Jun 11

2/ Their RC2 technology uses electric fields to carry power across solid surfaces. They already shipped the world's first wirelessly powered, window mounted 5G router with NetComm. Power goes through the glass. No drill, no cable.

1

2

515

All’evento Netcomm Focus Food & Grocery 2026 a Milano, Federico Dell'Acqua, Direttore di MarketSuite, la SW Platform di Eng – ha portato la nostra esperienza concreta su come dati, AI e omnicanalità stiano ridefinendo l'esperienza d'acquisto e i modelli.

eng.it/it/solutions/platform…

50

Jun 11

Bakhona Bo Netcomm nabo ifix anon.... however once you've exhausted all the local options if they fail hit me up. I'll plug you with someone who will take to SA for guaranteed fixing🤞🏽libuye lisharp. If li black outile I'd advise you to consider SA unless ke it's something else

2

1

577

May 11

Poste Italiane è stata protagonista al Netcomm Forum 2026 con le soluzioni innovative di logistica integrata e di consegna ideate per rispondere alle ultime tendenze del commercio digitale.

➡️ tgposte.poste.it/tgposte/202…

#TGPoste #PosteItaliane

1

3

364

Great to meet 7 Irish eCommerce companies at Netcomm Forum in Milan with Enterprise Ireland. Ireland ranks 1st worldwide for ICT exports, and this was an excellent opportunity for these indigenous Irish software and AI-focused companies to meet with Italian companies and partners

1

3

48

Apr 28

In occasione della Giornata Nazionale del Made in Italy, ho avuto il piacere di partecipare alla Camera dei Deputati all’evento “Sostenere il Made in Italy nel mondo”, organizzato dal collega On. Alberto Gusmeroli in collaborazione con Netcomm.

PMI, e-commerce e politiche per l’export: tre leve per portare le nostre eccellenze oltre confine. Il Made in Italy si tutela garantendo alle imprese strumenti adeguati e politiche di internazionalizzazione efficaci.

9

21

321

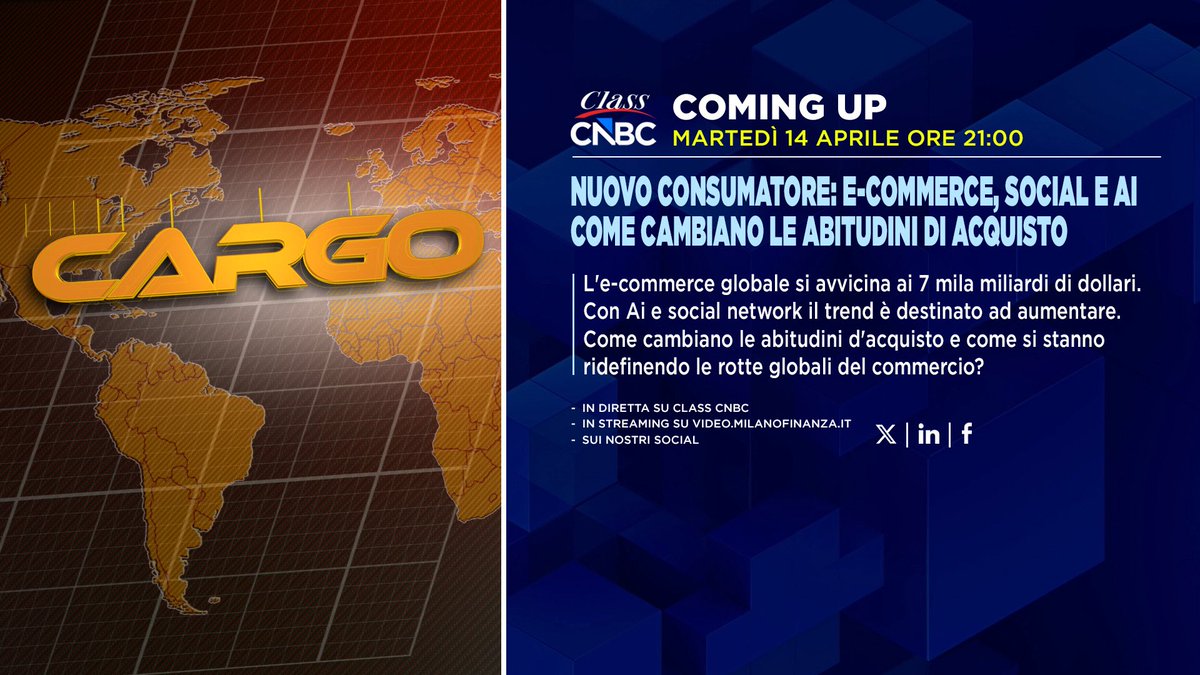

Apr 14

NUOVO CONSUMATORE: E-COMMERCE, SOCIAL E AI COME CAMBIANO LE ABITUDINI DI ACQUISTO

L'e-commerce globale si avvicina ai 7 mila miliardi di dollari.

Con Ai e social network il trend è destinato ad aumentare.

Come cambiano le abitudini d'acquisto e come si stanno ridefinendo le rotte globali del commercio?

Ospiti della puntata di #CARGO

@Robliscia Presidente Netcomm,

Karan Taurani Executive Vice President Elara Capital, Nadia Olivero, Docente di economia e gestione delle imprese Università di Milano Bicocca, Xiaolin Chen, Head of International KraneShares e Alessandro Gandini, Professore di sociologia Università di Milano

Stasera alle 21.00 su Class CNBC e in streaming su video.milanofinanza.it

1

2

406

Feb 9

Photocopier Sales Consultant – NetComm

Minimum 3 yrs photocopier sales experience, good communication skills & driver’s licence required.

Closing: 11 Feb 2026

Apply: jobs.eswazi.org/job/photocop…

#EswatiniJobs #Hiring

1

2

244

🚨 For Sale: Ford Sierra Cosworth RS500

Netcomm inspired Group A RS500, built to the highest specification, using the best ideas & designs from Rouse & Eggenberger etc. Race wins in the UK & Europe🏆

£160k 🏁

#FordFriday | #RS500

(📸 racecarsdirect.com/Advert/De…)

2

20

398

Nah, tuh, dengerin kata Opie, kita harus istirahat! 😮💨 Sampai jumpa di Cerita Komunikasi berikutnya, NetComm friends!

Grafis:

Shakila Ameera Siddik

Takarir:

Nadira Mutiara Rasyantie

Narahubung: Asya (ID LINE: asya11dec)

#CeritaKomunikasi

2

190

COMM ENTHUSIAST: TIME MANAGEMENT VERSI ANAK KOM

Halo, NetComm friends!

Gimana, sih, cara anak Kom manage waktu antara akademik vs. proker yang terkenal banyak? 😵💫

Tenang aja, Opie bakal hadir di sini untuk ngasih tau gimana cara dia manage waktu akademik dan kesehariannya!

2

1

12

522

28 Nov 2025

Comincia il #BlackFriday: 35 milioni di italiani pronti allo shopping online per una spesa complessiva stimata attorno ai 2 miliardi di euro, secondo le stime dell'Osservatorio eCommerce B2C Netcomm-@polimi. Il servizio di Silvana Sempreviva.

1

3

704

Sampai jumpa di Cerita Komunikasi berikutnya, NetComm friends!

Grafis:

Rania Allyssa Syarief

Siti Qeynissa Shafira

Takarir:

Nadira Mutiara Rasyantie

Mona Natalia Christina

Narahubung: Asya (ID LINE: asya11dec)

#CeritaKomunikasi

2

283

25 Oct 2025

💥Haftanın öne çıkanı: $Lantronix ( $LTRX )

🚀 Lantronix’te gelişmeler:

- Drone Pazarı: ABD Ordusu için Teal drone üretimi başladı.

- Telekom: Büyük operatörle 50.000 baz istasyonu modernizasyonu.

- Yazılım: Percepxion platformu ile tekrarlayan gelir potansiyeli 📈

💡 Büyüme Motorları:

- Edge AI: Qualcomm işbirliğiyle uzun vadeli fırsat

- Akıllı Şebekeler: Gridspertise ile İtalya’da dağıtım sürüyor

- 5G: NetComm satın almasıyla Avustralya/Yeni Zelanda pazarına genişleme

💰 Yatırım Görüşü:

Edge AI ve akıllı şebeke trendlerinden faydalanacak konumda. Qualcomm işbirliği ve NetComm entegrasyonu büyümeyi hızlandırabilir. Hisse değerlemesi makul. OLUMLU bakıyorum.

@TradersPub @PubNasdaq

Yatırım tavsiyesi değildir!!!

#Lantronix #EdgeAI #IoT #5G #Yatırım

4

5

20

2,314

14 Oct 2025

They do it by connecting using raw sockets (historically NTSockets) which establishes the connection first, then you can forge whatever you want because you don't rely on DNS. We blogged about the netcomm portion in

proofpoint.com/us/blog/threa…

2

3

96

27 Aug 2025

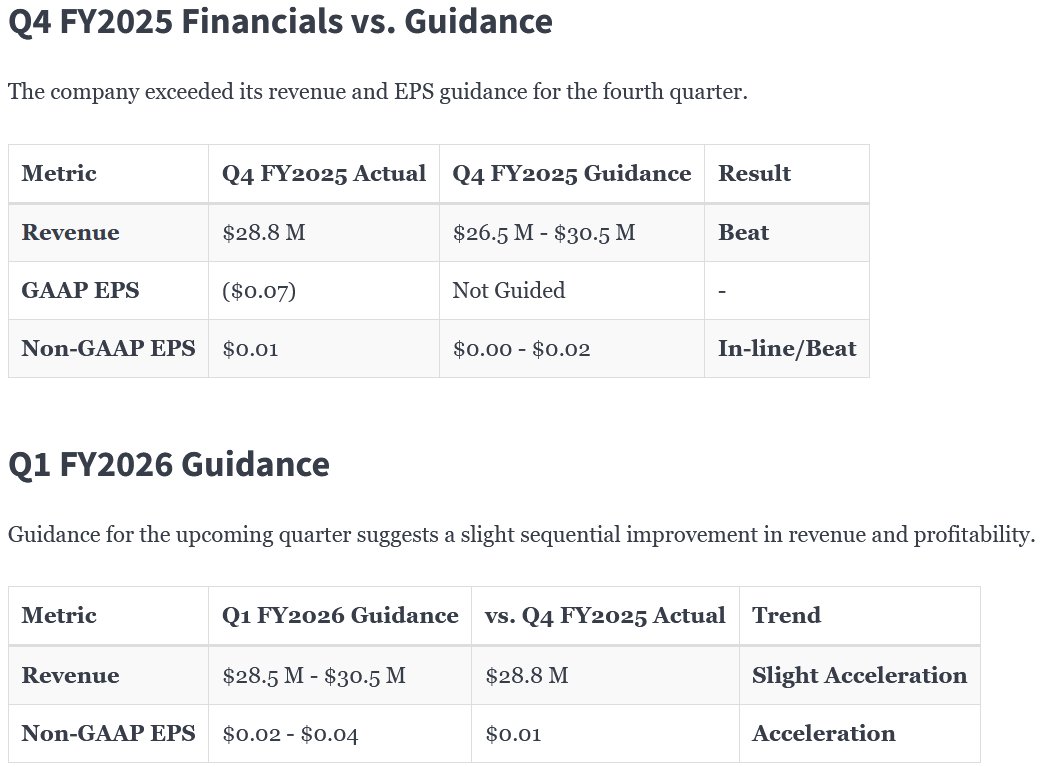

$LTRX earnings:

Lantronix: Strategic Wins Materialize, but Growth Outlook Remains Tepid

Lantronix delivered a solid Q4, beating revenue and EPS guidance while announcing significant new design wins in defense and telecom. The company is successfully executing its strategy to de-risk from its paused smart-grid customer and gain traction in Edge AI.

However, the balance sheet shows some strain with lower cash and equity year-over-year, and the Q1 guidance points to only modest sequential growth. While the strategic progress is encouraging for bulls, the muted near-term financial outlook will keep bears engaged. The story is improving, but the company still needs to prove it can translate these strategic wins into accelerated, profitable growth.

Themes, Drivers, and Concerns

Themes

🟢 Core Business Growth & De-risking: The company continues to successfully grow its business outside of the paused Gridspertise contract. Key wins with a Tier-1 wireless operator and in the defense drone market demonstrate tangible progress in diversifying revenue streams.

🟢 Edge AI Focus Yielding Wins: The strategy to focus on Edge AI is bearing fruit. The selection by Red Cat’s Teal Drones to power a U.S. Army drone with Lantronix’s System on Module (SoM) is a significant validation of this strategy.

🟢 Strengthening Financial Discipline: Despite a lower cash balance YoY, the company has notably reduced its total debt from over $16M to under $12M, strengthening the balance sheet and reducing interest expense.

🟡 NetComm Integration: While a driver last quarter, there was no specific update on the NetComm acquisition’s performance in this release. Its progress remains a key point to watch.

Drivers

🟢 Major New Customer Contracts: The announcement of a “secured multi-year contract with a Tier-1 U.S. wireless operator” is a major highlight. This could provide a stable, recurring revenue stream and potentially smooth out the historical lumpiness in the out-of-band business.

🟢 Penetration of Defense Market: The Red Cat design win for the U.S. Army’s drone program provides a strong foothold in the high-margin, secure defense market, offering a new and promising growth vector for FY26 and beyond.

🟢 New Product Introductions: The launch of the NTC-500 Series industrial-grade 5G routers shows continued innovation and expansion of the product portfolio to address high-growth markets like private 5G and industrial IoT.

Concerns

🔴 Gridspertise Uncertainty: There was no mention of the company’s largest customer, Gridspertise, in the press release. This implies shipments remained at zero in Q4, and the timing for a resumption of orders remains a key uncertainty for investors.

🟡 Balance Sheet Health: While debt is down, key metrics like cash, total assets, and stockholders’ equity have all declined year-over-year. Maintaining liquidity while investing for growth will be critical.

🟡 Modest Growth Trajectory: The Q1 guidance, while showing slight sequential growth, does not yet reflect a significant inflection point from the new design wins. The market will be looking for a clearer path to the double-digit growth previously mentioned for FY26.

Questions for the Earnings Call

Tier-1 Wireless Contract: Can you provide more details on the new Tier-1 wireless operator contract? Specifically, what is the potential revenue scale, and when do you expect it to start contributing meaningfully?

Gridspertise Status: Could you give us an update on your conversations with Gridspertise? Does the lack of an update change your previous expectation for a return to shipments in Fiscal 2026?

Fiscal 2026 Outlook: Last quarter, you guided for double-digit growth in the core business for FY26. Does your Q1 guidance and recent design wins reinforce that view? Can you discuss the expected cadence of growth through the year?

Gross Margins: You previously guided for some gross margin pressure in Q4. How did margins perform, and what are your expectations for Q1 and the full fiscal year?

Cash Flow: Cash declined by about $6M year-over-year. What were the primary uses of cash, and what is your outlook for operating cash flow generation in FY26?

1

3

876

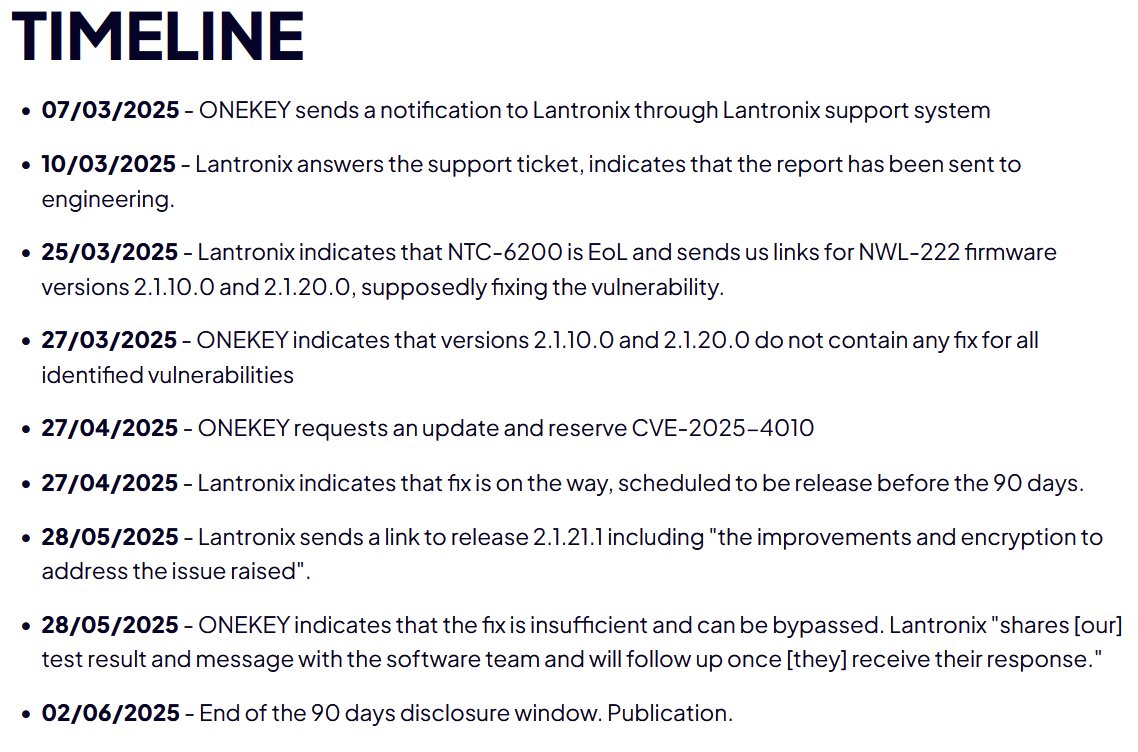

2 Jun 2025

We continue publishing advisories on issues identified by our platform using bash static analysis. Today we look at CVE-2025-4010 affecting Netcomm (aka Lantronix) NTC-6200 and NWL series.

We're still waiting for a proper patch. Link below 👇

1

1

4

723

16 Apr 2025

Netcomm Forum 2025, anche

quest’anno, presenti!🙌😎

@ConsNetcomm

#netcommforum2025

#netcommforum #networking #digital

3

29

16 Apr 2025

We're grateful that #ShopCircle was invited to the #2025NetcommForum organized by Consorzio Netcomm. It's inspiring to witness how the ecommerce ecosystem continues to evolve, and exciting to see @Shopify as a main partner this year. 👏🏼

Day one already brought great panels around the future of ecommerce, AI-driven tools, and the importance of building with and for merchants.

We're proud to be a part of a community shaping what's next. 💚

2

1

4

308