prices, and a host of other concerns.

1

21

📈 Earnings Deep Dive,

Delhivery Ltd

#Q4FY26 #Nifty #DELHIVERY

Delhivery achieves profitability and ₹10,000 crore revenue in FY26, delivers a billion parcels! 🚀💰

A deep dive into their Q4 FY26 Concall ⬇️

Delhivery Ltd marked a significant FY26, crossing ₹10,000 crore in revenue from services and delivering over a billion parcels, alongside 2 million metric tons of freight in PTL.

Q4 also saw strong sequential growth in Express volumes.

The company achieved a notable turnaround in profitability, with FY26 adjusted EBITDA reaching 7.3% (₹764 crore) and PAT at ₹347 crore.

Critically, it became free cash flow positive with ₹89 crore, a year ahead of its initial target.

This robust performance, coupled with a strong balance sheet of over ₹4,500 crore in cash, positions Delhivery for disciplined reinvestment into new growth pillars while maintaining capital efficiency and improving returns on invested capital.

🔹 Outlook & Guidance 🎯💡

- Management anticipates e-commerce industry growth of 15-20% in the medium term.

- The competitive landscape is seen as more rational, favoring scaled 3PL providers over 1PL.

- SCS projects must pass an internal hurdle rate, ensuring margin-accretive growth.

- Capex intensity is projected to remain low at around 4%, with AI/robotics not altering this trajectory.

- Transport ROIC is targeted to reach 25% driven by profitability improvement towards 10% adjusted EBITDA.

- Significant investment of ₹130–160 crore is planned for FY27 into new growth pillars, notably intracity logistics.

🔹 Q4 Performance Highlights 📊💰

- FY26 revenue from services reached ₹10,486 crore, with Q4 contributing ₹2,848 crore.

- The company delivered over a billion parcels in FY26, with Q4 Express volumes at 306 million parcels.

- PTL freight volumes hit 2 million metric tons in FY26, and Q4 saw ~549k tons, reflecting 20% growth.

- FY26 adjusted EBITDA stood at 7.3% (₹764 crore), and PAT was ₹347 crore (3.2%).

- Free cash flow turned positive at ₹89 crore, achieving this milestone one year ahead of schedule.

- Express business maintained normative margins of 16–18%, while PTL gross margins expanded from 14% to 28%.

- Supply Chain Services (SCS) revenue was ₹729 crore with a 10.9% service EBITDA margin, marking a decisive turnaround.

- Net working capital days materially improved to 11 days from 38 days three years ago, due to enhanced billing and client selection.

🔹 Management Tone & Strategy 🧭🛡️

- Management attributes strong performance to structural cost advantages and operating leverage.

- Strategic calls included exiting specific non-scalable businesses, like mother warehousing for quick commerce, and renegotiating client contracts.

- Working capital improvement stemmed from faster billing through AI/systems and disciplined client selection based on payment philosophies.

- AI is strategically deployed for operational efficiency in areas like claims automation and PTL paperwork reduction, without increasing tech team size.

- In-house developed AGVs are scaling up in mega gateways to enhance facility movement and address labor market tightness.

- Reinvestment into new growth pillars, particularly Delhivery Direct (intracity/intercity SME logistics), aims to externalize internal capabilities.

- CEO emphasizes a disciplined approach, rejecting past industry "burn/capex frenzy" and focusing on sustainable, profitable growth.

13

🚄 #IRFC – Long Term Setup Building? 👀📈

🔹 Price is respecting a major rising trendline support

🔹 After a long correction phase, stock is trying to build a base

🔹 Current zone around ₹95–100 looks important

🔥 Key levels to watch:

✅ Support: ₹85 - 90 zone

🎯 Sustained can bring fresh momentum Towards 110

Keep on watchlist, confirmation is the key. 📊

#IRFC #StockMarket #Nifty #StocksToWatch #Nifty50 #Breakoutstocks

2

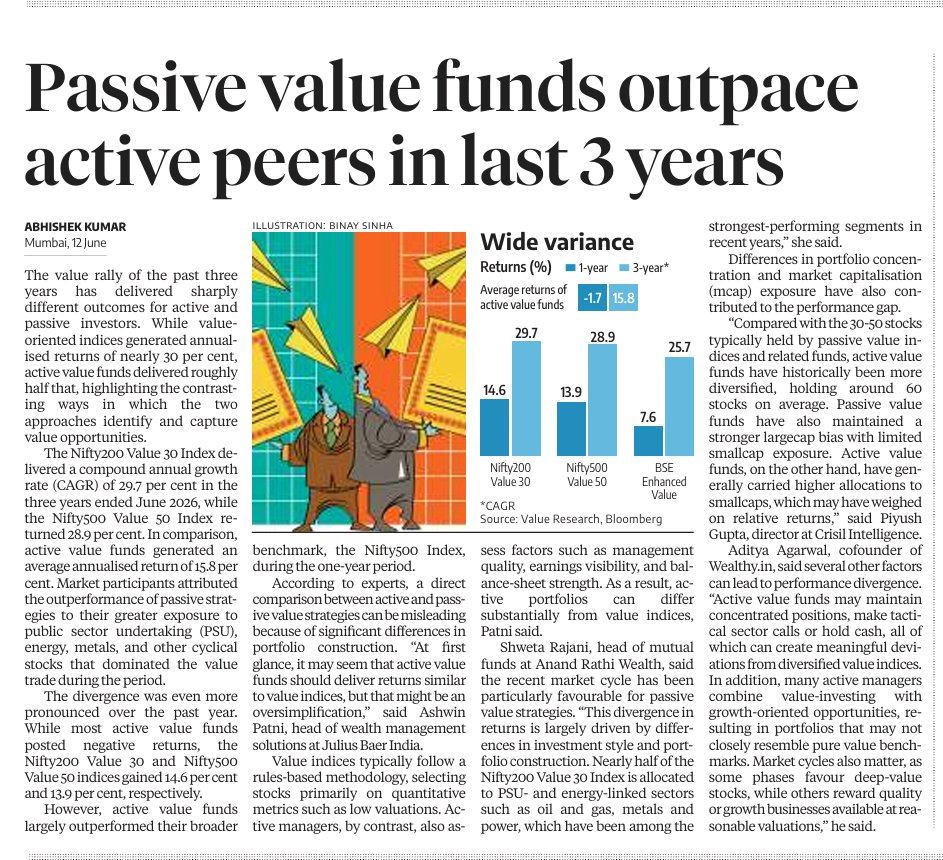

🔍 Passive Value Funds Outshine Active Peers — A 3-Year Wake-Up Call for BFSI

The past three years have delivered a stark verdict in India's value investing space: passive strategies have decisively outperformed active management, and the gap is too wide to ignore.

The Numbers

Nifty200 Value 30 Index: ~29.7% CAGR (3-year)

Nifty500 Value 50 Index: ~28.9% CAGR (3-year)

Active value funds (average): just ~15.8% (3-year), and a negative -1.7% in the last 1 year alone

Why the Divergence?

Passive indices leaned heavily into PSU, energy, metals, and cyclical stocks — segments that dominated the value rally

Active funds maintained more diversified portfolios (~60 stocks vs ~30-50 for passive), with higher smallcap allocations that underperformed on relative returns

Active managers often blend value with growth-oriented bets, drifting portfolios away from pure value benchmarks

Rules-based indices follow quantitative screens (valuation metrics), while active managers weigh management quality, earnings visibility, and balance-sheet strength — leading to fundamentally different portfolio construction

BFSI Implications

Highlights the growing relevance of passive/index-based products in India's evolving MF landscape

Raises questions for wealth managers and distributors on positioning "smart beta" and factor-based funds vs traditional active value schemes

Underscores the need for clearer investor communication on style drift in active value funds

Could accelerate flows toward passive value ETFs/index funds, impacting AUM mix for AMCs

Does this trend signal a structural shift toward passive investing in India, or is this just a phase favoring deep-value over active stock-picking?

#MutualFunds #PassiveInvesting #ValueInvesting #IndianMarkets #BFSI #AssetManagement #Nifty #IndexFunds #InvestmentStrategy #WealthManagement #CapitalMarkets #FinancialServices

3