Jun 12

Gold Sector in M&A Frenzy: Dwindling Reserves Drive B2Gold and Orezone – Hidden Gem: Desert Gold #Gold #Commodities #Investments #Africa #M&A news.financial/comments/gold…

1

62

May 22

Orezone Gold Corporation $ORE / $ORZCF

Orezone reported its first drill results from the recently acquired Casa Berardi Mine, including 16.10 g/t Au over 6.7 metres and 6.47 g/t Au over 21.5 metres.

The results support planned pit expansions and continued evaluation of down-plunge continuity, adding momentum to Orezone’s development work at the Quebec gold operation.

@OrezoneC

Link: globenewswire.com/news-relea…

#Gold #Mining #Quebec

5

12

4,534

ORE reported initial drill results from the Casa Berardi mine in Quebec, including 16.10 g/t Au over 6.7m and 6.47 g/t Au over 21.5m from the F160 and F134 zones. Orezone says drilling is targeting pit expansion and underground potential.

Read more: orezone.com/press-releases/o…

1

2

128

May 20

May 20 #ASX #drilling lnkd.in/eBk7tF_5

Get in your inbox @ market open: lnkd.in/ePSrAwSb

Fin Resources Limited $FIN.AX | Orezone Gold Corporation $ORE.TO | Meeka Metals Limited $MEK.AX | Cazaly Resources Limited $CAZ.AX | GBM Resources Ltd $GBM.AX | Saturn Metals Limited $STN.AX | MB Gold Limited $MBG.AX | Barton Gold $BGD.AX | Strata Minerals Limited $SMX.AX | Corazon Mining $CZN.AX | GIBB River Diamonds Ltd $GIB.AX | Marimaca Copper $MARI.TO | Amara Minerals #AM3 | Enova Mining $ENV.AX | Benz Mining Corp. $BZ.V

#gold #copper #antimony #REE #tungsten #ASX

1

2

3

1,350

May 19

Canadian Earnings — Last Week's Winners

May 11–17

Sector winners who delivered at least one of:

✓ Revenue growth

✓ Margin expansion

✓ Guidance raise

✓ Capital action

⚡ ENERGY

$PEY.TO — Peyto Exploration

Quadruple win. Record Q1 production 147,513 boe/d ( 10% YoY), $293M FFO, $171M earnings, dividend hiked 9%, $89M debt repaid in the quarter. Cash costs $1.28/Mcfe (-10% YoY). Half of 2026 gas hedged at $3.96 already.

$BIR.TO — Birchcliff Energy

Revenue $217.8M ( 10% YoY), OCF 21%, free funds flow 260%, debt down $36.5M from year-end. Realized 112% premium to AECO.

$NPI.TO — Northland Power

Revenue $774.6M vs $665.1M ( 16.5% YoY), NI to shareholders $88.6M, OCF $571M.

$LGN.V — Logan Energy

Production 43% YoY (14,237 boe/d), sales 37%, adj funds flow 56%, OCF 62%. Closed $66.3M Simonette acquisition, raised $70M equity, borrowing base upsized $150M → $250M.

$KEI.TO — Kolibri Global Energy

Gross revenue US$24.7M ( 17% YoY), production 15% to 4,685 BOEPD, Adj EBITDA $14.8M, FCF $9.2M. Strong cash generation as drilling cycle moderates.

$KEY.TO — Keyera

Plains Canadian NGL business acquisition CLOSED May 12 (within window) — major capital action. Q1 OCF $322M, DCF $133M adjusted for acquisition costs.

⛏️ MINING & METALS

$DSV.TO — Discovery Silver

Revenue $285M vs $0 prior year — first full quarter at Cordero post-Newmont acquisition. 60% mine margin, OCF flipped from -$6M to $43M.

$KNT.TO — K92 Mining

Quarterly record revenue $236.3M ( 63% YoY), EBITDA $179.9M ( 68%), net earnings $116.6M ( 66%), OCF $114.2M ( 81%). Cash hit record $287M.

$USA.TO — Americas Gold and Silver

Revenue nearly tripled YoY (record). Profit flipped from $19.7M loss to $9.98M profit. OCF up $21.9M, cash to $122M.

$GMIN.TO — G Mining Ventures

Revenue $139.9M ( 43% YoY), OCF $69.7M, FCF $56.2M. G2 Goldfields acquisition closed April 9, consolidating the Oko district in Guyana.

$FNV.TO — Franco-Nevada

Operating income $577.8M, OCF $520.4M — Q1 OCF 39% above FY2025 quarterly average.

$AAUC.TO — Allied Gold

Zijin C$44/share all-cash deal closing May 29 — final quarterly print before delisting. Headlines understate it; binding takeover within the window is a real capital event.

$ORV.TO — Orvana Minerals

Record quarter. OCF $29.9M, cash grew $32M → $48M.

$ABX.TO — Barrick Mining

Adj net EPS $0.98 ( vs PY despite 17% QoQ production drop on seasonal pattern), AISC -4% YoY, realized gold $4,823/oz ( 66% YoY). $3B buyback authorized. Hemlo and Tongon divestitures completed in Q1.

$APM.TO — Andean Precious Metals

Revenue $163.1M ( 163% YoY), gross profit 228%, net income $48.2M ( 230%), Adj EBITDA $71.0M ( 224%). FCF $39.6M vs -$1.5M PY. Filed for NYSE listing. $204M in liquid assets, net cash ~$70M.

$ORE.TO — Orezone Gold

Revenue US$185.9M ( 125% YoY), net earnings $39.6M ( 148%), Adj EBITDA $94.2M (record). Gold production 35%. Stage 1 hard rock plant declared commercial production. Casa Berardi (Hecla Quebec) acquisition closed March 25 — total assets nearly doubled to $1.30B.

$ASM.TO — Avino Silver & Gold Mines

Revenue US$39.4M ( 109% YoY, record), net income $15.9M ( 183%, record), EBITDA $25.5M ( 163%). Silver realized $86.42/oz ( 173%). Cash $138.6M ( $36.9M QoQ). NCIB approved. Maiden 127M Ag-eq oz P&P reserve published.

$GAU.TO — Galiano Gold

Gross revenue US$166.5M ( 117% YoY), Adj EBITDA $93.4M ( 364%). Mine operations flipped to $72.5M profit from $19.8M loss prior year. Gold production 68%. Zero debt, $114.9M cash.

$DNG.TO — Dynacor Group

Sales US$154.1M ( 93% YoY), EBITDA $13.6M ( 86%), net income $7.3M ( 42%). Q1 record processing and production. Senegal pilot commissioning Q2 2026.

$JAG.TO — Jaguar Mining

Revenue US$44.6M ( 22% YoY), gross profit $27.9M (margin 63%). MTL strategic production restart announced. Realized gold prices driving operational reset.

$AYA.TO — Aya Gold & Silver

Revenue US$117.3M ( 247% YoY, record), gross profit $83.8M (margin 71.4%), net income $48.5M (vs $6.9M PY). OCF $70.2M ( 785% YoY, record). Production 40% YoY. Cash $171.7M; $14M debt principal repaid.

💰 FINANCIALS

$MFC.TO — Manulife

Core earnings 8% CER, Core EPS 11%, dividend 10%, $1.2B returned to shareholders, Core ROE 16.5% ( 90 bps YoY). Schroders Indonesia acquisition closed.

$POW.TO — Power Corp

Net earnings $820M ( 19% YoY), Adj EPS $1.43 ( 17%). $1.2B returned to shareholders in Q1 ($0.8B dividends $0.4B buybacks). Sagard-Unigestion combination closed April 2026. Great-West ROE 16.8%, IGM AUM $314B ( 14% YoY).

💻 TECHNOLOGY

$CSU.TO — Constellation Software

Revenue $3,181M ( 20% YoY), organic 6%, OCF 9%, FCFA2S 44%. $1.00/share dividend declared, $809M deployed on Q1 acquisitions.

$VCM.TO — Vecima Networks

VBS revenue 9.6% YoY, Entra DAA deployments 13.5%, Adj EBITDA 9.2%. Calendar 2026 revenue growth guidance RAISED to 22.5–30% (from 20–30%). Charter Spectrum multi-year DOCSIS 4.0 deal announced. Third consecutive quarter of gross margin expansion.

$QBR-A.TO — Quebecor

Net income to shareholders $225.4M ( 18% YoY), basic EPS $1.00 ( 22%), Adj EBITDA $576.6M ( 4.9%). Telecom adj EBITDA 6.6%. $85.2M Class B repurchases.

$CGY.TO — Calian Group

Q2 FY2026 revenue $228.7M, net profit $6.7M (record), EPS $0.59. Adjusted EBITDA $28M ( 60% YoY). Defense and Health segments driving the print.

$QTRH.TO — Quarterhill

Revenue US$38.6M ( 14% YoY), gross margin 1,600 bps to 28%. Operating loss halved to -$3.7M from -$7.3M. AI-driven intelligent transportation systems segment grew sharply.

🏭 INDUSTRIALS

$FTT.TO — Finning International

Record Q1 adjusted EPS $1.02. Product support 6% YoY (8th consecutive quarter). Dividend raised 7.4% to $0.325 — 25th consecutive year of increases. Equipment backlog $3.8B (record). Adj ROIC 18.7%.

$BRM.V — Biorem

Revenue $6.8M ( 44% YoY). Net earnings flipped to $201K profit. Record $77M order backlog. 18.6M share float.

$MAL.TO — Magellan Aerospace

Revenue $285.1M ( 9.3% YoY), gross margin 130 bps to 14.2%, EBIT 41.5%, Adj EBITDA 35.4%, EPS $0.29 ( 52.6%). Signed TKMS Teaming Agreement on Canadian Patrol Submarine Project torpedoes.

$ANRG.TO — Anaergia

Revenue $55.2M ( 122% YoY), gross profit 135%, margin 130 bps to 23.0%. Adjusted EBITDA flipped positive ($1.1M vs -$3.9M). Third straight quarter of positive Adj EBITDA.

$GRN.TO — Greenlane Renewables

Revenue $9.5M ( 36% YoY), gross margin 300 bps to 43%. System sales 38% YoY, parts & service 32%. Signed Panasonic Brazil definitive agreements for Cascade LF localization. Backlog $31.5M.

$ATRL.TO — AtkinsRéalis

Revenue $3.0B ( 18% YoY), Adj EBITDA $253.7M ( 18%), net income to shareholders $92.8M ( 34%), diluted EPS $0.56 vs $0.39. Cash $1.1B. Engineering Services and Nuclear segments drove the print.

⚡ UTILITIES

$H.TO — Hydro One

Revenue $2,648M ( 10.0% YoY), net income to common $391M ( 9.2%), EPS $0.65 ( 8.3%). Selected to develop Greenstone, Sudbury-to-Barrie, and Red Lake Transmission Lines — extends rate base growth into the late 2020s.

$BLX.TO — Boralex

Revenue $286M ( 21% YoY), production 12% to 1,888 GWh, operating income $92M ( 42%). Brookfield La Caisse going-private agreement at $37.25/share (31.8% premium) — shareholder vote scheduled for June 4, 2026.

💎 ROYALTIES

$ELE.TO — Elemental Royalty

Record revenue US$24.3M ( 83% YoY), Adj EBITDA $17.7M ( 55%), OCF 340% YoY. Inaugural US$0.12/share dividend, new US$150M revolver, 2.5% NSR acquired post-quarter on Western Queen Gold.

$DIV.TO — Diversified Royalty

Revenue 11.8% YoY, distributable cash 10.4%, dividend 13.9% YoY. Binding agreement to acquire Mr. Lube Tires franchisor; BarBurrito added 9 restaurants to royalty pool.

🛒 CONSUMER

$CTC.TO — Canadian Tire

Net income 176% YoY ($129.5M vs $47.0M continuing). Diluted EPS $2.02 vs $0.67 ($2.00 normalized). Retail revenue ex-petroleum 5%. SportChek 3.3% comp (7th straight growth quarter), Mark's 1.2%. $64.5M buybacks $90.7M dividends paid.

$XLY.TO — Auxly Cannabis

Revenue $39.8M ( 22% YoY), gross margin 55% ( 700 bps from 48%). Adj EBITDA $12.3M ( 65%) — 31% margin. OCF before WC $11.3M ( 102%). NCIB authorized.

🏥 HEALTHCARE / M&A

$CTX.TO — Crescita Therapeutics

ClinActiv take-private at $0.80/share — 74% premium to 5-day VWAP. Shareholder vote held May 14. Expected to close Q2 2026.

Full breakdowns: investorlens.io

#TSX #CanadianStocks #Earnings #FinTwit

2

6

648

May 13

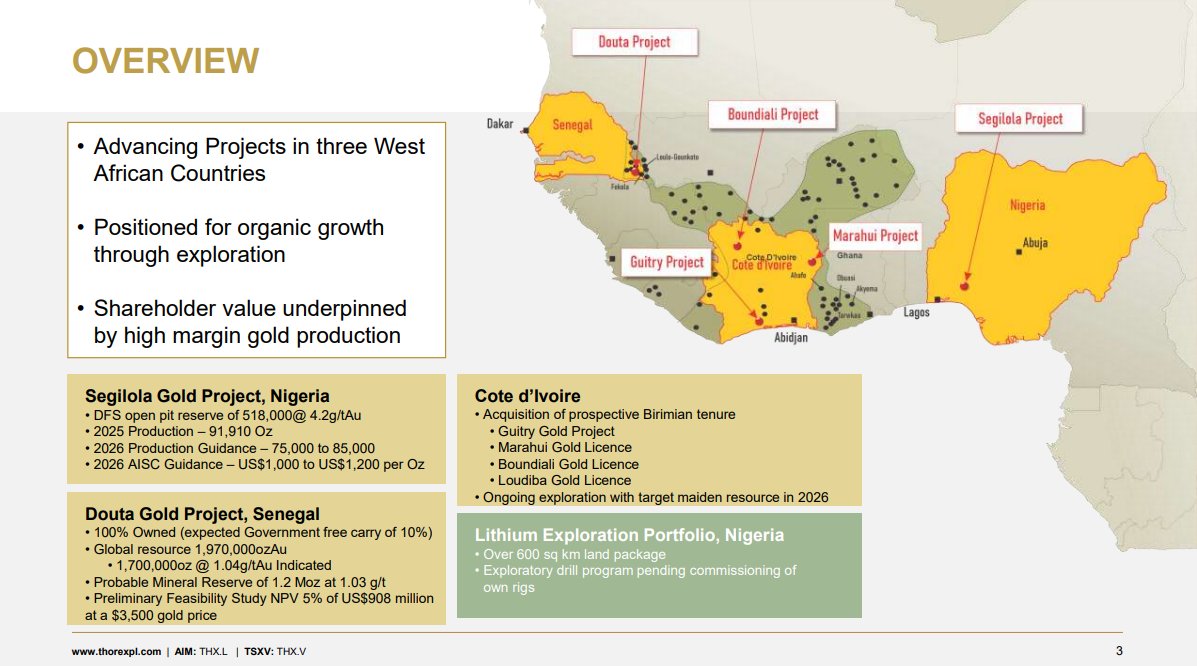

Unlocking West African Alpha: A Deep Dive into Thor Explorations Ltd. $THX.V⛏️

Thor Explorations has successfully transitioned from a high-risk explorer to a premier, high-margin gold producer.

As of May 2026, the company stands as a beacon of execution in a volatile sector. Here is the institutional-grade breakdown:

1. The Company & Structure

Thor is the pioneer of modern industrial mining in Nigeria with its flagship Segilola Gold Mine and is rapidly expanding into Senegal (Douta Project).

The shareholder base is institutional-heavy, anchored by the Africa Finance Corporation (AFC), with significant management "skin in the game" led by CEO Segun Lawson. The narrative has shifted from "proving Nigeria works" to "how fast can we scale in West Africa?"

2. Production & Development

The Segilola Mine remains the cash cow, producing ~91,910 oz in 2025 with 2026 guidance targeting 75k-85k oz at an enviable AISC of $1,000 - $1,200/oz.

However, the real growth engine is the Douta Project in Senegal. The 2026 PFS highlights a massive Pre-Tax NPV (5%) of $908M with a 73% IRR.

Thor is evolving into a diversified multi-asset producer with additional lithium exploration upside.

3. Valuation Snapshot (May 13, 2026)

Market Cap: ~946.5M CAD (~$690M USD) at $1.42/share.

Net Debt: Effectively in a Net Cash position (calculating Net Debt strictly without leasing liabilities).

Enterprise Value (EV): ~$670M USD.

EBITDA: Strong operational margins drove 2025 EBITDA to the $140M - $160M USD range.

The balance sheet is pristine, allowing for growth without traditional equity dilution.

4. The Execution Track Record

Thor achieved first gold at Segilola in July 2021.

Critically, the project was delivered on a ~$100M CAPEX budget—an incredible feat of capital discipline in a sector known for cost overruns.

5. Peer Group & Market Position

Compared to peers like Orezone or Galiano, Thor has historically traded at a discount due to its single-asset profile. That gap is closing.

Thor’s unique edge? A robust dividend policy (approx. $32M returned to date), which is almost unheard of for a junior-to-mid-tier grower.

6. 2030 Forecast: The Road to 200k Ounces

By 2030, with Douta in full swing and Segilola moving toward underground operations:

Projected Production: 150k - 180k oz p.a.

Projected EBITDA: ~$180M - $220M USD (assuming normalized gold prices).

Valuation: Trading at a forward EV/EBITDA of ~3x-4x, there is significant re-rating potential toward the 5x industry average as Douta de-risks.

7. Risks vs. Opportunities

Risks: Geopolitical shifts in West Africa and single-asset dependency until Douta is commissioned in 2027.

Chances: Aggressive $27M-$33M exploration budget for 2026 could significantly extend Mine Life (LOM) and unlock Tier-1 scale potential in Senegal.

Conclusion

Thor Explorations is a rare "Execution Play." They built the mine, paid down the debt, and are now paying the shareholders while funding a Tier-1 project in Senegal from cash flow.

For those seeking West African gold exposure with a disciplined management team, THX remains a top-tier pick.

Disclaimer: Not a financial advice. Always do your own DD. 📈📊

#GoldMining #Stocks #Investing #ThorExplorations #Mining #WestAfrica #Gold #THX #Finance

1

1

5

551

Orezone to announce Q1 2026 results on May 13 (after TSX close).

Webcast:

May 13 – 2pm PT / 5pm ET

May 14 – 7am AEST

Listen: edge.media-server.com/mmc/p/…

3

110

Orezone Q1 2026 Update:

• 38,789 oz gold produced (vs 28,688 YoY)

• 37,962 oz sold

• $4,887/oz avg price

• Bomboré: 37,563 oz

• Casa Berardi: 1,226 oz (post-acq)

• Commercial production achieved Jan 16

orezone.com/press-releases/o…

#Gold #Mining #ORE

2

8

254

Burkina Faso is demanding the right to own 40% of West African Resources' mine. They already have 15% free carry. Now they are demanding the ability to purchase an additional 25%. They will receive 40% of the profit.

Orezone Gold and IAMGold both have large mines in Burkina Faso. They likely will face the same demand. 🙄

mailchi.mp/c1a926748dd3/annu…

34

8

176

22,795

Orezone Gold Completes Strategic Acquisition of Casa Berardi Gold Mine and Quebec Exploration Portfolio $ORE.TO tinyurl.com/2xzhnvxq

2

1,416

Here’s the full list additions/deletions.

Realized the attachment was quite legible for some.

Added (27):

Montage Gold Ord

Merdeka Gold Res Ord

Hycroft Mining Holding Corp

Americas Gold and Silver Corp

Snowline Gold Corp

Southern Cross Gold Cons Ltd

Abrasilver Resource Corp

Tongguan Gold Group Ltd

Osisko Development Corp

Predictive Discovery NPV

Orezone Gold Corp

Dateline Resources NPV

G2 Goldfields Inc

Collective Mining Ltd

Integra Res Corp

Galiano Gold Inc

Archi Indonesia Tb

CNMC Goldmine Hold NPV

Andean Precious Metals Corp

GT Gold Hold Ltd

West Red Lake Gold Mines Ltd

Vox Royalty Corp

Andean Silver Ltd NPV

Antipa Minerals NPV

Founders Metals Inc

U S Gold Corp

J Resources Asia P

Deleted (3):

Royal Gold Inc

Blue Gold CL A Ord

Pan American Silver Corp

#Gold #GDXJ

🚜⚒️🌎🥇

2

2

20

7,620

$FNV – Franco-Nevada

Record revenues, update on Cobre Panama, and interesting acquisitions, a lot to like here.

- Royalty portfolio from Victoria Gold, Banyan Gold $BYN & i-80 Gold $IAUX, C$55M, Yukon & Nevada

- Bullabulling Gold Project royalty, Minerals 260 $M260, A$170M A$50M equity, Western Australia

- Granite Creek, Ruby Hill, Cove & Lone Tree royalty, i-80 Gold $IAUX, $250M, Nevada

- Casa Berardi gold stream, Orezone Gold $ORE, $100M, Quebec

- Yilgarn Star Gold Mine royalty, Barto Gold Mining (private), $4.7M, Western Australia

1

1

23

2,384

Mar 5

@SummitRoyalties: How a New Precious Metals Royalty Company Amassed 47 Assets in Four Months

- Summit Royalties built a 47-asset portfolio in just four months through three major transactions, raising approximately $23M USD while becoming cash flow positive and never issuing warrants.

- The company has three producing assets generating revenue: Madsen (1% NSR yielding ~500 oz gold annually), Orezone (50% silver stream producing 37.5k oz), and Zancudo (ramping up in Q3 2026).

- With only two full-time employees, the team has completed $2 billion in royalty deals over the past decade, with management and directors owning 15% of the company.

- Trading at 0.75-0.8x NAV with an ~$85M USD market cap, Summit represents significant value compared to peers, having appreciated from $0.90 to $1.60 per share in under four months.

- The company targets scaling to $10M annual revenue and $200-300M market cap through accretive acquisitions, with a strong deal pipeline and access to institutional capital from prominent mining investors.

youtu.be/T8cvi-I88b8

2

6

442

Feb 26

HL CANADIAN FIRST NATION SEEKS TO HAVE ITS SAY AS PART OF UPCOMING SALE OF HECLA QUÉBEC AND THE CASA BERARDI MINE TO OREZONE GOLD CORPORATION .

560

【Hecla Miningの決算から見る銀】

決算、凄まじい数字でしたね!

純利益9倍というパワーワードもさることながら、銀価格の高騰を完璧に利益へ変えた運営力は、まさに「銀の盟主」としての貫禄を感じます。

さらに踏み込んだ

3つの追加情報を整理しました💡

1️⃣「銀への特化」を加速させるCasa Berardiの売却

今回の発表で最も重要な戦略的動きは、ケベック州のCasa Berardi金鉱山の売却です。

狙い: 金から「純粋な銀生産者」へのシフト。売却完了後、売上の約73%が銀に由来することになり、銀価格上昇の恩恵をよりダイレクトに受ける体質になります。

🐬現金確保

現金と約1.12億ドル相当のOrezone社株式を受け取ります。これにより、さらなる債務削減や、銀鉱山への再投資が可能になります。

2️⃣銀価格の強気設定と利益率の改善

決算説明会では、驚きの数字がいくつか共有されました。

実現価格: 2025年第4四半期の銀の実現価格は、なんと1オンスあたり約70ドルに迫る水準でした。

COMEX(紙の銀市場)ではなく上海(実物市場)や実需業者に直接卸している可能性があります。

🐬コスト構造: 銀のAISC(全維持コスト)は、2026年のガイダンスで15.00ドル〜16.25ドルと予測されています。現在の現物価格(50ドル〜80ドル付近を推移)を考えると、利益率(マージン)は驚異的なレベルで維持される見込みです。

簡単に言うと70ドルー15ドルが利益と言うことです。

3️⃣2026年は探査の爆発年度

生産ガイダンスは2025年比で少し保守的ですが、その分「未来への投資」が凄まじいです。

•予算倍増: 2026年の探査・事前開発予算を2025年の約2倍に増額。

• ターゲット: 特にネバダ州(Midas、Hollisterなど)での予算を3倍に増やし、新たな高品位銀の発見を狙っています。また、絶好調のLucky Friday鉱山では2026年半ばに冷却プロジェクトが完了し、今後10年以上続く「黄金期(銀ですが)」の基盤が整います。

🐬個人的な考察

Heclaは、単に「銀が高かったから儲かった」だけでなく、負債を減らし、現金を8倍に増やした」という、盤石な財務基盤を作り上げた点が最大の評価ポイントです。

銀の需給逼迫が続く2026年において、この「身軽で銀特化」な体制は非常に強力と考えられます。

Feb 18

⚡️HECLA RELEASES 2025 RESULTS- NET INCOME UP A MIND NUMBING 9X YEAR OVER YEAR!⚡️

🔥Silver production totaled 17.0 million ounces

🔥Revenue Exceeded $1.4 BILLION

Hecla Mining Company (NYSE: HL) released its Q4 and full-year 2025 earnings results today, marking a standout year for the leading U.S. silver producer.

For the full year 2025, Hecla achieved record performance across key metrics:

Revenue exceeded $1.4 billion, up 53% from 2024.

Net income applicable to common stockholders reached $321.2 million ($0.49 per share), a nine-fold increase year-over-year.

Adjusted EBITDA hit a record $670 million, nearly double the prior year.

Silver production totaled 17.0 million ounces (at the high end of guidance), with gold at 151,000 ounces (also exceeding targets).

The company generated strong cash flows, reduced total debt by 50% to $276 million, slashed net debt to $34 million, and ended with $242 million in cash and a net leverage ratio of just 0.1x.

All operations were free cash flow positive, with record output at Lucky Friday (5.3M oz silver) and Keno Hill's first profitable year under Hecla ownership.

In Q4 2025, results remained robust amid higher metal prices:Revenue surged to $448.1 million (up significantly YoY and beating estimates).

Net income applicable to common stockholders was $134.3 million ($0.20 per share), with adjusted figures also topping expectations.

The quarter benefited from strong contributions across mines, including Greens Creek and Lucky Friday.

Hecla declared a quarterly cash dividend of $0.00375 per common share (payable March 24, 2026) and $0.875 per Series B preferred share.

Looking ahead, the company is positioning as North America's premier silver producer following the pending sale of its Casa Berardi gold mine (up to $593 million, expected close in Q1 2026).

2026 silver production guidance is set at 15.1-16.5 million ounces, with plans to nearly double exploration and pre-development spending to $55 million.

CEO commentary highlighted 2025 as "transformational," with strengthened operations, balance sheet, and focus on silver growth.

This release underscores Hecla's operational strength and strategic shift in a favorable precious metals environment.

#Silver #Mining #HeclaMining #Earnings

2

29

2,431

Feb 17

As you may of heard, after 7 years with Orezone, I've flown the nest and moved onto @OnyxGoldCorp!

I can't thank the $ORE.TO team enough for all they taught me, but it's time to get back to my exploration roots!

5

23

2,047

Jan 29

Josh- huge thanks for posting your position in Orezone gold this summer. I bought it when I saw one of your screenshots :) I'm up 120% and still holding. What a gem....it's still making moves and flying under the radar. Genius find

8

2

162

Hecla Mining Company (NYSE:HL) has agreed to sell its Casa Berardi #gold operation in Québec to Orezone Gold (TSX:ORE,OTCQX:ORZCF) for total consideration of up to US$593 million. #GoldMining #GoldInvesting investingnews.com/hecla-sell…

2

191

Une mine d’or québécoise vendue pour plus de 800 M$

Le géant américain Franco-Nevada, cofondé par le Québécois d’origine Pierre Lassonde, aidera Orezone à financer la transaction par le biais d’un flux aurifère de 100 M$ US journaldequebec.com/2026/01/…

2

77