Jorge Rodríguez retweeted

4 Jul 2025

I hope Ahmonza gets free sometime to draw a third character from DISMALIA, because both his Bosco and Praetoria are one of the best they've looked.

3

4

165

May 23

It will be the Praeto principle, of the people will be doing all the work

3

36

Jan 19

Cult: $ASSDAQ

Community doesn’t sleep, just ask praeto lol, the diamond hands holding on to many assets.

6

101

Jan 2

3

1

14

218

18 Dec 2025

$Boreo new CEO puts skin in the game

Incoming CEO Tuomas Kahri bought 22,000 shares (~300 k€) from major shareholder Praeto Capital, which owns ~70% of the company.

Management alignment matters, especially when the investment is made with personal capital rather than options or RSU.

I do not expect material strategic shifts under the new leadership. More likely, there is a temporary pause in M&A activity during the transition.

The key variable / trigger for 2026 is a potential recovery in Finnish construction and industrial demand, where $Boreo has meaningful exposure.

If the cycle turns, it would support the strategic agenda: higher profitability, improved ROCE, and renewed growth. I expect updated strategic targets in 2026.

11 Aug 2025

Reflections:

Positive:

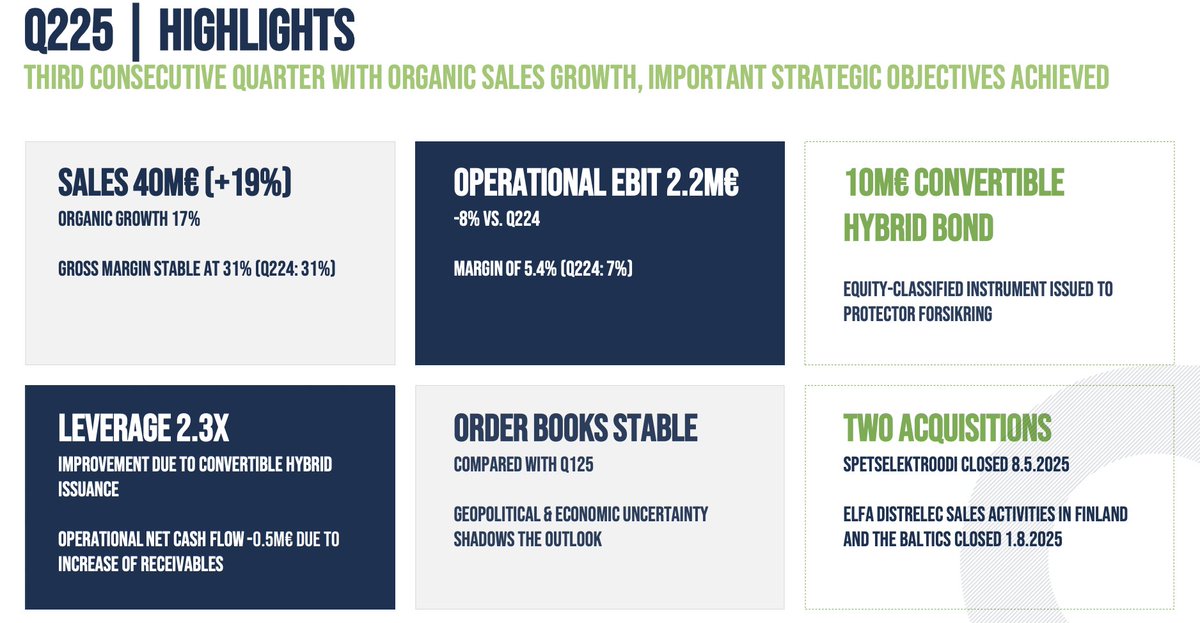

- Sales: 40.2 M€ ( 19% & organic 17%) - continuation of the positive sales momentum turnaround

- Back with the M&A transactions - two acquisitions during Q2

- 10 M€ convertible hybrid bond - leverage down to healthier (still high) 2.3x

Negative:

- 3.5 M€ increase in working capital - mainly due to increased sales at the end of Q2

- Operational EBIT %: 5.4% (7.0%) - increased fixed costs and a higher impact from earn-out provision releases

IMO, $BOREO delivered a solid result with a third consecutive quarter of revenue growth after a rough operational period without acquisitions. Now the growth will be supported by recent acquisitions, including Elfa Distrelec in Finland and the Baltics, and Spetselektroodi AS in Estonia, which further diversify and strengthen the Group’s revenue base. Additionally, the successful issuance of a 10 M€ convertible hybrid bond has strengthened the balance sheet and improved leverage (from 3.1x to 2.3x – excluding hybrid bonds), positioning $BOREO for future acquisitions aligned with its strategic M&A criteria.

Despite solid top-line momentum, operational profitability remains under pressure. Operational EBIT declined by 8% to 2.2 M€, primarily due to increased fixed costs and lower earn-out provision releases compared to the previous year. The gross margin remained stable at approximately 31%, indicating resilient core business operations. The order books have stayed stable since Q1 2025, without clear signs of accelerated growth. Working capital increased by 3.5 M€ organically due to higher receivables linked to strong sales late in the quarter.

While $BOREO is still far from achieving its key financial targets of 15% annual operating EBIT growth and a minimum ROCE of 15%, the recent progress in revenue growth, financing, and operational improvements set a positive foundation for continued advancement. The current valuation of EV/EBIT 10.3 (LTM) is, IMO, providing an attractive price considering the current positive trend. However, it’s valuable to consider the current (lack of) quality of the business – ROCE 8.4%, which is far below quality peers, e.g., from Sweden which have ROCE / ROIC in the mid to high teens.

8

2,828

30 Nov 2025

This was never my first account but for sure my main. Born and live in the UK, 8 username changes all to do with my name Praeto.

Real person, not hiding pretending to be someone I'm not like many KOLs within CT.

DCA $ASSDAQ and come believe with me, join our community, understand the message and teach. Show up, be positive and preach.

You have the power to make a difference, question is if you're willing instead of just waiting.

1

6

254

3 Oct 2025

You want a gem tmas?

This is PRAETO over at $Assdaq Capital. What I’ve got here is time sensitive and I wanted to make sure you personally had a shot at it.

Now you’ve heard of Nasdaq right? The crown jewel of Wall Street. Well what I’ve got here is the ASSDAQ, a brand new, community powered movement asset that’s been taking the Solana ecosystem by storm. This isn’t some backyard project tmas, this is the people’s exchange, flipping Trad-Fi on its head.

Right now, we’re sitting at the absolute ground floor of this run. I’m talking about an opportunity where the upside isn’t 20%, isn’t 200%, it’s life changing. This thing has conviction, it has momentum, and the community behind it has the kind of high octane energy you cannot ignore.

Now here’s the deal I’m not asking you to mortgage the house tmas. Let’s start you small, let’s get your feet wet. I’ll put you in for a position of, say, 5,000,000 ASSDAQ that way when this thing rips, and believe me, it’s going to rip, you’re not kicking yourself for sitting on the side lines watching everyone else’s portfolios do backflips while you’re left wondering what if. So, let’s not overthink this, tmas.

The train’s leaving the station I’ll lock you in right now for 5,000,000 units. Sound fair enough?

7Tx8qTXSakpfaSFjdztPGQ9n2uyT1eUkYz7gYxxopump

7

6

15

377

27 Aug 2025

Fuck you, fuck you all, fuck you higher.

Respect and Pump Praeto, become Assdaqtivists.

I'm an ASS guy and and i hold $assdaq

1

5

57

8 Jul 2025

🚨 NOUVELLE VIDÉO DISPONIBLE ! 🚨

🔥 Regarde la vidéo ici 👉 youtu.be/nT82TqmMzAc

🔗 Et pour toutes les infos, Contactez Praeto sur notre discord.

1

2

2

102