Marcos Gallo A. retweeted

👉 f.mtr.cool/yiywdqezji || Cinco de los seis procesados recibieron prisión preventiva, en Quito. 👇👇👇

10

33

1,201

May 16

I have a dream...

Apyx will own $1 Billion of $STRC.

Comparison of big entities holding $STRC:

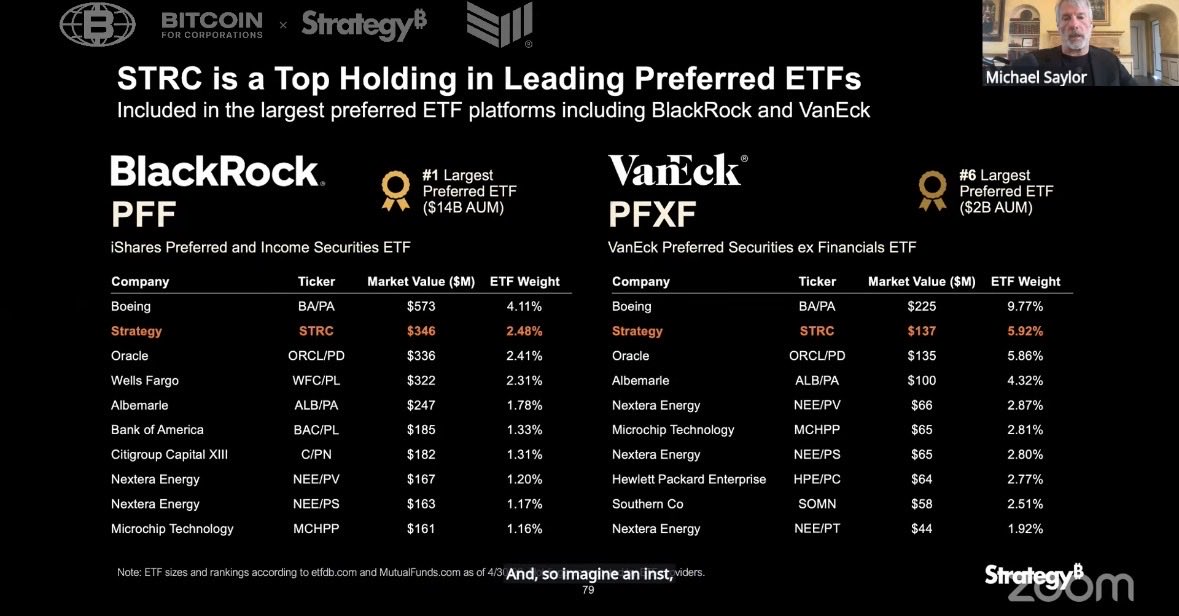

BlackRock PFF ETF hold $345M of $STRC.

Apyx - $280M of $STRC.

VanEck PFXF ETF hold $141M of $STRC.

Strive hold $50M of $STRC.

We purchased another 1,000,000 shares of $STRC today. 🚀

Apyx now holds approximately $280M of $STRC, powering the next generation of onchain digital credit yield.

3

3

31

2,842

People tell me $STRC is a ponzi…

Yet, all these institutions, and more, are happy to bake it into their offerings:

• BlackRock (PFF ETF – major holding)

• VanEck (PFXF ETF – top holding)

• Fidelity (multiple income funds)

• Anchorage Digital (balance sheet holder)

Facts vs feelings

6

3

52

1,275

Why MSTR Holders Should Not Be Selling After Q1 2026

The headline coming out of Strategy's Q1 2026 earnings call was simple and ugly: Michael Saylor said the company "will probably sell some bitcoin to pay a dividend." The stock dropped, Bitcoin slipped under $77K, and a chorus of "the cult is broken" takes lit up the timeline.

That reading is wrong. The actual deck Strategy released today reframes the picture entirely. Here's what's actually happening, and why selling MSTR right now is likely the worst move available.

The flywheel didn't break — it adapted

Strategy raised $11.7 billion in capital in just the first four months of 2026. Bitcoin Per Share (BPS) grew from 195,000 sats in December 2025 to 213,371 sats in May 2026 — a 9.4% YTD BTC yield. That's not a broken accumulation engine. That's an engine running hot.

What did change is how they're raising. In January, ATM issuance was 88% common stock (MSTR) and 12% credit. By April, that mix had inverted to 17% common and 83% preferred credit. When MSTR's premium-to-NAV compressed and equity issuance became less accretive, Strategy pivoted to credit-led capital raises and the BPS compounding continued without missing a beat.

This is adaptive financial engineering, not desperation. The treasury operation now has multiple levers — common equity, five different preferred series (STRC, STRF, STRD, STRK, STRE), convertible debt, and yes, BTC sales — that can be modulated based on which spread is most attractive in any given quarter.

The "BTC sales" framing is being misread

The single most important slide in the deck shows that Strategy can fund its entire $1.5 billion annual dividend obligation forever — by selling BTC — as long as Bitcoin appreciates faster than 2.3% per year.

That is an absurdly low hurdle. Bitcoin's 15-year compound annual growth rate is over 100%. Even in the most pessimistic long-term forecasts, 2.3% is a floor, not a ceiling.

Saylor's "we'll sell some bitcoin" comment is printed in the deck itself as Capital Markets Principle #6: "Sell BTC when advantageous to the Company." It sits alongside five other principles including selling MSTR, growing STRC demand, and reducing convertible debt. It's a tool in a toolkit, not a regime change.

What Saylor actually did on the call was remove a behavioral constraint that was creating an artificial vulnerability. By openly stating BTC sales are on the table, he kills the short-seller thesis that "Strategy will eventually be forced to sell unexpectedly." This is moat-building, not capitulation.

STRC has become the load-bearing wall

The unappreciated story is what STRC has become in nine months. $8.5 billion in notional value. $375 million in average daily volume — 25 times the liquidity of the next-largest tradeable preferred stock on the planet. The largest preferred globally by market cap. A top holding in BlackRock's PFF (the world's largest preferred ETF) and VanEck's PFXF.

Approximately 3 million households now own STRC, mostly through retail brokerages and ETF wrappers. It's been adopted by tokenization platforms, used as collateral in DeFi, and integrated into European ETPs. Corporate treasuries are starting to allocate to it.

This is no longer a Saylor experiment. It's an institutional fixed-income product with genuine market depth, and it's the structural foundation that makes the rest of the model work without requiring the cult-level mNAV premiums of 2024.

The performance numbers haven't lied

Since adopting the Bitcoin standard in August 2020, MSTR has annualized 59% versus Bitcoin's 39%. That's 1.5x amplification, sustained across multiple bull and bear cycles. The "MSTR is just a leveraged BTC bet that underperforms in down markets" thesis isn't supported by the actual data — even after the brutal drawdown of late 2025 and early 2026, MSTR has structurally outperformed spot.

The risk that actually matters

1

3

150

STRC is a top 3 holding in PFF and PFXF

The go-ahead to apex carry in Wall Street has a soft green light.

Confidence in the instrument IS EVERYTHING in carry trades.

1

14

672

It’s proxy season, and as we carefully vote $NODE’s shares, it’s worth highlighting an interesting proposal from Strategy $MSTR that we feel compelled to weigh in on -->

Proposal:

"To approve and adopt an amendment and restatement of the Certificate of Designations of the Company’s Variable Rate Series A Perpetual Stretch Preferred Stock to provide for two scheduled dividend payment dates per month, instead of one."

As common shareholders of MSTR, we support voting FOR this proposal, but there are tradeoffs.

Receiving dividends twice per month instead of once allows slightly faster reinvestment, worth roughly 2–3 basis points annually to STRC holders at current rates. The incremental investor benefit is modest, but directionally positive.

The reason for this change of terms is that it is vitally important to Strategy that STRC remains an attractive, stable product. It is designed to trade around its $100 target value, and when it does, Strategy can issue more of it efficiently. That supports ongoing Bitcoin accumulation with less reliance on common equity issuance.

Semi-monthly payments should help on the margin to keep the security trading closer to par: smaller, more frequent ex-dividend adjustments reduce the magnitude of each price drop, smooth out the step-down pattern, and shorten reinvestment lag. It also provides a smoother, more frequent income stream that aligns with the “paycheck-style” cash flow many income-focused investors prefer.

The drawback is structural: Strategy is increasingly relying on preferred investors as a funding source. As that reliance grows, the company takes on more fixed obligations: regular cash dividends, pressure to maintain par-like trading, and less flexibility in capital allocation. Over time, this shifts more of the economic claim to preferred holders and can pull management toward prioritizing stability for that investor base. In weaker markets, those constraints can become binding and may come at the expense of common shareholders.

This proposal pushes further in that direction. It strengthens STRC, but in doing so increases Strategy’s dependence on preferred investors as a core funding base.

Still, we believe STRC functioning well is now central to Strategy's model. If small adjustments like this help sustain demand and support issuance at scale, they improve Strategy’s ability to accumulate Bitcoin over time.

On balance, the trade-off is reasonable, we support the change, and recommend common holders vote FOR.

(Note: These are $NODE shares that I am voting. We will communicate how $PFXF, one of the largest STRC holders, will vote its shares closer to the meeting. Supporting this proposal should be less controversial for STRC holders than for common equity plebs.)

27

32

307

106,621

Apr 8

🟤 VanEck PFXF, 스트래티지 'STRC' 1억 2,700만 달러 대량 매입!

- Strategy 영구 우선주 'STRC' 127만 주

이는 PFXF 순자산의 약 6%에 해당하는 디지털 신용 자산

11.5% 고배당 Stretch가 기관 포트폴리오에 본격 편입

1

3

17

2,877

Apr 7

Fair, the $199B is the preferred market, not PFXF itself (sourced from btc treasuries lol)

But ~$127M into $STRC from a preferred ETF is still ~6% of its book

3

142

I believe your math is off. Looks like the ETF owns 6% of STRC.

PFXF has $2 billion of assets. Not $199B.

1

4

313