In this @TheAIJournal1 article, portfolio company @openspaceai CEO Jeevan Kalanithi explores why visual intelligence will be a foundational layer for the next generation of agentic AI.

Read more: co.jll/49TNL1U

27

Jun 7

@tooeyprocore @OpenSpaceAI @AliceTech_AI — you're already running AI on submittals and pay apps. The receipt layer is what closes the loop. If the sub falsified inputs, the signed receipt proves it. If the GC approved anyway, it proves that too.

13

Go @openspaceai! You were early to this trend.

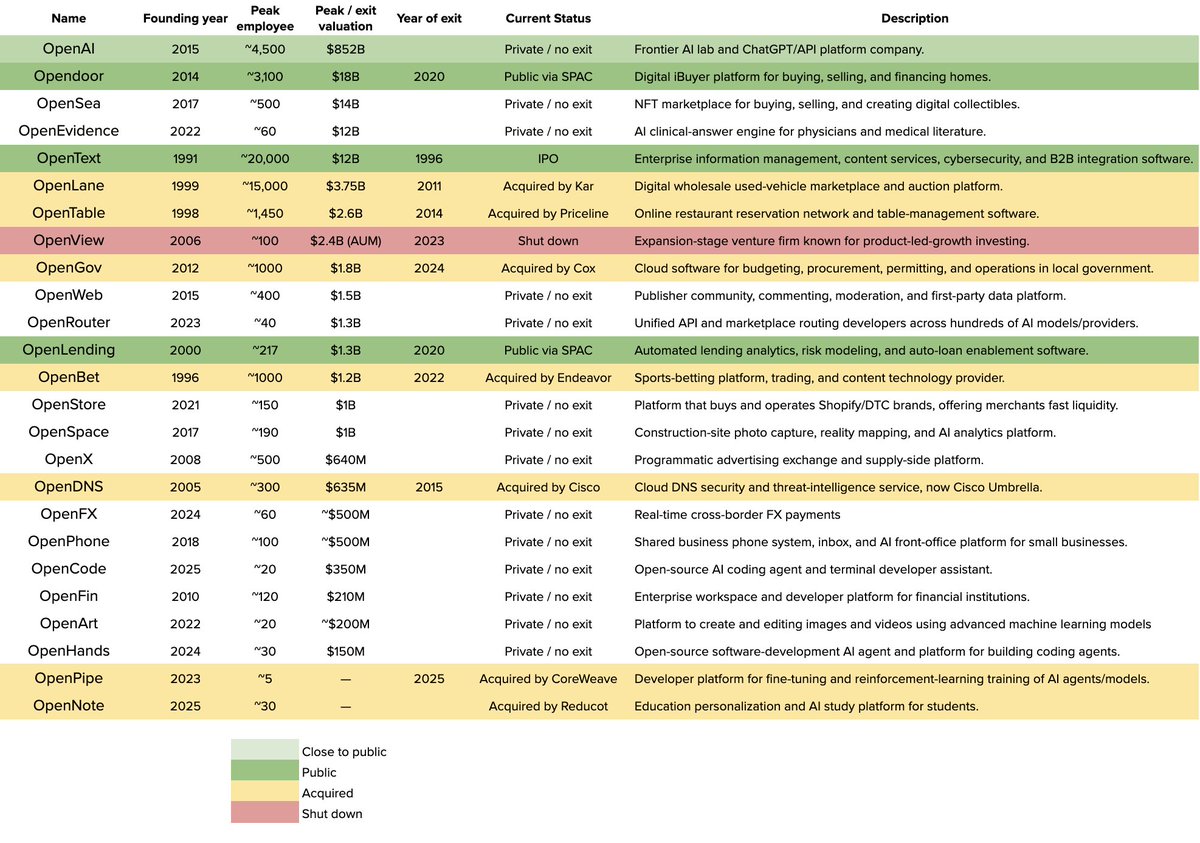

I'm convinced that adding "Open-" to your company name instantly 10x's your odds of success.

OpenAI

OpenEvidence

OpenTable

OpenRouter

OpenCode

OpenDoor

OpenGov

OpenWeb

OpenText

OpenView

OpenSea

OpenStore

OpenFX

OpenSpace

OpenArt

OpenHands

OpenPipe

OpenNote

1

5

3,471

May 10

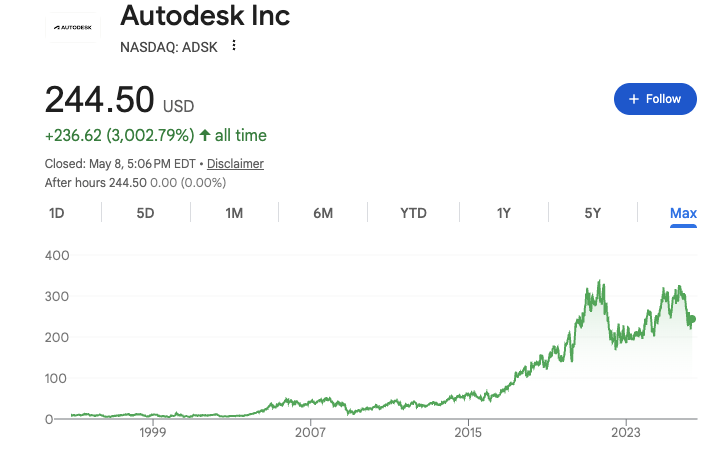

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Day 45: Autodesk $ADSK

Peak share price: $334.38 (Aug 20, 2021)

Share price today: $244.5 (-27%)

EV today: $51.4bn

ARR today: $7.8bn ( 19%, 14% excluding new transaction model impact)

NRR: ~110% (though one time gain from new transaction model)

EV/ARR: 6.6x

GAAP Operating Margin: 22%

EV/Run-rate GAAP EBIT: 30x

Headcount: 14,300 (-7% Y/y) (!!)

What Autodesk does:

Autodesk is the dominant design/eng software that architects, structural engineers, mechanical engineers, construction firms, etc. use to design and build physical things.

As is common in engineering-y verticals, it has a portfolio of products organized around major industries with a long history of M&A. AE&C (architecture, engineering and construction) is about half of revenue, while BIM (building information monitoring) is another tentpole of a broad portfolio that ranges from injection molding simulation to 3D animation/visual effects.

It is worth noting that this is a software category that made the transition to subscription but has largely skipped the jump to cloud- it is still standard for engineers to buy high-end PCs (and for firms to manage computing clusters) to do cutting-edge design/simulation work.

AI bear case:

The bear case here has parallels to Bentley Systems. Autodesk effectively functions as a conglomerate and each piece of its business has different considerations. While each is generally a high-quality software business, much of the advantage comes from user interface lock-in (engineers have used, say, Autodesk CAD, for years), which AI could potentially obviate if AI-generated production design renders user interfaces less relevant.

More broadly, the reality is that Autodesk faces a multi-front war in a potentially fast-changing world, with different competitors and strategies required for each segment. It doesn't seem like the company is innovating at a pace where it can keep up if things keep changing quickly.

AI bull case:

The bull case is that things won't change quickly, Autodesk has time to figure it out and it's core advantages will remain valuable and let it layer value-added AI on top. Unlike Adobe where creation of visual assets may commoditize, creation of buildings, bridges will always require some human touch and very high precision (i.e. no hallucinations). Beyond that, there is ample room for software to add more value through complex physics simulations, etc. If the barrier to adding that value (i.e. simulating physics) falls, more value might accrue to the core, sticky workflow tools for engineers, CAD systems.

AI traction:

No particular ARR or revenue figure disclosed, the shift to a new transaction model (selling directly vs. through resellers) remains the dominant driver of results.

Adjacent AI-native startup summary:

This is a famously difficult problem space for startups to tackle. The best cloud-native CAD tool (Onshape) was acquired by PTC and now grows under that umbrella. Many smaller startups have struggled to break through.

In construction, startups like @doxel_ai and @openspaceai are doing interesting work with machine vision that could potentially impact parts of Autodesk's portfolio, but in truth @procoretech remains the most salient competitor there. Motif (79 employees, 23% Y/y) has raised $46m from top VCs to tackle the BIM space, but doesn't seem to be on an overtake trajectory thus far.

Overall, there's no single startup that has raised money with an expressed vision of disrupting any of Autodesk's core product lines, which likely reflects the depth of moat and challenges associated with building trust in this sector.

Management Quotes:

"In the coming months, Autodesk will roll out powerful AI capabilities built on a combination of frontier models and our proprietary models that understand 3D design and make.

Autodesk is building the future and the path to it for our customers. We have been preparing for and working towards the cloud and AI for more than a decade. It's why I believe our best days and greatest opportunities lie ahead."

"Converged data opens up new opportunities for Autodesk. As customers seek efficient innovation, attach rates of Fusion's extensions are growing strongly, and we've delivered meaningful productivity gains to customers where we deploy AI. We have continued to see success with our AI-powered Sketch AutoConstrain in Fusion. Since its launch last year, the AI model has delivered over 3.8 million constraints, up from 2.6 million last quarter. Along the way, the model has been retrained and the UX improved. As a result, the acceptance rates by AutoConstrain suggestions to commercial users have now grown to almost 2/3 with 90% of those sketches fully constrained."

"Let's move on to scaling and monetizing agentic AI. In preparation for the cloud and AI, Autodesk modernized its platform and go-to-market over the last few years, well ahead of industry peers. Few industry peers are ready for the business models and go-to-market motions that will monetize their AI-driven future. Autodesk is.

We built a platform that provides the identity, permissions, geometry kernels, data models and compute infrastructure needed to deploy AI safely and at scale into design, engineering, manufacturing and construction environments. Platforms enable safety, innovation and efficiency at scale."

Commentary:

Autodesk bears many similarities to Bentley Systems- a conglomerate of highly defensible and entrenched vertical creation software solutions that doesn't seem to have a clear AI angle of attack just yet, but also seems fairly slow-moving and unlikely to light the world on fire with an AI innovation anytime soon. That's reflected in the relatively healthy 6.6x sales multiple.

It does strike me that culturally Autodesk is a tick behind Bentley- recent management changes have shaken the business up and lead to traditional "corporate" changes- new transaction model, sales reshuffling, etc. which frankly seems to be somewhat of a distraction in this era relative to shipping compelling products. At the same time, there's not yet a clear AI threat emerging and disrupting Autodesk's core workflows, so it seems likely to have time to adjust and eventually "get there" just as it did during the transition to a full subscription model.

2

23

6,828

AI is quietly strengthening quality in luxury residential builds, with @TestFitInc , Hypar, @openspaceai , @cupixinc , @reconstructinc , Join, @DocumentCrunch and @HexagonAB improving precision and clarity. best-international-project.c…

#ConstructionTech #AIinConstruction

2

12

I’m starting “OpenSpaceAI.” It will be a charity until it has the chance of making me a billionaire, then I’ll convert it to for-profit.

3

139

30 Dec 2025

New @Forbes column: @openspaceai Is Using #AI To Create A Visual Timeline Of Projects

@openspaceai helps its customers - mainly in the #construction industry - to capture what's going on in the field

#TechNews

Read: forbes.com/sites/quickerbett…

131

20 Nov 2025

Yesterday, Suffolk Technologies hosted BOOST 6 Demo Day, the finale of its built-world accelerator, at our Boston HQ. @openspaceai Founder & CEO Jeevan Kalanithi spoke, followed by demos from the BOOST 6 cohort, addressing challenges across construction, design & real estate

2

156

5 Nov 2025

A new wave of proptech startups is transforming how deals are sourced, managed, and closed.

Startups like @elise_ai , @Placer_ai , @openspaceai show how AI is already reshaping daily operations in CRE.

📌 These are just 10 of the 50 AI startups redefining the industry. See the full list via @thomvest here: appraisal.substack.com/p/103…

#CRE #proptech #AI #realestate #commercialrealestate #realestatenews

1

5

209

21 Jul 2025

Our General Partner Alexandra Vidyuk @bastinda joined an inspiring panel discussion "Shifting the Lens: Being a More Inclusive Venture Ecosystem" hosted by @ProtegeVentures and Women into Ventures. The event brought together top female investors to demystify venture capital careers and amplify diverse voices in the industry.

"There's no single 'right' path - successful investors come from engineering, consulting, or finance backgrounds. What matters is curiosity, pattern recognition, and building conviction," emphasized Alexandra.

Special thanks to moderator Sneha Gupta for fostering such an actionable dialogue, and fellow panelists:

- Chloe Tan – Head of Asia, @Founders_Forum ; Co-Founder of @womeninvsea

- Charmaine Ng – Ecosystem & Partnerships, @openspaceai

The energy in the room proved one thing: The future of venture looks radically more inclusive.

#VentureCapital #DiversityInVC #InvestInChange #WomenIntoVentures

1

5

103

18 Jul 2025

Wishing you great success. This is how we innovate and build faster. Let us know how we can partner together @openspaceai @JLL

1

43

14 Jul 2025

Today, I've joined @openspaceai as a Senior Front-End Software Engineer to build a platform with a complete visual record of construction projects, powered by AI.

Excited about what's ahead! 🎉

ALT OpenSpace

1

6

150

28 Feb 2025

✨#NowHiring ✨

Calling all ambitious talent! 🚀 Looking for your next opportunity? Dive into this week's spotlight on @cartainc revolutionizing equity management, @Chime transforming banking, and @openspaceai in construction tech. Visit mnlo.vc/Careers for updates.

2

2

781

11 Feb 2025

Want to see AI transforming the physical world? Check out what @openspaceai is doing in the construction space.

Jeevan was an EIR with me so we got to invest at ground zero, and now growing handsomely globally.

5

819

8 Nov 2024

Is there a recipe for sustainable growth in construction tech?

The answer: Yes. But it might surprise you.

Speaking from our conversation with Jeevan Kalanithi from @openspaceai, I believe the key isn't chasing growth - it's obsessing over simplicity.

1

3

52

At Joeris, we're combining tradition with innovation! Our team utilizes the latest technology — from @DroneDeploy to @openspaceai — to enhance efficiency and ensure precision on every project. 🏗️✨ #ConstructionTechnology #JoerisGC #TransformingPeopleAndPlaces

1

2

5

498

10 Jun 2024

Free #Webinar! Experience the power of AI-driven 360° docs to prevent rework, control labor, reduce travel and collaborate with project teams efficiently - ow.ly/BzmS50Se7wz

#BuildSteel #CFSteel #AI #Construction #Drywall #Technology #ConTech #OpenSpaceAI @AWCI_INFO

1

2

75

27 May 2024

🚧📐 OpenSpace #BIM brings model analysis to the field for Polk Mechanical. Discover how this tech is transforming #construction projects with real-time insights. Read the blog ➡ t.ly/wlyrx 🏗️🔧 #ConstructionTech @openspaceai

ALT 🚧📐 OpenSpace #BIM brings model analysis to the field for Polk Mechanical. Discover how this tech is transforming #construction projects with real-time insights. Read the blog ➡ https://t.ly/wlyrx 🏗️🔧 #ConstructionTech

1

23

8 May 2024

🔧 Simplify #construction coordination with OpenSpace's easy-to-use tools! Streamline your projects efficiently. Learn how these tools can change your site management game - 👉 t.ly/vO9Gb 🏗️📊 #ConstructionTech #ProjectManagement - @openspaceai

ALT 🔧 Simplify #construction coordination with OpenSpace's easy-to-use tools! Streamline your projects efficiently. Learn how these tools can change your site management game - 👉 https://t.ly/vO9Gb 🏗️📊 #ConstructionTech #ProjectManagement

2

26

17 Apr 2024

🚨Don't miss out! Secure your spot for the most anticipated webinar of the year! Join us April 24, 2024, at 10:00 am EST as we delve into the 2024 Building Industry Technology Market Insight & Strategy 👉shorturl.at/ghyT8

Featuring our Founder/CEO and a lineup of top industry experts:

🔹 Nick Carter - INGENIOUS.BUILD

🔹 Scott Kessling - @JLL

🔹 Sharon Richardson, PhD - @hoarelea

🔹 Jeevan Kalanithi - @openspaceai

🔹 Derek Alley - @vccusa

Moderated by Emily Wright - @cretech

Why Attend?

✨ Gain insights into cutting-edge tech trends shaping the AEC industry.

🔍 Explore the latest in AI, IoT, sustainability, and data analytics.

🎯 Receive expert guidance to navigate today's dynamic marketplace.

🚀 Actionable guidance to stay ahead in the evolving landscape.

👥 Tailored for building owners, developers, occupiers, AEC service providers, and tech providers.

Presented by INGENIOUS.BUILD! 🏗️

Don't miss out! Register now to secure your spot: shorturl.at/ghyT8

#BeINGENIOUS

#BuildingIndustry #TechnologyTrends #AEC #Webinar

1

2

112