May 6

$STEM Q1 2026 earnings: Profitability Pivot Works, But Software Growth Stalls

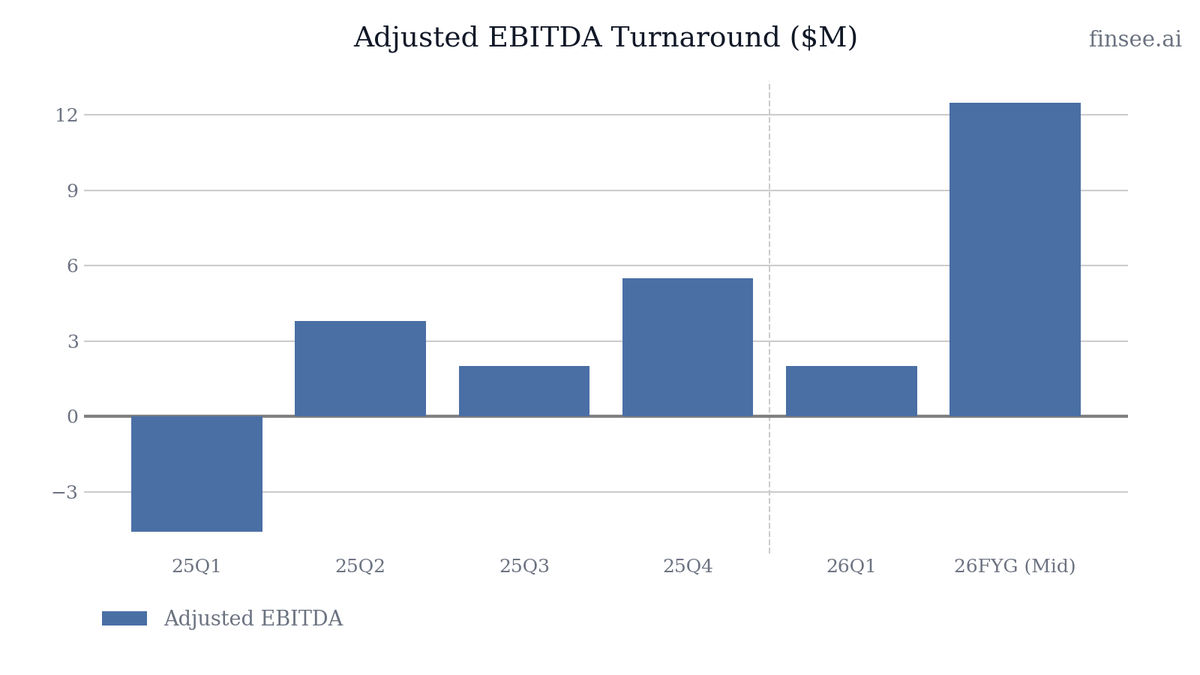

Stem's strategic pivot away from low-margin hardware to a software-centric model continues to yield major profitability improvements. While total revenue decelerated, falling 11% YoY to $29.0 million, this was an intentional byproduct of eliminating hardware resale. The true story is margin expansion: non-GAAP gross margin reached a record 52%, driving a fourth consecutive quarter of positive Adjusted EBITDA ($2.0M). However, the underlying software growth engine is showing signs of fatigue. Annual Recurring Revenue (ARR) was completely flat sequentially at $61.2M, and Managed Services ARR actually shrank. The company reaffirmed its FY26 guidance, implying a steep back-half weighted acceleration in software sales that carries significant execution risk.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 — The intentional wind-down of the low-margin hardware business is fully visible. Non-GAAP gross margins accelerated to 52%, up from 46% a year ago, permanently shifting the company's profitability profile.

• 𝐂𝐨𝐧𝐬𝐢𝐬𝐭𝐞𝐧𝐭 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 — Stem delivered its fourth consecutive quarter of positive Adjusted EBITDA, proving that the aggressive 2025 cost-cutting and workforce reductions are durable.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐨𝐟𝐭𝐰𝐚𝐫𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐢𝐬 𝐒𝐭𝐚𝐥𝐥𝐢𝐧𝐠 — Software, services, and edge hardware revenue grew only 4% YoY to $29.0M, a sharp deceleration from the 25% YoY growth seen in FY25. ARR growth was sequentially flat.

• 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 𝐑𝐞𝐭𝐮𝐫𝐧𝐬 — After generating positive Operating Cash Flow in the second half of 2025, cash flow reversed to negative $8.3M in Q1, eroding the cash balance to $36.6M.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The operational discipline is commendable, and margins are excellent. However, a software company trading at premium multiples needs aggressive ARR growth. A sequentially flat ARR quarter paired with a return to cash burn makes the reiterated FY26 guidance look highly ambitious.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐑𝐞𝐜𝐨𝐫𝐝 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐯𝐢𝐚 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐌𝐢𝐱

Accelerating. The transition away from battery hardware resale is doing exactly what it was designed to do: inflate margins. GAAP gross margin expanded from 32% in 25Q1 to 38% in 26Q1, while non-GAAP gross margin surged to 52%. By shedding empty-calorie hardware revenue, Stem's gross profit dollars actually grew YoY despite the 11% drop in total sales.

🔴 𝐀𝐑𝐑 𝐒𝐭𝐚𝐠𝐧𝐚𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐌𝐚𝐧𝐚𝐠𝐞𝐝 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 𝐃𝐞𝐜𝐥𝐢𝐧𝐞 [NEW]

Decelerating. Total ARR landed at $61.2 million, virtually unchanged from $61.1 million in Q4 2025. More concerning is the underlying mix: Managed Services ARR reversed, dropping 4% sequentially from $20.4M to $19.5M. For a company banking its future on recurring software and services revenue, flat sequential ARR growth in Q1 creates a steep hill to climb to hit the $65-$70M year-end target.

🟢 𝐌&𝐀 𝐚𝐧𝐝 𝐏𝐚𝐫𝐭𝐧𝐞𝐫𝐬𝐡𝐢𝐩𝐬 𝐭𝐨 𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐭𝐡𝐞 𝐒𝐭𝐚𝐜𝐤 [NEW]

Stem is actively augmenting the PowerTrack platform. The April acquisition of Vienna-based raicoon GmbH brings automated fault detection into the fold, which should accelerate issue resolution for solar assets. Concurrently, a co-marketing agreement with Nuvation Energy creates a fully North American-made BESS control stack, strategically positioning Stem to win bids where domestic sourcing and security are mandated.

🔴 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐑𝐞𝐯𝐞𝐫𝐬𝐞𝐬 𝐢𝐧𝐭𝐨 𝐍𝐞𝐠𝐚𝐭𝐢𝐯𝐞 𝐓𝐞𝐫𝐫𝐢𝐭𝐨𝐫𝐲

Reversing. Operating cash flow swung to an $8.3M outflow, compared to an $8.5M inflow in 25Q1 and an $8.2M inflow in 25Q4. While H1 seasonality is typical, the company ended Q1 with only $36.6M in cash and equivalents (down from $48.9M in Q4 2025). Achieving the FY26 guidance of $0-$10M in positive OCF will require near-perfect working capital execution in the back half of the year.

🔴 𝐌𝐚𝐜𝐫𝐨 𝐔𝐧𝐜𝐞𝐫𝐭𝐚𝐢𝐧𝐭𝐲 𝐋𝐨𝐨𝐦𝐬 𝐎𝐯𝐞𝐫 𝐭𝐡𝐞 𝐒𝐮𝐩𝐩𝐥𝐲 𝐂𝐡𝐚𝐢𝐧

Management continues to flag macroeconomic and geopolitical risks, including global inflationary pressures, interest rates, and the uncertainty surrounding the 'One Big Beautiful Bill' (OBBB) and import tariffs. While Stem's software is largely insulated from direct tariffs, its customers' hardware installations are not. Delays in site commissioning directly delay Stem's ability to recognize software revenue and AUM growth.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐞𝐝 𝐁𝐚𝐜𝐤𝐥𝐨𝐠: $23.0 million

Accelerating sequentially. Up from $21.3 million at the end of 25Q4. Stem added $15.0 million in bookings during Q1, offsetting $10.6 million in hardware revenue and $2.3 million in project services converted during the quarter.

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐀𝐬𝐬𝐞𝐭𝐬 𝐔𝐧𝐝𝐞𝐫 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 (𝐀𝐔𝐌): Solar: 37.5 GW | Storage: 1.7 GWh

Stable. Solar AUM grew 4% sequentially to 37.5 GW, proving steady adoption of PowerTrack for solar monitoring. Storage AUM was completely flat sequentially at 1.7 GWh, aligning with the stagnant ARR figures.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $140 - $190 million

Stable. Management reaffirmed full-year guidance. With Q1 delivering only $29.0M, Stem needs to average over $45M per quarter for the rest of the year to hit the $165M midpoint. This implies an expectation of severe back-half acceleration.

𝐅𝐘𝟐𝟔 𝐒𝐨𝐟𝐭𝐰𝐚𝐫𝐞, 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 & 𝐄𝐝𝐠𝐞 𝐇𝐚𝐫𝐝𝐰𝐚𝐫𝐞 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $130 - $150 million

Stable. At the $140M midpoint, this represents flat growth compared to the $141.4M delivered in FY25. Given the 4% YoY growth in Q1, this target appears achievable but underscores the lack of top-line hyper-growth.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $10 - $15 million

Stable. Reaffirmed guidance implies a significant acceleration from FY25's $6.7M. With $2.0M generated in Q1, Stem is on pace but requires volume leverage in Q3 and Q4 to clear the midpoint.

𝐅𝐘𝟐𝟔 𝐘𝐞𝐚𝐫-𝐄𝐧𝐝 𝐀𝐑𝐑: $65 - $70 million

Stable. Hitting the $67.5M midpoint requires adding $6.3M in net new ARR over the next three quarters. Given that Q1 added roughly zero sequential ARR, this metric demands aggressive acceleration.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐌𝐚𝐧𝐚𝐠𝐞𝐝 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐨𝐧

Managed services ARR declined 4% sequentially to $19.5 million. Was this driven by customer churn, proactive contract pruning, or a slowdown in brownfield site conversions?

𝐏𝐚𝐭𝐡 𝐭𝐨 𝐭𝐡𝐞 𝐀𝐑𝐑 𝐓𝐚𝐫𝐠𝐞𝐭

With Q1 ARR essentially flat sequentially, what specific product lines or geographic regions give you the visibility to confidently reiterate the $65-$70 million year-end ARR target?

𝐫𝐚𝐢𝐜𝐨𝐨𝐧 𝐌𝐨𝐧𝐞𝐭𝐢𝐳𝐚𝐭𝐢𝐨𝐧

Regarding the raicoon software acquisition, is this technology being integrated as a standard feature of PowerTrack, or will it be monetized as a premium add-on to drive ARPU expansion?

𝐇𝐚𝐫𝐝𝐰𝐚𝐫𝐞 𝐑𝐞𝐬𝐚𝐥𝐞 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲

Guidance still allows for up to $40 million in battery hardware resale this year, yet Q1 saw significantly reduced hardware sales. Do you expect this to be highly concentrated in a single quarter, and how will it impact gross margins in that specific period?

1

2

1,141

Mar 25

$STEM | The $1.5 billion accumulated deficit is the only number the bears want to talk about, but the 45-minute technical tape is currently telling a far more profitable story. While retail is still waiting for a "moon shot" based on legacy hardware hype, the smart money is quietly accumulating the SaaS pivot. With 2025 delivering the first-ever positive Adjusted EBITDA ($7M) and a massive 100 MWh software win in Germany, Stem is effectively transforming from a distressed industrial firm into a high-margin AI infrastructure play.

The objective data on the chart is surgical. Our REVERSAL PRO indicator has officially triggered a BULLISH trend. After successfully building a double-bottom at the $9.55 and $9.96 structural nodes, price has just reclaimed the $10.37 resistance. At $10.54, we are now in a technical "launch zone" where the path of least resistance leads directly to the $11.12 reversal node.

The "SaaS or Bust" Reality

The Bull Case: This isn't your 2024 Stem. Management has aggressively slashed hardware resales (now down to 43% of revenue) to prioritize the Athena AI platform and PowerTrack EMS. With 2026 software margins targeted at 40%-50% and $61M in ARR, the valuation framework is shifting from a 0.8x P/S industrial multiple toward a 3x-4x SaaS multiple.

The Bear Case: Execution risk remains extreme. Despite the $138M paper profit in 2025, the market is ruthlessly pricing in the cash burn required to scale the international software hub. Chasing the $11.12 resistance without a confirmed back-test is how retail traders become the exit liquidity for institutional "scalpers."

Technical Roadmap: The momentum oscillator in the top pane has successfully exited the "liquidity drain" and is printing a bullish impulse. If the $10.37 level holds as the new structural floor, the mathematical target shifts toward the macro $12.86 reversal node.

The Strategic Play

Are you still bag-holding from the $30 IPO mania or looking to tactical play this AI-energy reversal? "Hope" is not a strategy when trading a high-beta SaaS pivot. You need to identify the exact institutional "order blocks" and the real-time invalidation levels to survive the volatility of the software ramp.

For my detailed execution roadmap and the specific price triggers I am tracking for $STEM, connect with me via the WhatsApp link in my bio.

#STEM #CleanEnergy #AI #TradingStrategy

2

182

$STEM - Stem’s PowerTrack™ EMS Selected for 100 MWh of Utility-Scale Energy Storage Projects in Germany .

2

709

Feb 15

Every throne casts a shadow… but only one man knows how to rule from inside it.

My new track Shadow on the Throne is live. Based on my debut novel The Scion.

🔗 suno.com/s/jfZL8w2DZT83N8b5

#RebelEnergy #AntiHeroVibes #PowerTrack

1

4

31

Happy Republic Day, India!

Warm wishes to our Powertrack family, valued clients, trusted partners, and everyone across India.

Let’s celebrate unity, progress, and the spirit that drives a stronger future.

#PowertrackAfrica

#RepublicDay #RepublicDayIndia #TeamPowertrack #India

2

38

再生可能エネルギーの成長を裏で支える黒子、STEMがAIで躍進しつつある。太陽と風という不安定な電源が主役になる時代、電力網は新たな頭脳を必要としている。

BloombergNEFも示す巨大成長市場で、STEMは「蓄電池のAI」として生き残れるのか?

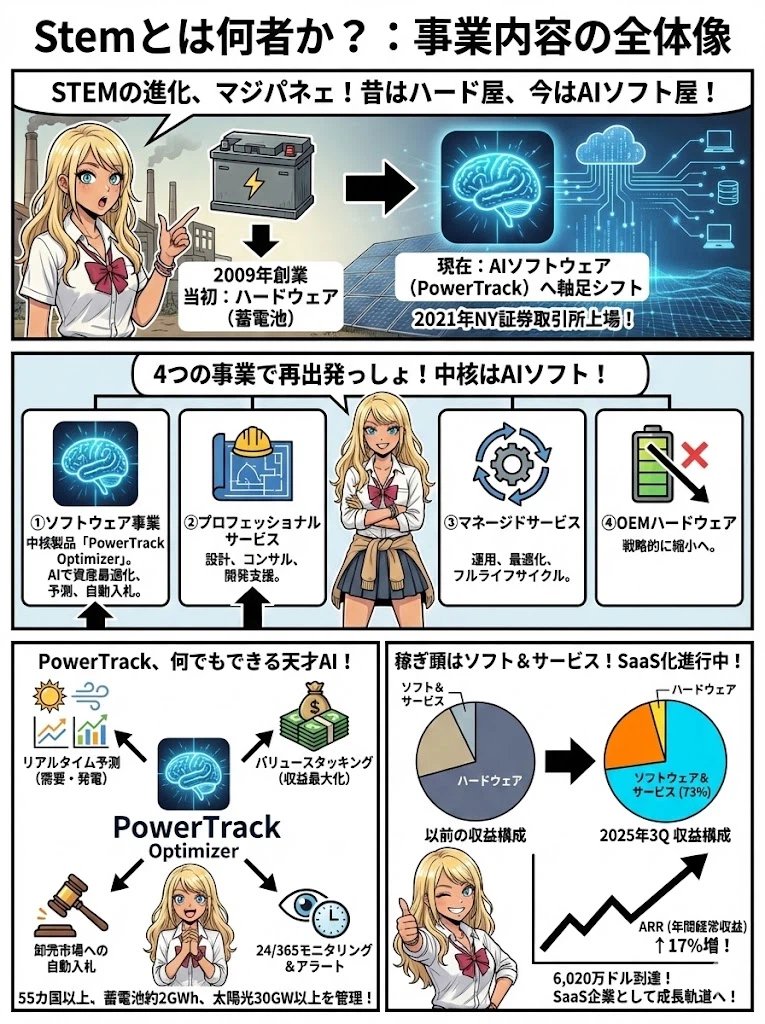

STEMのビジネスはただの蓄電池企業ではない。

再エネの最大の弱点である間欠性を、AIソフトウェアで制御し価値に変える点にある。太陽光は夜に止まり、風力は風任せだ。この不確実性が増すほど、最適化ソフトの価値は指数関数的に高まる構造である。

一方でSTEMの株価推移は極端だ。

2021年にSPAC上場時13億ドル超と評価されたが、その後は赤字継続で暴落。2025年には1対20の株式併合を実施し、時価総額は約1.7億ドルのマイクロキャップに転落した。市場は期待と失望を同時に織り込んでいる。

現在のSTEMは4事業体制へ再編されている。中核はAIによる電力資産最適化ソフト「PowerTrack」である。世界55カ国以上、蓄電池約2GWh、太陽光30GW超を管理し、発電予測、卸市場入札、制約管理を24時間自動で行う点が強みだ。

注目すべきは収益構造の変化である。

2025年Q3時点で売上の約73%がソフトウェアとサービスとなり、ハードウェア依存から脱却が進んだ。ARRは前年比17%増の6,020万ドルに到達し、SaaS型ビジネスとしての輪郭が明確になりつつある。

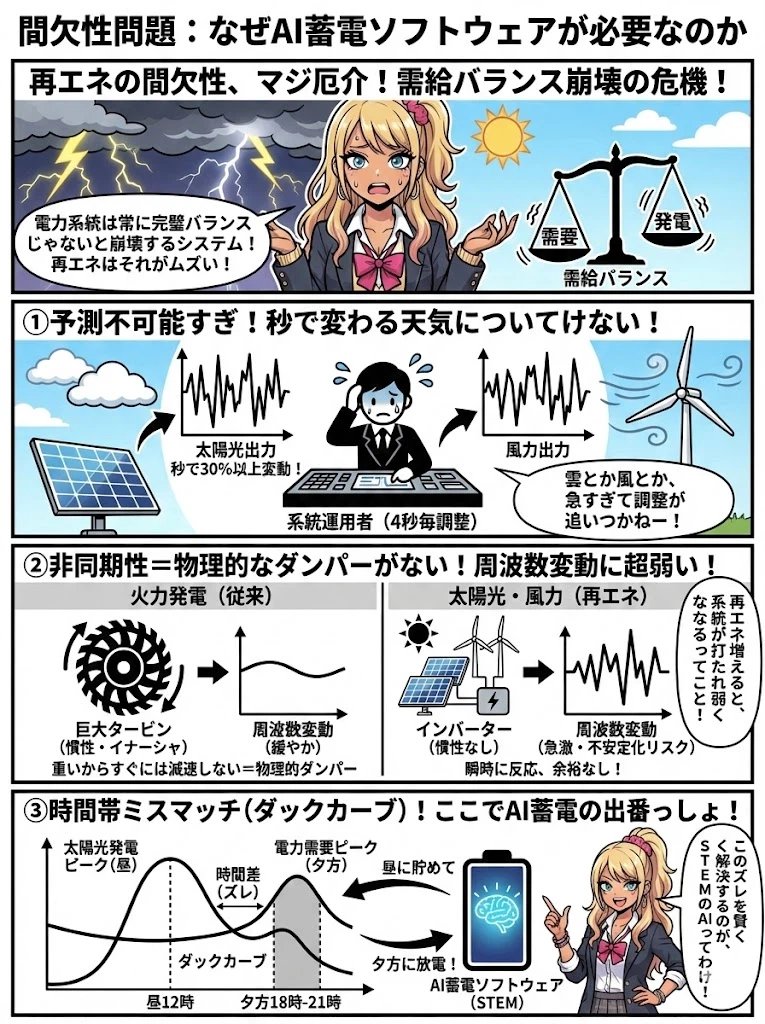

STEMの存在価値を理解する鍵が「間欠性問題」である。電力系統は需給が崩れれば即座に不安定化するが、再エネは出力が秒単位で変動する。従来の火力が持つ物理的慣性がないため、再エネ比率が高まるほど制御は困難になる。

この課題を象徴するのがカリフォルニアのダックカーブだ。昼は太陽光過剰、夕方は急激な電力不足が発生する。2024年、蓄電池が夕方ピークの最大電源となったことで、再エネ+蓄電池が解決策になり得ると実証された。この制御を担うのがAIである。

蓄電池はただの貯蔵装置ではなく、収益を生む資産である。電力価格差、需給調整、容量市場、系統安定化など複数の価値を同時に最大化する「バリュースタッキング」が必要だ。人間の判断では不可能な最適化を、PowerTrackはAIで実行する。

しかしリスクも大きい。

STEMは依然として赤字体質で、資金調達環境が悪化すれば事業継続リスクが高まる。また競合も増加しており、大手電力ITや他のエネルギーソフト企業との競争は激しい。技術優位を収益に転換できるかが最大の分岐点だ。

STEMは「再エネ時代のインフラAI」という巨大テーマを握る一方、財務的には崖っぷちに立つ企業である。成功すれば化けるが、失敗すれば消える。その両極端な可能性こそが投資家を惹きつける理由だ。この構造を理解することが判断の出発点となる。

続きはnoteを読んでください。

note.com/koziii/n/n1ddfaf24c…

1

1

23

8,467

27 Dec 2025

Think power? Think ruling the track?

Max Verstappen 🤝 Boomeroo Power Track with LED

#Goldmedal #GoldmedalIndia #GoldmedalElectricals #SwitchToTheAmazing #Formula1 #MaxVerstappen #F1 #PowerTrack #SmartHome #Sockets

1

2

309

23 Dec 2025

All I ever wanted for Christmas was a giant Scalextric. The closest I got was a set called PowerTrack.

What’s on your all time Christmas wish list?

3

9

621

6 Dec 2025

Bring your charger towards you so effortlessly with Boomeroo power track that your mom also says,

Waah Shampy Waah!!!

#Goldmedal #GoldmedalIndia #SwitchToTheAmazing #GoldmedalElectrical #Sockets #PowerTrack #Charging

1

1

84

12 Nov 2025

Emmvee Photovoltaic Power Limited IPO

Final Verdict

Evaluate For Medium Term

Highlights of the Issue :

Date : 11-13 November

Price Band : 206-217

Size : 2,900 Crore

Fresh - 2,144 Crore

OFS - 756 Crore

M.cap : 15,024 Crore

Objects Of The Issue :

▪︎ Repayment Of Debt - 1,621 Cr

▪︎ GCP - 523 Cr

Key Pointers :

▪︎ Emmvee is India's 2nd Largest Pure-play Integrated Solar Module and Cell Manufacturer; It's Solar Module Capacities stands at 7.80 GW and Cell Capacity stands at 2.94 GW

▪︎ The Company is in the Process of adding 2.5 GW Topcon Solar Module Capacity in FY26 and An Integrated 6 GW Solar Module and Cell Facility in H1 FY28

▪︎ Emmvee is one of the very few Players with Cell Capacity of Topcon Technology of 2.9 GW; Only 3rd after Waaree Energies (4 GW) and Adani Solar (2 GW) and 2nd Largest just behind Waaree Energies

▪︎ Emmvee's Customers Include Ayana Renewables, Clean Max Enviro Energy, Hero Energies, Prozeal Green, KPI Green, Aditya Birla Renewables, Blupine Energy, Lineage Power, BN Peak Power-I, KMV Projects, Powertrack Packaging, SILRES Energy, Kintch Synergy, Zodiac Energy, E Ramamurthy Minerals and Metals, InSolare Energy, Universal Transformers and

Mars Energy Group, Inc. Etc.

▪︎ The Company has an Orderbook of 5.36 GW which Translates around ~7,500 Cr Revenues indicating strong Revenue Visibility

▪︎ The Company is aiming to Deleverage its Balance sheet Leading to saving of interest Costs substantially (It will raise further debt from IREDA for the 6 GW Integrated Facility Capex)

Financials and Personal Assumptions :

FY23

Revenue : 644.4 Crore

PAT : 6.9 Crore

FY24

Revenue : 954.4 Crore

PAT : 28.9 Crore

FY25

Revenue : 2,360.3 Crore

PAT : 369 Crore

Q1 FY26

Revenue : 1,042.2 Crore

PAT : 183.7 Crore

FY26E

Revenue : 5,600 Crore

PAT : 930 Crore

FY27E

Revenue : 8,650 Crore

PAT : 1,250 Crore

Valuing Emmvee at 15× FY27E PAT, Fair Value Comes At 271, Implying An Upside Of 25%

(FY26 Assumption : 7.8 GW Capacity Utilization at 50% blended with 1,450/ MW realization due to Topcon quality and better realization;

Q1 had 5.2 GW, Q2 partial use of Capex and H2 will have full effect of new Capex Hence, the blended Utilization assumed at 50%)

(FY27 Assumption : 10.3 GW Capacity at 60-65% Utilization with realization of 1,350; Assuming the abundance supply of modules in FY27 taking a 10% hit in realizations)

*Have put in Assumptions so that the viewers can understand the thesis

Fundamentally Emmvee stands just behind Waaree and ahead of Premier in terms of current capacity and Topcon Cell giving an upper edge

Waaree trading at ~25×FY27E

Premier trading at ~24×FY27E

We have valued Emmvee at 15× FY27E due to reasons like;

▪︎ Sectoral De-rating (Started Already from last 2 quarters)

▪︎ Supply Matching the demand In H2 FY28*

▪︎ Waaree and Premier trying hard to go beyond Solar Module/ Cell to Other High Growth Elements in the Power Space

▪︎ Emmvee being rigid to only Modules and Cells (At this point)

▪︎ Waaree and Premier are mostly Completed/ Completing Backward integration (Aluminum Frames, EPE encapsulant, Copper Ribbons, Junction Box and Silicone Sealants) whereas Emmvee is yet to start in this backward integration

Overall A Good Quality Company From a Good Space with high Growth with Good Management at Reasonable Valuations

The Anchor Book was Impressive and the Company and the Bankers have kept some scope on the Table for Investors

Just A Personal View, Only For Educational Purposes

17

8

269

52,243

27 Oct 2025

This image perfectly illustrates the "New Stem" strategy. It's no longer just about hardware. The company has built an end-to-end energy intelligence platform designed to create a sticky customer ecosystem. $STEM

The strategy is to lead with consultative professional services and the core powerTrack software for asset monitoring. From there, they can upsell high-margin, AI-powered managed services, which are powered by the powertrack pptimizer. This allows them to manage the entire project lifecycle for solar, storage, and hybrid assets.

Hardware is now just one component of a complete solution, offered only when it's profitable and bundled with their high-value software and services. This integrated approach is the engine of their entire pivot to a recurring-revenue, software-centric business model.

3

7

2,008

19 Oct 2025

1/2 Swing Trade: $STEM A Bet on the AI Energy Intelligence Pivot

My trading thesis in $STEM is centered on the market's early recognition of a high-risk, high-reward turnaround story. The company is in the midst of a strategic pivot from a capital-intensive, low-margin hardware reseller to a high-margin, AI-driven software provider, and recent results suggest the execution is gaining traction faster than consensus expectations.

This transformation is underpinned by a decisive shift away from hardware resales toward the high-margin PowerTrack software and services suite. This move was validated by the Q2 2025 results, which showed a significant expansion in GAAP gross margin to 33% and, for the first time in company history, positive adjusted EBITDA. This financial inflection point was further de-risked by a crucial debt exchange in June that reduced outstanding debt by nearly $200 million, extending the company's operational runway.

The most critical upcoming catalyst is the Q3 2025 earnings report, scheduled for 10/29. This will be the first full quarter reflecting the new strategy's impact. Continued strength in ARR growth, sustained high gross margins, and a clear path toward positive operating cash flow will serve as the ultimate proof points that the turnaround is succeeding and that the business model is fundamentally changing.

This trade is designed to capture the market's re-rating of $STEM as it transitions from a financially distressed hardware company into a profitable, scalable SaaS leader in the high-growth energy intelligence sector.

Part 2 covers the chart and where we will be buying

$FLNC $NRGV $ENPH

2

5

1,621

3 Oct 2025

Quelle expérience incroyable ! 🌟

Le Marathon de Ville Powertrack 2025 a rassemblé notre équipe, nos familles et notre communauté dans une véritable célébration de la santé, de l’unité et de l’endurance.

#PowertrackAfrique #EspritdÉquipe #Marathon2025 #FamillePowertrack

1

2

21

14 Sep 2025

From racing then to powering now - here’s a track you’ll never outgrow. ⚡

The Boomeroo Power Track allows you to add, remove or reposition sockets as per your need - making powering devices super convenient and cool.

#Goldmedal #GoldmedalIndia #SwitchToTheAmazing #GoldmedalElectrical #Sockets #PowerTrack #Charging

1

2

231

8 Sep 2025

avec les solutions de Fuel Monitoring de Powertrack Africa, chaque goutte compte et chaque dollar est préservé.

👉 Prêt à transformer les pertes en économies ? Discutons-en.

wwww.powertrackafrica.com

#PowertrackAfrica #Fleet #DRCongo #FleetMonitoring #FleetManagement #FuelSavings

1

4

30

6 Sep 2025

From Athena to PowerTrack: can Stem’s bold rebrand convince investors its SaaS pivot is working? business-news-today.com/from… #Stem #PowerTrackOptimizer #EnergyTransition #CleanEnergy #SaaS

1

3

27