Jun 12

I remember months ago NexGold was high up on your list and silver storm was barely on your radar. What changed? I own both and am playing the high risk reward portfolio

1

2

189

HNWinvestor retweeted

Jun 12

Posted on behalf of NexGold Mining Corp. — $NEXG.v; $NXGCF

@NexGoldMining recently provided an update on the ongoing development of its 100%-owned and fully permitted Goldboro Gold Project in Nova Scotia, confirming that key pre-construction activities remain on track.

Following the release of this operational timeline, management highlighted that work is actively focused on an updated Mineral Resource Estimate to support an updated Feasibility Study, which is anticipated for completion by the end of Q3 2026.

Simultaneously, the company has progressed detailed engineering and procurement ahead of planned earthworks in September 2026, while launching a 30,000-meter reverse circulation infill drill program to target the first few years of planned production.

Looking ahead, the updated Feasibility Study will play a crucial role in advancing the company's previously announced US$175 million non-binding letter of intent for potential project financing.

See the full update here: nexgold.com/nexgold-advancin…

2

10

220

6/12/2026 Buy the Dip List

youtube.com/watch?v=Qqic-hYx…

AI summary of the video:

Chesapeake — Long-duration Mexico development story. Core thesis is permit unlock → rerating. He thinks if Discovery gets a greenfield permit in Mexico it creates a precedent helping Chesapeake (and GoGold). Build timeline long (2–3 years), thinking roughly toward 2030. Why upside? Market not valuing future free cash flow yet.

Silver Tiger — Multi-stage growth story. Build first mine → then two underground mines later. Don’s angle: market only values near-term assets and ignores later pipeline. Long-term leverage play.

SilverCo — Nearer-term than most. Already producing. Acquired Nova Silver. Goal: ~4M oz next year → ~10M oz by 2028. Don sees unusual combination of production large upside.

Silver Storm — Production beginning now, but current operation only modest scale. Real upside = San Diego project. Biggest issue = uncertainty around build timing.

Vizsla — Bullish after nearby permitting progress. Acknowledges cartel concerns but dismisses them because he sees project as “too big to fail.”

Guanajuato — Simple formula stock. Conditions:

Maintain/grow production (~4M oz)

Keep costs under control

Silver reaches $200

Risk = dilution if silver stalls.

1911 Gold — One of his favorites. Low capex. Production starts Q4. Thesis = ramp from startup → 70–100k oz/year over a few years. Additional nearby feed gives scalability.

Aftermath — Optionality story. No PEA yet. Large silver inventory manganese lowers expected cost structure. Long timeline.

NexGold — Canadian producer/growth setup. First mine straightforward. Big upside comes later from building Goliath (3–4 years out).

Andean Silver — Very simple thesis: restart mine. Previously mined ~5M oz and expects restart around Q1 2028. Don worries acquisition risk because project looks attractive.

GoGold — Likes management/insiders. More complex than Andean because requires building two mines. Full value only realized years later. Strong dependence on higher gold prices.

Norsemont — Waiting for updated PEA. Likes:

Existing mill

Low capex

Large resource

Not slam dunk but strong risk/reward.

Heliostar — Already producing but has multiple growth projects. Don likes undervalued producers with steady growth.

BMC — Yukon silver project. Advanced. Environmental permit achieved but permitting still viewed as major risk. High projected free cash flow.

Blue Lagoon — Small producer now. Probably tops out around 80–100k oz unless later mill build. Not huge scale but meaningful upside if successful.

Santa Cruz — Buy-the-dip candidate. Existing production plus future growth via Soracaya. Don likes producers that can add ounces.

Endeavor — Existing producer. Growth from Pitarrilla. Current high costs partly financing-related and expected to ease. Thinks valuation ignores future expansion.

Denarius — Building Colombian mill now. Then Spain project (Lomero). Thesis = if both execute → major leverage.

Avino — Producer with surprising upside. Conditions:

Silver to ~$200

Grow to ~8M oz

Control costs

Silver Mountain — Restart story. Production expected soon. Large resource and valuation seen as unusually depressed.

Boumadine — Production not expected until 2029–2030. Don expects rerating once construction starts.

Honey Badger — Speculative. Large silver-zinc project in Canada. Fully permitted (major positive). Many unknowns remain.

Spanish Mountain — High-risk development. Wants construction-ready by ~2028. Very high capex (~$900M), but Don became more positive due to scale.

Talisker — Producer growth story. Market dismissing it. Goal:

~100k oz by 2028

Long-term ~200k oz

Acquisition risk exists.

Integra — Don added personally. Existing Florida Canyon mine underperforming but future value = building two more mines. Long-term.

Revival — Similar to Integra. Build multiple mines. Stronger sentiment environment could revalue U.S.-based assets.

Lahontan — One of his cleaner setups.

PEA → construction → only ~6-month build.

Nevada open pit = lower execution complexity.

Jaguar — Producer in Brazil. Three mills; currently underutilized. Thesis = fill mill capacity over ~5 years.

New Found Gold — Long-term production growth story after Maritime acquisition. Likes location.

P2 Gold — Calls it a Lahontan clone. Similar scale, open-pit style, exploration upside.

McFarlane — Early development optionality. Roughly 5M oz moving toward 8M oz. Long build timeline.

Discovery Silver — One of the bigger conviction names. Existing production giant upside from Cordero permitting.

Key numbers he mentioned:

~1B oz silver

Early years ~30–32M oz silver equivalent annually

Potential “monster” if permitted.

Thor Explorations — West Africa exposure (Nigeria/Senegal). Not for everyone politically, but Don likes it.

Sun Silver (bonus pick) — Not on favorites list but highlighted. Nevada optionality play:

~540M oz AgEq

Waiting for PEA

Huge capex ($1–1.5B)

Construction target ~2028

Don floated 40-bagger potential if execution works.

Meta takeaway (his actual filter):

He repeatedly favored (1) producers adding production, (2) restarts, (3) optionality plays waiting for sentiment expansion, (4) development stories where permitting unlocks valuation.

28

26

187

37,718

Jun 10

Gold Market Strength and NexGold Mining's Goldboro Project Position Retail Investors for Opportunity

ow.ly/n3SW50Z9YgB

Explore how geopolitical trends are boosting gold and why NexGold Mining Corp.'s fully permitted Goldboro Gold Project offers a compelling development story for investors seeking Canadian gold exposure.

$NEXG.V $NXGCF @NexGoldMining

1

1

247

Jun 10

Gold Market Strength and NexGold Mining's Goldboro Project Position Retail Investors for Opportunity

ow.ly/n3SW50Z9YgB

Explore how geopolitical trends are boosting gold and why NexGold Mining Corp.'s fully permitted Goldboro Gold Project offers a compelling development story for investors seeking Canadian gold exposure.

$NEXG.V $NXGCF @NexGoldMining

1

1

67

I bought more NexGold, Contango, Aya, and Nord Precious Metals.

2

71

Stocks&Thoughts retweeted

Jun 8

Fully Permitted Canadian Gold Project Advances Toward Key Q3 Milestone

ow.ly/J1sk50Z8Vko

NexGold Mining Corp. ( $NEXG.V $NXGCF ) reported continued advancement at its Goldboro Gold Project, including feasibility study work, permitting activities, engineering, procurement, community engagement, and pre-construction planning.

@NexGoldMining

2

4

410

Jun 8

Fully Permitted Canadian Gold Project Advances Toward Key Q3 Milestone

ow.ly/J1sk50Z8Vko

NexGold Mining Corp. ( $NEXG.V $NXGCF ) reported continued advancement at its Goldboro Gold Project, including feasibility study work, permitting activities, engineering, procurement, community engagement, and pre-construction planning.

@NexGoldMining

1

3

93

Posted on behalf of NexGold Mining Corp. - $NEXG.v; $NXGCF

In a recent interview, @NexGoldMining President and CEO Kevin Bullock sat down to discuss the company's strategic plan to become Canada's next mid-tier gold producer.

During the conversation, Bullock highlighted several key points driving the company's current momentum:

- Explains why the junior #gold market is entering a critical transition point, noting that investors are beginning to move down from senior and mid-tier producers into the developer space.

- Breaking down NexGold's immediate roadmap for the fully permitted Goldboro project in Nova Scotia, touching on their established First Nation agreements and the expected timeline leading up to a formal construction decision.

- Discussing the Goliath Gold Complex in Ontario, emphasizing how it will serve as the next phase of the company's corporate growth strategy.

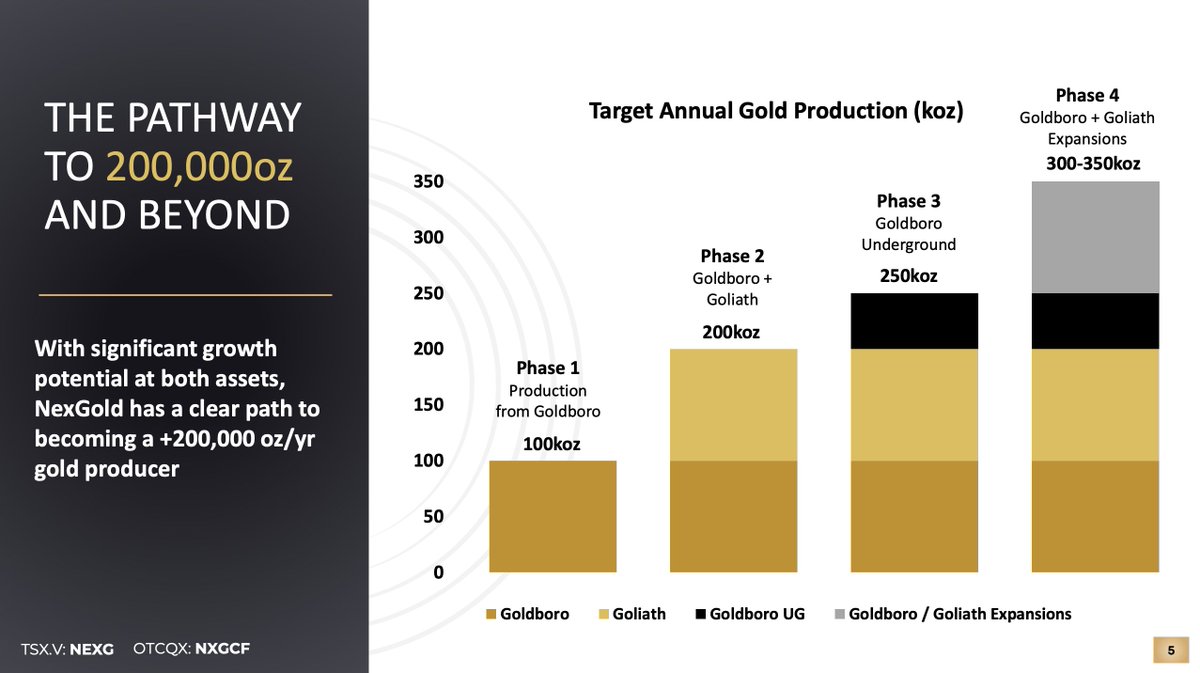

Looking ahead, Bullock emphasized the company's aggressive development timeline, explicitly targeting the end of 2028 to pour their first gold at Goldboro.

He closed by outlining NexGold's long-term objective to build a robust project pipeline that could ultimately grow toward 300,000 to 350,000 ounces of annual production.

See the full video here: youtube.com/watch?v=3ax77Z_g…

2

15

360

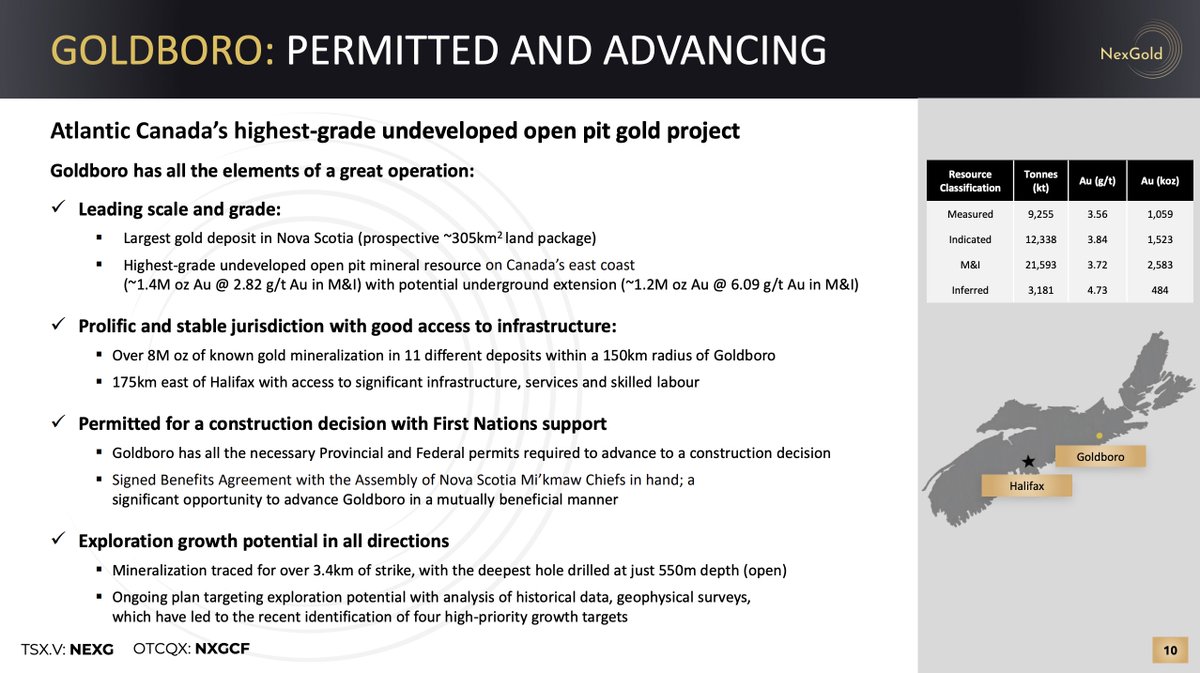

Posted on behalf of NexGold Mining Corp. — $NEXG.v; $NXGCF

NexGold Mining recently provided an update on the advancement of key development activities at its 100%-owned and fully permitted Goldboro #Gold Project in Nova Scotia.

In the news release, they highlighted an updated Feasibility Study, community engagement, permitting updates, procurement, engineering and technical activities, exploration, and human resources.

Describing the unique nature of the asset, CEO Kevin Bullock commented, "Permitted, shovel-ready, Canadian gold projects like Goldboro are incredibly rare, and we understand not only how special this opportunity is, but also the importance of getting it right."

The company plans to provide regular updates as it steadily de-risks the project ahead of a potential construction decision targeted for late Q3 2026.

See the full release here: nexgold.com/nexgold-advancin…

Jun 1

Press Release: NexGold Advancing Key Development Activities on Schedule at the Goldboro Gold Project in Nova Scotia

nexgold.com/nexgold-advancin…

$NEXG $NEXG.v $NXGCF #NexGold #Goldboro #CommunityEngagement #NovaScotia #Mining

2

9

179

Jun 4

$FOR.V - FORTUNE BAY CORP.

I took a position in FOR. 69.9M shares. No debt. Tight structure. Maximum leverage to gold. MRE done. PEA done. PFS soon.

The worth: Market cap: C$54M. NPV at spot gold (US$4,535): C$1.8B. That's 3 cents on the dollar.

The asset: 1.2 Moz gold in Saskatchewan — #3 jurisdiction globally. 97% Indicated. Approved EIS since 2008. Written First Nations consent through DFS. PEA done. PFS executing now, completion YE2026/Q1 2027.

The man: Wade Dawe owns ~15% and has already sold two companies for C$400M . He bought C$445K of stock personally in 2025 at C$0.32. Now C$0.77. He's not done.

The catalysts: 700 assays in the lab from targets outside the current resource. Manhattan Uranium drilling 25 targets on Fortune Bay's land right now. PFS completion in 6–9 months opens M&A conversations.

The precedent: Fresnillo paid C$780M for Probe Gold in January 2026 — same stage, same jurisdiction, 39% premium. At 0.20× NAV, FOR's takeout value is C$7–11/share.

You can all the angles on FOR below, the detailed research however is in the research document on drive.google.com/file/d/1bCx….

The Discount Angle

C$54M market cap. C$1.8B NPV at spot gold. That's 3 cents on the dollar. Even if you haircut everything by 50% for development risk, you're still paying 6 cents. Name another Canadian gold developer priced this cheap.

The Gold Leverage Angle

Every US$100 move in gold = C$61M change in NPV. Gold is at US$4,535. The PEA was modelled at US$2,600. The bull case is now spot. The stock hasn't moved. FOR is a leveraged gold call option with a 13.9-year mine life underneath it.

The M&A Angle

Fresnillo bought Probe Gold in January 2026 for C$780M — 0.2–0.3× NAV, 39% premium. Same stage, same jurisdiction quality. At 0.20× NAV, FOR's takeout value is C$7–11/share. Current price: C$0.77. The chairman has already done this twice.

The De-Risking Angle

97% Indicated resource. Approved Environmental Impact Statement since 2008. Written First Nations consent through Definitive Feasibility Study. Saskatchewan — #3 mining jurisdiction globally. Every 2026 technical workstream returning clean data. This is not a speculative explorer. It's a developer where the hard work is already done.

The Operator Pedigree Angle

Wade Dawe built and sold Brigus Gold for ~C$350M at a 45% premium. Then built and sold Keeper Resources for C$51.6M all-cash. He's doing it again at Fortune Bay — same playbook, same jurisdiction category, bigger gold price backdrop. He bought C$445K of stock personally at C$0.32. Now C$0.77. Still cheap.

The Unpriced Upside Angle

The PEA modelled a doré flowsheet. New met results show >50% gold to gravity concentrate at 0.08% feed mass, >90% flotation recovery.

If the PFS switches to concentrate, AISC drops materially vs the PEA base case. The market has priced zero of this.

Add Golden Pond (all 7 holes hit, 578 assays pending), the Box down-dip extension at 3.70 g/t over 21m outside the MRE, and an underground scenario not in any economic model. The PEA is the floor, not the ceiling.

The Resource Angle

989,600 oz Indicated at 1.28 g/t Au. 214,200 oz Inferred at 0.90 g/t. Total 1.2 Moz — and 97% of the mine plan is already Indicated.

That's not a conceptual resource. It's 838 drill holes over 80,000m, reconciled to within 1% of 64,000 oz of actual historical production from the same ore body. And it's about to get much bigger. Some step-outs:

3.70 g/t over 21.0m (incl. 9.89 g/t over 7.0m)

6.95 g/t / 3.72 g/t / 4.55 g/t stacked 8.72 g/t over 2.0m

2.54 g/t over 17.0m (incl. 6.61 g/t over 5.0m)

1.20 g/t over 23.2m (incl. 4.68 g/t over 3.2m, 12.20 g/t over 1.0m)

2.06 g/t over 6.88m

8.95 g/t over 1.0m

16.53 g/t over 13.6m.

578 assays still in the lab. Frontier: 135 assays pending. Athona West: not yet drilled. The 2 km gap between Box and Athona almost entirely undrilled. Updated MRE hits in 2027. None of the expansion ounces are in the current PEA economics.

The Hidden Optionality Angle

Nobody is talking about Mexico.

Fortune Bay holds 100% of the 4,176 ha Rio Negro concession in Chiapas — valid until 2051, no royalties, no back-in rights. Prior operators (Linear Gold, then Kinross) drilled 89,000m in 342 holes focused entirely on near-surface epithermal gold.

Historical resource: 1.74 Moz Au 6.7 Moz Ag (M&I Inferred). High-grade historical intercepts: 100m @ 12 g/t Au & 64 g/t Ag at Campamento; 22m @ 10 g/t Au at Laguna Chica.

Nobody drilled the porphyry underneath.

One hole — IXM08-51 — intersected 601.4m @ 0.28% Cu / 0.68 g/t Au / 2.71 g/t Ag from surface. That's the upper halo of a district-scale copper-gold-silver-molybdenum porphyry system. The geological setting parallels Grasberg and Bingham Canyon at the district scale. No focused copper exploration has ever been conducted. The buried porphyry has never been drill-tested.

This asset is valued at approximately zero in every model. It's not needed for the Goldfields thesis to work. It's not in any analyst's numbers.

It's just sitting there.

The Jurisdiction Angle

Saskatchewan is #3 mining jurisdiction globally (Fraser Institute 2025). Royalty and taxation framework unchanged since 2006. Regulators who actively want mining to happen — Verran's own words: "It's so nice to talk to regulators who listen and want to broaden their mineral economy."

No indigenous land claim uncertainty, no federal impact assessment (below 5,000 tpd threshold), no permitting lottery. Compare that to Nevada title disputes, Quebec court injunctions, or anything in West Africa. The jurisdiction risk premium the market is applying to FOR is essentially zero — because it should be.

The Infrastructure Angle

This is not a greenfield project in the middle of nowhere. Road to the Box deposit. Active hydro powerline. Airport at Uranium City 13 km away. Existing camp and facilities. Multiple operating uranium mines within 350 km with comparable logistics. The 2008 feasibility study already designed the mine — Fortune Bay is updating it, not starting from scratch. C$301M capex looks different when the site prep is already done.

The Tight Share Structure Angle

69.9M shares outstanding. FD ~82.2M. In a junior mining peer group where 300–400M share counts are routine, Fortune Bay is surgical. Every dollar of value creation hits fewer shares. In a re-rating scenario — PFS completion, M&A approach, gold breakout — the per-share leverage is maximum. Dawe knows exactly what he's doing keeping the count tight.

The Uranium Kicker Angle

Most investors in FOR have no idea there's a uranium portfolio attached. Manhattan Uranium (TSXV: MANU) is drilling up to 25 targets at Murmac & Strike right now — June 2026, fully funded, largest program to date. Best hole to date: M24-017 returned 8.4m @ 0.30% U₃O₈ including 1.20m @ 1.79% U₃O₈, with individual assays up to 13.80% U₃O₈ — textbook Athabasca unconformity geometry. If Manhattan hits a discovery, FOR holds the underlying land and collects either a JV interest or NSR royalties. A uranium discovery on optioned land costs Fortune Bay shareholders nothing. It's a free lottery ticket on the hottest uranium basin in the world.

The Cheapest MCap/NPV Angle

Canadian gold developers routinely trade at 5–10% of NPV. Fortune Bay is at 3%. The peer set — Amex Exploration, NexGold, Getchell — all trade at multiples of FOR's MCap/NPV ratio. The discount has not narrowed as gold has run from US$2,600 to US$4,535. It has widened. Every week that passes without a re-rating is another week of compounding undervaluation against a rising gold price backdrop. At some point the gap closes. It always does.

The Bankable Resource Angle

The most de-risked PEA-stage resource in the Canadian peer group. 97% of the mine plan is Indicated — not Inferred, not historical, not conceptual.

989,600 oz Indicated across 24.0 Mt at 1.28 g/t, drilled in 838 holes over 80,000m, reconciled to within 1% of 64,000 oz of actual underground production from the Box Mine (1939–1942). SRK Consulting signed it. Ausenco is building the PFS on top of it. This resource is bankable today. The PFS makes it financeable.

The Permitting Fast Lane Angle

A provincially approved Environmental Impact Statement has existed for a 5,000 tpd open-pit operation at this exact site since 2008. The PEA's 4,950 tpd throughput is designed to stay below the federal impact assessment trigger — provincial permitting only. A First Nations Exploration Agreement signed November 2022 grants documented written consent through to and including Definitive Feasibility Study. That is not "community engagement ongoing." That is pre-existing written consent covering the entire study sequence. Pam Bennett has personally navigated the Saskatchewan permitting system on 14 mining projects. The permitting pathway is not a risk. It's a competitive advantage.

The Catalyst Runway Angle

The PFS isn't the only catalyst. It's the last one in a sequence that's already running.

Between now and PFS completion (YE2026 / Q1 2027), every quarter delivers:

Imminent:

Manhattan Uranium drilling up to 25 targets at Murmac & Strike — mobilisation confirmed June 4, 2026. Results H2 2026.

Neu Horizon Uranium ASX listing ~June 29, 2026 — A$15M IPO, funded partner for The Woods uranium option.

578 Golden Pond assays still in the lab. All 7 holes already confirmed gold. Historical hole in same area: 16.53 g/t over 13.6m. When these land, the resource footprint expands visibly.

135 Frontier assays pending — first data from an untested target.

Summer 2026:

Athona geotechnical drilling (4 holes, ~400m) — PFS-level data for the second pit, which is 25% of the mine plan.

Athona West drilling — tests the 2 km undrilled gap between Box and Athona. High impact if it hits.

Concentrate trade-off study output — does the PFS switch from doré to concentrate? If yes, AISC drops materially vs the PEA baseline.

Phase 2 waste rock kinetic testing results — confirms the acid generation profile for permitting.

H2 2026:

Poma Rosa amparo ruling — binary outcome, upside if successful.

Manhattan uranium drill results — discovery scenario adds a narrative the market hasn't priced.

YE2026 / Q1 2027:

PFS completion (Ausenco-led). This is the document that makes the asset financeable, enables institutional capital, and opens M&A conversations with majors. Dawe doesn't need a buyer before the PFS. He needs the PFS to start the conversation.

2027:

Updated MRE incorporating all 2026 drilling — Box extensions, Golden Pond, Frontier, Athona West. First time the market sees what the resource actually looks like post-expansion drilling.

Saskatchewan regulatory permitting advancement building on the 2008 EIS.

Strategic partner / JV / M&A conversations get serious. Probe/Fresnillo closed January 2026 — majors are actively buying Canadian developers at 0.2–0.3× NAV.

The stock is at C$0.77. The next six months deliver more data than most juniors produce in three years. None of it is priced in.

10

20

75

17,834

$ASHL $ASHL.cn #GOLD It's June! @AshleyGoldCorp is half way through the year of 2026.

What did we accomplish so far?

Financings and Corporate Updates

January 26, 2026 – Launches LIFE Charity Flow Through and Concurrent LIFE Hard Dollar (min. $800k, max. $2M allocation), Plans Extensive Winter Campaign on Tak Patents: The company opened a charity flow-through and hard-dollar financing under the Listed Issuer Financing Exemption to fund winter drilling and exploration on the Tak Patents.

March 11/13, 2026 – Announces Closing of LIFE Hard Dollar and Charity Flow Through Financings, Funding Diamond Drill Program: The financings closed successfully, providing the capital required to execute the Phase 1 diamond drill program on the Tak Patents.

January 8, 2026 – Announces Howie Core Cutting Update, Sets NSRs for Howie and Burnthut Main Block to Zero, Dryden Area, ON, Grants Options: Ashley eliminated NSRs on key Dryden-area assets (Howie and Burnthut Main Block) to enhance project value and granted stock options to directors, officers, and consultants.

January 14, 2026 – Announces Filing of Early Warning Report (President Surpasses 10% Ownership Threshold): President Noah J. Komavli filed an updated NI 62-103 Early Warning Report after the Tak Patents acquisition increased his ownership above 10%.

April 24, 2026 – Announces Filing of NI 62-103 Early Warning Report: A further early warning report was filed in connection with ownership or control changes.

April 28, 2026 – Completes Disposition of Tabor-Sakoose, Adds Retained Santa-Maria Claims to the Sale for Total Proceeds of $475k in Cash and Stock: The company finalized the sale of the Tabor-Sakoose property (plus retained Santa-Maria claims) for $475,000 in cash and stock, further streamlining its portfolio and generating non-dilutive capital.

Projects and Exploration Advances

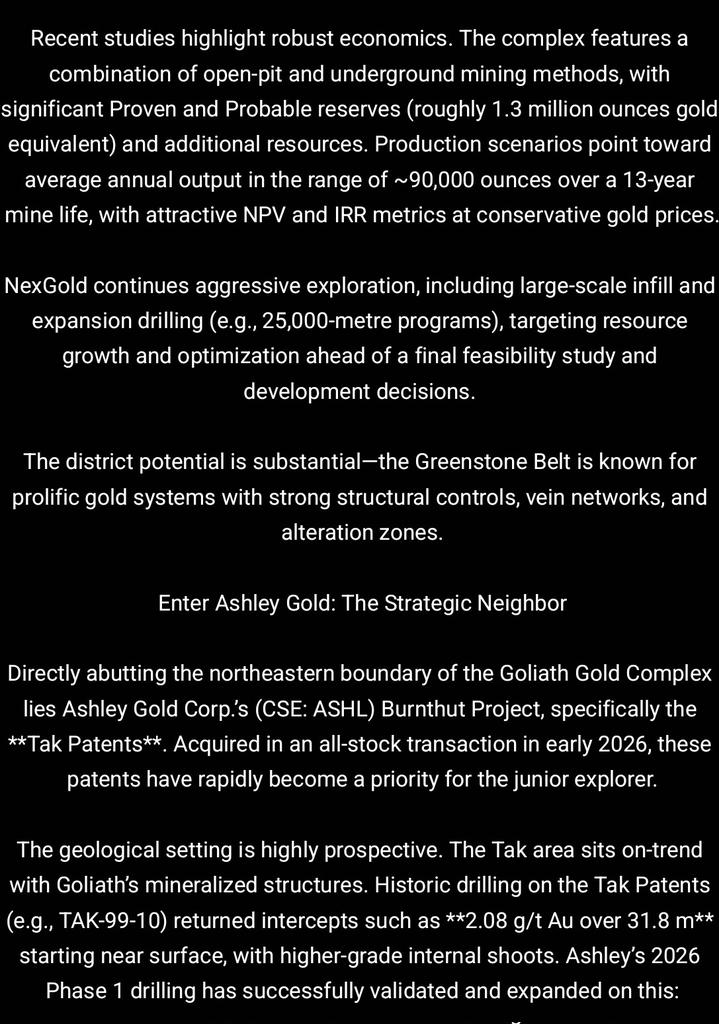

January 6, 2026 – Expands Presence Adjoining NexGold Mining Corp.’s Goliath Gold Complex, Acquires Ownership of the Tak Patents in All-Stock Transaction, Optimizes Burnthut Project, ON: Ashley acquired 100% ownership of the ~100 ha Tak Patents (patented ground directly adjoining NexGold’s Goliath Gold Complex) via an all-stock deal (3.5 million shares issued), consolidating historic bulk-tonnage gold data while retaining a 5% NSR to Royal Gold Inc. (with 2.5% buyback option for $1M).

January 8, 2026 – Howie Core Cutting Update & NSR Reduction (see Financings section above for combined corporate impact).

February 5, 2026 – Provides BC Update, Posts Bond for Gold Mountain Project: The company posted the required reclamation bond for the Gold Mountain Project in British Columbia and provided a general update on its BC assets.

March 14, 2026 – Provides Interim IP Data, 1 km Resistive Trend Unveiled on the Tak Patents Abutting NexGold Goliath-Gold Complex: Interim results from the Abitibi Geophysics OreVision IP survey identified a 1 km resistive trend aligning with historic gold zones on the Tak Patents; Perron Contracting was engaged for upcoming drill support.

April 2, 2026 – Announces Completed Mobilization to the Tak Patents, Abutting the NexGold Goliath-Gold Project: Drill trails, over 10 pad locations, rig, and skidder were fully in place, enabling the start of the Phase 1 diamond drill program targeting the historic D99Z zone and extensions.

April 20, 2026 – Provides Operations Update for Ongoing Tak Drill Program: The company updated stakeholders on active drilling operations and confirmed submission of core samples from the first hole (TAK-26-01) for assay.

April 23, 2026 – Concludes Phase 1 Drilling, Provides Additional Updates: Phase 1 drilling was successfully completed (four holes drilled), with further operational details released.

May 26, 2026 – Re-Mobilizes Field Crew for Phase 2 Tak Drilling and Prospecting – Bordering the NexGold Goliath-Gold Complex, Dryden Area, Ontario: Following encouraging Phase 1 results, field crews were re-mobilized to commence Phase 2 drilling and prospecting on the Tak Patents to further delineate the D99Z zone and test new targets.

Drill Results

March 19, 2026 – Intercepts 0.53 g/t Au over 24 m in Howie Maiden Drilling (Dryden Area, ON): Maiden diamond drilling at the 100% owned (0% NSR) Howie Project intersected a near-surface gold-bearing zone returning 0.53 g/t Au over 24 m (typical of bulk-tonnage systems) on only ~400 m of drilling, located adjacent to Dynasty Gold’s Pelham deposit.

May 1, 2026 – Submits TAK-26-02 for Fire Assay, Shares Example Mineralization, Provides Updates: Core from the second Phase 1 hole (TAK-26-02) was logged, cut, and submitted for fire assay; visual examples of mineralization were shared alongside operational updates.

May 5, 2026 – Submits TAK-26-03 for Fire Assay, Shares Example Mineralization: Logging and cutting of TAK-26-03 were completed and the core delivered to ActLabs; mineralization visuals were released.

May 11, 2026 – Submits Final Holes for Assay (TAK-26-04 and TAK-26-05), Shares Example Mineralization: The remaining Phase 1 holes were submitted for assay, completing the sample batch from the program.

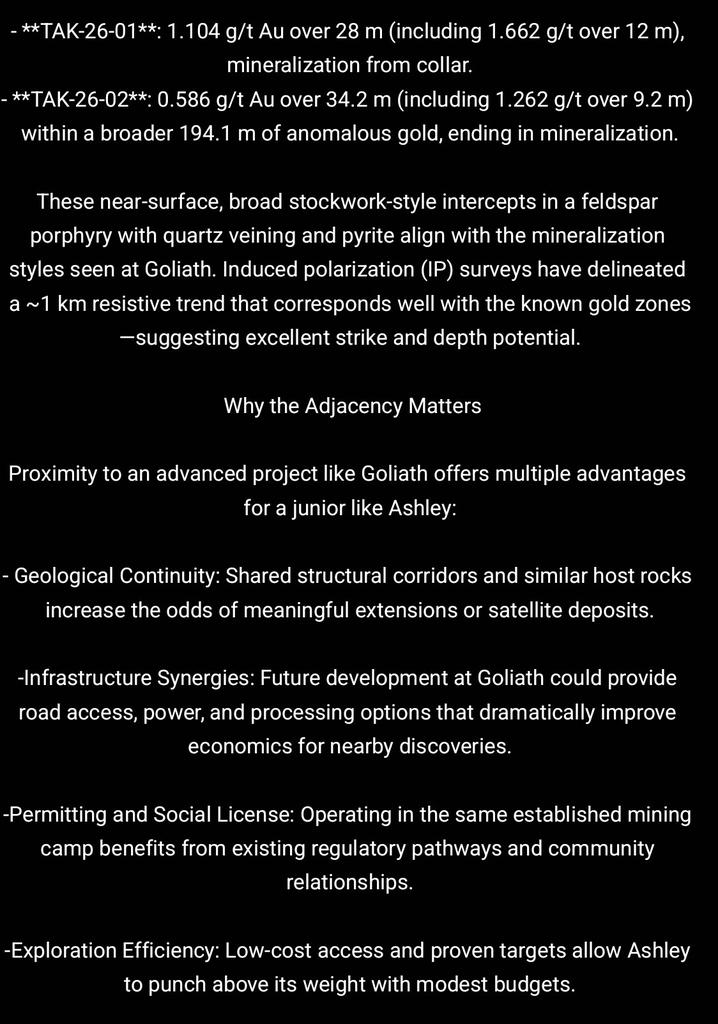

May 14, 2026 – Reports TAK-26-01 Assay from Phase 1 Drilling, Intercepts 1.104 g/t Au over 28 m (Including 1.662 g/t Au over 12 m) – Mineralization Starting at Collar: First assay results from Phase 1 confirmed historic mineralization; TAK-26-01 returned 1.104 g/t Au over 28 m (including 1.662 g/t Au over 12 m) starting from surface in the newly designated D99Z, with four additional holes still pending and Phase 2 guidance provided.

May 20, 2026 – Intercepts Multiple Gold-Bearing Intervals Including 0.586 g/t Au over 34.2 m from Surface Within 194.1 m of Anomalous Gold Mineralization (TAK-26-02): TAK-26-02 delivered broad near-surface gold mineralization, highlighted by 0.586 g/t Au over 34.2 m (including 1.262 g/t Au over 9.2 m) within a larger 194.1 m anomalous interval; the hole ended in mineralization, reinforcing the pervasive nature of the D99Z zone and supporting expansion potential.

1

7

536

Jun 2

Thank you to everyone who joined NexGold at @THEMiningEvent 2026 today in Québec City.

CFO Orin Baranowsky participated in a fireside chat discussing the Company's progress and development plans for Goldboro and the Goliath Gold Complex.

$NEXG $NEXG.v $NXGCF

1

27

550

Jun 1

NexGold Advancing Key Development Activities on Schedule at the Goldboro Gold Project in Nova Scotia | $NEXG.V

See News:

mininghub.com?id=6481710&pid…

1

2

7

398

Jun 1

Press Release: NexGold Advancing Key Development Activities on Schedule at the Goldboro Gold Project in Nova Scotia

nexgold.com/nexgold-advancin…

$NEXG $NEXG.v $NXGCF #NexGold #Goldboro #CommunityEngagement #NovaScotia #Mining

6

24

774