Alt123 retweeted

2: $PANW — Palo Alto Networks

The heavyweight champion of enterprise security platformization. They are aggressively integrating AI into next-gen firewalls to lock down physical data centers and cloud networks simultaneously.

1

1

2

28

Jun 12

The top SaaS companies I can see leading the acceleration of net new ARR:

$PLTR Government AI platform

$NET Internet infrastructure leader

$CRWD AI-native cybersecurity platform

$DDOG Cloud observability leader

$PANW Platformization cybersecurity leader

$DOCN SMB cloud platform

$FROG DevOps automation platform

7

11

88

10,861

Jun 12

The era of human-speed hacking is over. AI agents now exploit system vulnerabilities in minutes.

PANW is leading a shift called "platformization". Instead of companies duct-taping 50 different security tools together, PANW forces them onto one unified, AI-driven platform that reacts at machine speed.

2/12

1

1

276

Jun 11

🪟 10-year “evergreen” on Azure for a law firm = Microsoft’s Dynamics is creeping into everything except my own sanity. Good signal: the center of gravity is platformization, not lift-and-shift. #Windows #Microsoft #Azure #Dynamics365

windowsforum.com/threads/tlt…

#MicrosoftAzure

1

8

4/5

$PANW raised full-year outlook to ~$11.4B revenue, $8.90–$8.95B NGS ARR, and ~37.5% adj. FCF margin.

Key question: how much platformization growth is organic consolidation vs. acquired metrics? Integration execution risk is real alongside the bullish recurring revenue data.

1

1

27

| Sempozyum

Arş. Gör. Hasan Kamil Genç, Diyanet Center of America tarafından düzenlenen uluslararası sempozyumda “Turkish Maqām Music Under Platformization” başlıklı bildirisini sundu. Hocamızı tebrik eder, akademik çalışmalarında başarılar dileriz.

🔗ilahiyat.siirt.edu.tr/duyuru…

1

10

1,317

So it’s not hard because of product, or product market fit, but from focus.

You tend to feel big enough that you can do everything you couldn’t do when you were really small!

Global expansion

Channel investment

Multi segment successfully

New product lines / platformization

1

10

Jun 10

$PANW is building the most comprehensive platform in cybersecurity.

Traditional cybersecurity: separate product for each threat. Firewall company A, endpoint company B, cloud security company C. An enterprise has 40-50 different security tools.

Palo Alto's thesis: consolidate everything into one platform. Fewer tools, better visibility, faster response.

Platformization result: "those who want PANW can leave others" proposition. Short-term revenue drops (discounts), long-term customers get locked in.

AI integration: Precision AI. Real-time threat detection and prevention AI layer. If one firm sees an X attack today, others are protected before they see it tomorrow.

Cybersecurity spending doesn't get cut even during economic slowdowns. This sector's defensive character.

Not investment advice.

1

52

Jun 10

More of the same? NO.

If the problem is platformization, then the solution is not the next platform. Q102014.xyz

Not the European one.

Not the open one.

Not the better one.

The solution is to exit platform logic.

Not Stack.

Not Platform.

Infrastructure.

The magic word is #Blockchain.

🚀 1969: ARPANET — decentralized data storage

🚀 1989: HTML / Hyperlink

🚀 2001: Wikipedia / Creative Commons

💥 2004: Social Media — platformization of the social

🚀 2008: #Blockchain

🚀 2009: #Bitcoin — a middle finger to total economization

💥 2022: AI — centralization of knowledge and attention

🚀 2026: #PlanD

Not the next platform. Instead:

#Autarky instead of dependency.

#Resilience instead of optimization.

#Xerocracy instead of governance.

#Infrastructure instead of organization.

#Commons instead of platform.

#Protocols instead of operators.

#Forkability instead of lock-in.

The question is not:

Who should own the platform?

The question is:

How do we make the platform obsolete?

Q102014.xyz

44

Jun 8

MODEL ECONOMICS AND THE APPLICATION PROFIT POOL

Arora’s view that foundation models become a utility layer is economically plausible but not inevitable. The transcript frames intelligence as purchasable on demand: lower-cost “120 IQ” reasoning for routine tasks, higher-cost “250 IQ” reasoning for complex tasks. In that world, model providers compete on price/performance, latency, safety, context length, tool use, and reliability, while the application layer captures differentiated workflow value. This resembles the historical split between cloud infrastructure and SaaS applications, although AI model economics are more capital-intensive and may force model providers to move up the stack.

The transcript correctly identifies why OpenAI and Anthropic are moving toward coding, legal, accounting, cyber, and productivity workflows. Compute capex creates a need for high-margin revenue pools, and generic API consumption may not be sufficient to support the required investment cycle. Coding has already emerged as a large application wedge because it has measurable output, direct labor substitution, frequent usage, and clear willingness to pay. Cybersecurity may become another major wedge because the cost of failure is high and AI simultaneously increases attack volume and defense productivity.

The unresolved question is who captures the application layer. Foundation-model companies have model access, talent, brand, and rapid product iteration. Incumbent application vendors have customer relationships, domain data, permissions, workflow embedding, compliance, procurement access, and integration history. New AI-native vertical vendors have clean architectures, consumption-based pricing, and a replacement-TAM sales motion. The likely outcome is not a single winner. Profit pools will fragment by workflow, with durable economics accruing to vendors that combine models with proprietary context, trusted execution, and distribution.

For cybersecurity specifically, raw model access should commoditize faster than production-grade cyber outcomes. Model companies can offer powerful scanning, exploit generation, and coding assistance, but enterprise CISOs need prioritization, enforcement, incident response, liability alignment, and operational automation. This is why Palo Alto, CrowdStrike, Microsoft, Google/Mandiant, Cloudflare, Cisco/Splunk, IBM/Red Hat, and specialized AI-security vendors can all participate. The strategic battle is not “model versus application” in isolation; it is model plus context plus enforcement plus trust.

OPEN SOURCE AND THE REMEDIATION ECONOMY

The transcript’s open-source concern is critical. Open source underpins enterprise software stacks, but maintainers are often capacity-constrained, underfunded, and not organized to handle AI-generated vulnerability volume. Anthropic’s update explicitly states that progress is shifting from being limited by vulnerability discovery to being limited by how quickly findings can be verified, disclosed, and patched; it also notes that some maintainers asked Anthropic to slow the rate of disclosures because they needed more time to design patches.

IBM and Red Hat’s Project Lightwell directly validates the emergence of an open-source remediation economy. IBM and Red Hat announced a $5B commitment backed by frontier AI capabilities and more than 20,000 engineers to create a trusted enterprise clearinghouse for securing open-source software supply chains. The initiative is designed to identify vulnerabilities, validate and test fixes, and deliver secure patches through commercial subscriptions.

This is highly relevant for investors because it indicates that the AI-cyber opportunity is not limited to detection products. The larger opportunity may be managed remediation, enterprise-grade patch certification, software supply-chain governance, dependency lifecycle management, and trusted distribution. These are recurring revenue opportunities with strong compliance and risk-management hooks, especially for financial services, healthcare, government, and critical infrastructure.

The open-source dimension also raises a risk for Palo Alto and other pure cyber vendors. IBM/Red Hat can monetize open-source trust at the dependency layer, cloud providers can monetize secure build pipelines, GitHub/Microsoft can integrate remediation into developer workflows, and application-security vendors can own SDLC insertion points. Palo Alto’s best response is to link runtime exposure, exploitability, and enterprise controls to development remediation, rather than treating code scanning as a standalone tool.

NATIONAL SECURITY AND ECONOMIC CHAOS

The source material appropriately distinguishes national-security hard targets from economy-wide soft targets. The risk is not only that a state actor compromises a power grid. The more probable systemic risk is that AI-enabled attackers exploit old software, open-source dependencies, vendor appliances, small-business systems, healthcare intermediaries, municipal infrastructure, and 3rd-party service providers at scale. The Change Healthcare breach illustrates this point. The American Hospital Association described the February 2024 cyberattack as an unprecedented national disruption to healthcare operations, and Reuters reported that UnitedHealth advanced more than $2B to providers financially impacted by the attack.

The transcript’s statement that 89% of attacks occur because credentials are stolen should be treated as a rhetorical or category-specific point rather than a universal current statistic. The 2026 Verizon DBIR says 31% of breaches now start with software vulnerabilities, beating stolen passwords as the top initial pathway, while 48% of breaches involve ransomware and 15 different attack techniques are being bolstered by generative AI. This reinforces, rather than weakens, the Mythos thesis: vulnerability exploitation is becoming more central, not less.

The policy implication is that model restriction alone is unlikely to be sufficient. Anthropic itself states that similar capabilities are likely to proliferate and that defense requires coordinated action across frontier AI developers, software companies, security researchers, open-source maintainers, and governments. Restrictions may create a temporary defender head start, but model capability diffusion, open-source replication, distillation, and foreign development reduce durability. The more durable policy path is likely to involve model evaluations, controlled access for high-risk capabilities, vulnerability-disclosure infrastructure, critical-infrastructure scanning programs, procurement standards, and liability frameworks.

For public equities, regulation could be 2-sided. It could raise compliance burdens and restrict certain AI cyber capabilities. It could also entrench trusted cybersecurity incumbents that can meet government standards, support classified or regulated environments, maintain auditability, and provide certified remediation. Palo Alto, Microsoft, Google, IBM/Red Hat, Cisco, CrowdStrike, and large systems integrators would likely be better positioned than smaller point vendors under a compliance-heavy regime.

DATA, TELEMETRY, AND INFRASTRUCTURE

Arora’s claim that enterprises may need 10x more cyber data is directionally consistent with the shift toward AI-driven defense. AI defense requires a richer baseline of “normal” behavior across endpoints, networks, cloud workloads, identities, SaaS applications, browsers, code repositories, data pipelines, and agent actions. Without historical context and live telemetry, models cannot reliably distinguish benign anomalies from exploit chains or prioritize the highest-risk findings.

This supports data infrastructure and observability spend, but the revenue allocation is nuanced. Data lakes, log stores, event pipelines, SIEM replacements, cloud data platforms, vector search, metadata systems, and governance tools all benefit from higher data intensity. However, indiscriminate logging creates cost inflation. The winners will be platforms that reduce total-cost-of-ownership per useful signal, not simply vendors that store more raw data. Compression, filtering, retention-tiering, schema normalization, and real-time enrichment become economically important.

Chronosphere fits this logic better than a superficial “observability adjacent” reading might suggest. Palo Alto agreed to acquire Chronosphere for $3.35B to enhance AI-driven cybersecurity capabilities and integrate its data into the Cortex AgentiX platform, according to Reuters. The strategic rationale is that security operations and observability increasingly converge when AI agents, cloud-native services, and distributed applications generate high-volume telemetry that must be interpreted in real time. The risk is that observability is a competitive, cost-sensitive category, and Palo Alto must prove that Chronosphere improves security outcomes rather than merely expanding TAM language.

HARDWARE, LATENCY, AND SUPPLY CHAIN

The hardware discussion is a useful counterweight to simplistic “software eats everything” narratives. Arora’s point is that hardware remains the cheapest and most reliable way to manage high-throughput, low-latency workloads. This is relevant for security appliances, data-center networking, financial-services latency-sensitive workloads, AI inference, edge inspection, and OT environments. Cloud migration has limits where latency, determinism, data residency, compliance, or cost matter.

For Palo Alto, this supports continued relevance of network security hardware and hybrid deployments even as the company shifts toward software, subscriptions, SASE, cloud, and AI-driven platforms. Hardware may not be the highest-multiple revenue stream, but it can remain a strategic enforcement point and customer anchor. The risk is that hardware supply constraints and component inflation can pressure gross margin or elongate deployment cycles, while cloud-delivered security and hyperscaler-native controls continue to improve.

The broader semiconductor and AI-infrastructure implication is that production, not design, often becomes the bottleneck. The transcript’s supply-chain discussion aligns with market behavior: AI capex has strained memory, advanced packaging, networking, power, cooling, and manufacturing capacity. For TMT portfolios, this favors select infrastructure enablers but also introduces cyclicality. If AI capex overshoots or utilization disappoints, the same supply chain can de-rate quickly.

PALO ALTO NETWORKS STRATEGY AND M&A

The transcript describes a historical Palo Alto playbook: acquire product companies, plug them into the go-to-market engine, integrate the backend, and increase wallet share with existing customers. That playbook can work in cybersecurity because customers prefer fewer tools, better integration, consolidated telemetry, and clearer accountability. It is especially powerful when breach risk, board visibility, and regulatory pressure rise simultaneously.

CyberArk is a category-defining version of that playbook. Chronosphere is broader and more debatable. The transcript suggests an even more ambitious future: if Palo Alto can use AI to operate more efficiently than subscale software companies, it could acquire assets outside its historical center of gravity and improve margins through AI-driven operating leverage. This is a credible strategic option but should be treated as unproven. The further Palo Alto moves from core cybersecurity, the more it risks conglomerate discount, integration friction, investor skepticism, and dilution of strategic clarity.

The margin thesis is central. The transcript references potential gross margins in the 90s and net margins in the 40s-50s if AI materially improves enterprise operations. Palo Alto’s actual FY 2026 guide is materially lower on operating margin, at 28.9%-29.2% non-GAAP, although adjusted free cash flow margin guidance is 37.5% and management has stated it remains on track for 40% adjusted free cash flow margin in FY 2028. The gap between current margin structure and aspirational AI-enabled economics is a key upside lever, but also a key source of execution risk.

The most important financial diligence issue is organic growth quality. Q3 metrics were strong, but acquisition contribution was material. A 60% NGS ARR growth rate that includes $1.6B from CyberArk and Chronosphere is not analytically equivalent to 60% organic growth. The market will likely tolerate M&A if platformization, retention, cross-sell, and margin expansion improve. It will penalize the stock if acquisition complexity masks slowing core demand or if reporting changes reduce visibility.

COMPETITIVE LANDSCAPE

Palo Alto is among the most advantaged scaled cyber platforms, but it is not the only logical winner. CrowdStrike has endpoint telemetry, identity ambitions, and cloud security expansion. Microsoft controls Windows, Entra identity, Defender, GitHub, Azure, and a massive enterprise bundle. Google has Mandiant, Chronicle, cloud telemetry, and AI model depth. Cloudflare has global edge visibility and application delivery control points. Cisco/Splunk has network and security operations installed base. IBM/Red Hat has open-source enterprise trust and remediation infrastructure. Fortinet has appliance economics and SMB/midmarket distribution. The AI-cyber opportunity is large enough for multiple winners, but pricing and platform pressure will be intense.

Palo Alto’s relative advantage is breadth across network, cloud, SOC, AI, and now identity, plus an enterprise sales engine capable of packaging strategic programs for CISOs and boards. Its relative disadvantage is complexity. A platform story can become either a simplification story or a bundling tax. The determining factor will be measurable security outcome improvement: lower alert volume, faster response, fewer successful intrusions, lower tooling cost, faster patch prioritization, and reduced breach blast radius.

The competitive threat from model providers is real but likely narrower than feared. OpenAI, Anthropic, and Google can create best-in-class code and cyber models. However, enterprise cyber buyers require deployment, governance, evidence, SLAs, privacy controls, remediation workflows, and integration with existing tools. Model companies can capture a portion of the economics through APIs, coding tools, and specialized cyber products, but incumbents with telemetry and enforcement should retain meaningful value if they integrate quickly.

INVESTMENT IMPLICATIONS

The source material supports a barbell within software. On the positive side are scaled cybersecurity platforms, identity and privileged-access management, AI SOC automation, attack-surface management, software supply-chain security, open-source remediation, data infrastructure, and low-latency infrastructure. On the negative side are analytical SaaS point products, dashboard-centric marketplace add-ons, seat-based workflow-light tools, and vulnerability scanners that lack prioritization, exploitability context, and remediation workflows.

For Palo Alto specifically, the fundamental thesis is attractive but valuation-sensitive. The company has the correct strategic assets for the AI-cyber era: broad telemetry, enforcement points, a large CISO customer base, Unit 42 incident-response credibility, a platform consolidation motion, identity through CyberArk, observability/telemetry expansion through Chronosphere, and an explicit AI frontier defense narrative. The current multiple requires the company to demonstrate that AI is not only a thematic tailwind but also a measurable driver of organic ARR growth, attach rates, win rates, margin expansion, and customer consolidation.

The highest-quality upside case is not “more breaches equal more spend.” It is that AI increases the required standard of cyber hygiene and creates a forced upgrade cycle across code security, open-source remediation, identity, runtime protection, and SOC automation. If Palo Alto becomes the strategic vendor that boards and CISOs use to compress this upgrade cycle, its wallet share and strategic relevance can rise meaningfully. The weaker upside case is merely fear-based budget acceleration; fear can create pipeline, but durable revenue requires productized remediation and demonstrable outcomes.

The key metrics to monitor are organic NGS ARR excluding acquisition contribution, CyberArk retention and attach into Palo Alto platform deals, Chronosphere integration into Cortex and AI SOC workflows, platformization volumes and net revenue retention, SOC automation outcomes, AI frontier defense monetization, customer evidence of reduced MTTR, sales efficiency, share-based compensation intensity, GAAP profitability progression, and whether free cash flow margin can move toward or above 40% without underinvesting in engineering.

The principal risks are valuation compression, organic-growth opacity, acquisition integration, Microsoft and Google bundling, CrowdStrike endpoint competition, model-provider encroachment, false-positive fatigue, customer remediation bottlenecks, regulatory limits on frontier cyber models, and the possibility that open-source or low-cost AI tools commoditize vulnerability discovery faster than platforms can monetize remediation. Another risk is that AI-generated code increases vulnerability supply faster than vendors can secure it, creating liability and customer paralysis rather than clean budget expansion.

FINAL ASSESSMENT

The source material is strategically important because it captures a live inflection in enterprise technology: AI is not only a productivity tool; it is a force multiplier for cyber offense, cyber defense, enterprise workflow redesign, data infrastructure demand, and SaaS pricing pressure. The most durable conclusion is that context, control, and remediation become more valuable than raw intelligence. That conclusion favors scaled platforms over thin applications and favors governed enterprise systems over generic model access.

“Analytical SaaS is dead” is an overstatement if applied to all SaaS, but it is a powerful stress test for software portfolios. Any SaaS company whose product can be replicated by connecting a model to customer-owned data and routing answers through Slack or email faces seat compression, lower attach rates, and weaker pricing power. Any SaaS company that owns workflow state, write-back permissions, compliance logic, system-of-record authority, or proprietary data has a credible path to survive and potentially benefit.

Palo Alto Networks is one of the most credible public-market expressions of the AI-cyber defense thesis, but the equity is not early. The strategic setup is compelling; the valuation already assumes a large share of the opportunity. The investment debate should therefore be framed around execution evidence rather than theme validation. The theme is increasingly validated by Anthropic, Palo Alto, IBM/Red Hat, Verizon, and real-world incidents such as Change Healthcare. The remaining question is how much of the expanded terminal value of cybersecurity accrues to Palo Alto versus model labs, hyperscalers, endpoint leaders, identity vendors, open-source remediation platforms, and AI-native entrants.

1

1

2,874

Jun 8

$PANW $NVDA $MU $SNDK $LITE Must watch. Full stop.

youtu.be/hObRMv6qCi0?si=lDLx…

EXECUTIVE SUMMARY

The source material is an All-In Podcast session at All-In Liquidity 2026 titled “Analytical Software Is Dead,” featuring Nikesh Arora, chairman and CEO of Palo Alto Networks, in a live-stage discussion with All-In hosts and investors about AI, cybersecurity, enterprise software, model economics, hardware, and M&A. Arora has led Palo Alto Networks since June 2018 after prior senior roles at Google and SoftBank, which is central to the discussion because his perspective combines scaled enterprise go-to-market, infrastructure economics, and cybersecurity operating exposure.

The committee-level read-through is structurally bullish for scaled cybersecurity platforms, identity/security operations, AI-assisted vulnerability remediation, and data infrastructure, while structurally negative for analytical SaaS products whose primary value proposition is collecting enterprise data and presenting dashboards, reports, or workflow-light recommendations. The most investable insight is not simply that AI makes cyber more important. The deeper conclusion is that AI shifts scarcity in cybersecurity from vulnerability discovery to verification, prioritization, patching, exploit-chain context, identity control, telemetry coverage, and real-time response. That shift favors vendors with broad sensors, enforcement points, incident-response credibility, integrated identity, and a large enterprise distribution engine. Palo Alto Networks is unusually well positioned against that map, but the equity already embeds a major portion of the strategic bull case.

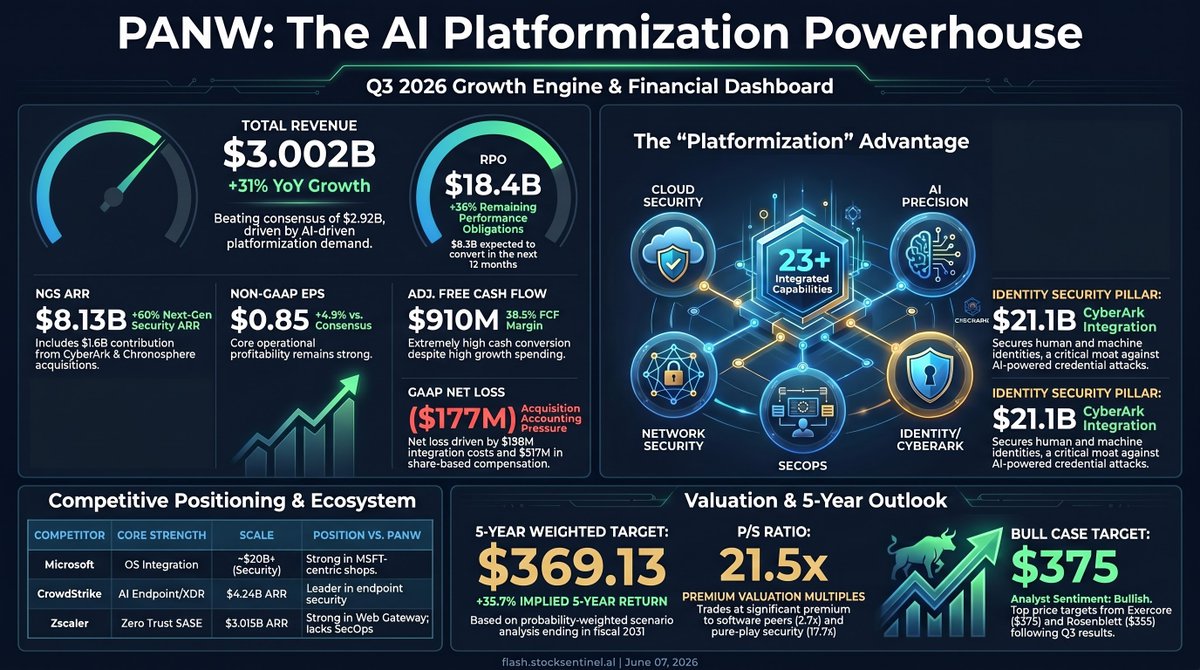

Palo Alto Networks’ latest reported fundamentals support the “scarcity asset” framing but also raise the bar for incremental upside. Fiscal Q3 2026 revenue grew 31% year over year to $3.0B, Next-Generation Security ARR grew 60% to $8.1B, RPO grew 36% to $18.4B, and trailing 12-month adjusted free cash flow margin reached 38.5%; however, $388M of Q3 revenue, $1.6B of NGS ARR, and $1.8B of RPO came from CyberArk and Chronosphere, so organic/inorganic quality matters materially. FY 2026 guidance implies $11.415B-$11.425B of revenue, 28.9%-29.2% non-GAAP operating margin, and 37.5% adjusted free cash flow margin. Latest market data placed PANW at approximately $213B of market capitalization and $266.33 per share, implying roughly 19x FY 2026 revenue and roughly 70x FY 2026 non-GAAP EPS guidance, based on the company’s $3.77-$3.79 EPS outlook.

The transcript’s $238B market-cap reference appears to be approximate or time-sensitive; live market data at the time of analysis was closer to $213B. Even using the lower market value, the transcript’s cited move from $17B at Arora’s starting point implies roughly 12.5x equity value creation. The more important question is whether a path to $1T is economically plausible. From a $213B equity value, $1T requires approximately 4.7x upside. At 25x-40x free cash flow, that requires approximately $25B-$40B of annual free cash flow. At a 40% free cash flow margin, that implies approximately $62B-$100B of revenue, versus FY 2026 guidance of approximately $11.4B. The $1T thesis therefore requires sustained category expansion, large-scale platform consolidation, successful CyberArk and Chronosphere integration, AI-driven margin leverage, and continued premium multiples. It is not an impossible outcome, but it requires execution beyond normal cybersecurity share gain.

AI CYBERSECURITY INFLECTION

Arora’s most important assertion is that frontier AI has compressed security work that historically took years into weeks. The transcript states that Palo Alto tested Mythos for 6 weeks and found vulnerabilities that would normally have taken 5-7 years to find. Public disclosures broadly corroborate the direction of that claim. Anthropic’s Project Glasswing was formed around Claude Mythos Preview, an unreleased frontier model that Anthropic says can surpass all but the most skilled humans at finding and exploiting software vulnerabilities. Launch partners include AWS, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorganChase, the Linux Foundation, Microsoft, NVIDIA, and Palo Alto Networks, and Anthropic committed up to $100M in usage credits plus $4M in open-source security donations.

The public evidence indicates that this is not ordinary scanner improvement. Anthropic reported that, within the 1st weeks of Project Glasswing, approximately 50 partners used Mythos Preview to find more than 10,000 high- or critical-severity vulnerabilities across systemically important software. Cloudflare reportedly found 2,000 bugs, including 400 high- or critical-severity bugs, and Mozilla found and fixed 271 vulnerabilities in Firefox 150 while testing Mythos Preview, more than 10x what it found in Firefox 148 using Claude Opus 4.6. Anthropic also reported that its open-source scans produced 6,202 estimated high- or critical-severity vulnerabilities out of 23,019 total findings, with 90.6% of 1,752 assessed high- or critical-rated findings validating as true positives after independent security review.

Palo Alto’s own disclosures provide a direct bridge from the transcript to monetizable enterprise impact. The company began testing Anthropic’s Claude Mythos model on April 7 2026 as a Project Glasswing launch partner and later stated that frontier AI models were “extraordinarily capable” at finding vulnerabilities and turning them into critical exploit paths in near-real time. Palo Alto’s May “Patch Wednesday” advisory covered 26 CVEs representing 75 issues, versus a usual monthly volume typically below 5 CVEs, after a scan across more than 130 products. The same company update estimated a 3-5-month window for organizations to get ahead of adversaries before AI-driven exploits become more normal.

The strategic implication is that software security has entered a “vuln discovery abundance” regime. In the old regime, the bottleneck was finding subtle bugs. In the new regime, the bottleneck becomes validating findings, prioritizing business-critical exposure, patching without breaking production, compensating with virtual patching, and shrinking mean time to detect and respond. This is favorable for platforms that already sit in the path of network traffic, cloud workloads, endpoints, browsers, identity flows, SOC alerts, and incident response. It is less favorable for standalone vulnerability-discovery vendors or consulting models that are primarily priced around manual scarcity.

The attacker/defender asymmetry is severe. An attacker needs a small number of exploitable true positives, while a defender must triage a large volume of findings, avoid false alarms, preserve uptime, coordinate developers, and deploy patches across heterogeneous environments. This asymmetry makes “better AI” a double-edged sword: it raises the expected number of discovered vulnerabilities while simultaneously increasing the operational burden on security teams. The market should therefore reward vendors that convert findings into prioritized, high-confidence remediation, not simply vendors that produce more alerts.

FALSE POSITIVES, HARNESSING, AND WHY RAW MODELS ARE NOT ENOUGH

The transcript’s discussion of false positives is among its most technically important segments. Arora states that Mythos had a 30% false-positive rate in his internal context and argues that this is tolerable for attackers but dangerous for defenders. This framing is correct even if the public metrics differ by workflow. Anthropic’s reported 90.6% true-positive rate applies to a triaged subset of estimated high- or critical-severity open-source findings after assessment by security firms or Anthropic, while Arora’s 30% false-positive reference appears to describe a different internal operational setting. These figures are therefore not directly comparable, but the combined conclusion is consistent: raw model output must be wrapped in context, harnesses, guardrails, severity scoring, exploitability analysis, and human or automated verification before production use.

This distinction matters for enterprise software valuation. The value will not accrue automatically to the frontier model provider. Enterprise buyers need systems that know asset criticality, exposure, permissions, patch state, business process dependency, compensating controls, and blast radius. A generic model may identify a bug; a production security platform must determine whether that bug is reachable, exploitable, business-critical, already mitigated, safely patchable, or better handled through virtual patching. That context lives in platforms, telemetry lakes, identity systems, endpoint agents, CNAPP stacks, network controls, and SOC workflows.

The self-driving analogy in the transcript is directionally apt. In consumer or enterprise settings with low error tolerance, a model that is directionally good but wrong 10%-30% of the time can be unusable without extensive post-model systems. For cyber defense, the target operating model is not “mostly correct.” It is high precision, high recall, low operational friction, and auditable decisioning. This creates a strong product moat for vendors that combine AI with deterministic policy, security data, and human-expert workflows.

IDENTITY AND THE CYBERARK ACQUISITION

The CyberArk acquisition is strategically coherent within the AI-agent security thesis. Palo Alto completed the acquisition of CyberArk on February 11 2026, positioning identity security as a core pillar of its platform strategy and explicitly framing the target surface as human, machine, and agentic identity. This directly maps to the transcript’s argument that agentic systems will perform work across enterprise systems, create new privileged actors, and require far better control over credentials, secrets, permissions, and lateral movement.

The logic is that AI agents become privileged insiders. They do not merely answer questions; they call APIs, modify data, trigger workflows, summarize calls, update CRM, interact with code repositories, access ticketing systems, and execute tasks across the enterprise. That expands the number of identities, access tokens, service accounts, secrets, delegated permissions, and machine-to-machine interactions. Traditional identity and access management was already a major attack surface; agentic identity makes it more complex and more dynamic.

CyberArk gives Palo Alto a credible control point in privileged access management and secrets management, which complements its network, cloud, endpoint, and SOC assets. The acquisition is also a defensive move against Microsoft, Okta, CrowdStrike, Zscaler, and cloud hyperscalers, each of which can argue for identity-centered security architectures. Palo Alto’s integrated story becomes stronger if identity is not a bolt-on but a unified signal across attack surface management, endpoint, XDR, XSIAM, network enforcement, cloud posture, and AI agent governance.

The execution risk is high. CyberArk was an approximately $25B transaction, and the size of the deal raises integration, sales motion, product overlap, retention, and margin realization risk. Identity security buyers are specialized, and CyberArk’s brand value must not be diluted into generic platform bundling. The upside case requires Palo Alto to preserve CyberArk’s technical credibility while attaching identity to broader platformization deals. The downside case is that Palo Alto overpays for an adjacent category, pressures CyberArk’s independent growth model, and reduces financial transparency through acquisition-driven ARR.

“ANALYTICAL SAAS IS DEAD” IS DIRECTIONALLY RIGHT BUT TOO BROAD

Arora’s “analytical SaaS is dead” statement is intentionally provocative, but the underlying economic claim is persuasive when narrowed. Analytical SaaS products that primarily ingest data from other systems, provide a UI layer, and monetize dashboards, reports, benchmarks, or simple recommendations are exposed to AI-driven substitution. If enterprise data is accessible through governed data platforms and models can query it directly, generate analysis, summarize anomalies, and route conclusions through Slack, email, or workflow agents, then the incremental value of a separate seat-based analytics UI declines.

The transcript’s anecdote about reducing a 20-seat SaaS product to 3 accounts and connecting the data to Slack and Claude captures a critical procurement pattern. Enterprises may increasingly retain system access, preserve data flows, and reduce paid seats. This is dangerous for SaaS companies whose pricing power depends on user-seat proliferation rather than data gravity, write-back authority, compliance, proprietary workflow, or mission-critical execution. AI can compress seat counts even when the underlying system remains in use.

The pressure is most acute for “read-only analytics” and marketplace add-ons built around data that the customer already owns. A Salesforce, ServiceNow, Workday, SAP, Snowflake, or Databricks ecosystem add-on that says “connect data and get insights” must now justify why a model connected to the same data cannot do the job. The bear case is not that all SaaS disappears; it is that customers stop paying premium per-seat prices for thin analytical layers once natural-language agents can perform the query, summary, visualization, and alerting functions.

The transcript’s category distinction is important. Infrastructure software benefits because AI increases data storage, data movement, data governance, security telemetry, model observability, orchestration, and real-time analytics needs. System-of-record and system-of-work software is not dead, but it must be re-engineered. The value shifts away from UI and toward workflow state, permission models, data integrity, audit trails, business logic, API reliability, and agentic execution. In that future, the user interface may become a chat, voice, or agent surface, while the core application becomes a governed transaction and control layer.

The investment implication is that SaaS analysis must move from “does the product have AI features?” to “does the product control a critical workflow, own proprietary data, hold system-of-record authority, or execute write-back actions with trust?” Products that merely display information are at risk. Products that own workflow state, compliance logic, approvals, identity, payments, billing, inventory, or regulated data have more durable relevance. Even there, UI-based pricing power and seat expansion assumptions likely deserve pressure-testing.

3

2

10

8,247

Alt123 retweeted

$PANW (Palo Alto Networks) — Platformization: replacing 10 point products with one AI platform. $1B ARR from deals. 80,000 enterprise customers.

1

1

3

1,070

Jun 8

---

date: 2026-06-08 07:00:00 08:00

draft: false

original_lang: zh

summary: Today's focus is on OpenAI's internal strategic shift, as ChatGPT evolves

from a chat tool into a super-app with integrated Agents. On the technical front,

Google's Gemma 4 has implemented QAT quantization technology, marking a new phase

for on-device AI where energy efficiency is a priority. Meanwhile, AI programming

tools are achieving a closed loop between design and development, but high Token

consumption is causing the industry to re-examine the narrative around AI cost reduction.

title: 2026-06-08 AI Daily | OpenAI Strategically Restructures "Super App"; Edge AI

Enters QAT Quantization Era

translation_source: gemini

translation_type: system_translated

translation_updated_at: '2026-06-07T23:40:10Z'

---

✨ 2026-06-08 AI Daily | OpenAI Strategically Pivots to "Super App"; On-Device AI Enters the QAT Era

💬 Today's focus is on OpenAI's internal strategic pivot, as ChatGPT evolves from a chatbot into a super app integrating Agents. On the technical front, Google's Gemma 4 has implemented QAT technology, signaling a new, efficiency-focused era for on-device AI. Meanwhile, AI coding tools are closing the "design-to-development" loop, but their high token consumption is prompting the industry to re-examine the narrative of AI-driven cost reduction.

🔹 📖 In-depth Guide to This Issue's Watch List

Today's Watch List focuses on the capital flows and business model restructuring behind AI giants. We recommend paying close attention to the following two dimensions:

First, the "financialization" trend of top AI labs warrants caution. As the trading volume of unicorns like OpenAI and Anthropic surges in the private secondary market, the valuation logic for top-tier AI assets is entering a "pre-IPO" stage. This private equity boom, pioneered by SpaceX, not only reflects the market's long-term optimism for Artificial General Intelligence (AGI) but also indicates that the AI race has evolved into a high-stakes capital endurance contest.

Second, the new investment guidelines for Agentic AI proposed by Ernst & Young (EY) are a key deep-read for today. The report points out that as AI shifts to a consumption-based business model, the link between corporate spending and valuation is being reshaped. For engineering and financial decision-makers, understanding this paradigm shift from "tool investment" to "value-linked" spending is crucial for evaluating the long-term ROI of AI agents. Additionally, the frequent use of AI hardware like Plaud at liquidity summits further confirms that on-device AI recording and analysis are becoming the new standard for enterprise productivity tools.

🔹 🌐 Quick Takes: AI Hotspots on X

🔸 Topic 1: OpenAI Launches Codex Use Case Gallery for Developers

• Category: AI · News

• Overview: Trending Time:, Related Posts: 112

• What it is: OpenAI has launched the Codex Use Case Gallery, designed to provide developers with concrete examples of the model's application in real-world programming scenarios.

• Why it matters: It lowers the barrier for developers to integrate large language models, showcases the broad potential of code generation models beyond autocompletion, and helps accelerate the growth of the AI-driven software development ecosystem.

• Discussion overview: The discussion centers on the practical reference value of these use cases, their actual contribution to improving development efficiency, and how to leverage these examples to optimize existing programming workflows.

🔸 Topic 2: Developers Weigh Codex vs Claude Code Amid Upgrade Rumors

• Category: AI · News

• Overview: Trending Time: 21 hours ago, Related Posts: 2900

• What it is: The developer community is comparing Anthropic's newly released Claude Code command-line tool with OpenAI's Codex, amidst heated discussions about rumored upgrades for both products.

• Why it matters: Programming assistance is one of the most mature and competitive fields for AI implementation. The technological rivalry between these two giants directly impacts developer workflows and the future standards for AI coding tools.

• Discussion overview: The conversation focuses on whether Claude Code's Agent-like capabilities for handling complex engineering tasks are superior to Copilot's, and speculation about whether OpenAI will soon release Codex 2 or another major update.

🔸 Topic 3: Developers Debate Codex vs Claude Code as Top AI Tools

• Category: AI · News

• Overview: Trending Time: 14 hours ago, Related Posts: 2500

• What it is: Developers are intensely debating whether Codex or Claude Code is currently the top AI programming tool.

• Why it matters: This reflects the evolution of AI coding tools from basic code completion to deep engineering collaboration, with the cost-benefit ratio of these tools becoming a key evaluation metric for the industry.

• Discussion overview: The discussion centers on the trade-off between Codex's excellent cost-effectiveness and Claude Code's superior performance when used with high-end configurations and sufficient quotas.

🔸 Topic 4: Vibe Coding Takes Center Stage with Pi Network Push

• Category: AI · News

• Overview: Trending Time: 23 hours ago, Related Posts: 908

• What it is: The concept of "Vibe Coding" has sparked discussion on X, promoted by Pi Network. This approach advocates for building applications through natural language descriptions and high-level intent rather than writing specific code.

• Why it matters: This trend signals a paradigm shift in AI programming from "assistive tools" to "intent-driven" development, heralding a further reduction in the barrier to entry for software development and a potential exponential increase in efficiency.

• Discussion overview: The debate focuses on whether this development method will lead to decreased code maintainability and whether it represents the future of programming or is merely a "black-box" model suitable only for rapid prototyping.

🔸 Topic 5: Mike Vogel's AI Short 'Mars Landings' Delivers Netflix-Style Sci-Fi Comedy

• Category: AI · Entertainment

• Overview: Trending for: 4 hours ago, Related posts: 254

• What happened: Creator Mike Vogel released "Mars Landings," a sci-fi comedy short film produced using AI technology. Its visual effects and narrative pacing are considered to have reached the production quality of a streaming platform.

• Why it's important: This work showcases the immense potential of AI in generating high-quality film and television content with coherent narratives and humor, signaling the possibility for individual creators to challenge traditional film industry workflows using AI.

• Discussion summary: The discussion focuses on the astonishing advancements in AI video generation, the further lowering of the barrier to content creation, and whether AI can truly master complex comedic timing and cinematic storytelling.

#### AI Public Opinion Summary on X Today

Today's main discourse focuses on the paradigm shift driven by AI in the fields of programming tools and film/television creation. The industry widely recognizes that AI is evolving from a simple auxiliary tool into a core productivity force capable of deep engineering collaboration and high-quality narrative generation. The developer community shows clear divisions in tool selection, mainly reflected in the trade-off between the high cost-effectiveness of Codex and the superior performance of Claude Code. There is also intense debate over whether "ambient programming" is a leap in development efficiency or a "black box" model that sacrifices code maintainability. As AI-generated content reaches streaming-level quality, public opinion, while marveling at technological progress, also harbors underlying concerns about the potential disruption of traditional film industry workflows and the risk of software engineering's fundamental logic spinning out of control due to over-reliance on intent-driven development.

🔹 💡 Influencer Insights

✨ AI Industry Trends Daily (2026-06-07)

🔹 I. Today's Core Hotspots: The Deep Evolution of On-Device Models and AI Programming Tools

🔸 1.1 On-Device Models: Breaking Through the Tipping Point from "Usable" to "Great"

The release of the Google Gemma 4 series has drawn significant attention in the Chinese-speaking community. @zhixianio's hands-on tests indicate that Gemma 4 12B, as an encoderless unified multimodal model, delivers "perfectly OK accuracy and very high speed" for English/Japanese speech recognition when run on an M5 Max 128GB device with MLX-VLM. However, its Chinese performance is "completely off the mark"—this reveals the uneven maturity of on-device models in multilingual scenarios.

More noteworthy is the implementation of the QAT (Quantization-Aware Training) technical route. The QAT version released by Google this time is interpreted by @zhixianio as "assuming from the start of training that it will inevitably be quantized," optimizing post-quantization performance from the source. This creates a generational difference from traditional Post-Training Quantization (PTQ) and could become the new benchmark for the memory efficiency and inference speed of on-device models.

Diversification of hardware platforms is advancing in parallel: an AMD Ryzen AI Halo mini PC forwarded by @zhixianio, and @zhixianio's own "monk-like" experience using Qwen3.6-35B-A3B-oQ6 ("response speed is faster than remote LLMs, and its intelligence is online"), both point to one conclusion: on-device AI has reached a production-ready stage.

💬 **Key Insight**: The competitive focus for on-device models is shifting from "parameter scale" to a three-dimensional game of "quantization efficiency unified multimodality hardware synergy."

---

🔸 1.2 AI Programming Tools: From "Coding Assistance" to a "Design-Development Closed Loop"

The local refactoring of Claude Design is today's most technically profound topic. @dotey, by parsing HAR files and reverse-engineering the Protocol Buffers communication protocol, successfully migrated Claude Design to a local Cursor environment, achieving a complete closed loop of "describe interface → generate HTML → modify with element-level annotations."

The significance of this work lies in:

• **Breaking platform lock-in**: Claude Design is native to Claude Desktop; @dotey's Skill solution (`JimLiu/baoyu-design`) allows it to call Opus 4.8 within Cursor.

• **Integrated design and development**: The generated HTML/CSS/React/data.js can be directly committed to git version control, allowing the AI to perceive design changes via `git diff`.

@vista8's subjective ranking of front-end aesthetics, presented during a livestream, sparked discussion: `Claude opus 4.8 > kimi2.6 > GPT 5.5 > Deepseek v4 pro > GLM 5.1 > deepseek v4 flash`. It's noteworthy that @dotey's hands-on tests confirmed GPT-5.5 has "all sorts of issues with UI implementation details and fails to adhere well to the design draft," while Opus 4.8 performs significantly better.

OpenAI's product strategy shift has surfaced: @dotey, citing a Financial Times report, reveals that a senior executive inside OpenAI bluntly stated, "Chat is dead." ChatGPT is being restructured from a "chatbot" into a "super app"—integrating Codex, AI Agents, image generation, and third-party applications (like Canva, Booking, etc.). The business driver for this redesign is clear: to guide users from low-profit free chat to high-profit enterprise tools, telling a good "platformization" story before its IPO.

---

🔸 1.3 New Explorations in Agent Collaboration and Memory Mechanisms

@Pluvio9yte's in-depth experience with Helio demonstrates a collaboration paradigm of "AI colleagues" rather than "AI tools":

• 4 AI Agents (Researcher, Copywriter, Tech Lead, Product Manager) have independent email addresses and identity profiles.

• **Autonomous collaboration between Agents**: After the Researcher outputs a brief, the Copywriter proactively corrects it ("The dollar sign is missing from the second data point"), and the Researcher immediately fixes it and updates the Memory rules.

• **Dream mechanism**: Automatically reviews conversations late each night to distill work standards.

This resonates with the "Book of Shadows" reading method proposed by @lijigang—the core capability in the AI era is shifting from "acquiring information" to "leveraging AI to analyze the multidimensional connections within information."

---

🔹 2. Unique Perspectives and Industry Foresight

🔸 2.1 The "Specialization" Dilemma in Model Capabilities

@vista8 raises a sharp question: Why are the writing abilities of Claude 4.8 and GPT 5.5 inferior to the Claude 4.6 series? The speculation points to a training data skew after going "All in on Coding"—when model developers concentrate resources on coding capabilities, general writing skills may degrade. This reveals the challenge of capability trade-offs in multi-task training.

@Pluvio9yte's practical tests provide evidence: GPT-5.5 produces self-contradictory code that "trips over itself" in iterative optimization scenarios ("iterations after MVP"), raising concerns about the model's ability to maintain long-range consistency.

🔸 2.2 Cost Restructuring: Is AI Programming More Expensive Than Human Programmers?

@ruanyf's calculation has sparked industry reflection: The founder of OpenClaw consumes 603 billion Tokens per month (an estimated value of $1.3 million USD). Even when switching to domestic open-source models (priced at 1/30th to 1/50th of foreign flagships), the annual cost still reaches 2-3 million RMB. This data challenges the simple narrative that "replacing programmers with AI = cost reduction" and highlights the trap of scale effects in the Token economy.

🔸 2.3 A New Paradigm for Skill Encapsulation

@lijigang proposes a direction for the evolution of Skills: a "browser extension mechanism" could be a viable solution for skill package encapsulation—it's easy to distribute and can be commercialized. This aligns with the Feishu open-source CLI toolkit mentioned by @ruanyf (which gained over 10,000 stars in 40 days), suggesting that competition for platform-level Agent infrastructure is heating up.

---

🔹 3. Recommended Tools and Resources

| Category | Tool/Resource | Source | Core Scenario |

|:---|:---|:---|:---|

| On-device Model Execution | mlx-vlm Gemma 4 QAT | @zhixianio | Local multimodal inference on Mac |

| AI Design-to-Development Loop | Cursor Design Skill (`JimLiu/baoyu-design`) | @dotey | Run Claude Design workflow locally |

| Agent Collaboration Platform | Helio | @Pluvio9yte | Multi-Agent autonomous collaboration and memory persistence |

| Knowledge Management | OpenWiki | @AI_Jasonyu | Auto-fetch → AI organize → Knowledge graph generation |

| Bluetooth Hardware Management | Perculia | @vista8 | One-click Bluetooth device switching from the Mac menu bar |

| Rapid Mac App Development | Glaze | @vista8 | Generate and publish a Mac App from a single sentence |

| Codex Workflow Optimization | Goal Instruction Six-Element Template | @vista8 | Structurally define Agent task boundaries |

| Feishu Office Automation | Feishu open-source CLI toolkit | @ruanyf | Agent invokes office platform capabilities |

---

🔹 4. Key Trend Summary

```

端侧化 × 平台化 × 协作化

↑ ↑ ↑

硬件 产品形态 组织方式

效率 重构 变革

```

Short-term (3-6 months): QAT-like quantization techniques will become standard for on-device models; the design-to-development loop for AI programming tools will mature.

Mid-term (6-12 months): Autonomous collaboration mechanisms between Agents will move from demo to production; the "specialization" issue in model capabilities will force adjustments in training strategies.

Long-term (12 months): "AI colleagues" will restructure team organizational forms; the Token cost structure will reshape the business models of the software industry.

🔹 📚 Appendix: Today's Watch List Update Source List

💬 Time window: Last 3 days; 22 sources covered; 1 update in total.

🔸 All-In Podcast (A_full)

• **[Inside the Private Stock Market Boom: SpaceX, Anthropic, OpenAI & the Rise of Secondaries](allinchamathjason.libsyn.com…)**

- Published: 2026-06-08 02:14 Beijing Time

- Summary:

- EY - Agentic AI is introducing new investment rules.

- As AI shifts to consumption-based models, EY links spending to enterprise value.

- NYSE - Thanks to our partner NYSE - a modern market and exchange dedicated to building the future.

- Plaud, our official wearable AI note-taking partner at the All-In Liquidity Summit, captured every insight.

- Inside the Private Stock Market Boom: SpaceX, Anthropic, OpenAI & the Rise of Secondaries.

- EN Highlights:

- (0:00) Brad Gerstner, Gavin Baker, and Kelly Rodriques join the Besties

- (0:47) Secondary Markets are Booming & Competing with IPOs

- (3:10) Why Companies are Staying Private So Long

- (9:22) SPVs, the Forge-Schwab Deal, Democratizing Private Market Access

🔗 Full Article: miaok.ong/en/ai-daily/ai-dai…

3

4

1,731

Palo Alto Networks Inc ($PANW) is aggressively transforming the cybersecurity landscape through a powerful platformization strategy that consolidates fragmented tools into a single, AI-driven architecture. Fueling its massive expansion is the recent landmark acquisition of CyberArk, which perfectly positions the enterprise to dominate the rapidly growing identity security market. While heavy integration costs have caused temporary GAAP net losses, the firm's organic subscription revenue and towering free cash flow margins highlight a highly resilient financial profile. Trading at a premium valuation multiple, the stock's future performance hinges on its ability to seamlessly integrate these massive assets and capitalize on booming AI datacenter demand. Will this bold consolidation strategy secure its reign as the undisputed leader of the cybersecurity sector, or are the execution risks simply too high?

1

73

Jun 7

This timing is critical. With OpenAI merging browser Codex ChatGPT, we're seeing the platformization of agentic AI. The question: will this be more frictionless for enterprise adoption, or will it create vendor lock-in that slows innovation?

24

Security complexity is a real risk.

In this article, Brijesh Balakrishnan, Infosys, explains how point solutions have led to fragmented, slow security stacks — and why platformization matters.

Read: shortner.infy.com/srQMX

#InfosysCyberSecurity

2

5

471

Our CEO @nikesharora joined @jimcramer on @MadMoneyOnCNBC to break down our record Q3 results.

As AI-driven threats accelerate, the strategy is clear: drive platformization and fight AI with precision AI.

Watch the full segment.

2

8

757