Iraq (Oilfield Operations): Chevron signed framework agreements to secure exclusive 1-year negotiation rights to acquire the operatorship of the West Qurna 2 oilfield from Russian producer Lukoil. Deals were also made to explore and develop the Nasiriyah and Balad fields.

1

52

Iraq (Oilfield Operations): Chevron signed framework agreements to secure exclusive 1-year negotiation rights to acquire the operatorship of the West Qurna 2 oilfield from Russian producer Lukoil. Deals were also made to explore and develop the Nasiriyah and Balad fields.

35

ENERGY BRIEF JUNE 12 2026

CURRENT GEOPOLITICAL SITUATION

LNG traffic through the Strait of Hormuz is moving again, but the route remains exposed. Additional LNG tankers have exited the waterway despite reduced traffic and elevated security risk, while a South Korean-operated LNG carrier also cleared the Strait after being stranded near the area. Passage is possible, but LNG buyers, shipowners and insurers remain under pressure until the security picture stabilizes.

A reported Iran–U.S. proposal could reopen the Strait of Hormuz and provide temporary oil sanctions relief, according to Iranian state media cited by CNBC. The proposal is not a confirmed final agreement, and enforcement remains the key issue. Crude oil, LNG, tanker routing and insurance can only normalize if both sides accept a durable navigation framework.

Ukrainian strikes continue to pressure Russian oil infrastructure and fuel logistics. The Institute for the Study of War reported continued Ukrainian strikes against Russian oil infrastructure, while Russian-held areas face worsening gasoline shortages. Russia’s fuel network remains exposed to drone pressure, refinery disruption and military resupply strain.

ENERGY REPORT

WOODSIDE / PETROCHINA / BROWSE GAS JV

Woodside exercised a pre-emptive right to buy PetroChina’s 10.67% stake in the Browse gas joint venture, blocking Inpex from entering the project. Browse is Australia’s largest undeveloped conventional gas resource and is intended to support the North West Shelf LNG facilities as older fields decline. Woodside protects control over future gas supply; Inpex loses access, while North West Shelf partners gain stronger alignment.

VENTURE GLOBAL / ATLANTIC-SEE / GREECE LNG

Venture Global and Atlantic-SEE LNG Trade doubled their long-term LNG supply agreement to at least 1 million tonnes per annum (MTPA) from 2030 for 20 years. Atlantic-SEE, a joint venture between AKTOR Group and DEPA Commercial, plans to move U.S. LNG into Greece and onward through the Vertical Corridor into Central and Eastern Europe. Venture Global, Greek import infrastructure and regional gas buyers benefit; spot-exposed buyers remain under pressure.

PETROBRAS / EQUINOR / BRAZIL OFFSHORE

Petrobras will acquire a 50% stake from Equinor Brasil in the Itaimbezinho offshore block in Brazil’s Campos Basin. Equinor will remain operator with 50%, while PPSA will manage the production-sharing contract. Petrobras strengthens its Campos Basin upstream position; Equinor keeps operatorship but shares future development cost and exposure.

INDIA / FUEL SALES / SHORTAGE CONTROL

India restricted bulk gasoline and diesel purchases at retail fuel stations to protect domestic supply. Commercial consumers were barred from buying fuel at retail outlets, while daily diesel purchases were capped at 200 liters per customer or vehicle for up to 90 days. Retail consumers benefit from protected supply; commercial buyers, trucking firms and fuel retailers remain under pressure.

By Victor Stoichkov

#EnergyBrief #OilAndGas #LNG #StraitOfHormuz #EnergySecurity #GlobalEnergy

1

130

Jun 12

🚨BP is selling minority stakes in 2 deepwater hubs sitting on 10 billion barrels of discovered oil.

This isn't an exit!

It's a smart move in deepwater capital management right now🛢️⚡

Kaskida and Tiber-Guadalupe are BP's next 2 major operated hubs in the Gulf of Mexico both in the ultra deep Paleogene, both sanctioned, both using 20,000 psi technology that only a handful of companies in the world can operate.

Combined nameplate capacity: 160,000 b/d of oil.

First oil: 2029 and 2030.

Kaskida: >3 billion boe in-place. 32,500 ft wells. 275 million boe in Phase 1 alone. BOEM development plan approved.

Tiber-Guadalupe: 6 Tiber wells plus Guadalupe tie-backs. Same 20K platform technology. FID taken in 2025.

Why sell stakes in your best projects?

Because deepwater is a capital-timing problem, not a quality problem.

Capex is front-loaded: 2024–2030, before a single barrel flows. Cash arrives only after 2029–30.

By farming down to 50%, BP recovers sunk exploration costs, cuts future capex in half, keeps operatorship and redeploys capital into short cycle shale or buybacks while both hubs keep building.

The strategic logic under Meg O'Neill:

BP's US production target: 1 million boe/d by 2030, nearly half its global output.

It already runs Thunder Horse, Atlantis, Mad Dog, Na Kika, Argos.

Kaskida and Tiber-Guadalupe are hubs 6 and 7.

The Paleogene position up to 10 billion boe is the long-term growth engine.

Selling 25-50% of each doesn't weaken the strategy, it funds it. 🌍

🛢️Oil is up 40% this year.

The deepwater economics window is wide open.

BP isn't retreating from the Gulf.

It's building the most capital efficient path to dominating it.

(do not miss my latest article on oil in the below comments)

1

12

34

2,622

TER retweeted

Jun 12

Until 2025, the aircraft operated under the name Mounthill Ltd but switched operatorship to UMO Ltd in order to get the PNCF permit — which has now been suspended in the wake of the incident.

TheCable understands the pilot, Chris Baca, a Pakistani, has also been arrested for allegedly breaching the aviation age limit.

x.com/i/status/2065263477590…

Jun 12

EXCLUSIVE: Aircraft in Asaba incident linked to Abuja church as FG arrests 'overage pilot'

The private aircraft that landed on a road in Ogwashi-Uku area near Asaba, Delta state, on Wednesday is owned by an Abuja church, TheCable understands.

Sources in the know informed TheCable that the Nigeria Civil Aviation Authority (NCAA) has established that the aircraft was registered in the US in the name of the church.

thecable.ng/exclusive-aircra…

1

4

1,335

EXCLUSIVE: Aircraft in Asaba Incident Linked to Dunamis Church as FG Arrests 'Overage Pilot'

The private aircraft that landed on a road in Ogwashi Uku area near Asaba, Delta State, on Wednesday is owned by Dunamis International Gospel Centre, TheCable understands.

Sources in the know informed TheCable that the Nigeria Civil Aviation Authority (NCAA) has established that the aircraft was registered in the US in the name of Dunamis, whose senior pastor is Pastor Paul Enenche.

It was brought into Nigeria to operate on a non commercial flight (PNCF) permit.

Under the terms, according to aviation rules, it is not supposed to be used as private charter, but this condition is now believed to have been violated.

Until 2025, the aircraft operated under the name Mounthill Ltd but switched operatorship to UMO Ltd in order to get the PNCF permit, which has now been suspended in the wake of the incident.

UMO is owned by Mike Olaoye, a member of the church.

TheCable understands the pilot, Chris Baca, a Pakistani, has also been arrested for allegedly breaching the aviation age limit.

He is said to be 70 years old, five years above the age limit for pilots operating in Nigeria.

Source: @thecableng

1

119

Jun 11

It was brought into Nigeria to operate on a non-commercial flight (PNCF) permit.

Under the terms, according to aviation rules, it is not supposed to be used as private charter but this condition is now believed to have been violated.

Until 2025, the aircraft operated under the name Mounthill Ltd but switched operatorship to UMO Ltd in order to get the PNCF permit — which has now been suspended in the wake of the incident.

UMO is owned by Mike Olaoye, a member of the church.

thecable.ng/exclusive-aircra…

1

9

26

19,886

[WATCH] Petronas is transferring operatorship and stakes in several producing oil and gas assets in Peninsular Malaysia and Sarawak to EnQuest to optimise its portfolio and extend the life of mature fields.

Read more: nst.com.my/business/corporat…

83

Jun 11

#NSTBusinessTimes Petroliam Nasional Bhd (Petronas) is transferring operatorship and stakes in several producing upstream assets in Peninsular Malaysia and Sarawak to EnQuest Petroleum Production Malaysia Ltd.

bit.ly/4elG1XX

237

Petronas is transferring operatorship and stakes in several producing upstream assets in Peninsular Malaysia and Sarawak to EnQuest Petroleum Production Malaysia Ltd. #NSTBusinessTimes

nst.com.my/business/corporat…

166

Australia's oil and gas sector is moving fast in 2026. Woodside's Scarborough project is 96% complete with first LNG cargo expected by year end. Santos just achieved first oil at Pikka in Alaska. Beach Energy's Waitsia gas plant is delivering. Karoon completed its Baúna operatorship transition in May.

Five companies. One sector navigating geopolitical volatility and delivering anyway.

Read the full breakdown: investingnews.com/biggest-as…

1

72

Jun 10

$PBR ACQUIRES 50% STAKE IN ITAIMBEZINHO BLOCK

$PBR is teaming up with Equinor again, grabbing a 50% interest in the Itaimbezinho exploration block in the Campos Basin. $ENQR

🔹 Equinor keeps operatorship with 50%, PPSA manages the PSC

🔹 Strengthens Petrobras’ position in a core area with existing synergies (Raia project, Jaspe license)

🔹 Aligns with 2026–2030 Business Plan to replenish reserves

283

Jun 10

#PRD

🧵 #PRD THREAD PART 3 — HE ACTUALLY SAID IT OUT LOUD. THE MARKET STILL DIDN'T LISTEN.

January 2025 investor presentation. Publicly recorded. Every word below is verbatim.

🎙️ THE QUOTE THAT CHANGES EVERYTHING

Forget broker notes. Forget bulletin boards. Here is the CEO of #PRD — in his own words — explaining exactly why flowing gas is irrelevant to the investment thesis:

💬 "The market only gives value for — oh you flow 100 barrels a day today, you know, or you flow a million cubic feet of gas — that won't get us over the line with our divestment. So I make no apology whatsoever for focusing on securing the assets in a way that allows us to divest them anyway."

Read that again.

He is not building toward a flow test. He is not trying to impress retail investors with production numbers. He is building an asset package engineered for industry acquisition — and the acquirer doesn't need flowing wells to write the cheque.

The market has been waiting for a flow test that was never the objective.

💬 "The industry values our assets based on legal title, funds spent on developing the assets, resources, exploration potential — all these other good things that the market currently gives no value for."

Two completely different valuations of the same asset:

🏪 Stock market value: ~£31M — priced on daily production, share price momentum, retail sentiment

🏭 Industry value: legal title ✅ £18.7M capitalised spend ✅ 441 BCF 2C ✅ exploration upside ✅ helium ✅ Jurassic charge ✅ Jersey structure ✅

Griffiths knows exactly which valuation matters. And it isn't the one the LSE is using.

🔥 MORE FROM THE SAME PRESENTATION — THINGS NOBODY FLAGGED

💬 "We never forget and we never forgive. That's our motto. If you don't like it — tough. That's why we'll do whatever it takes."

This is a CEO who had the Tendrara opportunity taken from him, watched Sound Energy's shareholders make a return on his work, and built PRD specifically to make sure it doesn't happen again. This is personal. This is motivated.

💬 "We are not an AIM company. We're a Main Market company integrated on the Main Market after the reorganisation last year — regulated by the FCA. That's a different set of controls compared to AIM."

Why does this matter? Because Main Market = UK Takeover Code applies in full. Rule 2.2 confidentiality obligations. Rule 9 mandatory bid threshold. Concert party provisions. The regulatory architecture for a clean Gulf NOC acquisition is all in place — and most retail investors don't realise PRD isn't on AIM.

💬 "If we're selling shares in Jersey there is no capital gains tax. So that's why the companies are structured in the way they're structured."

Tax-free exit. For the acquirer AND for PRD. Engineered from day one.

💬 "We always maintain operatorship — to control our costs and to accelerate execution of strategic decisions. If we were a minority partner we could still be waiting years to get projects off the ground."

100% operatorship. 75% equity. Jersey structure. Zero UK assets. No CGT on exit. Deal architecture pre-disclosed.

Every single element of this company was built for one purpose.

💬 "No point in diluting your asset down to 10% and expect people to come running to your door because it's an immaterial asset. The choice is either dilute at shareholder level or dilute your assets — which in turn dilutes the value potential and makes it 10 times harder to look at divestment."

This is why PRD has never farmed out Morocco. Not because they couldn't. Because 75% of something worth $692M is worth protecting. A 10% farm-out at current market pricing would be catastrophically value-destructive. Griffiths knows it.

💬 "You won't sell that for a billion dollars on day one — but what you can do is structure a deal whereby you get significant back costs, opportunity costs for getting the licence interest... and also milestones as various things tick off — like an appraisal well, development, first gas."

He literally describes the HOA deal structure — back costs milestone payments — in plain English, 12 months before it was publicly disclosed. This was always the plan.

💬 "We'll never give an inch on values in terms of what we can realistically achieve for a divestment. We call Predator for a reason."

📐 AND THE NUMBERS HE CITED IN JANUARY 2025

These are from the same presentation — MOU-5 pre-drill, before it was drilled:

🔢 187 km² structural size — "greater than Greater London"

🔢 4.4 TCF 2P net gas resources (prospective, undrilled)

🔢 $1.3 billion unrisked undiscounted annual gross revenues in success case at $7/MCF

🔢 74.6 BCF 2P helium resources net to PRD

🔢 $3.5 billion gross unrisked undiscounted 2P helium revenues at $400/MCF

🔢 136p per share independently assessed risked value — at 12% chance of success

The current share price is 3.5p.

The broker risked value was 148p. That's not a typo.

💬 "Where else in the world onshore at present can you have this kind of risk/reward ratio for a $2.4 million well where Predator has 75%... three kilometres from infrastructure linked to Europe?"

Nowhere. That's the answer. Nowhere.

🧠 WHAT THE SMART MONEY SEES THAT THE MARKET DOESN'T

The retail market is pricing PRD as a small, speculative, non-producing E&P company on the Main Market with a difficult testing programme and an uncertain timeline.

The industry sees:

✅ 4,301 km² licence — northeast Morocco ✅ Five wells drilled, data gathered, learning curve complete ✅ 441 BCF 2C certified TCF-scale Jurassic/Triassic upside undrilled ✅ Three kilometres from GME pipeline to Europe ✅ No CGT on Jersey exit ✅ CEO with 40 years' experience who has done this before with Tendrara ✅ £18.7M past costs recoverable at signing ✅ Third party funding MOU-6 — someone already committed ✅ $7B deal adviser engaged ✅ UAE CDA signed since 2021

The acquirer doesn't need flowing wells. They need legal title, data, and structure. PRD has all three.

⚠️ Independent research only. Not investment advice. DYOR.

#PRD #Morocco #LSE #oilandgas #divestment #Morocco #helium #smallcaps

@PredatorOilGas @GrahamHengland @AM231982 @Blowster85 @Share_Talk @OilVoice

4

26

941

Jun 10

🇲🇾 EnQuest PLC, has agreed to acquire participating interests in four offshore production sharing contracts (PSCs) in Malaysia from Petroliam Nasional (PETRONAS).

EnQuest will assume operatorship and participating interests in the Balingian PSC, SK8 PSC and D35 PSC, and will also participate as a non-operating partner in the PM6/12 PSC. themalaysianreserve.com/2026…

1

81

Since assuming operatorship of OML 17 in 2021, @HeirsEnergies has:

- More than doubled oil production to 50,000 bpd

- Tripled gas production to 135M scfd

- Contributing about 5% of Nigeria's oil output and about 5% of domestic gas supply

#HHImpact

#AfricapitalismInAction

#HeirsEnergies

1

1

330

Jun 9

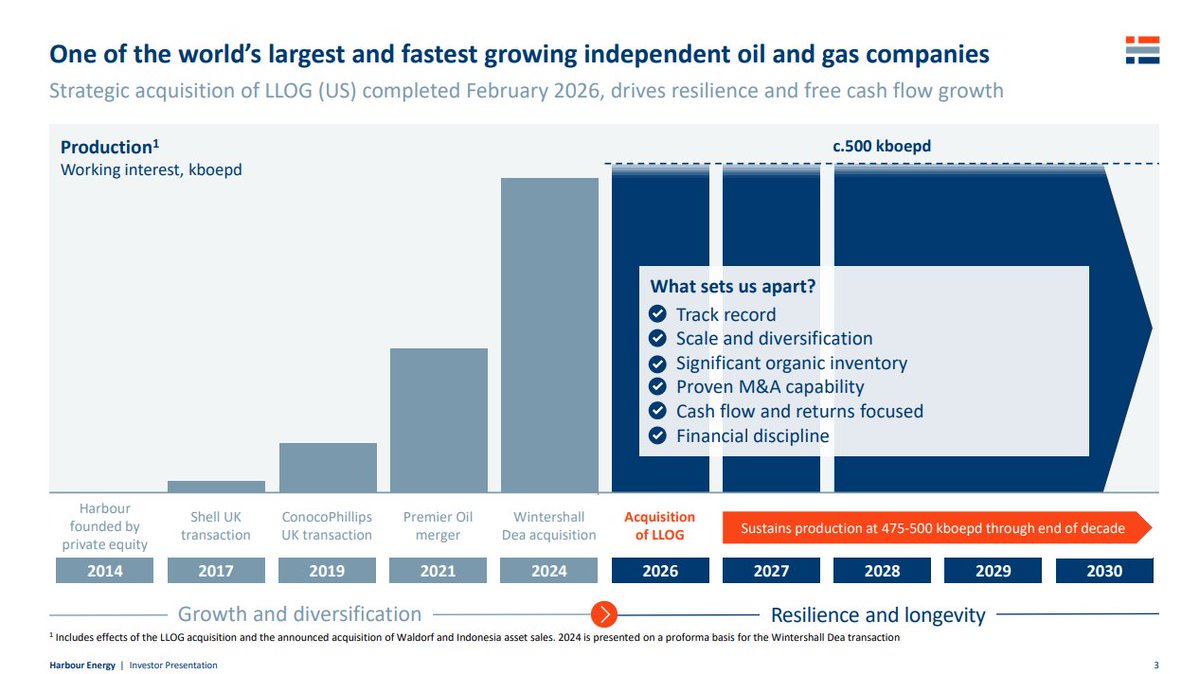

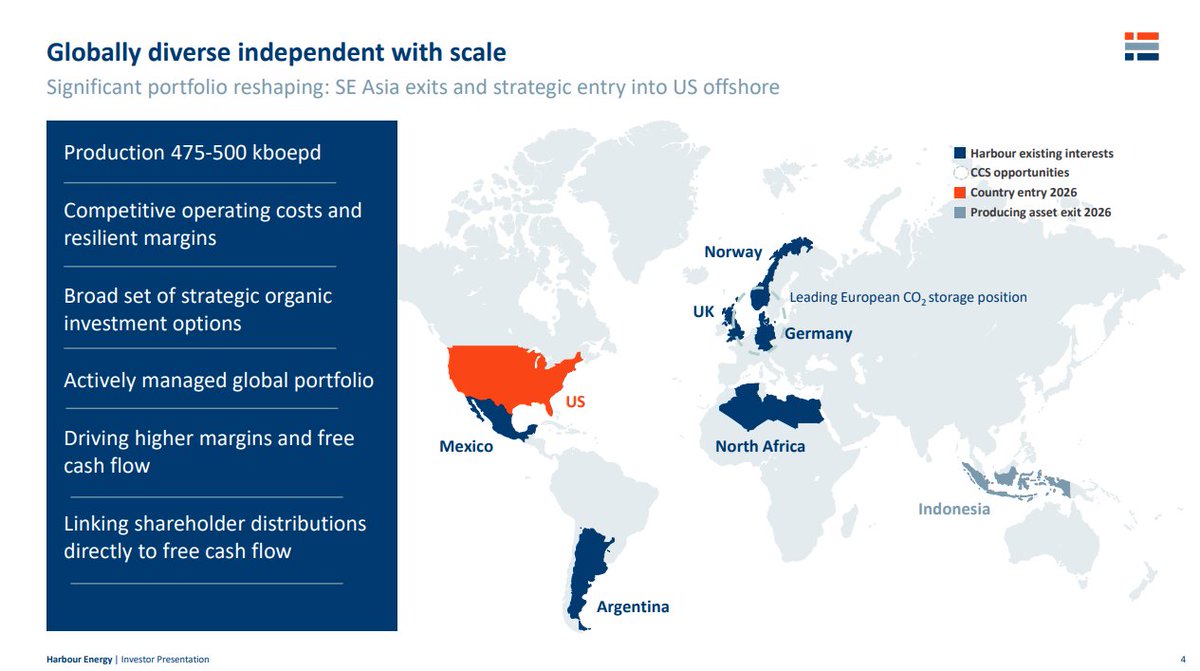

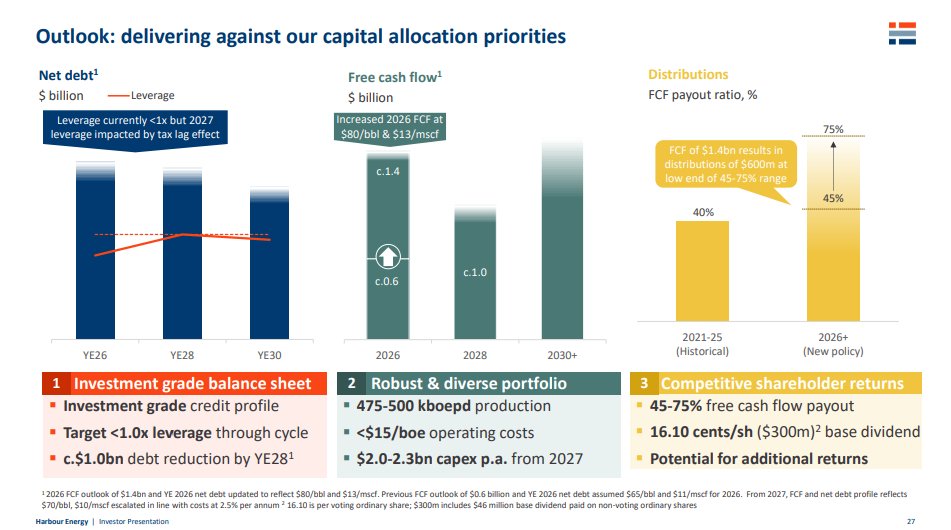

Harbour Energy ($HBR) - Deep Dive Equity Analysis 🛢️🇬🇧

I've broken down Harbour Energy’s latest FY2025 results and Q1 2026 developments. Here is why this UK heavyweight is aggressively transforming into a diversified global E&P powerhouse.

1️⃣ Company Introduction

• Company:

Harbour Energy is the UK’s largest independent oil and gas producer. Following the monumental Wintershall Dea asset acquisition, it has officially transitioned into a global upstream player.

• Shareholders:

The shareholder registry has evolved significantly, with BASF and LetterOne now holding major stakes following the Wintershall Dea integration, providing strong institutional backing.

• From Past to Future: Historically a North Sea-centric operator, Harbour has strategically pivoted to a globally diversified portfolio spanning Europe, the Americas, and North Africa to dilute regional regulatory risks.

• Technology:

They are heavily focused on capital-efficient offshore technology (like phased FPSO developments) and are actively optimizing their Carbon Capture and Storage (CCS) portfolio to align with energy transition mandates.

2️⃣ Product Presentation & Current Developments

2025 and early 2026 have been entirely transformative. FY2025 production hit a record 474 kboepd (up 84% YoY).

More importantly, Harbour completed the $3.2B acquisition of LLOG in February 2026, giving them a premium foothold in the US deepwater Gulf of Mexico.

They are actively high-grading the portfolio: divesting Indonesian assets for $215M, acquiring Waldorf (UK) for $170M to unlock tax synergies, and securing operatorship of the massive 750 mmboe Zama oil field in Mexico.

3️⃣ Valuation Snapshot

Share price ~274 GBp / 1.58B shares out

• Market Cap: ~$5.6 Billion USD

• Net Debt (strictly excluding leasing): ~$7.2 Billion USD (reflecting the completed LLOG transaction)

• Enterprise Value (EV): ~$12.8 Billion USD

• FY25 Adjusted EBITDAX: $7.2 Billion USD

4️⃣ Earnings Snapshot

Harbour is a cash-generating machine. Despite lower commodity prices, FY2025 Free Cash Flow (FCF) surged to $1.1B (up from $0.1B in FY24). Unit operating costs plummeted by 22% to a highly competitive $12.8/boe.

Backed by this liquidity, management announced a highly attractive shareholder return policy targeting a 45-75% FCF payout, initiating a $300M annual base dividend while prioritizing debt reduction until leverage drops below 1.0x.

5️⃣ Peer Group Comparison

Trading at a trailing EV/EBITDA of roughly 1.7x, Harbour looks severely discounted compared to the broader energy sector median of ~3.5x.

When stacked against UK-centric peers like EnQuest (trading around 1.9x EV/EBITDA) or Ithaca Energy, Harbour offers significantly larger scale, superior geographical diversification, and a much cleaner path to rapid deleveraging.

The market is pricing Harbour like a mature North Sea pure-play, ignoring its newly acquired global, long-life assets.

6️⃣ Forecast 2030 & Valuation

Management guidance points to steady production of 475-500 kboepd through 2030, supported by $2.0B-$2.3B in annual capex.

Assuming a mid-cycle Brent price of ~$65-$70/bbl, I project 2030 EBITDA to stabilize around $6.5 Billion USD.

If the market eventually rerates $HBR to a highly conservative 2.5x EV/EBITDA multiple by 2030, the implied Enterprise Value would hit $16.25 Billion.

With FCF expanding to ~$1.0B annually by 2028 and aggressively paying down the $7.2B debt pile, the equity value expansion over the next four years is highly asymmetrical.

7️⃣ Acquisition Potential

Harbour's DNA is built on M&A. While 2026 is focused on digesting the LLOG and Wintershall Dea assets, they remain the ultimate consolidator.

As supermajors continue to pivot toward renewables or exit mature conventional basins, Harbour is perfectly positioned to snap up stranded, cash-flowing assets at distressed multiples, utilizing their improved global footprint.

8️⃣ Opportunities / Risks

• Opportunities: The Waldorf acquisition alone is expected to unlock $900M in UK tax losses. Furthermore, organic growth in Argentina (Vaca Muerta LNG) and Mexico (Zama) guarantees a 2P reserves replacement ratio of over 100% through 2028.

• Risks: The UK Energy Profits Levy (windfall tax) remains a persistent political headwind. Additionally, their current $7.2B debt load requires flawless integration of the newly acquired assets, leaving them temporarily sensitive to severe macro shocks in global Brent and European gas spot prices.

9️⃣ Conclusion

Harbour Energy has successfully executed one of the most aggressive E&P portfolio transformations of the decade. The combination of plunging OPEX, record production, and massive FCF generation makes the current ~1.7x EV/EBITDA multiple look entirely mispriced.

For patient capital willing to ride out the deleveraging phase over the next 24 months, Harbour presents a compelling deep-value proposition with a robust dividend yield.

Disclaimer: Not a financial advice. Always do your own DD.

2

7

496

Formalised JV gives @NlRimfire 60% and operatorship of Avondale, strengthening its scandium position in Australia’s heartland. $RIM

discoveryalert.com.au/news/r…

127

Jun 8

What nonsense. So SOCAR took over the operatorship. Nothing changes IRL.

175