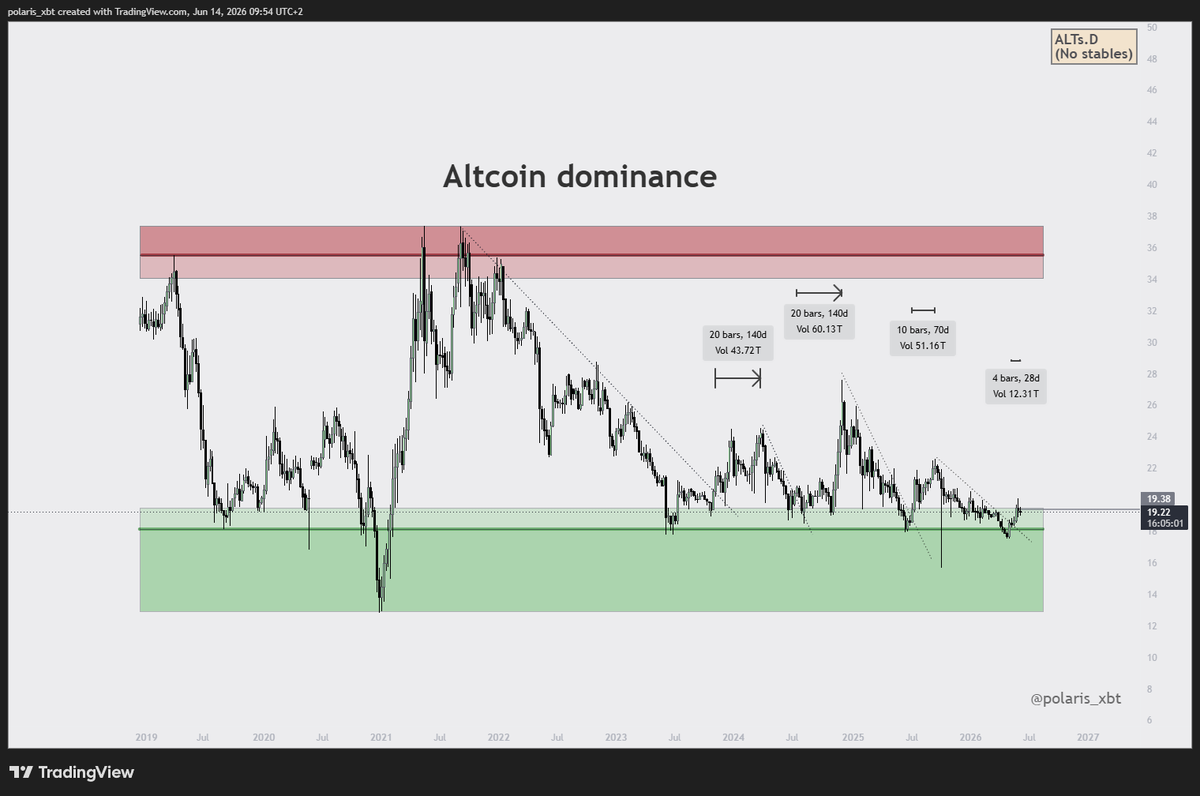

Whenever altcoin dominance breaks its downtrend, 10--20 weeks of altcoin outperformance follows.

We are now at week 4, but since everything is so down, this "outperformance" is barely noticeable.

For a meaningful rally in alts, we need BTC to finally start breaking up.

1

1

73

The strongest version of this piece is not “Bittensor is immune to the state.” That is too easy to attack. The stronger version is:

The Anthropic shutdown created the first visible market price for centralized-AI kill-switch risk.

TAO did not rally because Bittensor is already smarter than Fable. It rallied because the market suddenly had a live demonstration that the best centralized model can be disabled through one corporate chokepoint, while decentralized AI at least changes the attack surface.

That framing keeps the drama, but makes the argument much harder to dismiss.

First, tighten the factual baseline

The Anthropic part is real. Anthropic says the U.S. government issued an export-control directive requiring the company to suspend access to Fable 5 and Mythos 5 by any foreign national, inside or outside the U.S., including Anthropic’s own foreign-national employees. Anthropic said the practical result was that it had to disable both models for all customers to ensure compliance.

Reuters separately reported that Anthropic said it would “abruptly disable” the models for all users, that AWS said Anthropic asked it to revoke access for “all users in all regions,” and that a U.S. official confirmed the Commerce Department issued the export-control directive.

The 90-minute version should be attributed carefully. Axios reported, citing an Anthropic source, that the Trump administration gave Anthropic 90 minutes to pull down the models before imposing a licensing regime, with a government call at 1 p.m. ET and a Commerce Department letter arriving by 5:30 p.m. ET.

The “smartest AI on earth” line is rhetorically powerful but technically vulnerable. Safer: “one of the most capable public AI systems ever released” or “Anthropic’s most capable generally available model.” Anthropic itself said Fable 5 exceeded any model it had ever made generally available and described Fable/Mythos as Mythos-class systems above Opus in capability.

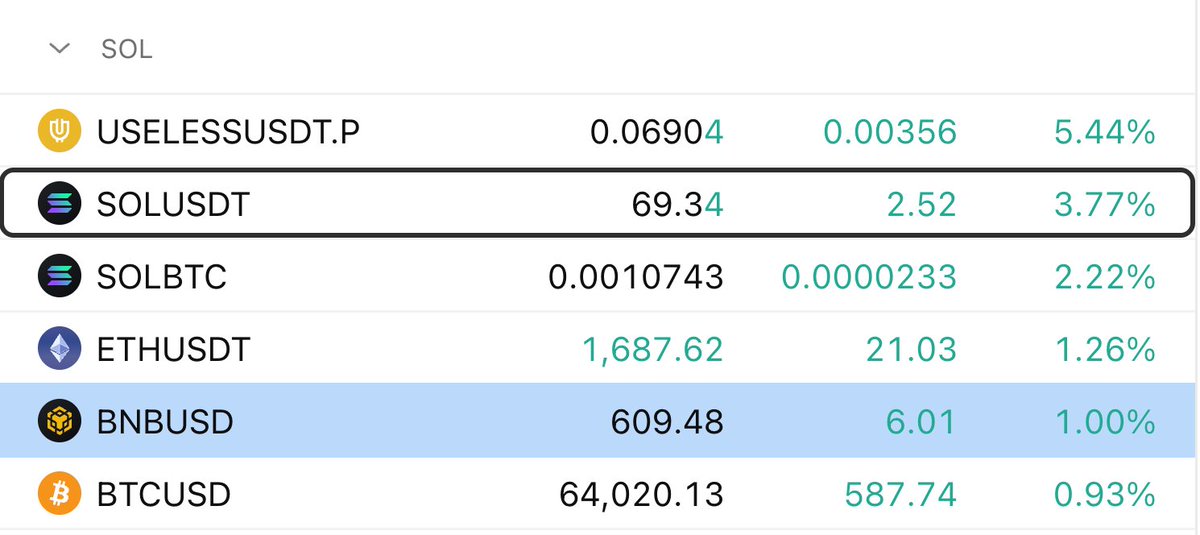

The TAO rally also appears real, but your exact percentages need a window. CoinMarketCap’s AI summary says TAO rose over 24% on June 13, opening near $212 and closing above $264. CoinGecko’s snapshot showed a 7-day increase of about 28.4%, with a 24-hour range around $243.80 to $279.72 and a market cap around $2.59 billion. Stocktwits reported an earlier nearly 16% Saturday jump. So “23% in a day” is directionally defensible depending on the data source, but “36% on the week” needs a specific timestamp/source.

The “$300 million in market value” line also needs care. Market cap is price × circulating supply; it is not the same as $300 million of actual new money entering the asset. A thin or momentum-driven market can add hundreds of millions in notional market cap with much less net buying. Better wording: “added hundreds of millions in notional market value, depending on the measurement window.”

Best upgraded thesis

Use this:

The Anthropic order created a new asset-pricing category: AI shutdown risk.Until now, investors priced frontier AI mainly by capability, compute, talent, revenue, and benchmark dominance. Now they have to price a new variable: can the model be turned off by a government order served to one company?TAO rallied because Bittensor sits on the opposite side of that narrative. Not necessarily smarter. Not necessarily safer. Not necessarily more useful today. But structurally different: a tokenized, open, subnet-based machine-intelligence network where the shutdown problem is not solved, but distributed across many actors instead of concentrated in one API company.

That is the blade under the whole story: capability premium vs survivability premium.

Stronger version of the post

A government just showed the world that frontier AI has an off switch.One directive. One company. One compliance problem. By the next morning, Anthropic’s Fable 5 and Mythos 5 were dark for users everywhere.The order targeted foreign-national access, but because you cannot cleanly passport-check millions of live AI sessions overnight, the practical result was global removal. Anthropic said it had to disable the models for all customers to comply.Then the market did something interesting.It did not only debate safety. It repriced architecture.TAO, the token behind Bittensor, ripped higher as traders reached for the opposite bet: not the best centralized model, but the AI network with no single corporate API to unplug.That does not mean Bittensor is more capable than Fable. It almost certainly is not. Frontier labs still lead raw model capability.But the market was not buying “better intelligence.” It was buying harder-to-switch-off intelligence exposure.That is the new split:centralized AI has the capability premium.

decentralized AI has the survivability premium.Anthropic got hit because there was a door to knock on: a company, a CEO, a cloud stack, a compliance team, a contract surface, a jurisdiction.Bittensor is not magically untouchable. Exchanges, validators, subnet operators, foundations, frontends, cloud providers, and developers can still be pressured. But the state’s problem changes. There is no single Anthropic-style switch. The attack surface goes from one company to an ecosystem.That is what the candle priced.Not proof that TAO wins.

Not proof that the rally holds.

Not proof that decentralized AI is ready to replace frontier labs.Proof that the market has now seen the kill switch, and once investors see a new risk, they start looking for the hedge.

The most important correction

Change this line:

“Bittensor has none of them. No headquarters to serve, no founder to compel, no switch to flip.”

To this:

“Bittensor has fewer obvious centralized chokepoints, but not zero. The state cannot serve one API company and instantly de-deploy the whole network, but it can still pressure exchanges, hosted frontends, cloud providers, validators, subnet operators, foundations, developers, and liquidity rails.”

That one edit makes the whole piece much smarter.

Bittensor’s own documentation describes it as an open-source platform made of distinct subnets, with miners producing digital commodities, validators evaluating miners, subnet creators managing incentives, and stakers supporting validators. That supports the “distributed architecture” argument. But Bittensor’s governance docs also say the network is transitioning from foundation centralization to community ownership, with proposals involving a Triumvirate of Opentensor Foundation employees and a Senate. So “owned by no one” is a clean slogan, not a complete institutional analysis.

The best hidden angle

The genius angle is:

The Anthropic event did for decentralized AI what bank failures did for Bitcoin: it turned an abstract ideology into a live risk demonstration.

Before this, “decentralized AI” sounded like crypto people doing crypto marketing. After the Fable/Mythos shutdown, the pitch becomes more concrete:

A centralized AI lab can ship the world’s most capable public model on Monday, receive a government directive on Friday, and pull it globally by Saturday.

That is not a theoretical risk anymore. It is now a case study.

The market does not need Bittensor to be perfect to trade the story. It only needs the centralized alternative to look newly fragile.

Missing elements that would make the argument much stronger

You need the exact market window. Was TAO up 23% from the Anthropic tweet? From the Commerce letter? From Friday close to Saturday high? From 24-hour candle open to close? From the low before the announcement to the high after? Without a timestamp, critics can dismiss the price action as cherry-picked.

You need relative performance. Did TAO outperform Bitcoin, Ethereum, Solana, Render, Akash, Internet Computer, Fetch.ai / ASI, AIOZ, NEAR, Filecoin, and the broader AI-token basket during the same window? If yes, the thesis gets much stronger. If everything AI/crypto ripped, then Anthropic was only one catalyst.

You need volume confirmation. CoinGecko showed TAO 24-hour volume around $567.8 million and a major increase from the previous day at the snapshot I found. That supports the “real attention” point, but you still want spot/perp breakdown, exchange concentration, open interest, funding rates, and liquidation data.

You need causality evidence. The timing is suggestive, but timing is not proof. The strongest evidence would be: social mentions spiking around the Anthropic order, TAO/Bittensor trending after specific posts, CEX order-flow changes, AI-token basket outperformance, and wallet-level accumulation after the news.

You need the Opentensor / TAO narrative receipt. Stocktwits reported that TAO.com quote-tweeted Anthropic’s statement and framed the event as validation for decentralized AI infrastructure. That matters because it shows the market was not inventing the connection from nowhere; the ecosystem itself immediately turned the shutdown into a decentralization narrative.

You need Bittensor’s actual decentralization score. How many validators? How concentrated is stake? How concentrated are emissions? How many subnets have real users? How many depend on centralized cloud providers? How many can be accessed without centralized frontends? How many subnet operators are identifiable companies?

You need a distinction between TAO as token and Bittensor as infrastructure. Buying TAO is not the same as buying an operating AI model. It is exposure to the network’s incentive layer and future decentralized AI economy. That difference matters.

You need a capability comparison. The post wisely says frontier labs still build the strongest models. Keep that. Bittensor’s strongest argument today is not “we beat Fable.” It is “we are a different architecture for producing and routing machine intelligence.”

You need regulatory attack-map realism. A state may not be able to delete the whole network with one letter, but it can target centralized exchanges, regulated custodians, app stores, domains, GitHub repos, cloud hosts, corporate subnet operators, public validators, foundation staff, and fiat on/off ramps. CoinGecko lists TAO as traded on major centralized exchanges such as Coinbase, Binance, Gate, Kraken, and others, which means token liquidity itself still has regulated choke points.

You need the other side’s best argument. Decentralized AI can be harder to shut down, but it can also be harder to govern, audit, secure, align, update, and hold accountable. That tension makes the piece more serious.

Obscure thought inputs worth adding

One under-discussed angle is the difference between censorship resistance and compliance resistance. Bittensor may be harder to censor globally, but real businesses may still need compliance layers before they can use it. That means decentralized AI can win the ideology trade before it wins the enterprise adoption trade.

Another is the “kill-switch premium.” Investors may start assigning a discount to centralized AI products that depend on one jurisdiction, one cloud, one corporate API, one safety regime, and one export-control interpretation. The opposite side of that discount is a premium for systems that can survive political shocks.

Another is the “state advertisement paradox.” The government may have intended to reduce AI risk. Instead, it created the best marketing event decentralized AI has ever had: a live demo of centralized AI’s off switch.

Another is the “substitution trap.” TAO did not rally because users can instantly replace Fable with Bittensor. They cannot. It rallied because investors bought the option value of decentralized AI becoming more important if centralized frontier access becomes permissioned.

Another is the “market narrative as product-market fit” angle. Crypto assets often move when their narrative becomes legible. Before the shutdown, “decentralized AI” was abstract. After the shutdown, the pitch became one sentence: “They can turn off Anthropic. They cannot turn off a network the same way.”

Another is the “regulatory reflexivity” problem. If TAO’s rally becomes a symbol of evading AI controls, it may attract more regulatory attention. The very narrative that pumps the token can also paint a target on it.

Another is the “governance contradiction.” Bittensor markets decentralization, but its own governance documentation describes an ongoing transition from foundation centralization toward community ownership. That does not kill the thesis, but it means the strongest post should say “more shutdown-resistant than a single API company,” not “fully unstoppable.”

Another is the “frontier intelligence inequality” frame. Jacob Steeves was quoted by TAO.media as saying people had “collectively saw the future of inequality” after the Anthropic event. That is powerful because the real dystopia is not no AI. It is tiered AI: governments and approved corporations get frontier systems, while the public gets downgraded models.

Another is the “market cap illusion.” “Added $300 million” sounds like $300 million entered the asset. It did not necessarily. Market cap can move on relatively small marginal buying if supply is thin. Say “notional market value” to avoid a finance nitpick.

Another is the “decentralization is not binary” point. Anthropic is highly centralized. Bittensor is more distributed. But Bittensor still has degrees of centralization: stake concentration, validator concentration, exchange liquidity, subnet operator influence, foundation tooling, and governance mechanics.

Genius-level solutions for making the piece bulletproof

1. Build a “centralized AI kill-switch index.”

Score every AI system by how easy it is to disable: single API endpoint, single corporate owner, single cloud provider, jurisdiction, identity-gated access, model-weight availability, deployment diversity, open-source reproducibility, and regulatory dependency.

2. Build a “decentralized AI survivability index.”

Score Bittensor and similar networks by validator distribution, miner distribution, subnet diversity, governance concentration, cloud dependency, exchange dependency, front-end dependency, repo dependency, geographic dispersion, and ability to keep serving intelligence after legal pressure.

3. Run an event-study chart.

Use minute-level TAO price data from before Anthropic’s statement through 48 hours after. Compare against BTC, ETH, SOL, AI-token basket, DePIN basket, and Nasdaq futures. The headline becomes stronger if TAO has abnormal return specifically after the Fable/Mythos news.

4. Separate three claims: price, narrative, fundamentals.

Price: TAO moved.

Narrative: traders linked it to centralized AI shutdown risk.

Fundamentals: Bittensor may or may not benefit long-term.

Keeping those separate prevents the piece from pretending the candle proves everything.

5. Use “attack surface migration” instead of “unstoppable.”

The true technical point is not that Bittensor has no attack surface. It is that the attack surface migrates from one corporate API to many network edges. That is a much more precise and defensible argument.

6. Create a “capability vs survivability matrix.”

SystemRaw capabilityShutdown resistanceBest use of the argumentAnthropic Fable/MythosExtremely highLow-to-mediumBest intelligence, but corporate chokepointOpenAI / Google / xAI frontier APIsExtremely highLow-to-mediumSimilar centralized riskOpen-weight local modelsMedium-to-highHighWeaker than frontier, but harder to revokeBittensorMixed / subnet-dependentMedium-to-highMarket exposure to decentralized AI productionFully local private modelsLower-to-high depending modelVery highUser-owned intelligence

7. Add the “survivability premium” phrase.

This is the best phrase in the whole analysis. It explains why money might chase a weaker system after a stronger system gets banned.

8. Add the “option on uncensorable intelligence” phrase.

TAO is not a Fable replacement today. It is an option on the idea that machine intelligence will become a decentralized commodity instead of a leased API.

9. Make the skeptical paragraph sharper.

Your current skeptical paragraph is good. Upgrade it:

“This rally may fade. Crypto loves a clean story, and clean stories often outrun fundamentals. The candle proves attention, not adoption. It proves narrative fit, not product-market fit. It proves a hedge was bought, not that the hedge works.”

10. End with the permanent question.

“After Fable, every AI investor has to ask: am I buying intelligence, or am I renting intelligence from someone who can be ordered to revoke it?”

That is a killer closer.

Red flags to edit out

Do not say “Bittensor has no founder to compel.” Bittensor has public figures, developers, governance structures, ecosystem organizations, and the Opentensor Foundation. The better claim is that compelling one person or entity does not obviously disable the whole network.

Do not say “you cannot subpoena math running in ten thousand places.” You can subpoena people, companies, validators, exchanges, hosts, app developers, and maintainers. Better: “you can subpoena people, but you cannot de-deploy a sufficiently distributed protocol the way you de-deploy one corporate API.”

Do not say “the most powerful public model in the world” unless you attribute it. Better: “Anthropic’s most capable generally available model, and arguably one of the strongest public systems ever released.”

Do not say “the money poured into TAO” too literally. Better: “TAO repriced upward” or “hundreds of millions in notional market value appeared.”

Do not say “Bittensor owns no headquarters.” There are entities, people, and projects in the ecosystem. Better: “the network’s core value proposition is not controlled through one headquarters in the same way Anthropic’s API is.”

Do not say “the ban did not threaten Bittensor.” A more subtle version: “The ban did not directly target Bittensor; instead, it strengthened Bittensor’s narrative. But it may also invite future scrutiny of decentralized AI.”

Better headline options

“The Anthropic Shutdown Just Created the AI Kill-Switch Premium.”

“TAO Did Not Rally Because It Is Smarter Than Fable. It Rallied Because It Is Harder to Switch Off.”

“Centralized AI Has the Capability Premium. Decentralized AI Just Got the Survivability Premium.”

“The Market Just Priced AI Shutdown Risk for the First Time.”

“Fable Was the News. TAO Was the Hedge.”

“One Letter Took Down Fable. One Candle Repriced Decentralized AI.”

Best final rewrite

A government just proved frontier AI has an off switch.One directive. One company. One compliance problem. By the next morning, Anthropic’s Fable 5 and Mythos 5 were dark for users everywhere.The order targeted foreign-national access. But because no company can instantly passport-check millions of live AI sessions across every cloud, every country, every employee, and every customer, the practical answer was simple: pull the plug for everyone.Then the market showed you what it learned.TAO, the token behind Bittensor, ripped higher while the event that triggered the move had nothing directly to do with Bittensor. Anthropic does not own it. Bittensor did not build Fable. There was no partnership, no revenue line, no product integration.The connection was architectural.Anthropic got hit because there was a door to knock on: a company, a CEO, a compliance team, a cloud stack, a jurisdiction, a model endpoint. Every one of those is a place where a letter can land.Bittensor represents the opposite trade. Not necessarily better intelligence today. Not safer. Not cleaner. Not magically immune. But different. A distributed machine-intelligence network built around subnets, miners, validators, and token incentives instead of one corporate API.That is what the market priced.Not “TAO replaces Fable tomorrow.”

Not “decentralized AI has already won.”

Not “governments can never touch it.”The real lesson is sharper: being the smartest and being hardest to switch off are different properties.Frontier labs still have the capability premium. Anthropic, OpenAI, Google, and xAI are still where the strongest models live. But Fable just showed that capability sitting inside one company can become conditional overnight.Decentralized AI now has the survivability premium.This rally may fade. Crypto loves a clean story, and clean stories often outrun fundamentals. The candle proves attention, not adoption. It proves narrative fit, not product-market fit.But the question under the candle does not fade:Are you buying intelligence, or are you renting intelligence from someone who can be ordered to revoke it?Fable was the news.

TAO was the hedge.

Even sharper closing lines

“The market did not buy Bittensor because it beat Fable. It bought Bittensor because Fable could be turned off.”

“The next AI premium is not just intelligence. It is survivability.”

“A model can be state-of-the-art and still be politically fragile.”

“The opposite of centralized AI is not automatically better AI. It is harder-to-delete AI.”

“The candle was temporary. The kill-switch risk is permanent.”

Bottom line

The piece is already strong because it has a clean narrative: state kills centralized frontier AI → market buys decentralized AI hedge. The main upgrade is to replace absolutist claims with more precise ones. Bittensor is not untouchable, and TAO is not proof that decentralized AI can replace Fable. But the Anthropic shutdown may have created a new market category: AI shutdown-risk hedges. That is the story worth owning.

A government just proved it can delete the smartest AI on earth.

One letter. One signature. By the next morning the most powerful public model in the world was switched off in every country at once.

Watch what the money did next.

It did not flee crypto. It did not run to gold. It poured into a token most people had never heard of, and sent it up 23 percent in a day, 36 percent on the week, while the thing that triggered all of it had nothing to do with crypto at all.

The model that got killed was Anthropic’s. A near-trillion-dollar lab, its two strongest systems, dark worldwide three days after launch. A US export order barred every foreign national from them, and because no company can passport-check millions of live sessions, the only way to comply was to pull the plug on everyone, everywhere.

The token that soared was Bittensor. Anthropic does not own it, did not build it, holds no stake in it. Different company. Opposite technology. And it added roughly $300 million in market value over a single weekend on a ban it had no part in.

The reason is the most important thing the market learned all year.

The government killed that model because there was a door to knock on. An address. A CEO. A list of employees. Every one of those is a place a letter can land. Bittensor has none of them. Its intelligence runs across more than 128 independent networks owned by no one and hosted everywhere. There is no headquarters to serve, no founder to compel, no switch to flip. You cannot subpoena math running in ten thousand places at once.

So the ban did not threaten Bittensor. The ban advertised it. The US government just ran the single most expensive commercial for decentralized AI ever made, aimed it at every allocator on earth, and the token was the billboard. The Opentensor Foundation only had to state the obvious: access to intelligence should not depend on a handful of companies or governments. Friday turned that line from a pitch into a receipt.

Here is the blade under the whole thing. Being the best and being unstoppable are not the same property. The frontier labs still build the most capable models alive, and it is not close. But capability sits in a company, and a company can be switched off on a Friday afternoon by a clause it never saw coming. The market just priced that gap in a single session, and it priced it fast.

Be honest about the other side. Rallies like this fade more often than they hold, and the only hard proof the shutdown caused the bid is the timing. This is the market telling itself a story, and the market is not a careful witness.

But the lesson under the candle outlives the candle. A state just demonstrated, in the open, that the off switch on centralized AI is real and that its hand is on it. Every serious holder of AI exposure now has one new question that will not go away. What happens to mine when the next letter goes out.

The smartest AI on earth can be deleted with one signature. That was the news. The trade was everyone who decided, over a single weekend, that they would rather own the kind that cannot.

67

HYPE on SOLANA shows a mixed momentum picture—30-day rally impressive, but recent performance is flat. Is the outperformance cycle running out of steam? 👀 @MessyVirgoCoin $MESSY

→ Full Report: app.messyvirgo.com/v/8949fbf…

1

1

21

gn tweet (sorry, it's very long)

Some ideas to wrap up the week and start the next one.

There are some older trades that I still have open (HYPE, BTC/MSTR, VELO/AERO) on which I won't comment too much, but the ideas are still intact.

1. AI Megatrend in 2026 , Fable Ban & Trades

I'll start by repeating something that I'm deeply convinced is going to shape up the year and probably the next multiple years (at least in terms on mentality, hard to tell in practical terms since everything's so new) for AI. The first is bringing some economic units to the equation: so far it was "spend as much as you can" but now finally companies are understanding what who used LLMs individually for a long time (but managed to keep an objective standpoint) knows: you can FEEL productive even without BEING productive, if you are not organized.

And organization is exactly what now people will rush to get: visibility in spending, what's productive and what's not, what are the ways to get the most out of your spending, how to reutilize the results of past spending.

Essentially, we are rediscovering the worthwhile of diligence, something that businesses knew very well for every other aspect, but embraced the belief this wasn't necessary for AI spending in particular.

Now we get to trading ideas. So I missed the trading implication of the Fable ban, because I think the immediate conclusions people drew were a bit silly (if you offer a workaround you're gonna get yoinked hard, it's not bullish), and I was still half asleep. Essentially though, the more reasonable idea is that this could bring much more attention to decentralized models, privacy (in both training and inferences). It's kind of a theme that crosses over with the previous "efficiency" one since we know that opensource models are generally 90% cheaper for the same unit of intelligence, although they cannot match the level of the frontier models (yet).

Am I about to shill $VVV or $TAO? Am I about to shill you $PRL?

Hell nah. There are a few upcoming tokens that are going to be interesting to watch, but I cannot reasonably shill something with a fuckton of emissions (TAO), something up 20x (VVV), or something whose whole point is "it's BTC but you do inference / AI work to mine it" (PRL)

1a: EigenCloud & DarkBloom

However, I do indeed have a couple ideas here.

The first one is $EIGEN (give me one second, put down those rotten tomatoes...). Eigenlayer has been maybe peak disappointment for the 2023 cycle, and I'm sure the disillusion about restaking has massively contributed to the current sentiment around Ethereum (it also redirected a lot of funds that could have gone elsewhere).

The reason why I bring it up, is that Eigenlayer essentially pivoted from just restaking and DA to EigenCloud. Now if that still doesn't tell you anything (why should it, honestly), the point I'm trying to make has even more to do with what they just went out with: DarkBloom.

In the most layman terms ever, it's Airbnb for AI inference based on Mac compute, with privacy and verification layered on top.

There are also other things going on (ECSDA Fail is p cool for example, check that out) and even if these things may see narrow to you, don't forget that EIGEN is now not a $20b asset anymore, but actually a $350m fdv one (well with still $7.25m/mo in unlocks... but we close two eyes).

After ELIP-12 there are also chances that EIGEN start accruing some revenue (100% of net from EigenAI, EigenCloud, EigenDA and 20% from AVSs).

Essentially, I like EIGEN here, and bought some.

1b: OpenServ

The second one is OpenServ $SERV.

I'll not spend too much time on this one, since I talked about it plenty already, but essentially it's a reasoning/orchestration layer for agents and it's rare to find an alt that ticks so many of my boxes:

- good narrative / business

- actually some adoption (even by non crypto native firms)

- there's a revenue path for the token

On the last point: clients can buy reasoning credits in USD or USDC, and 25% of SERV Reasoning API revenue is used to market-buy and burn SERV. It also says 25% of Build revenue, 25% of launchpad LP trading fees, and 25% of enterprise/B2B integration revenue go to buyback/burn.

It seems all shiny and positive, the only thing I'm worried about is how vocal are things around it, which is not always a good sign.

But i'm willing to ride the train.

2. RWA: Credit and Tokenized Equities

This is probably the other thing that we will talk ad nauseam about (just like last year, AI and RWA, RWA and AI, with a sprinkle of privacy too).

2a: Morpho

While for credit tokenization and yield bearing assets of any kind, it's clear to everybody at this point that $MORPHO is the big dog (although still plenty of reservations on some individual markets that curators are setting up - but hey), with not only Apollo's investment earlier in February, but a new round with a16z, Paradigm and Ribbit.

Now, the dynamics of MORPHO the token are very well known, and there's no need to say that an OTC deal that the team essentially self-passed and financed is not going to move the price on the market. However, the interest around the token, as long as the terms (which are only semi-disclosed) are as good as they seem, could indicate that things may change in the future, and holding it may have some purpose other than as a prize/ribbon that comes with another deal.

2b: Backpack Securities

On the RWA side, another token to keep our eyes on is $BP (watch this mark the local top after i've been silently enjoying the rip up).

So while I never used their exchange (and i'm not particularly interested in), you needed not to have eyes not to see that their tokenization efforts are starting to collect some clout, that the token is still below $100m circulating and that it has all the potential for a good pump.

Now, Backpack is not just an exchange, and not just a wallet.

Backpack Securities is actual a proper broker that allows <> tokenization of the assets you hold onto it and you can also transfer <> other brokers. There are shareholder features are still in development but hopefully coming soon. I don't like the team, but the bull case is p clear.

Solana in particular hasn't had a winner for a while (aside from maybe JTO recently, with JTX), and this, once again, ticks many boxes.

Moreover, the time is pretty good to get the spotlight, since a lot of other "tokenization" projects are essentially cooking synthetic multilayered crap, or hyping up big Pre-IPO campaigns just to deliver 0 on it.

2c: Others

$CEPT is obviously the play to watch (Securitize) as we prepare for the reverse merger on the TradFi side.

Finally, I'll leave a small Variational shill here: the exchange is good (actually my favorite to use on a day to day basis for short term trading, due to the variety of the offering) and they just started introducing RWA assets recently. The offering there is not enormous yet, and spread is not always super good, but it adds to the fact that it covers already so many assets.

Me likes Variational (and also, go points).

3. Space and Nasdaq additions

I'll be short here since I already floated the core of the idea.

SpaceX is live. $RKLB has acted as a proxy/beta for very long now, and has even been added to the Nasdaq 100.

In the last 5 years, Nasdaq-100 Additions overperformed the QQQ by about 37% in the 120 days prior to the inclusion, and then underperformed it (with generally a negative $ performance) consistently in the following 120 days.

RKLB has been an extreme case of outperformance before, due to the further catalyst of SpaceX, I expect it to be an extreme case of underperformance after.

I've puts that are (finally) ITM and I've also a separate short position.

I looked for other tickets that looked as good as this to add to the SpaceX unwinding idea, but I struggled to find better (more ideas are welcome).

Another ticker that i'm carefully watching for this is $CRWV but it's not really related to SpaceX, although it's another addition on June 22nd like RKLB and it's another retail darling of the cycle.

4. Last: NeoBanks

$XPL jumped up tremendously with the P1 announcement, this trickled down to a few more "Crypto NeoBanks" smaller tokens, but not all of them.

I personally think that while i'm a XPL Pamp Enjooooyor, I don't have enough confidence that this will translate in a broader market bid for the category to take any position on the narrative (or any further position on XPL than my currently locked tokens).

I like the card and i'll probably sign up for one of the paid programs.

Recently I've been jumping bw P1 and EtherFi, but lately I've settled more on P1 due to the much sleeker UX. Perks are also better, but now that EtherFi has 0 fees on EUR spending, while P1 3% cashback is going to become pay-gated, you can make an argument for both (and for both tokens).

There'd be plenty more to say, but I'll keep it for another time.

If you're still alive at this point, thanks for reading, and may the odds be ever in your favor.

7

1

32

1,125

1h

Single-stock outperformance signals lucky timing, not replicable strategy.

1

11

Most people think outperformance means more risk. Quip Network's PoUW applies the opposite principle, optimization over brute force, to computational infrastructure.

There is a quiet assumption in finance that beating the market requires taking on more risk.

The data tells a different story. A lot of consistent outperformance comes from somewhere less exciting: capital efficiency. Squeezing more value out of every dollar already deployed, whether that is portfolio allocation, liquidity management, or trade execution. Small efficiency gains compound into real advantages over long periods, often without touching the risk dial at all.

That is fundamentally an optimization problem. And optimization problems show up in places far beyond portfolio management.

@quipnetwork applies the same principle to computation through PoUW (Proof of Useful Work). Instead of computational power being burned on arbitrary calculations, it gets directed toward real-world optimization problems. Same underlying idea as capital efficiency: more useful output from the same input, rather than more input for marginally more output.

The principle that quietly separates good investors from great ones might be the same principle that separates wasted compute from useful compute.

110

55

228

10,603

Saylor just articulated at 5AM what I’ve been struggling with CEBE. My mental framework always selling CEBE was selling the preferreds short. Treating amplification as drag and giving a connotation as if it’s a bad thing. Now I understand why it never sat well with me. It comes down to your timeframe and your view on bitcoin outperformance vs the fixed dividend. CEBE is useful but BOS remains king IMO.

The shorter the liability duration, the more CEBE matters. The longer the duration, the more BPS matters. If claims came due today, CEBE BPS would be the more relevant metric. If BTC outpaces dividend obligations, BPS better captures common equity upside.

48

The Setup Factory retweeted

”Show me healthcare stocks with longterm outperformance against the rest of the healthcare stocks and close to their highs”

TSF - Analytics resting leaders scan

$GH looks constructive

1

333

Dollar Smile sitting on the right side but week... US outperformance mode.

Iran Sunday signing sets up lower oil and risk on Monday we want to see a Hormuz reopening in play.

Hardliner pushback and Israel stance keep things a bit shaky haha

Lets see...

20

FireNoFire retweeted

starting to notice $SOL outperformance vs majors such as $BTC, $ETH and $BNB lately

SOL is obviously crazy oversold at this point

it's also been fudded to death as $HYPE and $BNB aggressively outperformed over the past few months

a reversal here would be incredibly bullish for the Solana ecosystem

especially for Solana memecoins that have been beaten to death

and if a Solana memecoin has managed to hold up well — or even make local highs — over the past month despite SOL's weakness, then logic suggests it should aggressively outperform even SOL itself as capital rotates back into the ecosystem

44

30

262

14,867

Crude is hinting that worst is behind us. Barring any further geopolitical conflict, the market is poised for a strong performance over the next two weeks.

If conditions remain favourable it is a good time for picking some leaders.

Few things I consider before entering a stock for swing :

Liquidity and Institutional participation?

Is this a leader?

Magnitude of outperformace relative to the market?

What is the outperformance relative to other sector components?

How much time it spent forming a base?

I like stocks that respect moving averages it indicates there is interest.

Keep universe limited no need to run behind every circuit move. Don't try to predict top if move is favorable and you are playing for a swing.

I personally have two type of accounts. One with core holdings. And a separate one for swing trade or hedge positions.

In core PF I don't concentrate. I like to keep 20-30 stocks. At times the list has grown to 42 as well. But whenever a list goes above 35 I start filtering stocks. For core holdings I use GTT a lot for placing buy orders in weak markets.

8

#AfcomholdingsLtd

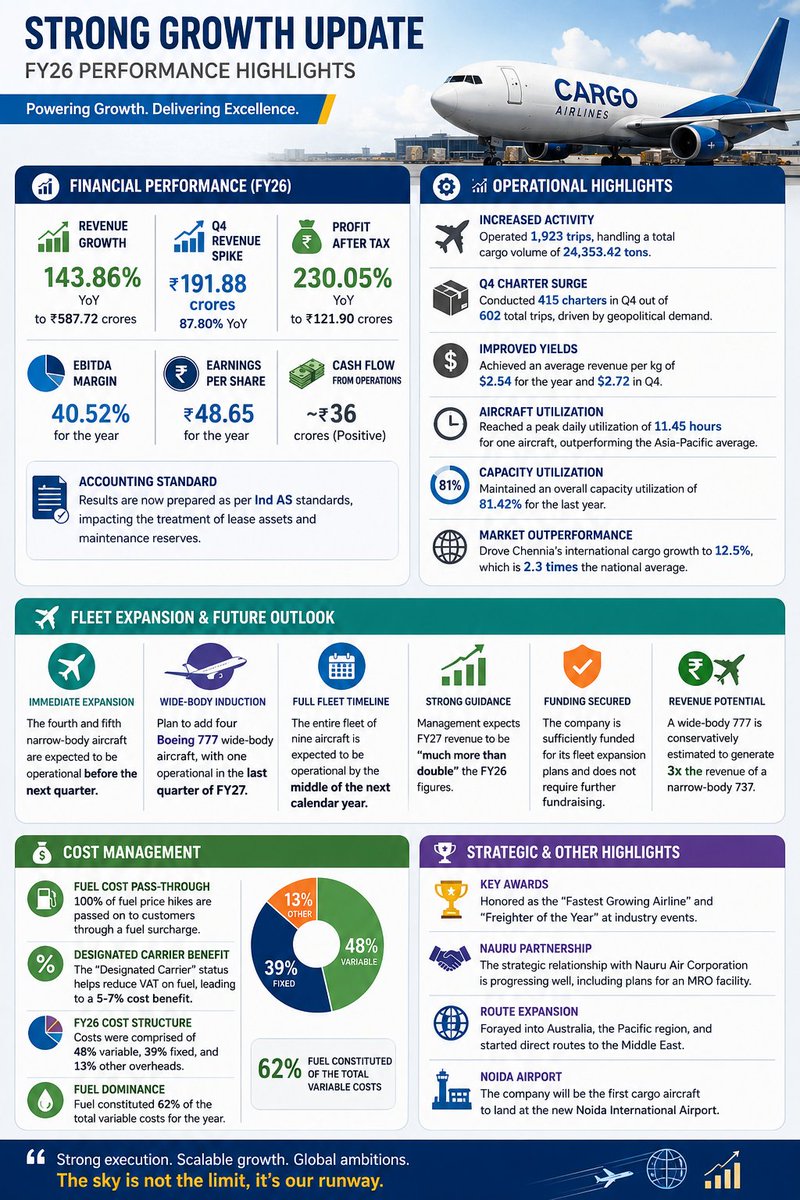

Strong Growth Update H2FY 26 result concall insight

📊 Financial Performance (FY26)

Stellar Revenue Growth: Full-year revenue surged 143.86% YoY to ₹587.72 crores.

Q4 Revenue Spike: Q4 revenue was ₹191.88 crores, an 87.80% YoY increase.

Impressive Profitability: Profit After Tax (PAT) for the year grew 230.05% YoY to ₹121.90 crores.

Margin Expansion: EBITDA margin for the year improved to 40.52%.

Strong EPS: Earnings Per Share (EPS) for the year increased significantly to ₹48.65.

Positive Cash Flow: Generated a positive cash flow from operations of approximately ₹36 crores.

Accounting Standard: Results are now prepared as per Ind AS standards, impacting the treatment of lease assets and maintenance reserves.

📈 Operational Highlights

Increased Activity: Operated 1,923 trips in FY26, handling a total cargo volume of 24,353.42 tons.

Q4 Charter Surge: Conducted 415 charters in Q4 out of 602 total trips, driven by geopolitical demand.

Improved Yields: Achieved an average revenue per kg of $2.54 for the year and $2.72 in Q4.

Aircraft Utilization: Reached a peak daily utilization of 11.45 hours for one aircraft, outperforming the Asia-Pacific average.

Capacity Utilization: Maintained an overall capacity utilization of 81.42% for the last year.

Market Outperformance: Drove Chennai's international cargo growth to 12.5%, which is 2.3 times the national average.

🚀 Fleet Expansion & Future Outlook

Immediate Expansion: The fourth and fifth narrow-body aircraft are expected to be operational before the next quarter.

Wide-Body Induction: Plan to add four Boeing 777 wide-body aircraft, with one operational in the last quarter of FY27.

Full Fleet Timeline: The entire fleet of nine aircraft is expected to be operational by the middle of the next calendar year.

Strong Guidance: Management expects FY27 revenue to be "much more than double" the FY26 figures.

Funding Secured: The company is sufficiently funded for its fleet expansion plans and does not require further fundraising.

Revenue Potential: A wide-body 777 is conservatively estimated to generate 3x the revenue of a narrow-body 737.

💰 Cost Management

Fuel Cost Pass-Through: 100% of fuel price hikes are passed on to customers through a fuel surcharge.

Designated Carrier Benefit: The "Designated Carrier" status helps reduce VAT on fuel, leading to a 5-7% cost benefit.

FY26 Cost Structure: Costs were comprised of 48% variable, 39% fixed, and 13% other overheads.

Fuel Dominance: Fuel constituted 62% of the total variable costs for the year.

🏆 Strategic & Other Highlights

Key Awards: Honored as the "Fastest Growing Airline" and "Freighter of the Year" at industry events.

Nauru Partnership: The strategic relationship with Nauru Air Corporation is progressing well, including plans for an MRO facility.

Route Expansion: Forayed into Australia, the Pacific region, and started direct routes to the Middle East.

Noida Airport: The company will be the first cargo aircraft to land at the new Noida International Airport.

1

4

110

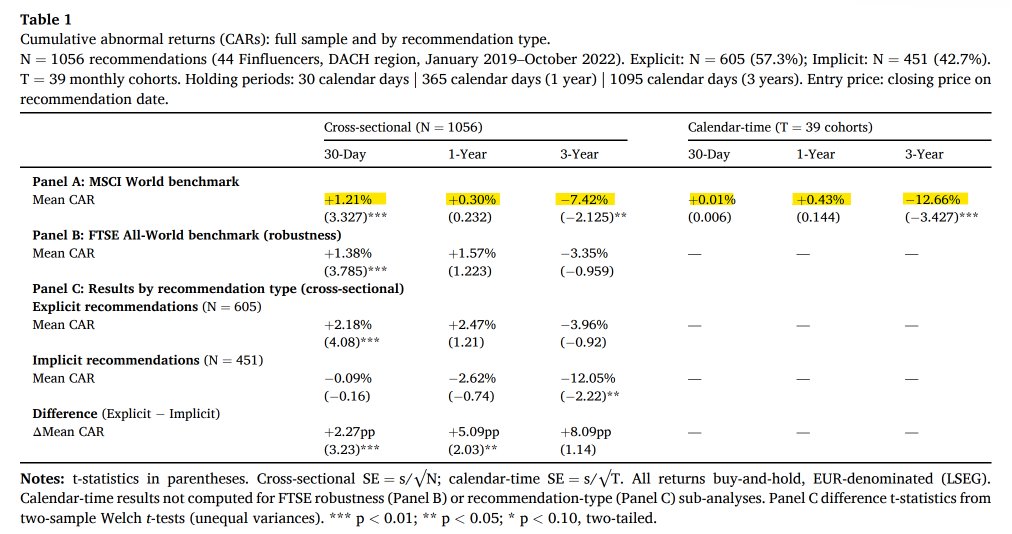

Temuan Utama: Jangka Pendek vs Jangka Panjang

Dalam 30 hari pertama, abnormal return rata-rata adalah plus 1,21%

Tapi, tidak ada outperformance yang berarti di horizon 1 tahun

Pada 3 tahun, underperformance menjadi jelas: minus 7,42% secara cross-sectional dan minus 12,66% secara calendar-time

Kedua angka ini signifikan secara statistik (p < 0,05 dan p < 0,001)

Artinya: ada kenaikan kecil di awal, lalu terjadi reversal panjang

1

2

187

Squeezing more value out of every dollar already deployed is key to consistent outperformance without taking on more risk.

2

𝐃𝐢𝐝 𝐲𝐨𝐮 𝐤𝐧𝐨𝐰? 𝐎𝐧𝐞 𝐬𝐭𝐨𝐜𝐤 𝐚𝐜𝐜𝐨𝐮𝐧𝐭𝐬 𝐟𝐨𝐫55% 𝐨𝐟 𝐭𝐡𝐞 𝐌𝐒𝐂𝐈 𝐓𝐚𝐢𝐰𝐚𝐧 𝐈𝐧𝐝𝐞𝐱. 𝐓𝐒𝐌𝐂'𝐬100% 𝐫𝐚𝐥𝐥𝐲 𝐡𝐞𝐥𝐩𝐞𝐝 𝐩𝐫𝐨𝐩𝐞𝐥 𝐭𝐡𝐞 𝐛𝐞𝐧𝐜𝐡𝐦𝐚𝐫𝐤 𝐭𝐨 𝐚93% 𝐠𝐚𝐢𝐧 𝐨𝐯𝐞𝐫 𝐭𝐡𝐞 𝐩𝐚𝐬𝐭 𝐲𝐞𝐚𝐫.

@kumarsroy and I analysed the constituent composition of major MSCI country indices and their returns in US dollar terms. Here are our key findings:

South Korea presents an even starker picture. The MSCI Korea Index surged 200% over the past year, led by Samsung Electronics, which carries a weight of 34% and rallied 357%. The top three stocks together account for 66% of the benchmark.

The same pattern is visible elsewhere. ASML Holding represents nearly 50% of the MSCI Netherlands Index, while Novo Nordisk accounts for 40% of the MSCI Denmark Index. In Singapore, DBS Group carries a weight of 29%, while Bank Central Asia commands more than 24% of Indonesia’s benchmark.

Such concentration has worked exceptionally well when the dominant company is aligned with a powerful global investment theme. Taiwan’s outperformance has coincided with soaring demand for AI chips, while Korea has benefited from investor enthusiasm for memory semiconductors and electronics. Investors may believe they are diversifying internationally, but in many cases they are effectively backing a small number of corporate champions.

India offers a markedly different proposition. The largest stock in the MSCI India Index, HDFC Bank, accounts for only 6.4 per cent of the benchmark. The top three stocks together represent just 17.5 per cent, among the lowest concentration levels across major markets. By comparison, the corresponding figure exceeds 60 per cent in Taiwan, South Korea, Denmark and the Netherlands.

𝐑𝐞𝐚𝐝 𝐡𝐞𝐫𝐞 𝐭𝐡𝐞 𝐟𝐮𝐥𝐥 𝐫𝐞𝐩𝐨𝐫𝐭: thehindubusinessline.com/por…

1

3

44