#mdpijcm

Check out #HighlyCitedPaper

📊 3k views | 31 citations

✨highlights the significant role of the #ALI as an independent prognostic factor for all-cause mortality in patients suffering from STEMI undergoing #pPCI

👉mdpi.com/2992830

🏫@unimessina

@MediPharma_MDPI

49

Jun 13

Fly ball, low wiff, ppci rating, dmg, iso

Sometimes I just run the trophy filter or the bombs and stars, make sure they got good conditions, 30% or higher fly ball and 48% or more power hitting

2

16

Jun 13

pPcI

⎐كُـود⎐كوبِون⎐خـِصم⎐

🎉 خصم مفاجأة

⎐ايهرب⎐ايهيرب اهرب

⊵IPY1290⊴

⎐دبدوب⎐

⎐Q16⊴

⎐ترنديول⊴ترند يول⎐

⊵BDL⊴

1

Jun 13

#GuidelinesSaturday

ACC/AHA🧵 STEMI- 2025 ACC/AHA ACS Guidelines #Key recommendations from Rao et al., Circulation 2025

🚨 STEMI ⬇️⏱️#TIMEISMYOCARDIUM

🟥 Class 1:

🥇 12-lead ECG within 10 minutes of first medical contact (FMC)

🥇 Class 1: EMS should notify the cath lab before arriving

🥇 Class 1: FMC-to-device goal ≤90 min (direct); ≤120 min (transfer)

🛑 Every 30-min delay in PPCI → 7.5% increase in relative 1-year mortality risk. #PPCI

🫀 PPCI is the preferred reperfusion strategy — but timing matters:

🟥 [Class 1] (LOE A)

✅ <12h from symptom onset → PPCI

🟡 [Class 2a]

🟡 12–24h → PPCI reasonable

🟡 >24h ongoing ischemia/arrhythmia → PPCI reasonable

🛑 [Class 3: HARM]

🚫 >24h, stable, totally occluded, no ischemia → PPCI not recommended

#ReperfusionStrategy

💉 When you can't do primary PCI…

If anticipated FMC-to-device >120 min → give fibrinolysis (Class 1, LOE A) within 12h of symptom onset.

👌 Preferred agents: tenecteplase, reteplase, alteplase (fibrin-specific)

After lysis → transfer ALL patients to PCI center immediately. Early angiography at 2–24h recommended (Class 1, LOE B-R)

#Fibrinolysis #PharmacoinvasiveStrategy

🤛 Radial access is the new standard (Class 1, LOE A)

Meta-analysis of 7 RCTs (n=48,600 ):

↓ 24% relative reduction in all-cause death

↓ 51% reduction in major bleeding

↓ 62% reduction in vascular complications

#RadialAccess#PCIAccess

💊 Antiplatelet therapy in STEMI

🟥 [Class 1](LOE A)

✅️ Aspirin loading dose 162–325 mg → then 75–100 mg/day

✅️ Clopidogrel fibrinolysis

🟥 [Class 1](LOE B-R)

✅️ Add ticagrelor or prasugrel — preferred over clopidogrel for PPCI

🛑 [Class 3: HARM]

🚫 Prasugrel contraindicated in prior stroke/TIA

#DAPT#Ticagrelor#Prasugrel

🩸 Anticoagulation during PPCI

🟥 UFH — standard, Class 1 (C-EO)

🟥 Bivalirudin — now Class 1 for STEMI! (LOE B-R) — the BRIGHT-4 trial showed ↓ all-cause death ↓ stent thrombosis vs UFH when full-dose post-PCI infusion used for 2–4h

🟡 Enoxaparin IV — Class 2b alternative

🚫 Fondaparinux — do NOT use to support PCI (catheter thrombosis risk)

#Bivalirudin#BRIGHT4

❤️ Multivessel CAD in STEMI — major update! ⚡

🟥 Complete revascularization recommended in hemodynamically stable STEMI MVD (Class 1, LOE A)

🟡 Single-procedure multivessel PCI may be preferred over staged (Class 2b, LOE B-R) — BIOVASC MULTISTARS AMI

🚫 Cardiogenic shock → culprit-only PCI only (Class 3: Harm) — CULPRITSHOCK

#CompleteRevascularization#MVD

😮 Cardiac arrest STEMI

🟥 Resuscitated awake STEMI → PPCI (Class 1, LOE B-NR)

🟡 Comatose favorable features STEMI → PPCI reasonable (Class 2b)

🚫 Comatose hemodynamically stable NO ST-elevation → immediate angiography NOT recommended (Class 3: No Benefit, LOE A) — consistent across 6 RCTs

#CardiacArrest#PostROSC

⚡️ Cardiogenic shock — new MCS guidance

🟡 Microaxial flow pump (Impella) in selected STEMI severe/refractory shock → reasonable to reduce death (Class 2a, LOE B-R) — DanGer-SHOCK: ↓ 26% all-cause mortality at 180d (NNT=8)

⚠️ But: ↑ bleeding, limb ischemia, renal failure. Patient selection matters.

🚫 Routine IABP or VA-ECMO → not recommended (Class 3: No Benefit)

#CardiogenicShock#DanGerSHOCK#MCS

💊 Secondary prevention post-STEMI

🟥 [Class 1](LOE A)

✅️ High-intensity statin for ALL — consider adding ezetimibe upfront

✅️ Add nonstatin agent if LDL-C ≥70 mg/dL on max statin

✅️ DAPT ≥12 months if no high bleeding risk

✅️ Annual influenza vaccine

✅️ Cardiac rehab referral before discharge #SecondaryPrevention#StatinTherapy

🏁 STEMI 2025 — the takeaways:

1️⃣ Radial access is now Class 1 standard

2️⃣ Bivalirudin upgraded to Class 1 for PPCI

3️⃣ Complete revascularization: single-procedure preferred over staged

4️⃣ Microaxial pump: benefit shown but complications high — select carefully

5️⃣ Immediate angiography after non-STEMI arrest: still a firm Class 3

📄 Rao SV et al. Circulation 2025;151:e771–e862≤90min FMC-device26%↓ mortality (MCS)NNT 8DanGer-SHOCK#STEMI#CardioTwitter#ACSGuidelines2025

1

80

Jun 11

Liat Ro nya thoraxnya panjang benul, oh oke mungkin harus turunin leadnya biar menyentuh pas di jantung tapi ternyata tetap elevasi. Terus troponin keluar taraa 4 ribu sobat langsung PPCI

1

75

Jun 11

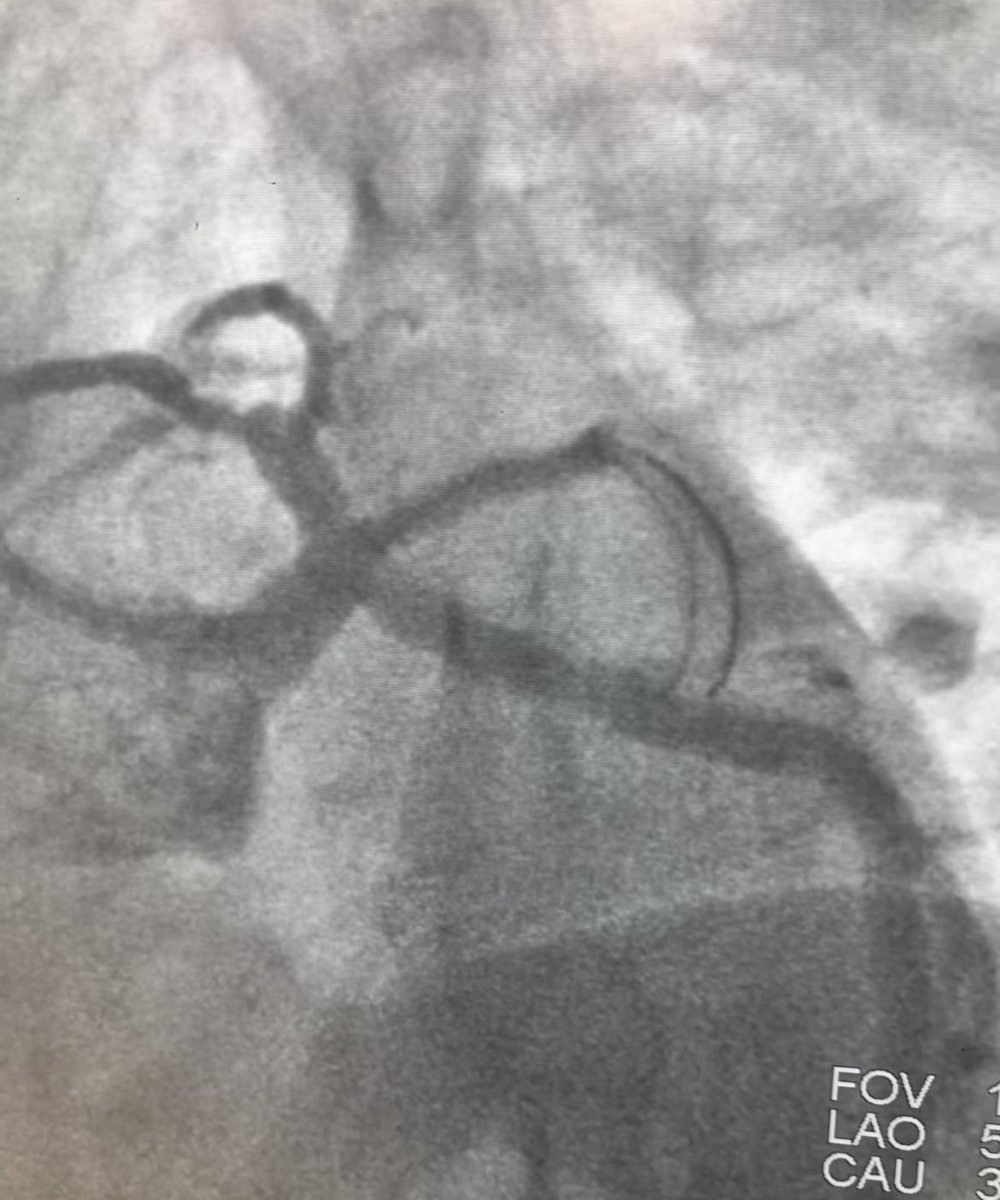

Isolated posterior STEMI is uncommon 3-10% of STEMIs . As suggested usually LCX in dominant system <commonly Ramus as in this case/ or OM . PPCI proximal ramus 2.5x33mm stents .

-50% of cases are not recognised as st dep in v1-3 misread as NSTEMI .

#cardiology #CardiEd

136

Gabina Consultoria

Especialista em PPCI — Projeto de Prevenção e Proteção Contra Incêndio.

share.google/nThbezV2y4tCEMu…

17

Default Judgment Must be Respected by Federal Court

Full Faith and Credit Act Controlled

Read the full article at lnkd.in/evHXiiFE and at zalma.com/blog.

Posted on June 9, 2026 by Barry Zalma

Post number 5368

Posted on June 9, 2026 by Barry Zalma

In Prime Insurance Company, Inc. v. Medicab Transportation, LLC, Jason Rhodes, and Dale Johnson v. Prime Insurance Company, Inc and Prime Property & Casualty Insurance, Inc. No. 2:24-cv-421-SPC-KRH, United States District Court, M.D. Florida, Fort Myers Division (June 3, 2026) Medicab, a paratransit company, bought two policies in 2021: a Business Auto Policy from PPCI and a Commercial Liability Policy from Prime. Both policies, as originally written, appeared to cover injuries arising from loading and unloading patients from Medicab vans.

After a patient, Margaret St. Aubin, fell while being unloaded from a van and suffered injuries, her Estate made a $1 million demand. Prime and its claims administrator concluded that the Commercial Policy’s loading/unloading language had been included by mutual mistake, because the parties allegedly intended only the Auto Policy to cover such automobile-related risks.

Prime then amended the Commercial Policy and filed a declaratory action in Utah seeking reformation of the Commercial Policy. Medicab did not appear, and the Utah court entered a default judgment reforming the policy and declaring no Commercial Policy coverage.

Later, the Estate obtained a $412,440.71 judgment against Medicab and its employees in Florida, exceeding the Auto Policy’s $100,000 limit. Prime then filed this federal action in Florida, while Medicab counterclaimed for breach of contract, bad faith, fiduciary breach, and misrepresentation.

LAW

Under the Full Faith and Credit Act, 28 U.S.C. § 1738, a federal court must give a state-court judgment the same preclusive effect it would receive in the rendering state. Applying Utah preclusion law, the court distinguished between claim preclusion and issue preclusion (collateral estoppel). Issue preclusion applies when:

1. the issue is identical to one decided previously,

2. there was a final judgment on the merits,

3. the issue was fully and fairly litigated, and

4. the party to be estopped was a party or in privity with a party in the earlier action.

Utah law also recognizes that a default judgment counts as a judgment on the merits, and that an insurer-insured relationship may create fiduciary duties in the third-party insurance context. Fraudulent and negligent misrepresentation claims require falsity, reliance, causation, and damages.

For collateral estoppel to bar a subsequent claim, four elements must be satisfied: (1) the issue challenged must be identical in the previous action and in the present case; (2) the issue must have been decided in a final judgment on the merits in the previous action; (3) the issue must have been competently, fully, and fairly litigated in the previous action; and (4) the party against whom collateral estoppel is invoked in the current action must have been either a party or privy to a party in the previous action.

DISCUSSION

The court held that the Utah default judgment had substantial preclusive effect. Medicab was a party to the Utah action. That preclusion barred Medicab’s contract claims, declaratory claim, and good-faith claim, because the Utah judgment had already determined that the Commercial Policy must be reformed, provided no coverage for the accident, and imposed no duty on Prime to defend or indemnify.

Utah law clearly indicates that default judgment is a judgment on the merits.

ANALYSIS

The case turns almost entirely on issue preclusion. The Florida federal court treated the Utah default judgment as binding not only on Medicab, but also on Medicab’s employees, because their rights depended on the same policy language and coverage position. When federal courts are asked to give res judicata effect to a state court judgment, it must apply the res judicata principles of the law of the state whose decision is set up as a bar to further litigation.

The court was also careful to separate claims that truly overlapped with the Utah adjudication from those that did not.

CONCLUSION

The Court declined Medicab Defendants’ invitation to set aside the Utah judgment. The court held that the Utah judgment precluded Medicab from relitigating whether the Commercial Policy covered the accident or whether Prime had a duty to defend or indemnify. Accordingly, Medicab’s claims for breach of contract, breach of good faith, declaratory relief, and breach of fiduciary duty failed, and PPCI was dismissed entirely.

ZALMA OPINION

Allowing a court to enter a default judgment against a plaintiff is a serious error. Once the judgment is entered it becomes final and all other courts, including federal courts, must give credit to the judgment regardless of claims providing to the judgment. The claims of bad faith died because of the default judgment.

(c) 2026 Barry Zalma & ClaimSchool, Inc.

Please tell your friends and colleagues about this blog and the videos and let them subscribe to the blog and the videos.

Subscribe to my substack at gbarryzalma.substack.com/sub…

Go to X @bzalma; Go to Barry Zalma videos at Rumble.com at rumble.com/account/content?t…; Go to Barry Zalma on YouTube- Cwww.youtube.com/channel/UCy…; Go to the InsuranceClaims Library – lnkd.in/gwEYk.

43

Default Judgment Must be Respected by Federal Court

Full Faith and Credit Act Controlled

Read the full article at lnkd.in/evHXiiFE and at zalma.com/blog.

Posted on June 9, 2026 by Barry Zalma

Post number 5368

Posted on June 9, 2026 by Barry Zalma

In Prime Insurance Company, Inc. v. Medicab Transportation, LLC, Jason Rhodes, and Dale Johnson v. Prime Insurance Company, Inc and Prime Property & Casualty Insurance, Inc. No. 2:24-cv-421-SPC-KRH, United States District Court, M.D. Florida, Fort Myers Division (June 3, 2026) Medicab, a paratransit company, bought two policies in 2021: a Business Auto Policy from PPCI and a Commercial Liability Policy from Prime. Both policies, as originally written, appeared to cover injuries arising from loading and unloading patients from Medicab vans.

After a patient, Margaret St. Aubin, fell while being unloaded from a van and suffered injuries, her Estate made a $1 million demand. Prime and its claims administrator concluded that the Commercial Policy’s loading/unloading language had been included by mutual mistake, because the parties allegedly intended only the Auto Policy to cover such automobile-related risks.

Prime then amended the Commercial Policy and filed a declaratory action in Utah seeking reformation of the Commercial Policy. Medicab did not appear, and the Utah court entered a default judgment reforming the policy and declaring no Commercial Policy coverage.

Later, the Estate obtained a $412,440.71 judgment against Medicab and its employees in Florida, exceeding the Auto Policy’s $100,000 limit. Prime then filed this federal action in Florida, while Medicab counterclaimed for breach of contract, bad faith, fiduciary breach, and misrepresentation.

LAW

Under the Full Faith and Credit Act, 28 U.S.C. § 1738, a federal court must give a state-court judgment the same preclusive effect it would receive in the rendering state. Applying Utah preclusion law, the court distinguished between claim preclusion and issue preclusion (collateral estoppel). Issue preclusion applies when:

1. the issue is identical to one decided previously,

2. there was a final judgment on the merits,

3. the issue was fully and fairly litigated, and

4. the party to be estopped was a party or in privity with a party in the earlier action.

Utah law also recognizes that a default judgment counts as a judgment on the merits, and that an insurer-insured relationship may create fiduciary duties in the third-party insurance context. Fraudulent and negligent misrepresentation claims require falsity, reliance, causation, and damages.

For collateral estoppel to bar a subsequent claim, four elements must be satisfied: (1) the issue challenged must be identical in the previous action and in the present case; (2) the issue must have been decided in a final judgment on the merits in the previous action; (3) the issue must have been competently, fully, and fairly litigated in the previous action; and (4) the party against whom collateral estoppel is invoked in the current action must have been either a party or privy to a party in the previous action.

DISCUSSION

The court held that the Utah default judgment had substantial preclusive effect. Medicab was a party to the Utah action. That preclusion barred Medicab’s contract claims, declaratory claim, and good-faith claim, because the Utah judgment had already determined that the Commercial Policy must be reformed, provided no coverage for the accident, and imposed no duty on Prime to defend or indemnify.

Utah law clearly indicates that default judgment is a judgment on the merits.

ANALYSIS

The case turns almost entirely on issue preclusion. The Florida federal court treated the Utah default judgment as binding not only on Medicab, but also on Medicab’s employees, because their rights depended on the same policy language and coverage position. When federal courts are asked to give res judicata effect to a state court judgment, it must apply the res judicata principles of the law of the state whose decision is set up as a bar to further litigation.

The court was also careful to separate claims that truly overlapped with the Utah adjudication from those that did not.

CONCLUSION

The Court declined Medicab Defendants’ invitation to set aside the Utah judgment. The court held that the Utah judgment precluded Medicab from relitigating whether the Commercial Policy covered the accident or whether Prime had a duty to defend or indemnify. Accordingly, Medicab’s claims for breach of contract, breach of good faith, declaratory relief, and breach of fiduciary duty failed, and PPCI was dismissed entirely.

ZALMA OPINION

Allowing a court to enter a default judgment against a plaintiff is a serious error. Once the judgment is entered it becomes final and all other courts, including federal courts, must give credit to the judgment regardless of claims providing to the judgment. The claims of bad faith died because of the default judgment.

(c) 2026 Barry Zalma & ClaimSchool, Inc.

Please tell your friends and colleagues about this blog and the videos and let them subscribe to the blog and the videos.

Subscribe to my substack at gbarryzalma.substack.com/sub…

Go to X @bzalma; Go to Barry Zalma videos at Rumble.com at rumble.com/account/content?t…; Go to Barry Zalma on YouTube- Cwww.youtube.com/channel/UCy…; Go to the InsuranceClaims Library – lnkd.in/gwEYk.

41

Default Judgment Must be Respected by Federal Court

Full Faith and Credit Act Controlled

Read the full article at lnkd.in/evHXiiFE and at zalma.com/blog.

Posted on June 9, 2026 by Barry Zalma

Post number 5368

Posted on June 9, 2026 by Barry Zalma

In Prime Insurance Company, Inc. v. Medicab Transportation, LLC, Jason Rhodes, and Dale Johnson v. Prime Insurance Company, Inc and Prime Property & Casualty Insurance, Inc. No. 2:24-cv-421-SPC-KRH, United States District Court, M.D. Florida, Fort Myers Division (June 3, 2026) Medicab, a paratransit company, bought two policies in 2021: a Business Auto Policy from PPCI and a Commercial Liability Policy from Prime. Both policies, as originally written, appeared to cover injuries arising from loading and unloading patients from Medicab vans.

After a patient, Margaret St. Aubin, fell while being unloaded from a van and suffered injuries, her Estate made a $1 million demand. Prime and its claims administrator concluded that the Commercial Policy’s loading/unloading language had been included by mutual mistake, because the parties allegedly intended only the Auto Policy to cover such automobile-related risks.

Prime then amended the Commercial Policy and filed a declaratory action in Utah seeking reformation of the Commercial Policy. Medicab did not appear, and the Utah court entered a default judgment reforming the policy and declaring no Commercial Policy coverage.

Later, the Estate obtained a $412,440.71 judgment against Medicab and its employees in Florida, exceeding the Auto Policy’s $100,000 limit. Prime then filed this federal action in Florida, while Medicab counterclaimed for breach of contract, bad faith, fiduciary breach, and misrepresentation.

LAW

Under the Full Faith and Credit Act, 28 U.S.C. § 1738, a federal court must give a state-court judgment the same preclusive effect it would receive in the rendering state. Applying Utah preclusion law, the court distinguished between claim preclusion and issue preclusion (collateral estoppel). Issue preclusion applies when:

1. the issue is identical to one decided previously,

2. there was a final judgment on the merits,

3. the issue was fully and fairly litigated, and

4. the party to be estopped was a party or in privity with a party in the earlier action.

Utah law also recognizes that a default judgment counts as a judgment on the merits, and that an insurer-insured relationship may create fiduciary duties in the third-party insurance context. Fraudulent and negligent misrepresentation claims require falsity, reliance, causation, and damages.

For collateral estoppel to bar a subsequent claim, four elements must be satisfied: (1) the issue challenged must be identical in the previous action and in the present case; (2) the issue must have been decided in a final judgment on the merits in the previous action; (3) the issue must have been competently, fully, and fairly litigated in the previous action; and (4) the party against whom collateral estoppel is invoked in the current action must have been either a party or privy to a party in the previous action.

DISCUSSION

The court held that the Utah default judgment had substantial preclusive effect. Medicab was a party to the Utah action. That preclusion barred Medicab’s contract claims, declaratory claim, and good-faith claim, because the Utah judgment had already determined that the Commercial Policy must be reformed, provided no coverage for the accident, and imposed no duty on Prime to defend or indemnify.

Utah law clearly indicates that default judgment is a judgment on the merits.

ANALYSIS

The case turns almost entirely on issue preclusion. The Florida federal court treated the Utah default judgment as binding not only on Medicab, but also on Medicab’s employees, because their rights depended on the same policy language and coverage position. When federal courts are asked to give res judicata effect to a state court judgment, it must apply the res judicata principles of the law of the state whose decision is set up as a bar to further litigation.

The court was also careful to separate claims that truly overlapped with the Utah adjudication from those that did not.

CONCLUSION

The Court declined Medicab Defendants’ invitation to set aside the Utah judgment. The court held that the Utah judgment precluded Medicab from relitigating whether the Commercial Policy covered the accident or whether Prime had a duty to defend or indemnify. Accordingly, Medicab’s claims for breach of contract, breach of good faith, declaratory relief, and breach of fiduciary duty failed, and PPCI was dismissed entirely.

ZALMA OPINION

Allowing a court to enter a default judgment against a plaintiff is a serious error. Once the judgment is entered it becomes final and all other courts, including federal courts, must give credit to the judgment regardless of claims providing to the judgment. The claims of bad faith died because of the default judgment.

(c) 2026 Barry Zalma & ClaimSchool, Inc.

Please tell your friends and colleagues about this blog and the videos and let them subscribe to the blog and the videos.

Subscribe to my substack at gbarryzalma.substack.com/sub…

Go to X @bzalma; Go to Barry Zalma videos at Rumble.com at rumble.com/account/content?t…; Go to Barry Zalma on YouTube- Cwww.youtube.com/channel/UCy…; Go to the InsuranceClaims Library – lnkd.in/gwEYk.

34

Btw we will be working on the trophy algo soon its either we will have it adopt the star and bomb algo or we have it follow a different path

Not to sure ! For now trophy just picks the top PPCI

1

12

1,204

14/ Harper, Schwarber, Devers, and Rice all graded extremely well because the signals weren’t fighting each other.

PPCI.

DMG.

AR Zones.

Pitch Edge.

Bullpen.

Spray.

Weather.

Everything was pointing in the same direction.

1

5

1,319

8/ Schwarber was different.

His profile wasn’t built on perfection.

It was built on violence.

34.9 PPCI.

.365 ISO.

67.7% Pull.

11 HR spray chart.

Three Elite Zones.

Elite power profile.

A pure ceiling play.

1

3

1,039

7/ Harper was ridiculous.

37.6 PPCI.

57.6% HardHit.

4 Elite AR Zones.

9/9 bullpen continuation.

Positive pitch edges.

Strong H2H.

Strong weather.

The entire card was screaming the same message.

1

3

1,315

2/ Most people open @TheStarTool and immediately sort by PPCI.

Highest number.

Highest star rating.

Highest projected HR probability.

Then they start building slips.

That’s not what the training teaches.

The training teaches process.

1

7

5,430

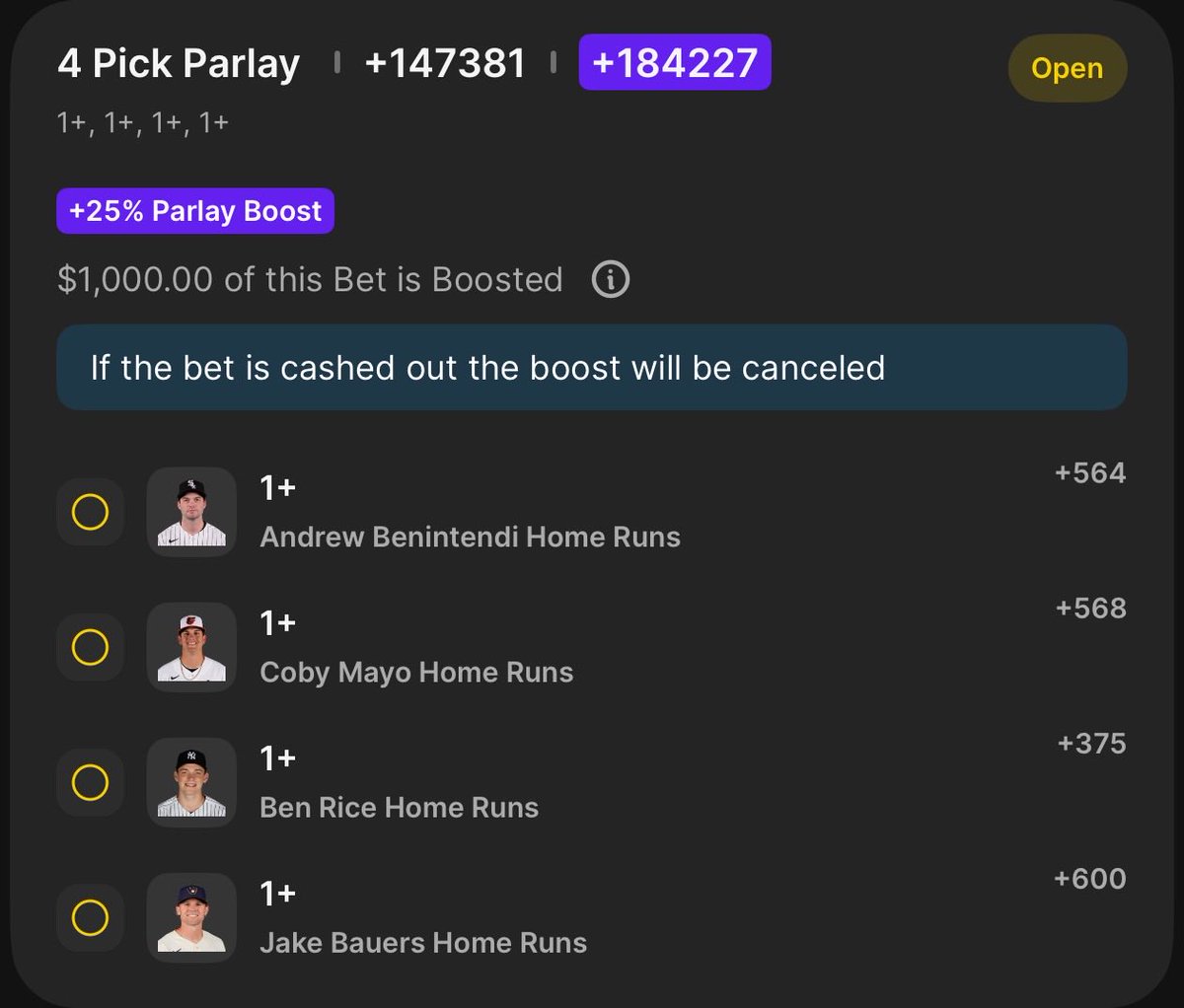

Built today's HR card entirely through process.

Not projections.

Not narratives.

Not "he's due."

Just:

✅ AR Zones

✅ Bullpen Matchups

✅ DMG

✅ PPCI

✅ HR Heat

✅ Spray Charts

✅ Pitch Arsenal Overlap

Final card:

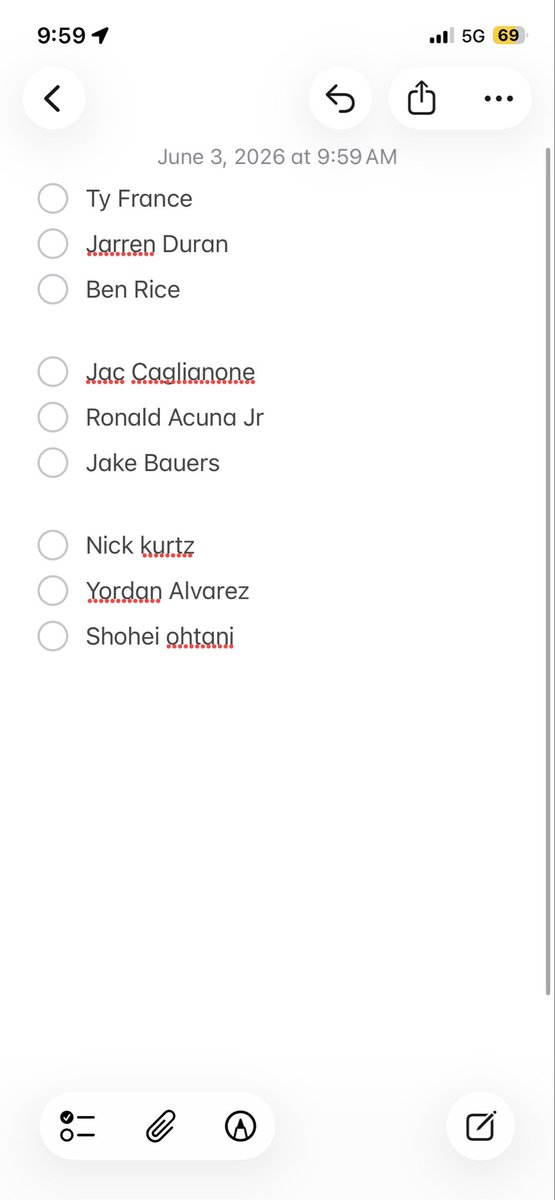

⚾ Andrew Benintendi

⚾ Coby Mayo

⚾ Ben Rice

⚾ Jake Bauers

Which one do you think leaves the yard first?

@TheStarTool

10

5

224

80,774

One thing Star Tool has taught me lately:

The best HR plays aren't always the hitters with the highest HR%.

Sometimes it's the hitter with the strongest ecosystem.

For example, Jake Bauers today:

✓ 9/9 AR Zone Advantage

✓ Favorable bullpen path

✓ Positive wind

✓ Strong PPCI

✓ Strong DMG

✓ Multiple winning pitch interactions

Most people stop at HR%.

The deeper edge is understanding why the HR probability exists.

Here's a full breakdown of the profile and what I saw in the data.

@TheStarTool

👇

1

2

21

3,047

Untuk menjadi seorang ahli di suatu bidang, pasti harus proses. Karena ada "pro" di dalam "proses".

.

.

Apalagi jabatan sepenting wakil presiden atau gubernur bank indonesia.

.

In frame: PPCI pertama mandiri dg bimbingan, pasien stemi inferior-posterior.

1

1

10

636