Daily Insights on Global Commodities Markets and Events | Commodity Trader | Founder of The Merchant (40k subs) 3x/week → themerchantsnews.substack.co…

Joined August 2024

- Tweets 7,337

- Following 329

- Followers 44,864

- Likes 2,721

4,187 Photos and videos

Pinned Tweet

Jun 11

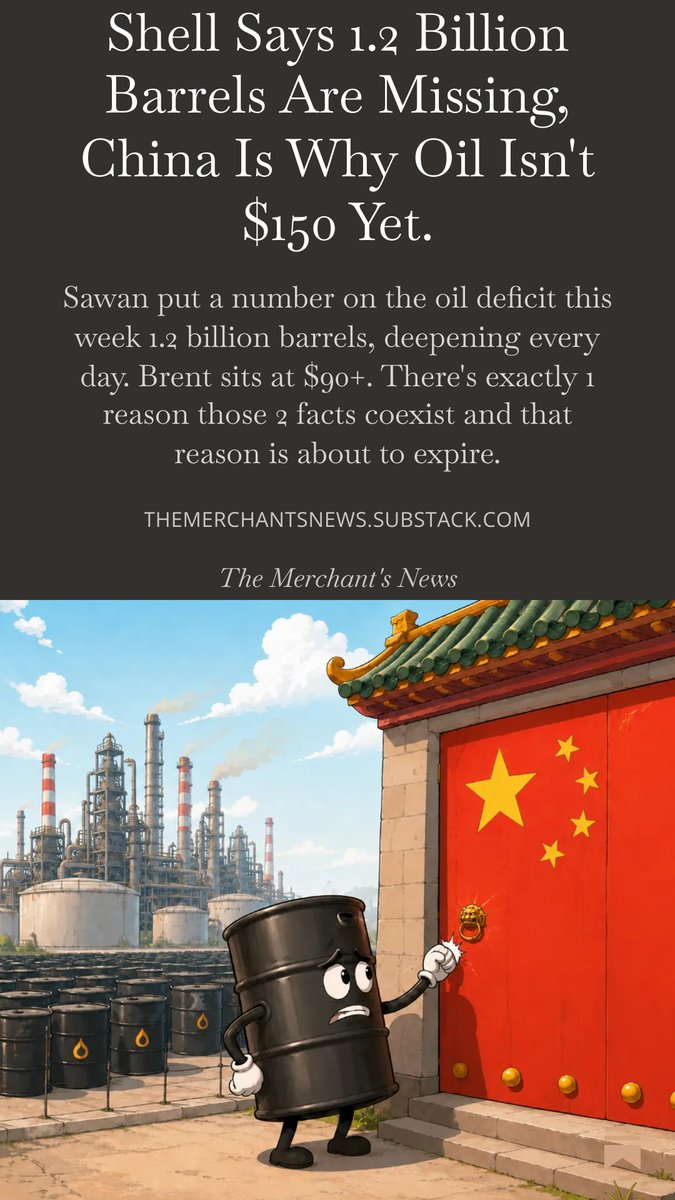

🚨Shell's CEO just put a number on this war

🛢️1.2 billion barrels of crude are missing from the market.

That's 12 days of global consumption.

And in Sawan's own words, the hole is "deepening every single day."

Now the part that should bother you.

Today Iran closed the Strait of Hormuz to all maritime traffic.

US crude inventories drew for the 7th straight week.

Over 10% of global production is offline.

And Brent closed in the low $90s.

A market this short, with its main chokepoint physically shut, should not trade there.

The 1979 Iranian revolution took 5.6 mb/d offline and tripled prices.

The 1990 invasion of Kuwait took 4.3 mb/d.

This disruption is roughly the size of both combined and the price barely moves.

That's a held market.

There is exactly 1 reason oil isn't at $150 already, and it's not OPEC, not demand, and not peace hopes.

It's a single buyer making a deliberate, time limited move that most desks are reading completely backwards as bearish, when it's the most bullish setup on the board.

In my latest article, I walk through the full mechanism

🔗 Link to the full article here👇

open.substack.com/pub/themer…

9

52

128

63,950

US product stocks started 2026 above every prior year.

⚠️They just fell below every prior year.

The yellow line is 2026.

Weeks 1-5: highest stocks in years.

US refiners well-supplied, cushion above historical norms.

Week 10: Iran war. Hormuz closes. US refiners ramp to maximum utilization to fill global gasoline, diesel and jet fuel gaps left by Middle East outages.

Week 21: stocks crash below every single prior year on the chart.

The cushion that absorbed the first months of the Hormuz shock is now gone.

What's left? refiners already running flat-out, product stocks below historical lows, and hurricane season just starting.

Any further disruption a Gulf Coast storm, an unscheduled refinery outage, a demand spike hits a system with no inventory buffer and no spare capacity to respond.

This is what "the US is the swing refiner of last resort" looks like when the buffer runs out.

Gasoline and diesel cracks this summer are one bad headline away from spiking hard.

My latest analysis on oil prices macro is in my article.

Link in the comments 👇

5

14

47

3,484

My latest analysis on oil prices macro is in my article.

Link 👇

themerchantsnews.substack.co…

1

6

899

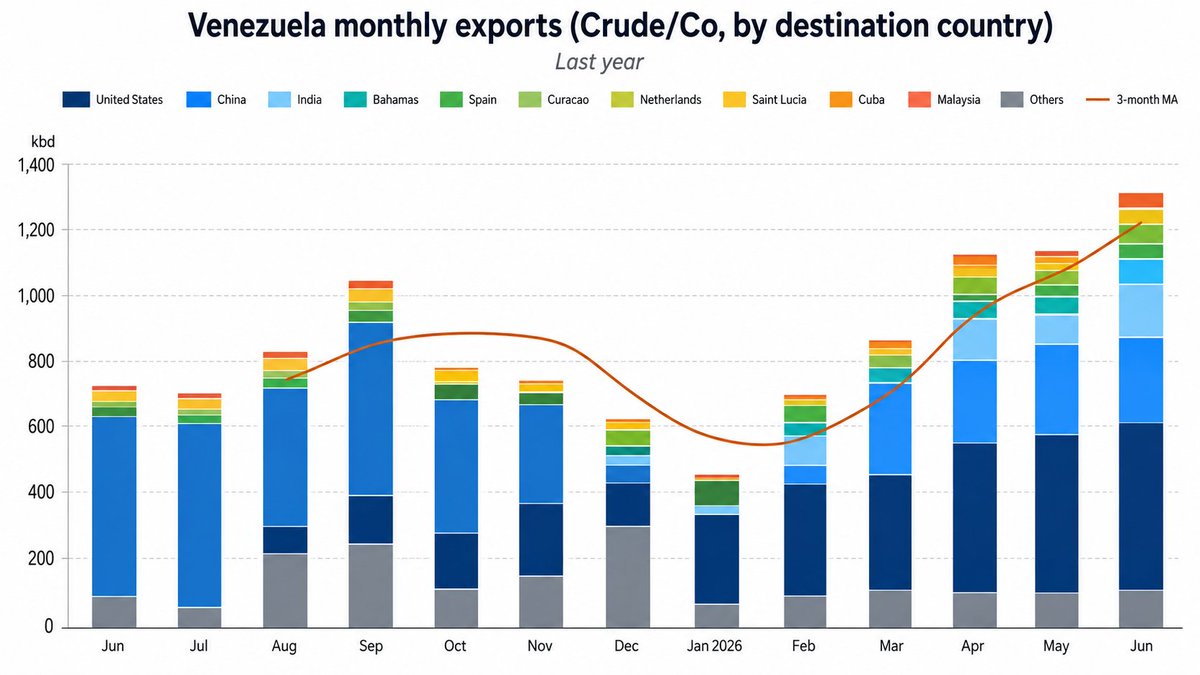

Venezuela's crude exports just hit 1,300,000 barrels per day.

The Hormuz crisis made this possible.

January 2026: exports collapsed to 450 kbd as the Iran war broke out.

June 2026: exports surged to 1,300 kbd nearly tripling in 6 months.

💰3 buyers drove the surge:

🇺🇸 US: the dominant buyer. Gulf Coast refiners need heavy crude to replace lost Middle East supply. Venezuela has it.

🇮🇳 India: barely present in 2025. Now a major buyer — hunting every non-Gulf heavy barrel available.

🇨🇳China: stepped in when US buying dipped, now sharing the market.

The logic is simple.

Iranian heavy crude is off the market.

Middle East sour grades can't transit Hormuz.

US and Asian refiners built for heavy feedstock need replacement barrels urgently.

Venezuela has 1.3 mb/d of heavy crude, Atlantic access, and no Hormuz exposure.

A year ago this was a sanctions story.

Today it's a supply security story.

The Hormuz crisis didn't just disrupt the Middle East.

It rehabilitated Venezuela as a strategic supplier to 3 of the world's largest oil buyers simultaneously.

25

129

408

60,282

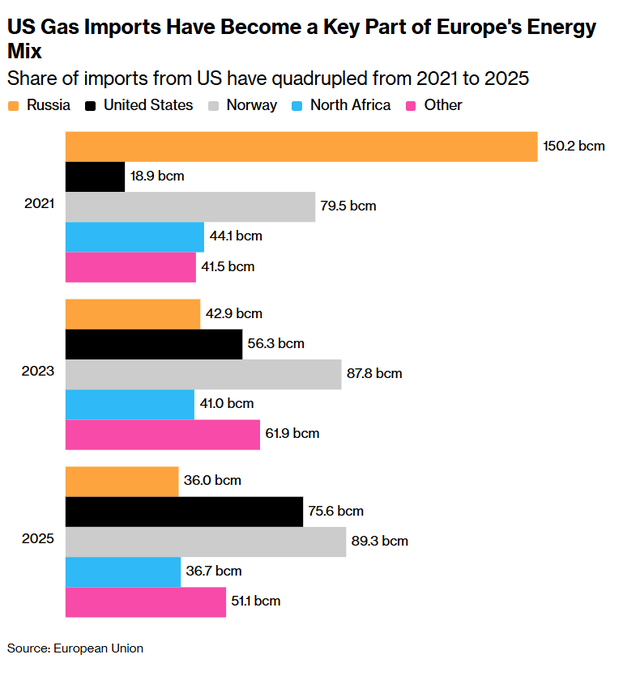

In 2021, Russia supplied 150 bcm of gas to Europe.

In 2025: 36 bcm.

The US went from 19 bcm to 76 bcm.

The numbers:

Russia: 150.2 → 42.9 → 36.0 bcm

United States: 18.9 → 56.3 → 75.6 bcm

Norway: 79.5 → 87.8 → 89.3 bcm (maxed out)

North Africa: 44.1 → 41.0 → 36.7 bcm (declining)

In 4 years, Europe replaced 114 bcm of Russian gas.

The US absorbed most of that gap a 4x increase in LNG exports to Europe.

Norway couldn't save Europe.

It tried output grew from 79.5 to 89.3 bcm but it was already near capacity. North Africa declined. "Other" helped but couldn't scale fast enough.

The US could, and did.

36 bcm of Russian gas still flows to Europe.

The political pressure to restore more especially as Hormuz tightens and prices spike is real.

The chart shows how far Europe has come.

It also shows the remaining exposure.

3

10

51

2,361

Silver Supply Is More Concentrated Than Most Investors Realize 🥈🌍

Mexico remains the world’s largest silver producer at roughly 173 million ounces

Then come

🔹 Peru at 131 million ounces

🔹 China at 113 million ounces

🔹 Russia at 56 million ounces

🔹 Bolivia at 50 million ounces

🔹 Chile and Poland at 43 million ounces each

Mexico alone accounts for around 20% of global supply

That matters because silver is no longer just a precious metal

It is also critical for

🔹 Solar panels

🔹 Electronics

🔹 EVs

🔹 Grid infrastructure

🔹 Industrial applications

And global silver supply has now run a deficit for five straight years

The signal is clear

Demand is rising

Supply remains concentrated

And the biggest producers are becoming more strategically important

3

8

33

1,880

FPSO vs FLNG vs FSRU vs FSO vs FSU 🚢

These offshore assets may look similar

But they do very different jobs

🔸FPSO

Produces, processes, stores and offloads oil and gas

🔸FLNG

Produces, liquefies, stores and exports LNG offshore

🔸FSRU

Receives LNG, stores it and converts it back into natural gas

🔸FSO

Stores crude oil and offloads it to tankers

🔸FSU

Provides floating storage for LNG, LPG, condensate or crude

The simplest way to remember them

🔹 FPSO = offshore factory

🔹 FLNG = floating LNG plant

🔹 FSRU = floating LNG import terminal

🔹 FSO = oil storage on water

🔹 FSU = flexible storage unit

Why they matter

🔹 Lower upfront cost

🔹 Faster deployment

🔹 Greater flexibility

🔹 Better access to remote fields

🔹 Stronger energy security

Offshore energy is not just about production

It is about choosing the right floating infrastructure for the right molecule

4

21

79

3,414

Ukraine Strikes 2 More Russian Energy Assets 🇺🇦💥🇷🇺

A joint Ukrainian drone strike targeted the Tamanneftegaz oil and gas terminal in Russia’s Krasnodar region

According to Ukraine’s SBU, the attack hit

🔹 5 fuel storage tanks

🔹 2 oil loading stands

🔹 Freight and storage areas at the terminal

🔹 Multiple facilities supporting oil, fuel and LPG exports

Russian regional authorities reported a major fire at the sea terminal in Volna, with 1 person killed and 3 injured (AP News)

Ukraine’s General Staff also reported a separate strike near Kotovo in the Volgograd region

The targeted facility is used for

🔹 Oil processing

🔹 Pipeline transportation

🔹 Pumping crude to Russian refineries

🔹 Supplying export infrastructure

A fire was reported at the site, although the full extent of the damage remains unclear (Reuters)

The message is clear

Ukraine is not only targeting refineries

It is targeting the full Russian oil system

🔹 Storage

🔹 Loading

🔹 Pipelines

🔹 Pumping stations

🔹 Export infrastructure

Every successful strike raises the cost and complexity of moving Russian energy

2

7

21

15,483

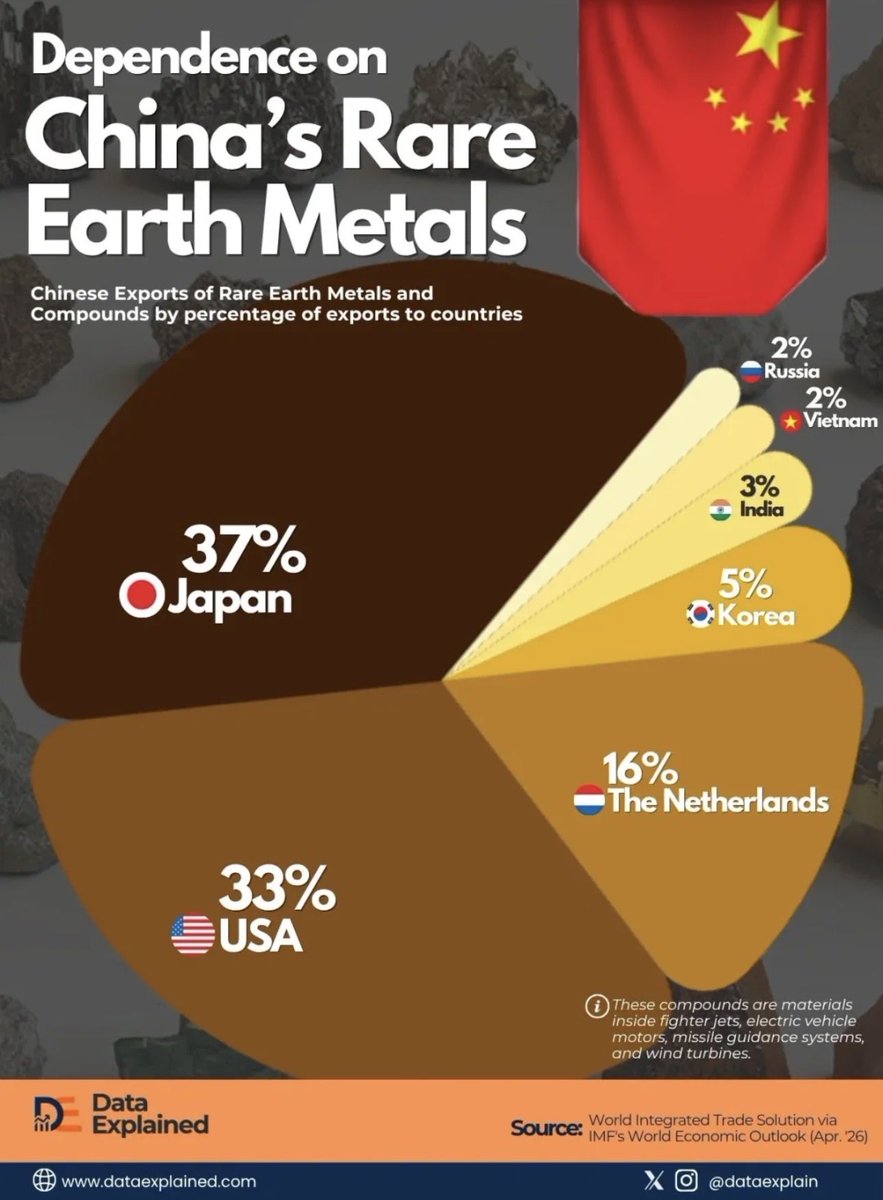

Rare Earths Are the New Supply Chain Chokepoint. 🇨🇳⚙️

China’s rare earth exports are heavily concentrated.

🇯🇵Japan takes 37%

🇺🇸The US takes 33%

🇳🇱The Netherlands takes 16%

🇰🇷Korea takes 5%

That matters because rare earths sit inside the systems every major economy needs:

EV motors

Wind turbines

Missile guidance

Fighter jets

Advanced electronics

This is not just a mining story.

It is industrial security.

The West can design the technology.

But if China controls the materials, China controls the bottleneck.

11

34

95

4,826

Global Trade Runs Through a Few Narrow Gates 🚢🌍

This map shows the world’s key maritime chokepoints

🔹 Malacca Strait

🔹 Taiwan Strait

🔹 Strait of Hormuz

🔹 Suez Canal

🔹 Bab el-Mandeb

🔹 Panama Canal

🔹 Cape of Good Hope

These routes carry the flows that keep the global economy moving

🔹 Oil

🔹 LNG

🔹 Containers

🔹 Food

🔹 Minerals

🔹 Manufactured goods

That is why chokepoints matter

A local disruption can quickly become a global price shock

🔹 Higher freight

🔹 Higher insurance

🔹 Longer routes

🔹 Delayed cargoes

🔹 Tighter supply chains

Globalization was built on efficiency

Energy security is now about resilience

4

17

34

2,370

Jun 12

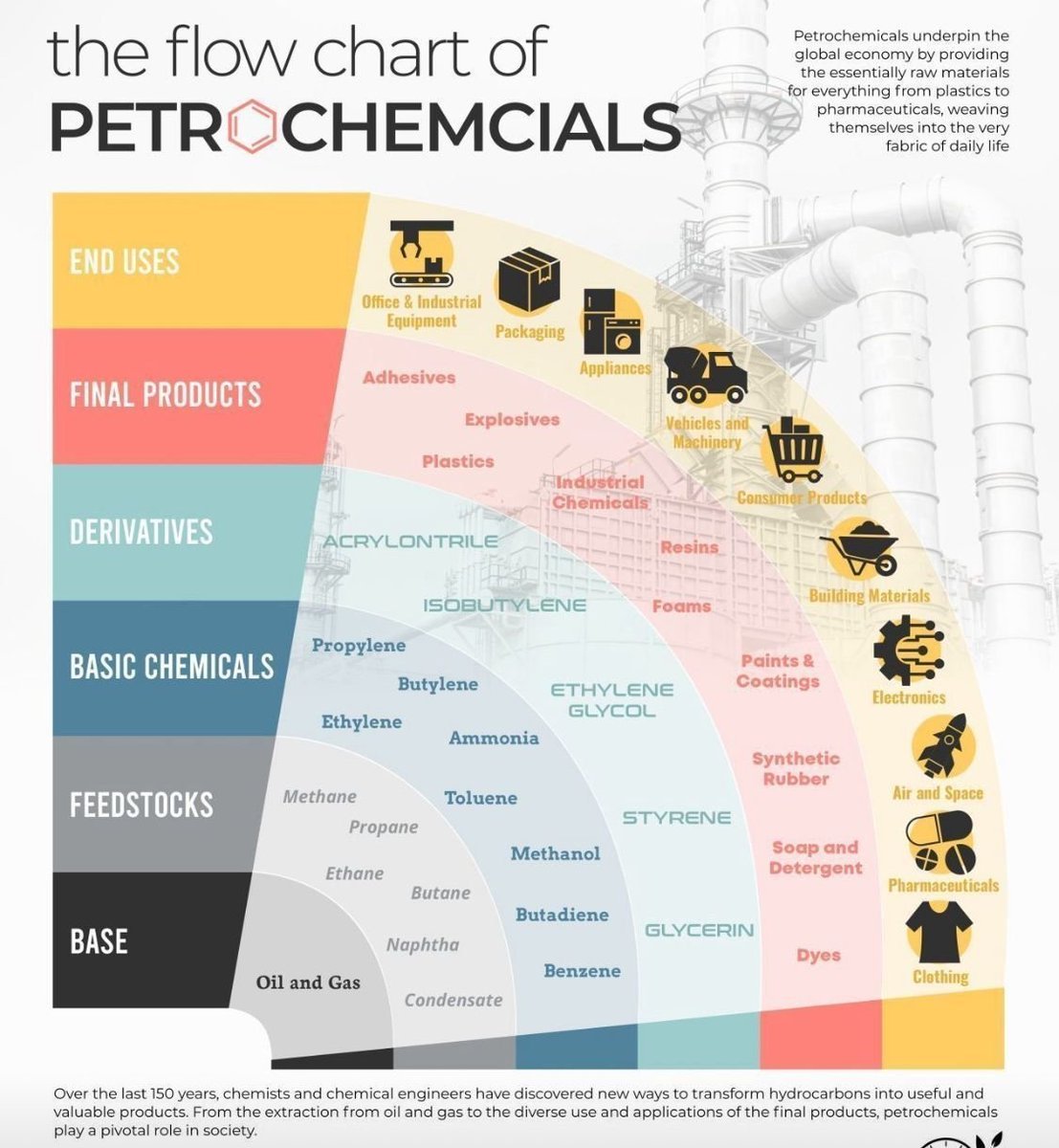

🛢️ Oil Is Not Just Fuel. It Is the Base of the Industrial Economy

Oil and gas become feedstocks like naphtha, ethane and propane.

These are turned into basic chemicals such as ethylene, propylene and methanol.

Which then produce:

• Plastics

• Synthetic rubber

• Resins and foams

• Industrial chemicals

And finally the products we use every day:

📦 Packaging

🚗 Vehicles

📱 Electronics

🏗 Building materials

💊 Pharmaceuticals

When oil markets are disrupted.

The entire manufacturing chain feels it.

My latest analysis on oil prices macro is in the below comments👇

7

46

156

5,883

Jun 12

🛢️The oil market now has a deadline: end of July

3 buffers have kept crude under $100 through the worst supply disruption in history.

ING says all 3 run out at roughly the same time.

Regular readers will recognize every one of them.

1️⃣China

China's buyer strike imports at the lowest since 2017, refinery runs slashed, drivers switching to EVs rather than pay war prices.

But Beijing started tapping its strategic reserves last month. The strike is now running on stored barrels.

Stocks, not flows. The clock is visible.

2️⃣ US exports

US crude exports are running 1.8M bpd above last year record highs.

The catch, per ING: those exports come from INVENTORY, not new production. Cushing is near operational lows.

Watch for the political risk nobody prices: a US export intervention if domestic tightness bites.

3️⃣the SPR

The US strategic release ends by late July with the reserve already at 1983 levels.

After that, no government cushion, peak summer demand, and a market ING says is in deficit all quarter.

Three buffers, one expiry date.

ING's path: Brent averages $110 in Q3, spiking $120–130 if Hormuz stays shut past July.

And one detail that should stop you cold: ING floats buyers eventually paying IRAN tolls for safe passage.

From blockade to toll booth that's how chokepoints monetize.

None of this is new to this feed: the buyer strike, the export drain, the SPR clock I covered each as it built.

What's new is convergence.

August oil will be decided by whoever blinks first: Tehran, Washington, or Beijing's inventory managers.

My latest analysis on oil prices is in the below comments👇

19

93

262

25,562

Jun 12

There is exactly 1 reason oil isn't at $150 already, and it's not OPEC, not demand, and not peace hopes.

It's a single buyer making a deliberate, time limited move that most desks are reading completely backwards as bearish, when it's the most bullish setup on the board.

In my latest article, I walk through the full mechanism

🔗 Link to the full article here👇

open.substack.com/pub/themer…

Jun 11

🚨Shell's CEO just put a number on this war

🛢️1.2 billion barrels of crude are missing from the market.

That's 12 days of global consumption.

And in Sawan's own words, the hole is "deepening every single day."

Now the part that should bother you.

Today Iran closed the Strait of Hormuz to all maritime traffic.

US crude inventories drew for the 7th straight week.

Over 10% of global production is offline.

And Brent closed in the low $90s.

A market this short, with its main chokepoint physically shut, should not trade there.

The 1979 Iranian revolution took 5.6 mb/d offline and tripled prices.

The 1990 invasion of Kuwait took 4.3 mb/d.

This disruption is roughly the size of both combined and the price barely moves.

That's a held market.

There is exactly 1 reason oil isn't at $150 already, and it's not OPEC, not demand, and not peace hopes.

It's a single buyer making a deliberate, time limited move that most desks are reading completely backwards as bearish, when it's the most bullish setup on the board.

In my latest article, I walk through the full mechanism

🔗 Link to the full article here👇

open.substack.com/pub/themer…

15

46

272

50,317

Jun 12

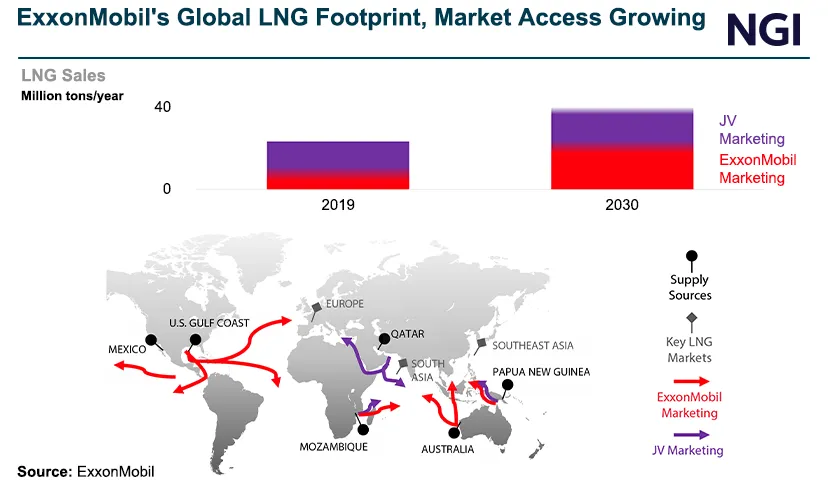

🚨ExxonMobil is internally studying Woodside Energy as an acquisition target.

Woodside ADRs jumped 6% on the news.

After a $60 billion Pioneer deal, Exxon may be about to make the biggest LNG bet in industry history 🇦🇺⚡

Bloomberg reported ExxonMobil has been running internal M&A scenarios on multiple targets Woodside Energy is among them.

No offer yet, but the market reaction says investors think the logic is real.

Why Woodside fits Exxon's playbook perfectly?

North West Shelf, Pluto LNG, Scarborough Pluto Train 2 (under development).

Browse gas resources.

60–70% of Woodside's revenue is LNG, flowing into Japan, Korea, China on long-term contracts.

Exxon already runs LNG out of QatarEnergy, Golden Pass (Texas, >18 mtpa), PNG and Mozambique.

Adding Australia completes the global LNG map every major basin, every major Asian buyer.

What Exxon is actually building?🧱

Pioneer gave Exxon the Permian.

The signal after closing: more M&A where long life, large scale assets can anchor decades of cash flow.

Woodside is exactly that a Tier-1 operator with long-life gas in the world's highest-value LNG market. 💰

⚠️Woodside is Australia's flagship upstream company.

Any US supermajor takeover goes through Australian foreign investment and national interest review.

A full deal would likely be a multi tens of billions transaction comparable to Pioneer in scale.

💡also Shell, bp, TotalEnergies... Every major is trying to lock in long-term LNG volume for Asia right now because the Iran war just made every buyer in the world want contracts signed yesterday.

The race to own premium LNG supply is accelerating.

Woodside is one of the last mega prizes available.

(subscribe to my newsletter link in my bio)

7

19

61

6,203

Jun 12

🛢️🚨Shell, in a single day:

-Pauses its $3B share buyback.

-Prepares to sell $1B of offshore wind farms.

-Pushes toward closing a $16.4B gas acquisition, its biggest deal in a decade.

That's one company telling you its thesis.

💰The deal:

The ARC Resources acquisition is Shell's largest since BG in 2016 and the logic is geographic.

ARC's gas sits next to Shell's fields feeding LNG Canada (Shell: 40%).

LNG Canada ships to Asia without touching Hormuz, Suez OR Panama. The shortest safe route on the map.

Why Shell needs it?

Shell's quiet problem are aging fields and dwindling reserves.

Analysts said it needed a big discovery or a big deal.

It chose the deal paid 75% in shares, at a 20% premium.

When a supermajor pays up with its own equity, it's telling you which assets it thinks outlast the cycle.

Same day: wind farms for sale, India renewables under review, buyback already cut from $3.5B to preserve cash after war-related strain.

Under Sawan, Shell isn't an "energy company" anymore. It's becoming a gas-and-LNG machine with an oil business attached.

Follow the full year: Gunvor buys US shale gas.

Shell signs in Venezuela, blocks rivals at Browse, now $16.4B for Canadian gas while selling wind.

The biggest players have stopped debating the transition's pace.

They're positioning for a long gas era.

11

76

311

29,709

Jun 12

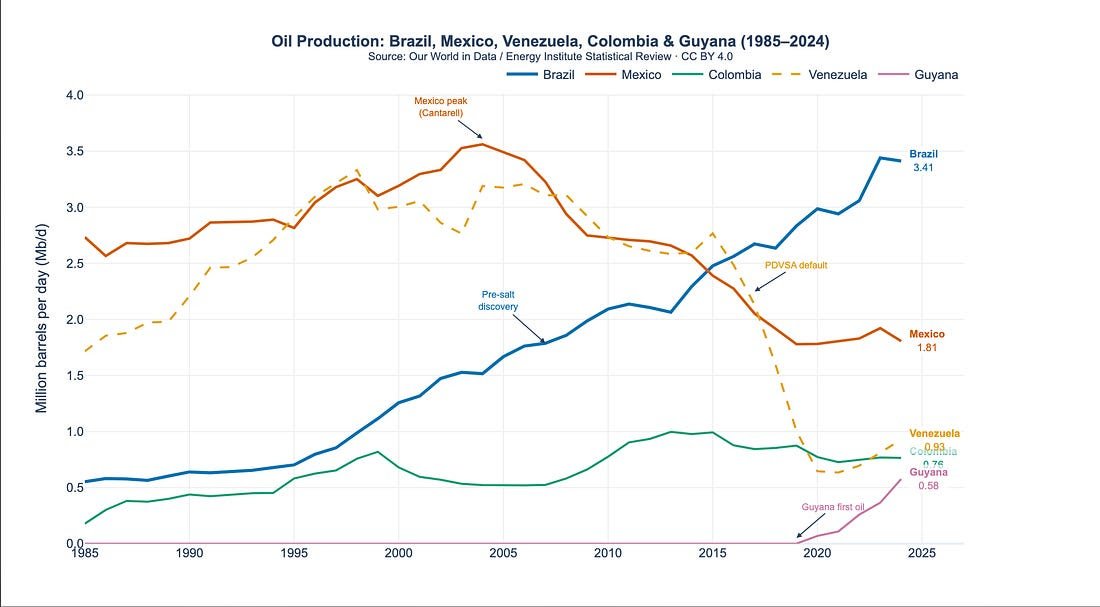

In 1998, Venezuela pumped 3.3M bpd and Brazil barely 1M.

Today Brazil does 3.4M and Venezuela 0.9M.

Same continent.

Same geology era.

Opposite outcomes.

Rocks don't decide who produces oil, decisions do.

Venezuela holds the largest proven reserves on Earth and produces less than a quarter of its 1998 peak.

The chart marks the moment, PDVSA's default.

Underinvestment, politicized management, sanctions.

Reserves without capital and competence are just expensive dirt.

Mexico: Cantarell peaked at 3.55M in 2004, then halved a supergiant's natural decline never replaced.

Brazil: pre-salt discovery → patient investment → 3.41M bpd and climbing.

Guyana: zero in 2019, 0.58M 5 years later. Fastest oil ramp of the modern era.

This chart explains this month's news:

Shell signing in Caracas = majors betting Venezuela's curve can bend back up.

Petrobras buying Campos acreage = Brazil extending its winning streak.

Guyana's line = the steepest growth on the planet.

Production capacity is built or destroyed over DECADES, but priced in days.

Venezuela took 20 years to lose 2.5M bpd.

No deal, no peace, no Shell signature brings it back fast.

6

16

55

3,844

Jun 12

🇺🇸 The US Is Still the Global Oil Engine

13 Million Barrels a Day🛢️

United States 13.2 mb/d... the world’s largest oil producer

🇷🇺 Russia 10.2 mb/d

🇸🇦 Saudi Arabia 9.2 mb/d

🇨🇦 Canada 5.1 mb/d

🇮🇷 Iran 4.3 mb/d

the US remains the global energy anchor not OPEC, not Saudi Arabia, not Russia.

If you want to understand what’s moving the oil markets right now do not miss my latest article.

Link for the full article is in the comments👇

10

46

115

5,019